|

Market and Economic summary Global equity markets continued to struggle in February as market jitters around US inflation continued to drag markets lower in the first two weeks of February. As concerns of Russia invading Ukraine became a reality in the third week of February, markets moved into a sharp risk-off trade. This meant that money flowed out of emerging markets (EM), anything Russian or linked to Russia and into perceived safe-haven assets such as US treasuries and gold. This drove bond yields lower towards the end of the month and led to EM currencies weakening. Despite the recovery in developed market bonds towards the end of the month, global bonds ended the month lower. There was little room to hide in global markets in February however the two areas of the market that weathered the storm were global energy and materials.

0 Comments

People sometimes have the perception that insurance quotes are declined for ‘no reason’. However, an insurance policy is a contract. The insurer agrees to cover you according to how much risk they think they take on in doing so and set your premium accordingly. When the provisions aren’t met, the contract has effectively been broken and the insurer is exposed to more risk than ‘what your premium covers’ and ‘what was agreed to’. Beware: In the fine print there might be conditions that could disqualify your claim if not met. The insurance companies are completely within their rights not to cover you – because the contract is not valid anymore. The best course of action is to take care to understand the wording of your policy and to take the stipulations seriously. Story based on actual events, names have been changed to protect identity Rob had his car stolen at a shopping centre. He then contacted us and we registered the claim. The Insurance provider came back and requested the Car tracker logbook. Rob then informed us that his car tracker was cancelled as his policy lapsed due to non-payment. The insurance Company then requested details regarding the cancellation dates, proof of cancellation from tracking company, statements showing non-payment. Ultimately Rob could not provide any of these and later it was found that the tracker policy was under his brother’s name, this then caused the assessor to question “insurable interest” regarding the car. Upon further investigation there were other discrepancies found in the statement and the CCTV footage of the centre where the car was parked was requested for viewing. Ultimately the claim was rejected due to Condition of the policy not being met which is “Tracker is required to be active and working in order to have cover.” There are common pitfalls we see time and time again that result in insurance claims being repudiated, or only partially paid out because the ‘contract’ has been broken. Below are five key examples to look out for: 1.The regular driver and owner of a vehicle differ on a policy An example of where this happens, is if a parent is the policyholder of a vehicle that was purchased for their student child who is the regular driver. The parents have an insurable interest in the vehicle as there is a potential for financial loss if anything happens to it. In addition, if the child is not listed as the regular driver, the claim will likely be rejected and it may have an impact on the parents’ insurance risk profile. What can clients do to avoid this? Update your adviser on the full details of any new vehicle added to a policy, so that appropriate cover can be put in place. Do not assume that simply adding a vehicle to a policy will mean that it is covered. 2. Vehicle extras weren’t specified A case in point was when a client put in a claim for a bulbar that was stolen from his bakkie. No extras were noted in his policy and the sum insured was only sufficient to cover the bakkie itself. The claim was therefore rejected. What can clients do to avoid this? Ensure that all non-factory fitted accessories such as bull bars, sound systems and canopies are specified as additional extras, in addition to the sum insured value of your vehicle. Also keep in mind that you might need cover for mag rims on your tyres, so keep their replacement value in mind – anything you have changed or upgraded compared to the standard vehicle must be noted. 3. Security specifications weren’t adhered to All too common, this is an issue when claiming for a burglary/ theft. If your security features weren’t enabled at the time of the burglary, the claim will likely get rejected. If you tell your insurance company / broker that you have a tracker at the time of taking out the insurance policy it is your responsibility as the client to ensure that this tracking devise must have a valid contract and always be in a working order to prevent problems at claims stage, the client is responsible to ensure that the devise is active and working. If the tracker is no longer active the insurance company needs to be notified ASAP. On high value vehicle this may be a requirement in order to retain insurance cover. What can clients do to avoid this? Make sure you ask about any elements of your cover that are your responsibility. If you are covered for having a locked security gate, vehicle tracking devise, an active electric fence or burglar bars on your windows, these features need to be in place and in good working order at all times. This will keep both your property and you safe. 4. You moved but didn’t say anything to your insurer If you move and don’t notify your insurer of your new address, any claims at the new premises will be rejected. This might seem like an obvious change to make to your policy, but we do experience clients forgetting. What can clients do to avoid this? Insurers usually require that you give written notice of your new permanent, physical address before you move. This is because your new address means your risk has changed and your premium may also change. If you would like us to review your current policy contact Marizka in our Short-term department email; service@daberistic.com tel(011)658-1333 ext 108. Source: Apollotechnical.com, Business Report In this month’s article we share some changing trends in car insurance .

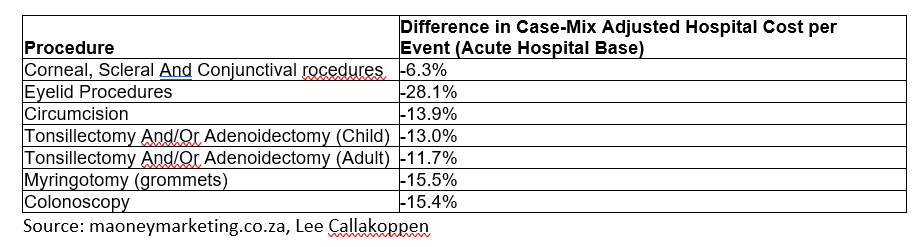

Digital innovation and the pandemic has reshaped how we live, work and drive. Thanks to digital technology, you can benefit from better pricing, claims management, more transparency and more convenience in your insurance experience. And things are only going to improve as new digital innovations come to market. Here are some of the trends we expect to see unfold in car insurance over the year to come: 1.Trends in vehicle ownership and getting about In late 2021, fuel prices reached record highs in most countries. South Africa was no exception; after breaking through the R20 mark for the first time in December, the fuel price keep rising and have hit another record high as oil and gas costs soar amid fears of a global economic shock from Russia's invasion of Ukraine. Petrol prices are climbing, money is tight, and Uber offers a cheap and reliable way to get around if you’re not commuting every day. Following the hard lockdown in 2020, many families are wondering whether they really need two cars in the driveway. Surprisingly with most employees forced to work from home had a better outcome than companies and employees could have hoped for. Productivity, work life balances and the hybrid module worked out so well that many companies and people are not planning a full-time return to the office. Several studies over the past few months show productivity while working remotely from home is better than working in an office setting. On average, those who work from home spend 10 minutes less a day being unproductive, and are 47% more productive. Now that we’re not driving around as much as we used to before the pandemic and rising petrol prices, it’s a good time to rethink car ownership. More and more people are downsizing their second car to a smaller and less costly vehicle, delaying the replacement of their car, or even selling one of their cars because they don’t drive that much anymore. And if you decide not to ditch your second vehicle, you’ll want to get an insurance policy that lets you pay less during the times you’re not driving a lot. Daberistic can help you get the best option. 2. Online car shopping and everything that goes with it According to World Wide Worx, South African ecommerce retail sales totalled R30.2 billion in 2020 – more than double the R14.1 billion achieved in 2018. The explosive growth is largely thanks to Covid and social distancing, together with accelerated investment in the technology that enables ecommerce. Now that people are more comfortable with shopping online for groceries, they’re also more interested in buying larger things like cars and insurance via a website or app. We can expect exciting developments in online car retail in South Africa in the next year or two. We may see online dealers and marketplaces make it simple for you to compare financing offers, vehicles and insurance, then get it all in one place. In future, you could complete a car purchase online, from researching your options and applying for a loan, to ordering the car and getting insurance cover. One of Daberistics’ car insurance consultants can assist you easily online. Perhaps you’ll shop for cars by reading reviews and viewing ultra-high-definition videos, only booking a test drive once you’ve chosen a car and want to confirm your decision. This has the potential to put you in complete control of your experience – car dealers, lenders and insurers will all need to up their game in terms of pricing, convenience and transparency to win your business. 3. Mainstream Digital Insurance While insurance had previously lagged behind many other industries in giving consumers access to convenient digital processes, the last year or two has seen mass adoption of pure online insurance offerings internationally. South Africa has been no exception. With digital insurance providers using automation and self-service to drive down overheads and operate efficiently, the result is a significant cost saving being reflected in sustainably lower premiums. As more customers move online to claim from and manage their cover, we can expect continued innovation to lead the charge on lowering premiums. 4. The amount of data available for telematics vendors will continue to increase. There are ever greater numbers of sensors on cars, and the rise of assistive technology means the amount of data available is increasing rapidly. Telematics has already been introduced to the industry. However, the more data that becomes available, the more insurers can know about how their customers drive. Insurance providers will increasingly leverage telematics technology to better understand who their customers are and how they are driving to more accurately price policies. 5. Need to add credit shortfall New vehicles are exceptionally costly right now due to lack of inventory from supply chain. The costs for car claims is skyrocketing because of the higher new and used car valuations, inflation and supply chain issues. This means there is an increased requirement for people to add credit shortfall on their policy. Credit shortfall cover is , In the event that your vehicle is written-off or stolen, Shortfall Cover will pay the difference between your comprehensive insurance and the outstanding balance you owe to your finance house, ensuring you're never out of pocket. To contact one of our Insurance Broker contact Marizka in our Short-term department email; service@daberistic.com tel(011)658-1333 ext 108. Source: Apollotechnical.com, Business Report  The concept of day hospitals is gaining popularity – particularly because of high hospital stay costs. Day Hospital are there to drive down the cost of procedures affordable. They are also known as Outpatient Surgery Centres which is option of having short stay/day surgical. A day hospital satisfies the patient’s need for a convenient, efficient and lean-cost facility, without compromising on quality clinical care. Advantages of day hospitals 1. No overnight stay – patients are admitted, operated on, and discharged on the same day 2. Child-friendly wards and facilities – day hospitals are the ideal alternative for children requiring same day surgery as the trauma of overnight stays are eliminated. 3. Lower risk of infection – since patients return home on the same day, the risks of cross infection are reduced, which results in a shorter recovery 4. Improved surgery scheduling – decrease in waiting lists 5. More efficient Doctors - Surgeons and anaesthetists are able to plan operating times, thereby increasing their productivity. Internationally there is a trend in increased day surgery for multiple reasons including: • Improved anaesthesia (with quicker recovery period) • Improved pain control (anaesthetic blocks and improved medication) • Instrumentation and procedures (keyhole surgery). Examples of price differences There remains a difference in costs between day and acute hospitals,’ says Callakoppen. The table below represents savings across some of the most prevalent surgeries. Examples of price differences There remains a difference in costs between day and acute hospitals,’ says Callakoppen. The table below represents savings across some of the most prevalent surgeries.  This is probably why the percentage of day cases, split between acute hospitals and day hospitals, is still biased toward acute hospitals. Currently the split of day cases being done in acute hospitals is 74% and 26% in day hospitals. This implies that 74% of all procedures which could be performed in a day hospital are currently performed in acute facilities.

If you would like to know if your option covers for a Day procedure, please contact Jo or Namhla in our Health Department email: service@daberistic.com tel(011)658-1333 In partnership with Morningstar: 2022 has started with no shortage of talking points in financial markets. January proved to be a rather volatile month for global markets, as concerns over persistently elevated inflation prints, potentially higher interest rates and geopolitical tensions (the escalating military conflict between Russia, Ukraine and NATO being the most apparent) weighed on sentiment. In partnership with Morningstar: The Russian invasion of Ukraine is increasingly fluid and potentially harrowing. As investors—not as politicians or news reporters—we thought some perspective on the investing implications from a multi- asset perspective is warranted. In partnership with Morningstar: In recent weeks, markets have been tossed back and forth by speculative headlines regarding the potential for Russia to invade Ukraine. The potential invasion has become a reality with Russia launching their troops into pro-Russian regions in Ukraine. This has led to the S&P 500 falling into a correction for the first time in two years, joining the Nasdaq Composite. (A correction is defined as a drop of more than 10% but not more than 20%.) |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|