The first month of 2020 proved to be eventful, kicking-off with a fatal US drone strike on Iran that claimed the life of a top-ranking military commander. January also saw the official signing of “Phase one” of the Sino-US trade deal as well as the formal exit of the UK from the European Union. The Wuhan “coronavirus”, however, dominated the headlines and ranked high amongst market concerns, with the World Health Organisation declaring it a “public health emergency” at the back end of the month. Most major markets ended the month lower as investors weighed the impact of the virus on global

growth. On the economic data front, data showed that the US economy grew in-line with expectations over the fourth quarter of 2019 and PCE Inflation (the Fed’s preferred gauge of inflation) rose marginally by 0.2% year on year in December. From a monetary policy perspective, the Fed and the ECB both kept their key policy rates unchanged at their January meetings, and further re-affirmed their commitment to meeting their inflation targets, which by extension implies further support to the economic expansion given the current fundamental backdrop. After a stellar 2019, the MSCI World Index ended the month -0.6% lower. Emerging markets also came under pressure, with the MSCI Emerging Markets Index returning -4.7% for the month on the back of US dollar strength and the risk-off trade as the market fixated on the coronavirus. Most major equity markets ended the month lower, with Japan’s Nikkei 225 (-1.6%), Germany’s FSE DAX (-3.3%) and the UK’s FTSE 100 (-3.8%) all ending the month in negative territory. Asian markets were no exception, with the Shanghai SE Composite ending the month lower (-1.9%). In the US, NASDAQ100 was a standout, ending the month higher (+3.0%) on the back of strong performance from Amazon which reported better than expected quarterly results and joined the likes of Apple, Microsoft and Alphabet in the “trillion-dollar market cap” space. Platinum (+0.7%) and Gold (+4.6%) both finished the month higher, with the latter largely benefiting from its “safe haven asset” status and the former from a continuation in the supply deficit within the PGM complex. The price of Oil (-11.9%) was hardest hit, as markets considered the demand impact of a slowdown in global travel, on the back of the coronavirus outbreak. The US Dollar was broadly stronger for the month, appreciating against the euro (+1.3%) and the pound sterling (+0.5%). It was, however, weaker against the Japanese Yen (-0.3%), which benefits from the “safe haven currency” status in risk-off markets. *All data is sourced from Morningstar Direct as at 31/01/2020. The performance of global asset classes is quoted in US dollars. Source: Morningstar

0 Comments

The year started with a largely risk off tone, as concerns around the Coronavirus and its impact on global economic growth drove investors out of equitie and into perceived safe havens including gold and developed market government bonds. US equities bucked the global trend slightly, with the NASDAQ delivering decent performance, largely due to strong performance from Amazon on the back of a better than expected earnings announcement. The UK finally left the EU on 31 January after years of uncertainty, entering an 11-month period during which it will need to renegotiate new trade agreements with its biggest partners in Europe. South African equities got off to a difficult start to the year, delivering poor performance in lin e with the risk off tone in major equity markets. Local bonds were the best performing local asset class for the month, supported by the largely unexpected interest rate cut by the South African Reserve Bank (SARB) in January. Local listed property continued to struggle, despite the attractive initial yields on offer as the sector continues to be plagued by lower lease escalations and high vacancies. The rand was significantly weaker against most major currencies during the month, which provided support to some of the locally listed rand hedge counters that generate significant earnings in foreign markets. The SARB cut the repo rate in its January meeting from 6.50% to 6.25%, with the Monetary Policy Committee (MPC) citing lower future inflation and growth forecasts. After three consecutive month on month declines, consumer price inflation (CPI) picked up to a year on year figure of 4.0% to the end of December 2019. The JSE All Share Index (-1.7%) finished the month l ower, as disappointing performance from local retail and bank shares weighed on the performance of the index. The weak rand propped up the performance of the Industrials (+1.6%) index, while Resources (-3.5%) and Financials (-5.2%) fared slightly worse. The top performing shares in January amongst the largest 60 companies on the JSE were Reinet Investments (+16.3%), Quilter (+13.5%) and British American Tobacco (+10.9%). The worst performing shares in January were Sasol (-21.2%), Kumba Iron Ore (-16.2%) and AVI (-13.0%). Listed property (-3.1%) had another disappointing month, weighed down by poor local consumer and business sentiment and oversupply in major office and retail areas. Local bonds(+1.2%) delivered decent performance, supported by the attractive yields on offer as well as the interest rate cut announced by the SARB during the month. Cash delivered a stable return of +0.6% for the month. The rand was weaker against most major currencies during the month. The rand depreciated against the US Dollar (-6.8%) the euro (-5.6%) during the month. *All data is sourced from Morningstar Direct as at 31/01/2020. The performance of South African asset classes is quoted in rands. Source: Morningstar  Did you know!

That you can request extended chronic or acute medication when you are travelling out of South Africa for more than a month or up to 6 Months. Discovery Health will review the request only when you need the extra supply of chronic or acute medication because you will be outside the borders of South Africa. The request will be declined if its longer than 6 Months. If you change Medical aid plan, cancel membership or if the membership is suspended during the period for which the extended medication is approved, member will be liable to pay the cost themselves. How to activate this benefit or what you need to do!

Please contact Namhla or Tammy in our Health Department, email health@daberistic.com , for more information regarding chronic benefit. Source: Discovery  While health organisations around the world are fighting the spread of the coronavirus, we would advise you to take note of the basic facts surrounding this new virus. As a Momentum Medical Scheme member, you can call a doctor for free via Hello Doctor, to discuss your symptoms or get more information about any specific questions you may have. Where and when did it all begin? On 31 December 2019, China alerted the World Health Organisation of several patients with flu-like symptoms in a city called Wuhan, the capital of Central China's Hubei province. Initial assessments of these patients ruled out "known" flu-like viruses including bird flu, seasonal flu, severe acute respiratory syndrome (SARS) and Middle East respiratory syndrome (MERS). Once these initial patients were assessed, they were placed into quarantine. The suspected source of the outbreak was identified as a busy seafood market in the city the following day. A few days later Chinese authorities identified the virus, called coronavirus, part of a family of viruses including the common cold, SARS and MERS. The new virus was named 2019-nCoV. What is a coronavirus? Coronaviruses were first discovered in the 1960s and their name comes from their crown or halo-like shape. Their danger lies in their ability to adapt. This means they can easily spread between and infect different species. While some coronaviruses can cause the common cold, others can develop into more serious illnesses that lead to difficulty breathing, pneumonia and death. What are the symptoms? Patients who have contracted the virus have experienced fever, shortness of breath and coughing. The virus can also cause bronchitis and pneumonia, an infection that inflames the air sacs in the lungs and can cause them to fill with fluid. Who is at risk? Those most at risk of contracting the coronavirus include those with cardiopulmonary disease, people with weakened immune systems, infants, and older adults.

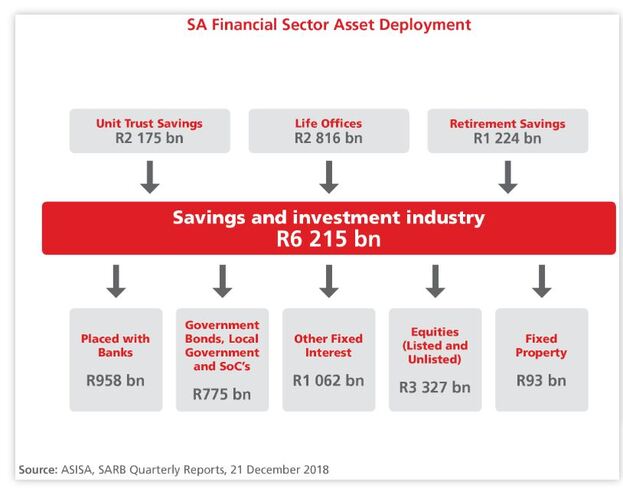

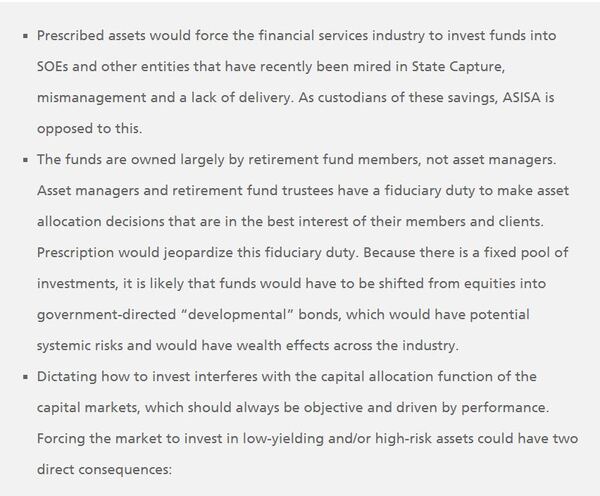

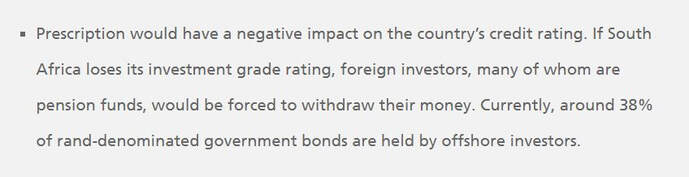

The issue of prescribed assets is one that Prudential is very concerned about due to its potentially negative impact on client returns. As a long-standing member of the Association for Savings and Investment South Africa (ASISA), they have been in full agreement with their approach to addressing the issue with the government, and would like their clients to know that they have been very active in their opposition so far. ASISA is a significant and credible representative for the financial services industry, with members holding savings and investments totalling R6.2 trillion, as shown in the accompanying graph.  ASISA, on behalf of the industry, has held extensive engagements with many parties on the potential negative impacts of prescribed assets, while also offering positive alternatives. These interactions have included directly with government Ministers, via Business Unity South Africa (BUSA) into the National Economic Development and Labour Council (Nedlac) and via the CEO Initiative. Here we unpack the views and research ASISA has been sharing to help clients better understand the issue. What does “prescribed assets” mean? The financial services industry understands prescribed assets to mean the government forcing the industry to buy government-backed assets like bonds and equities using the savings of their clients, including pension funds, life insurance companies and individual investors. These assets could be issued by state-owned entities (SOEs), by stand-alone projects like a highway, power plant or other specific public infrastructure initiative, or by the government directly for “general purposes” like funding transport or water infrastructure. The discussion around prescribed assets arose in the ANC’s 2019 election manifesto, which proposed to “investigate the introduction of prescribed assets on financial institution funds within a regulatory framework for socially productive investments (including housing, infrastructure for social and economic development and township and village economy) and job creation whilst considering the risk profiles of the affected entities”. However, it has not yet been officially tabled as part of any draft legislation or regulation, and hence there is very little detail around what form it would take. Underlying the proposal is the fact that the ANC government has effectively run out of funding options for its many spending priorities, and has identified the country’s pool of private savings (ASISA’s R6.2 trillion,) as a potential new source. Yet the practice of asset prescription is familiar to many South Africans since it was used under the Apartheid government between 1958 and 1989 for essentially the same purposes. What happened under the previous regime? Under the Apartheid government, pension funds, life insurance companies and the Public Investment Corporation (PIC, the manager of the Government Employees Pension Fund) were required to invest from 33% to 75% of their assets in government, government-guaranteed and specified approved bonds, resulting in large distortions in the local bond market. These prescriptions originally served as prudential guidelines, such as today’s Regulation 28. However, the Jacobs Committee of 1988, established to investigate these inefficiencies, found that the prescribed investments eventually came to be regarded as an “assured source of public funding”. As a consequence, we saw the development of a dual market, a lack of trading in the bonds as investors wanted to hold them to maturity, a lack of transparent pricing and underpricing of risk, and most importantly for investors, a resultant underperformance in returns from the prescribed assets: investors weren’t receiving adequate returns for the full risk they were assuming. The Jacobs Committee found that, because investors were forced to invest in prescribed assets rather than better-performing equities – holding far more bonds than would likely have been appropriate for their risk profiles – investors received a real return of 8.6% less than they should have in the 1970’s, and 2.9% less than they should have in the 1980’s. This was a significant opportunity cost to investors. In the face of these negative impacts, the Committee recommended abolition of the practice, which was implemented in the 1989 National Budget. A look at Namibia We only have to look north to Namibia to see the negative impact of prescribed assets on a financial market. The Namibian government instituted a minimum investment requirement in Namibian assets for pension funds, which has recently been increased to 45%. This is explained in more detail in Anthea Agermund’s article, “Regulations skew prices, asset allocation”, in this edition of Consider This. ASISA’s view Given the above, it should be no surprise that ASISA’s stance on prescribed assets is that it did not work under the Apartheid government, and that it would have negative effects on the country should it be introduced now. The primary concern is that the country’s savings becomes an instrument of state policy, and so avoids the investment discipline of financial markets and the fiduciary responsibility of asset managers and trustees, in turn imposing lower-than market returns on investors. Among the main elements of this highlighted by ASISA are the following:  1) The incentive for investment competition would be removed as funding would no longer be incentivized by performance; and 2) Given that capital is a finite resource, deserving or more appropriate projects or assets could be deprived of funding. These projects that would otherwise have driven growth and created sustainable employment would therefore not be funded. For example, think of a company raising capital to expand by issuing shares on the stock market. While this would create more jobs and contribute to economic growth, and pricing would be determined by the market, investors could miss this opportunity and the share issue could fail if they were instead obliged to buy the bonds of infrastructure projects that possibly offered below-market yields, or a risk profile inappropriate for the investor.  ASISA also points to examples of infrastructure project investments in other countries. According to an OECD member country survey, pension fund investments in infrastructure via unlisted equity and debt represent only 1.1% of assets under management. Exceptions include Australia and Canada, where the average infrastructure investment by pension funds is higher.

Financial institutions are willing to invest According to ASISA, the lack of funding for infrastructure projects in South Africa has had more to do with the absence of commercially viable projects than the willingness of financial institutions to fund them. In the past 10 years, the success of numerous public-private partnerships (PPPs) in the financing and construction of South Africa’s renewable energy programme, involving over R200 billion for 112 different projects, shows that this model can work well when the correct conditions are in place. Financial institutions have also indirectly participated in funding public sector spending through their purchases of government and SOE bonds valued at some R1.3 trillion. More recently, ASISA has been actively working with the government to find infrastructure financing solutions for water, energy and student accommodation projects, and is looking at collaborative delivery mechanisms with the government and the Development Bank of Southern Africa for programmatic financing solutions. They are optimistic that many of the country’s challenges can be overcome through effective PPPs going forward, without the need for prescribed assets. At Prudential, we agree with this view and ASISA’s approach in engaging with the government on this important issue. Going forward we will be following developments closely to ensure that our clients’ best interests are protected under any proposed solutions to our developmental financing challenges. To get more information on your investments , contact Kevin in our Investment department, email invest@daberistic.com , tel (011)658-1333  As a most loved local business, your clients rely on you to keep your doors open - even when disaster strikes. Business interruption insurance is designed to protect your business against lost profits should your property be damaged or destroyed by fire or natural disasters like flooding, earthquakes or tornadoes. Here are five must-know facts about this type of cover to safeguard your profits.

1. It’s cover added on to existing business insurance cover In order to have this type of cover, you need to have fire or property business insurance in place. While property insurance covers physical damages, business interruption insurance covers the profits you would have earned if it was business as usual. 2. Must-have for most types of businesses as part of their survival plan Can you imagine keeping up with orders if your most important piece of machinery burns down? Can you fathom having to close your doors for months – while still paying all your staff and bills? After working so hard to build up a fan base, can you imagine them going to your competitors? Most businesses should see business interruption insurance as a must-have survival plan. Work with your broker to plot out your worst-case-scenario and how you would deal with a disaster, especially for:

3. What business interruption insurance covers...and what it doesn’t A business interruption insurance policy will be tailormade to your business operations and turnover, but typically covers the following: Profit: You will receive funds to cover the profits you would have earned during the time you had to close your doors. This sum is based on the income of previous months and the forecast of trends in the future. Temporary relocation: While your premises are being repaired, it will cover costs for you to move to and operate from a temporary location. Fixed operational expenses: Based on historical costs, the policy would cover any expenses and costs that you continue to incur even though you’re not operating. E.g. wages, water, lights. Fines and penalties: Covering costs to service providers including any fines or penalties for being in breach of contract.

4. Accurately calculate your gross profit One of the common pitfalls of business interruption insurance One of the common pitfalls of business interruption insurance - where businesses find themselves underinsured - is when they don’t properly work out their gross profit. Your broker will help you ensure that this amount includes VAT and reflects either a 12-month period (if your maximum indemnity period is 12 months or less) or multiples of the annual turnover (where the maximum indemnity period is more than 12 months). There is a difference between what you know as a Financial Gross Profit, and an Insurance Gross Profit. The latter excludes costs/expenses that vary in direct proportion to a change in turnover. Examples are purchases, bad debts, discounts allowed and direct commission. If, for example, turnover or sales dropped by 10%, so would each of these costs. 5. Work out a sufficient indemnity period Your broker can help you set the right indemnity period for your business. This should allow you enough time to remove damaged property, replan your business (including getting building plan approval), reorder stock and machinery, rebuild your property (including any installations), recover lost markets and restore your turnover to what it would have been had the disaster not happened. Remember, there is no one-size-fits-all approach to getting a business back on its feet. With Santam’s small business insurance solutions, we can help you protect the business you’ve worked so hard for. Speak to your broker to find out more about the essential insurance cover for your unique business needs. If you would like to get a quote for your Business Interruption , please contact Edmond in our Short-Term department, email shortterm@daberistic.com , tel (011)658-1333 Source: Santam |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|