|

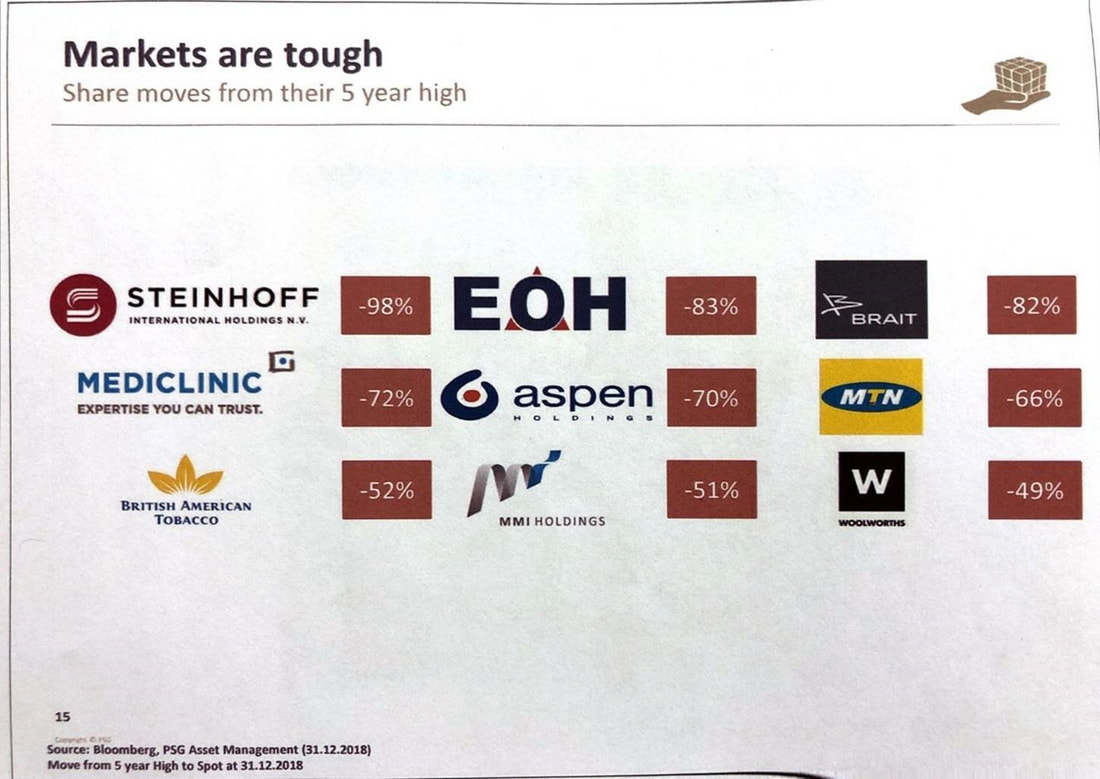

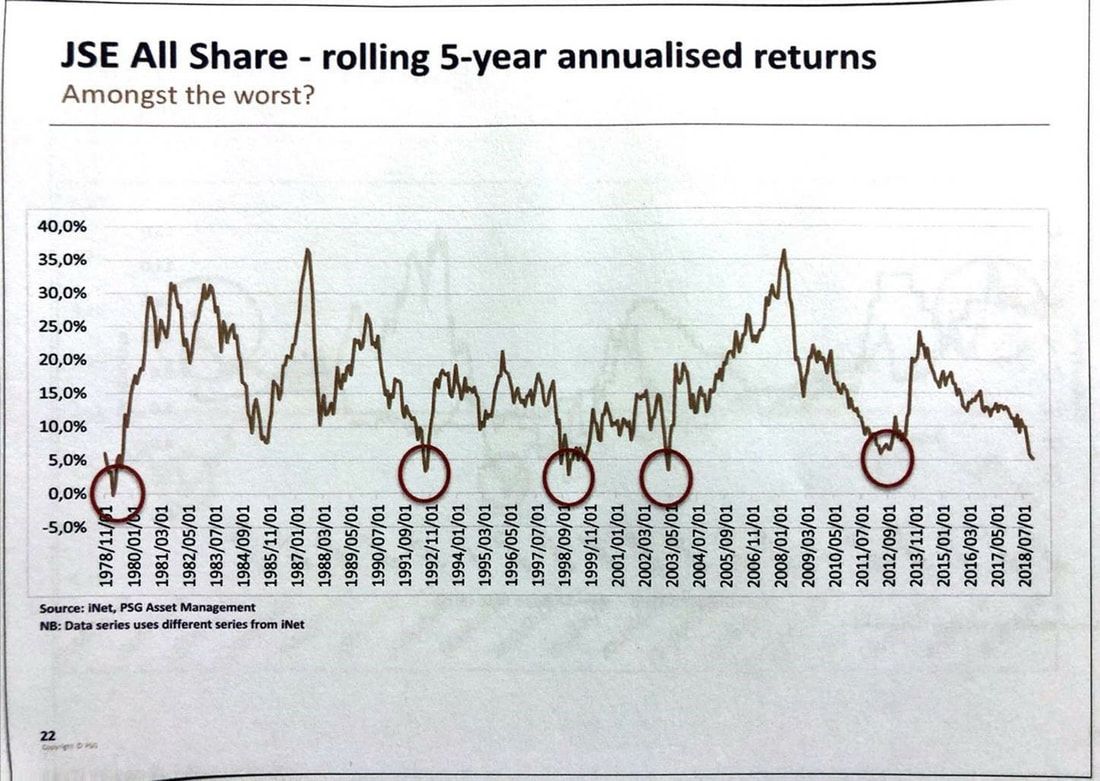

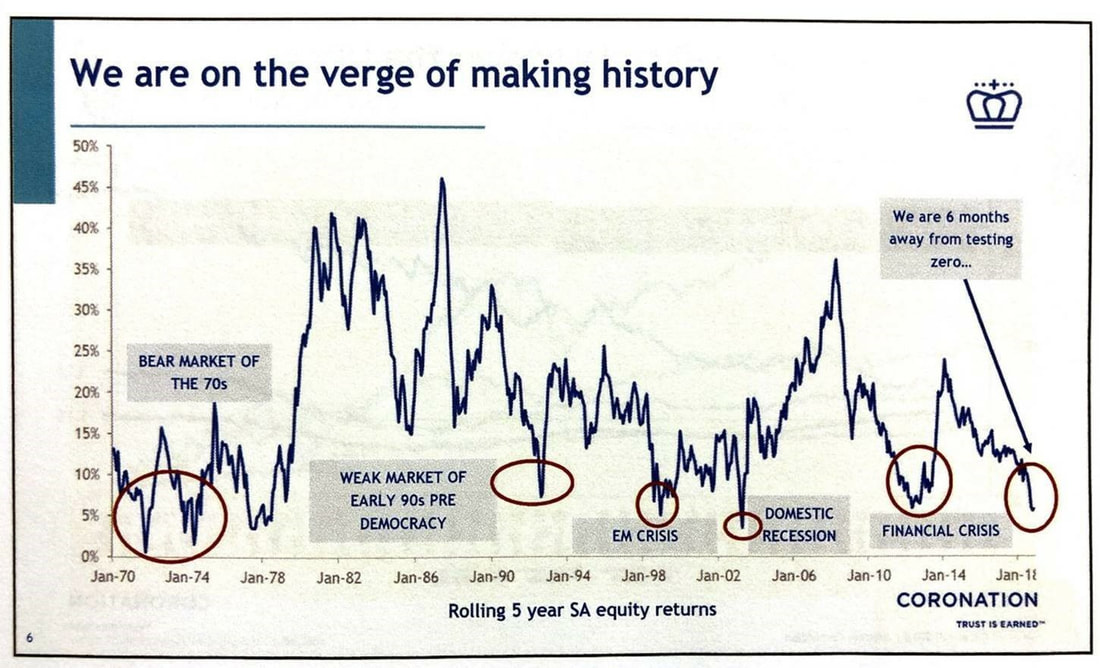

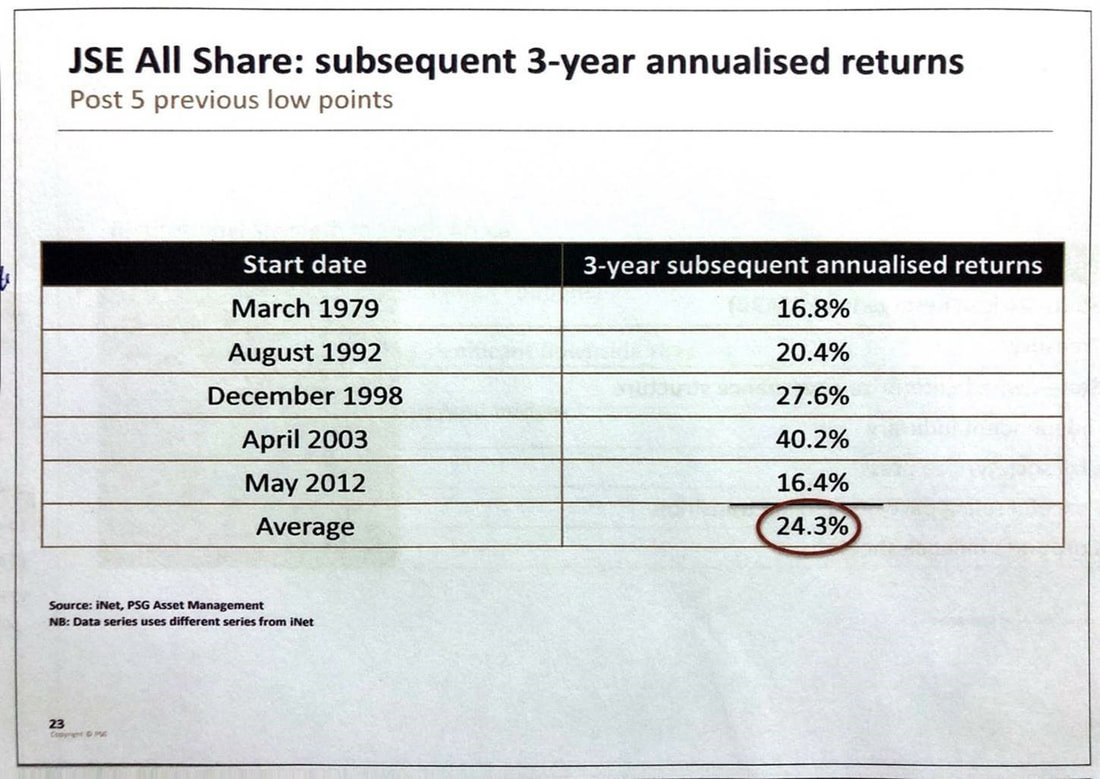

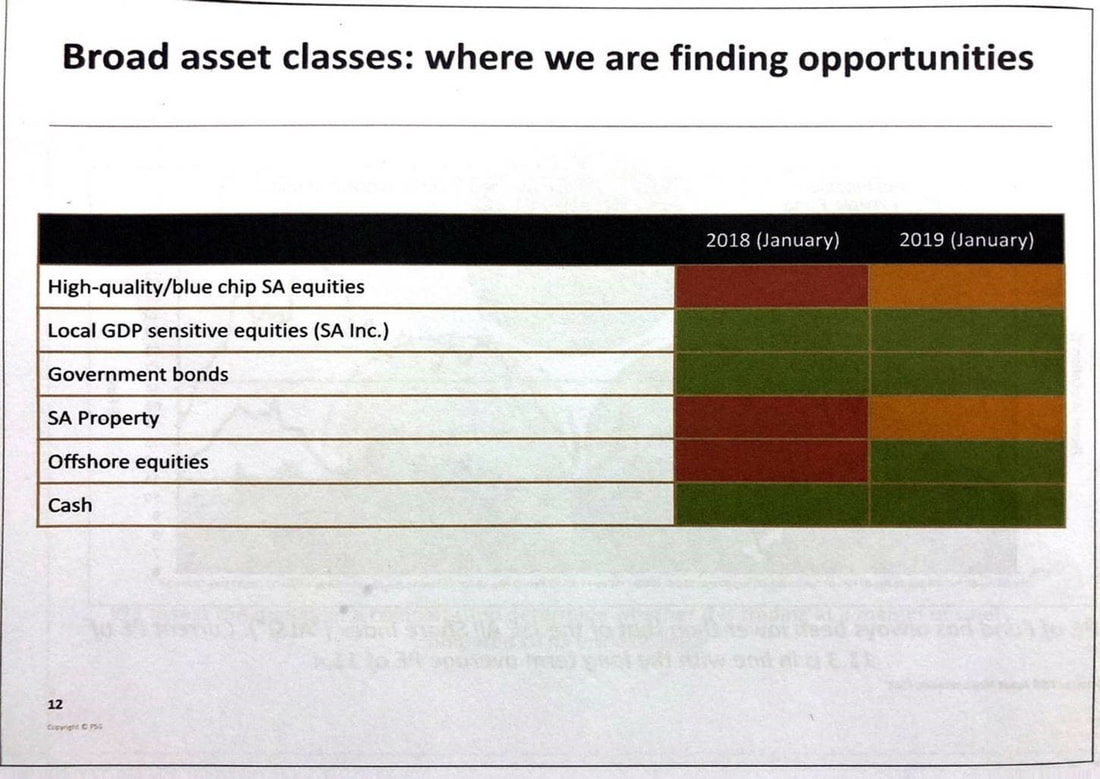

Summary The US-China trade war that began more than a year ago has been hurting the economy and trade of the two largest economies of the world, while also disrupting and re-shuffling the global supply chain. In addition, the United States hiked interest rates four times last year, increasing the rate to 2.25%, attracting funds back to the United States, first hitting emerging markets, and then hitting the US stock market. The US stock market had the second worst rate of return in December in the past 100 years (-7.8%). The South African asset management companies that I rate highly agree that the South African stock market and global emerging markets are at or near historical lows, and many good investment opportunities are found at this stage. We recommended long-term investors to continue to have exposure to growth (stock) assets, which could provide a 60% return over the next three years. *** Global The US-China trade war has been more than a year since the US declared it last year. President Trump of the United States believes that China was competing unfairly. The US trade deficit with China is huge and continues to expand. China infringes on intellectual property rights, as well as providing subsidies to public and private companies. Sanctions include imposing 10% tariffs on imported products from China, lawsuits and measures against ZTE, Huawei and other Chinese telecommunications companies, and containing Chinese companies in the 5G sector. From the recent statistics on Chinese economic growth and import and export volume, China’s exports in February fell by 20.7% from the previous year to US$135 billion, the largest decline since February 2016, indicating that the US-China trade war is having a significant negative impact on China. China's stock market fell 25% in 2018, but since the start of 2019, China's stock market has risen by 25% due to the recovery of global investor confidence and the Chinese government's monetary easing. In 2018, the US stock market was steadily rising, until it experienced a sharp 7.8% drop in December and a 6.1% decline over the year, the first annual negative rate of return since the 2008 global financial crisis. However, it has risen 11.48% since the beginning of this year. South Africa After Cyril Ramaphosa was sworn in as new president at the beginning of last year, there were high expectations from all sectors, which was termed Ramaphoria. However, the US-China trade war, the emerging market currency crisis, the ANC party’s two-faction fighting have caused the high spirits to evaporate quickly. The successive commissions of inquiry have opened up the lid on the rampant corruption and briberies during the Zuma era, so now we know that the National Treasury was hollowed out, and the infrastructure is crumbling. Eskom frequently broadcasts news of mismanagement, energy crisis and implements load shedding, which darkens investor confidence. South Africa’s economic growth rate last year is only 0.8%, and this year is not going to be any better due to the Eskom factor. South Africa's stock market fell 8.5% in 2018, the first annual negative rate of return since the 2008 global financial crisis. If former President Zuma sees the stock market return history, he will brag that, during his presidency, the stock market has risen every year and has never fallen! This is a bit ironic. South Africa's stock market has risen 6.3% since the beginning of this year. The four South African fund managers I rank most highly, based on my long-term observation, analysis and evaluation, agree that 2018 was a tough year for all investors: they lost money no matter where they put their money (except bank deposits and bonds). PSG pointed out that 2018 was a year of trying to avoid landmines:  In 2018, the following well-known listed companies have brought huge losses to investors.  The South African stock market is now near the bottom of the five troughs experienced over the past 40 years.  Coincidentally, Coronation also has the same analysis:  However, they also agreed that 2019 is a year of turnaround. The PSG research report pointed out that the annualized rate of return for the three years after the past five lows was as high as 24.3%, that is, the cumulative rate of return for three years was 92%. Even using the lowest annualized return rate of 16.4%, the investor's 3-year cumulative return would reached nearly 60%. This is the so-called reversion to the mean. Even if the South African economy does not do much, by going from the bottom of a market cycle to the average of a market cycle, with a little boost of investor confidence, the investors could receive this kind of return.  PSG Asset Management is currently positive on the following asset classes (marked by green): South African domestically focused stocks, government bonds, overseas stocks and cash.  Even though 2018 was a disappointing year for investment returns, we recommend investors not to give up on the stock market; continue to hold stock positions in the medium and long term, with exposure to South Africa and offshore markets. Allocate positions in shares, bonds and cash. During this trying time, I chose this pearl of wisdom from Warren Buffett to remind myself and investors:

Now is not the time to give up; it is probably the best investment opportunity since the 2008 global financial crisis.

0 Comments

It's been 22 years since I joined Vitality in 1997. Back then, Vitality was a simple programme with a few benefits like gym membership discount. Over time Vitality has developed remarkably into the comprehensive programme and benefits it is today.

Did you know the great reasons to Join Vitality: • You can get up to 100% savings on your monthly gym fee, Virgin Active or Planet Fitness • You can get up to R1 000 Cash back per family each month for buying Healthyfood at Pick n Pay or Woolworths • Half price movies at ster-kinekor, plus kids watch for free before 7pm • Up to 50% of your fuel spend back, at BP or Shell (Vitalitydrive) • Weekly rewards ranging from coffees and smoothies to dream holidays with Vitality Active Rewards • You can get up to 35% savings when travelling. PLUS save up to 100% on two local flights a year (flight partners are Kulula.com, Emirates, British Airways and Qantas) • You can get up to 50% of your Discovery Life premiums back every five years • Get up to 25% off Uber trips How to increase your Vitality Status Step 1: Complete online health assessments : Complete online health assessments in the ‘Know your health’ section of Vitality’s website at www.discovery.co.za. You can earn as many as 2,500 Vitality points. Step 2: Learn about your health: The next step is to do your Health, Nutrition and Fitness test. You can earn up to 30,000 points. Step 3: Buy Healthy Food: Earn more Vitality points for buying HealthyFood. You can earn a maximum of 1 000 Vitality points every month when you buy HealthyFood from Pick n Pay or Woolworths. You’ll earn up to 20 Vitality points for every HealthyFood product and have 5 Vitality points deducted for every less desirable product you buy. Maximum 12,000 Vitality points a year. Step 4: Get active: Get active in a way that suits you best by attending accredited gyms and using fitness devices. Up to 30,000 Vitality points a year. Step 5: Do further health checks: Have more health checks at your GP or at the Discovery prefer provider. Your family can earn thousands of Vitality points! These are, HIV , cervical cancer vaccination, pap smear, mammogram, prostate screening, glaucoma screening. Contact Tammy or Namhla our Healthcare Consultants to apply for Vitality membership, or get to use your Vitality benefits today: Tel: 011-658-1333 WeChat: daberistic  Author: Edmond Lee

So you recently bought short-term insurance, thinking that you are covered fully regardless of the circumstances? Think again. Many insurance buyers forget that insurance is based on certain fundamentals which must be adhered to in order to have continuous cover. The rationale is that although insurance is a risk transfer mechanism, there is still a responsibility for client to manage risk effectively. Below are some key ones which may be useful to you. Did you know?

Below are some key points that relate specifically to motor insurance:

We at Daberistic believe that by providing the right advice and solution to clients, we can create win-win relationships which will ultimately benefit everyone. If you are looking for advice on your short-term insurance needs, you can contact us on the following channels:

According to a study, 90% of people who retire with money from their retirement funds buy living annuities to provide them with a regular income in retirement. So what are living annuities? And what are life annuities? Are life annuities dead? I would like to explain these two types of products for provision of retirement income. It would be very beneficial for you to generate a more detailed financial plan to give you a better understanding of your options. You can use this tool from 10x. Life annuities and living annuities are the two main products that can provide you with an income from your retirement savings. A life annuity is an insurance-type product and a living annuity is an investment-type product. Each of these meets different needs so you will need to decide which will best meet your particular goals. Life Annuity Life annuity is also called fixed annuity or guaranteed annuity. A life annuity is a contract between you and a life insurance company. You give the life insurance company a retirement capital lump sum. In return, it secures you a pre-determined income for the rest of your life. There are different types of guaranteed annuities. Some provide an income that increases with inflation, others pay a level income and others yet may increase over time, subject to market returns. In order to ensure a level of income that sustains your lifestyle needs, you should consider an inflation-linked life annuity, which provides an income that keeps pace with inflation. Although your income is guaranteed for your whole life, your income ceases when you die. Your heirs won't be able to inherit whatever is left on the death. In other words, the capital dies with the investor. For the sake of guaranteeing value for money, I suggest you purchase a life annuity with an underlying guarantee of income for a minimum period, typically between 10 to 20 years. This period is called a guarantee period. A life annuity with a guarantee period will pay a slightly lower retirement income than one without a guaranteed period. Typically, you also have no say over the initial income and no flexibility to change your income or to move to another annuity or service provider once you've purchased the product. It is wise to use a financial advisor to get quotes from reputable annuity providers, to get the best initial income, terms and conditions. Living annuity On the other hand, a living annuity provides investors with flexibility to choose their income each year (subject to regulatory limits) and where their money is invested. This will give you the flexibility to draw a lower or higher income as and when your needs change. It will provide you with the flexibility to change service providers or purchase a guaranteed annuity at any time. Any remaining capital upon death passes to your heirs. However, in exchange for this flexibility, you take on the risk that the income may not last for your retirement years (on average about 30 years), as well as the risk that their investment returns are poor. This means that your future income could fail to keep up with inflation, or even that you outlive your savings. Below is a table summarising the difference between an inflation-linked guaranteed annuity and a living annuity:

Tax At retirement you may cash in up to 100% of the value of your provident fund, up to one-third of the value of your pension fund, and up to one-third of the value of your retirement annuity. However, there are potentially tax implications to taking a portion in cash. The table below shows you the tax rates for various cash amounts taken at retirement.

In addition to the tax above, the income you receive from either a life or living annuity would be taxed as per the applicable income tax table.

Which one should you buy? There are three possible options: A life annuity, a living annuity, or a combination of the two. Yes, it is possible to deploy your retirement capital to both types of products at the same time. There are two important factors to consider when you buy annuities: Health and flexibility. If you are healthy and your family exhibits a history of longevity, you should consider buying a life annuity with at least part, if not all of your retirement capital, with the balance in a living annuity. People that live longer will score with a life annuity, as they will get (a lot) more than they put in. While the liviing annuity gives you the flexibility to adjust your income as and when your needs change. If you are not healthy, e.g. having chronic conditions such as diabetes, heart conditions, hypertension, you may want to put most, if not all of your retirement capital into a living annuity. This way, you can enjoy the fruits of your years of hard work and savings while still alive, and able to leave the balance to your loved ones when you die. The balance is invested in a life annuity, to provide you with some guaranteed income. With a living annuity, the recommended drawdown rate, the percentage of the capital you draw as income, is 5% per annum. This would ensure the money should last you for up to 30 years in retirement. If you need a higher level of income, you should buy a living annuity, which allows you to withdraw up to 17.5% of your capital as income. Bear in mind that the more you withdraw, the quicker the money in a living annuity runs out. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|