|

Multi-asset or balanced funds can offer a measure of protection against market volatility, which is expected to continue as long as factors such as uncertainty over a possible investment rating downgrade for South Africa, unpredictable Chinese markets and question-marks over the timing of the next interest rate hike from the US Federal Reserve continue to impact on global economic jitters.

This is according to Brian du Plessis, Executive Director at Rezco Asset Management, which recently won two awards at the 2015 Raging Bull Awards. Du Plessis says, “The allure of multi-asset or balanced funds in times of market volatility is that the funds can increase or decrease the exposure of the fund to different asset classes. These asset allocation calls are undertaken by the fund’s portfolio manager. Portfolio managers who do their job correctly manage to reduce the downside that their funds experience but at the same time profit from a significant portion of the upside.” Du Plessis says balanced funds offer a way for investors to not get caught in the hype of the markets. “Balanced funds enable both individual and institutional investors to be invested across various asset classes, and in weightings which the professional portfolio manager feels are optimal given the current market environment. “By investing in a balanced fund, an investor is essentially outsourcing the asset allocation calls to a professional portfolio manager, whose job is to constantly monitor the market and determine the optimal weightings of the various asset classes in the fund’s portfolio. In so doing, the investor is also removing emotion from his investment decision making.” Du Plessis says the last few years have seen large amounts of investor flows into balanced (multi-asset) funds. “Various studies have shown that asset allocation calls are the single biggest driver of alpha, in other words generating returns above a fund’s benchmark.” He clarifies that Rezco’s asset allocation and investment philosophy protects its investors from the down side, while offering upside protection. “Core to what we are trying to achieve at Rezco is to obtain risk-adjusted returns for our clients, by gaining the most return for our clients without exposing their investment to too much risk. “Our investment philosophy is to preserve capital[1] in times of high volatility and to create wealth for our clients when the opportunities present themselves. This is obtained by picking the stocks in the portfolio that participate as much as possible in a bull market, and as little as possible in a bear market. In this way, the Rezco funds are able to preserve our clients’ capital[2] and create wealth.” When selecting a balanced fund, investors should choose funds that have a long-term track record (10 years or more) as well as fund managers with a proven track record of being able to manage money through both bull and bear market cycles. Source: Rezco Please contact Kevin or Thato, email: invest@daberistic.com, for any queries about Rezco investments

0 Comments

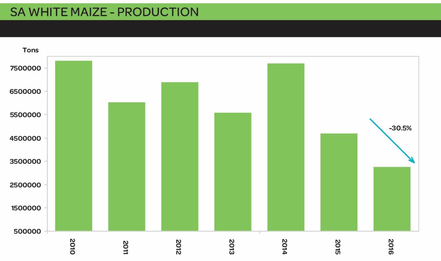

The South African agricultural sector has been in structural decline over the past 50 years. Back in the 1960s the agricultural sector represented around 10% of the South African economy. This fell to 7% in the 1970s, 5.5% in the 1980s, 4% in the 1990s and a mere 2% currently. Part of this decline reflects the systematic development and expansion of other parts of the economy, especially service sectors such a retail and finance. Unfortunately, it also reflects a systematic reduction in the number of farmers as well as a fall in the amount of land used for agricultural purposes. According to the Department of Agriculture, there were an estimated 60 938 commercial farming units in the country in 1996. This fell to 45 818 units in 2002 and 39 666 units in 2007 (latest data available), a total decline of almost 35%. At the same time, the number of people employed in the agricultural sector has dropped from around 922 000 in 1994 to 720 000 at the end of 2013. And in 2012 the value of agricultural imports surpassed the value of agricultural exports for the first time in at least five decades.   The farming sector has been plagued by a number of difficulties over the years, including a shortage of suitable irrigation in some parts of the country, sharp fluctuations in produce prices, an escalation in crime including livestock theft and farmhouse murders, a lack of infrastructure (including export infrastructure), very low wages for many farm workers, erratic weather patterns, and ongoing land claims that have still not yet been fully resolved. This combination of factors has made farming less attractive. Click here to read more

Source: Glacier Please contact Kevin or Thato, email: invest@daberistic.com, if you have any queries about any investing The next tax season opens on 1 July this year and smart investors who file early can look forward to some tax back from SARS later this year. What will you do with you tax refund? Fund your next holiday? Use it as a deposit on a new car, or simply continue to bolster your bank account? While July may still be a long way off, you only have until the end of February to contribute to your retirement annuity and reap the benefits for the current tax year.

What are the benefits of an RA? Firstly, you are increasing the savings pot and financial security available to you at retirement. In addition, under current legislation: • Your RA contributions are tax-deductible (up to an annual limit). • You don’t pay any tax on the capital growth and income while in the fund. • Your retirement savings are protected from creditors. • Your RA is not included in your estate upon death. How much is enough? Your financial planner will guide you in terms of how much you need to save every year to meet your retirement goals. In terms of how much makes sense from a tax perspective, SARS stipulates a set maximum for your total RA contributions for the 2015/16 tax year. You may contribute more, but you will not enjoy tax-deductibility for any amounts exceeding the annual cap. Currently you can enjoy the tax benefit for a total amount up to the greatest of: • 15% of your non-retirement funding income (i.e. the non-PEAR portion on your payslip plus any income from investments and your own business less the deductions allowed on these) • R3 500 less the amount that your payroll administrator has already deducted in terms of any contribution to a pension fund • R1 750 So, if you earned a salary of R500 000 for the year, of which your PEAR (pensionable earnings) were R400 000, and you received no business income or interest that exceeds the annual exemption threshold, you can contribute 15% of the remaining R100 000 non-PEAR earnings of your salary, and that contributions will be considered for a tax refund. (Remember to submit your RA tax certificate.) These limits will change from 1 March 2016, making it possible for you to contribute up to 27.5% of your salary or taxable income (whichever is the greatest) across your employer’s retirement fund and your private RA and enjoy the tax benefits. This is good news for next year! What if you don’t have an RA? It is possible to open an account within a few days. Discuss the options with your financial planner and make sure you understand the total costs involved, as well as the risks attached to the underlying funds in your RA. Source: FA News Please contact Kevin or Thato, email: invest@daberistic.com, if you have any queries about Retirement Annuity The retirement reform amendment, contained in the 2015 Taxation Laws Amendment Act, aims to align retirement funds over the long term. As part of the implementation of the Act, the following changes will be effective from 1 March 2016 1. Harmonisation of provident fund benefitsContributions made to provident funds before 1 March 2016, and all future contributions made by investors who will be 55 or older as at 1 March 2016, will not be affected by the harmonisation of provident fund benefits. At retirement, the full market value of these contributions (the vested benefit) can still be taken as a cash lump sum. Contributions made after 1 March 2016, by investors who will still be younger than 55 as at 1 March 2016 (the non-vested benefit), will now receive the same treatment at retirement as contributions to other retirement products, i.e. the investor will be allowed to take up to a third of the benefit in cash, while the remaining benefit will have to be used to purchase a living or life annuity. 2. Increase in the commutation threshold at retirementThe commutation threshold (de minimis) will increase from R75 000 to R247 500. This means that, if an investor’s non-vested benefit at retirement is less than or equal to R247 500 across all of their accounts in a specific product , the full benefit may be taken in cash. As mentioned above, full withdrawals can be made from vested accounts. The current tax treatment will still apply.The threshold to withdraw from a living annuity will remain unchanged at R50 000 for investors who took a cash portion at retirement, or R75 000 for investors who did not take a cash portion. Clients who wish to make use of the increased de minimis should therefore do so at retirement as it is not currently available in a living annuity. 3. Tax deductions on contributions to retirement annuitiesThe following table summarises the changes to tax deductions on contributions to retirement annuities:

4. Retirement annuity pay outs to non-residents National Treasury is changing the definition of ‘retirement annuity fund’ to allow foreigners who leave South Africa at the end of their working visa or visit to withdraw a lump sum benefit prior to retirement. The supporting documents required by SARS will be copies of the Tax Clearance Certificate, the investor’s passport indicating an exit from South Africa, and the visa showing the date of expiry. The requirements for South African residents who want to withdraw from their retirement annuities due to emigration will remain unchanged. 5. Retirement fund contributions and estate dutyYou may nominate a beneficiary on your retirement annuity. In the event of your death, the money in your retirement annuity account is paid out to your beneficiary, and you do not incur any estate duty (a form of tax). Source: Allan Gray Please contact Kevin or Thato, email: invest@daberistic.com, if you have any queries about retirement funds or Allen Gray offerings Introducing Vitality Gym Tracker – a handy new tool for gym members

Do you ever count up gym visits in your head, trying to figure out if you‘ve gone regularly enough to keep their Vitality gym benefit? No more! Discovery has developed a handy new tool for gym members to help you stay on top of your attendance. Clients can now stay ahead of the game by tracking their gym use The Vitality Gym Tracker enables Virgin Active or Planet Fitness members to view, track and plan gym visits in real time. It will tell them:

Vitality gym members simply need to:

Please note confidentiality rules do apply. As a spouse or additional dependant, gym members will only be able to track their own gym visits. They will not have access to anyone else’s on the policy. NEW online Vitality support page Discovery has set up a Vitality support page on their website for all queries related to fitness devices, apps and achieving Vitality fitness points. Clients can also view their Vitality status, see how many Vitality points they have, and access Vitality Active Rewards FAQs online. You can now take your kids for the NEW Kids Vitality Health Check Your can make sure your children are developing at a healthy rate by booking them for a Kids Vitality Health Check, now available at Clicks and Dis-Chem pharmacies in the Vitality Wellness Network. You’ll also earn 2 500 Vitality points for each child. What the Kids Vitality Health Check includes The Kids Vitality Health Check consists of body mass index (BMI) and blood pressure measurements, as well as a health behaviour and developmental questionnaire. A trained nurse will discuss any health concerns with you and you’ll also get a personalised feedback report after completing the assessment. What you need to know

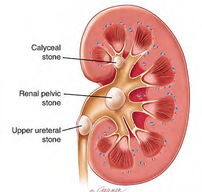

Please contact Namhla or Judy in our Health Department, email health@daberistic.com , if you have any queries about Vitality or Medical Aid Source: Discovery  The Council for Medical Schemes regularly receives enquiries and complaints with regards to unpaid or short paid accounts for the treatment of kidney stones. In this article the CMS provides information on the Condition itself as well as clarity on the Prescribed Minimum Benefits (PMB) for the condition. Let’s look at more information on Kidney stones

What are kidney stones? Kidney stones – also known as renal calculus, renal lithiasis and nephrolithiasis – are included in the PMB regulations. The condition refers to the presence of stones in the kidney. The stones are formed in the urinary tract by crystallisation of substances excreted in the urine.Kidney stones vary in sizes, about 70 to 90% of kidney stones are small enough to travel through the urinary tract and leave the body in the urine without being noticed. However, kidney stones that do cause symptoms have been described as one of the most painful disorders. Causes of kidney stones Kidney stones are formed when the urine does not have the correct balance of fluid and a combination of minerals and acids. Sometimes the natural ability of the body to inhibit the formation of kidney stones is compromised resulting in the formation of kidney stones. Kidney stones may consist of only one of the components mentioned below, but certain kidney stones consist of more than one of the components. It is therefore possible to have a stone that consist of calcium oxalate plus uric acid and sometimes even a third component. Click here to read more Please contact Namhla or Judy in our Health Department, email health@daberistic.com , if you have any queries about Vitality or Medical Aid Source: Medicalschemes Insurance can be a tricky business and it’s probably because of this that there are so many myths floating around about insurance and how it works. Here are some myths explained;

1. My insurance will pay off my vehicle finance if my car is destroyed If your car is financed, you will find that this is not necessarily true. When insurance companies pay for a written-off vehicle, the payment is based on how much the car is worth at the time of the accident. Seeing as your vehicle loan is based on how much your car was worth when you bought it, the insurance amount paid out may not be close to your loan amount because cars generally depreciate quicker over time – faster than the rate at which you are able to pay off your loan. Your loan also includes financing fees and interest, which are not covered by your insurance. Some insurers might offer a top-up insurance policy that can cover most of the shortfall between the insured amount and the loan amount. This is usually optional, so remember to select this cover if you need it. 2. I don’t need insurance Even if you are a fantastic driver or a very conscientious home owner, the fact is that accidents happen and possessions get stolen. Whether an event like this is your fault or not, it could cost you money that you might not have to get your car or home repaired or to replace your stolen items, for example. There are a variety of insurers out there that offer a selection of prices and policies. In fact, getting a quote these days is quite painless and you get to find out just how much you will pay in the end. Everybody needs insurance and very few will be able to afford what they lost without the help of insurance. If you are concerned, but are not sure how to proceed, it’s best to contact a financial adviser who can give you proper advice regarding your insurance needs. 3. My car’s colour will affect my insurance premium Most insurers don’t care about the colour of your car. In fact, they are more interested in knowing whether you’ve had any accidents before, the type of vehicle you have, the car’s age and a variety of other factors. To make sure, ask your insurer if they use the colour of your car to determine your premium. 4. I should get building insurance based on my property’s real estate market value You should get building insurance based on the following:

Source: Discovery Please contact Thomas or Innocentia in our Short Term Department; email shortterm@daberistic.com , to get your personalised car and household insurance quotes. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|