South African research shows that 43% of start-up business owners prefer to work from home. But would you be able to claim from your insurer if you are burgled or a fire destroys all your work material? Insurers require that you declare any information that might affect your risk, which is why it’s important to tell your insurance company that you’re running a home-based business.

Your checklist for proper cover Firstly, South African insurers’ definitions for home-based business differ – ask your insurer if you are fully covered under your household content and all risks cover, or if you should apply for commercial insurance cover. Find out if your insurer covers office equipment, laptops and computers at home even if they are used for your business. Household contents insurance does not usually cover software or the loss of data caused by equipment failure. If your business relies on electronic data and software you could consider a commercial policy for the reinstatement of your data. Do you have customers or suppliers who visit your home for business purposes? If so, what will happen if someone gets injured there? You could consider personal liability insurance which will protect you in the event of a lawsuit. Are the contents or your business covered against basic risks such as fire, lightning, explosion; storm, wind, water, hail, snow; an earthquake; and burglaries? Check with your insurer or broker that you have the correct policy in place. An important part of the success of any business is ensuring you’re protected from obvious risks. Evaluating your risk There are a few key areas of risk you need to watch out for. Ask yourself:

How to cover yourself against risks and claims If you answered “yes” to any of the questions above, it might be time to consider specific insurance for your small business. Here are the types of risk and claims you will be covered against:

If you have one or more employees at your home-based business, it is your duty to protect their safety by registering with the government’s Workmen’s Compensation Fund. Employers who pay their annual Workers Compensation fees are protected from being sued by employees who are injured at work, while employees are protected from financial loss. Read all about Workmen’s Compensation on Labour.gov.za. Check up on your insurer Always choose an insurance company that has experience in dealing with big and small businesses. Also, check that the insurer has a good record for claim payments. Santam, for example, paid out 99% of claims made in the past year. Find out if there are other benefits for policy holders, such as a 24/7 claims and emergency service. Source: Santam

0 Comments

Do you think of yourself as a healthy person? If you exercise a few times a week, make mostly positive eating choices, and rarely become seriously ill, you might well consider yourself to be. In fact, the thought of contracting a severe illness has most likely never entered your mind. Until you arrive at work one day to find out that an apparently healthy colleague of the same age as you has just been diagnosed with cancer. And then the realisation hits. There's a chance it could just as easily have happened to you.

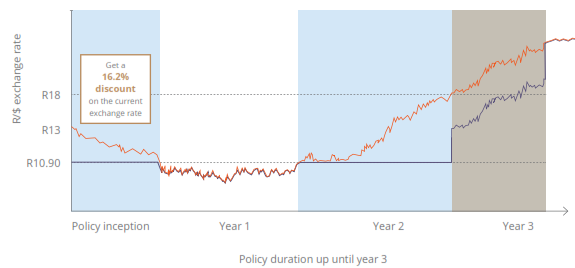

Suddenly you start to consider the possibility that a severe illness could become a reality in your own life. And that protecting yourself and your family against the risk of an illness is more than a nice-to-have it's a must-have in every way. Do I really need severe illness cover? It's a good question and if you're relatively young and in good health, you may think the answer to be a resounding no. But for a more accurate assessment of your potential risk factors, a look at actual statistics might help shed some valuable light. Over the past year, the severe illness claims paid out to Discovery Life clients have painted an interesting picture: On average, 38% of claimants in 2015 were female, while the majority of 62% were male. Of the claims made, a full 51% paid out to females were for cancer-related diseases, compared to 31% for men. While claims made for body systems such as gastrointestinal, ear nose and throat, respiratory, eye and musculoskeletal tended to be evenly paid out between genders, a total of 35% of claims made by men were due to heart and artery conditions, compared to just 8% for women. Finally, claimants between the ages of 41 and 60 were by far in the majority, representing 61% of claims made in 2015, with claimants from 26 to 40 representing only 16%. What these figures clearly indicate is that no matter your gender, age or health profile, severe illness cover always needs to be a priority not for you, then for the continued well-being and support of your family. Cover for severe illness When choosing your level of cover you should consider any outstanding debt and other liabilities that you would have to settle if you were to become severely ill. It is also important to consider the cost of modifications or lifestyle changes that would be required as a result of a severe illness. Please contact Kevin or Thato in our Life Department, email life@daberistic.com, tel (011)658-1333 to get a quote and more information on Severe Illness cover Source: Discovery  What is Gap cover? GAP cover pays YOU the difference between what the doctors charge in hospital and NHRPL, what the medical aid actually pays. The National Health Reference Price List (NHRPL) is a pricing system maintained by the Department of Health and the Council for Medical Schemes. The NHRPL specifies the rates to which your medical aid scheme must adhere. It is the amount of money that they are bound by law to pay out for a given situation. Doctors, hospitals and other medical service providers however, are not bound to these rates, and in fact charge up to 300% above these NHRPL prices. So despite thinking you are financially covered for any medical eventuality in its entirety, for the most part you are not, and are often liable for an enormous shortfall. Gap Cover policies are proving to be an invaluable safety net, as the shortfall between what medical schemes pay and what specialist doctors charge has widened, leaving policy holders with a medical bill big enough to put them back in hospital. To ensure you don’t find yourself with unpaid medical bills contact Namhla in our Health, email health@daberistic.com , tel (011)658-1333 and apply for gap cover Source: Covergap  The R10.90/$1 Life Plan special offer allows clients to pay a guaranteed exchange rate of R10.90/$1 on their Dollar Life Plan for three years! Clients can pay a guaranteed exchange rate of R10.90/$1 on their Dollar Life Plan for three years, and if the exchange rate exceeds R18/$1, a 20% discount on the exchange rate will apply. This offer ends on 31 August 2017. As part of the limited offer, clients are able to pay premiums for a new Dollar Life Plan based on a maximum exchange rate of R10.90/$1 for the first three years of their policy, as long as the R/$ exchange rate is less than R18/$1. This amounts to an exchange rate of up to 39% better than the market exchange rate. If the R/$ exchange rate is higher than or equal to R18/$1 during the first three years of their policy, Dollar Life Plan clients are still able to pay premiums based on an exchange rate that is up to 20% better than the market. If the exchange rate drops below R10.90/$, normal market rates will apply. To sign up for this awesome limited offer, please contact Kevin or Thato, email: invest@daberistic.com tel no: (011 658-1333) Illustration of the preferential exchange rate for Dollar Life Plan clients   Discovery Capital 200+ investment is back for a limited time only

Double capital | Unlimited upside potential | Downside protection If US and European equity markets go up by even as little as 1% over the next five years, you will receive at least double your initial capital at the end of five years. You will also receive unlimited upside potential and conditional downside protection. For more information on this offer you can view the sales flyer here. You can view the fund fact sheet here. Clients who previously invested in this product with Discovery in 2014/2015 are in line to double their investment. Please speak to Kevin Yeh on 011-658-1333, email invest@daberistic.com if you are interested in this investment opportunity.  National Treasury has made some changes to its exchange control policy which will be good news to South African residents who create intellectual property (IP), and who wish to invest offshore, according to Ben Strauss of legal firm Cliffe Dekker Hofmeyr.

Transfer of I "Until now, National Treasury has not been keen on allowing South African residents to 'export' IP. Some years ago, the Supreme Court of Appeal found that exchange control rules do not prohibit residents from transferring IP abroad without the approval of the SA Reserve Bank (SARB)," said Strauss. "However, National Treasury promptly amended the Exchange Control Regulations to include IP under the definition of 'capital' in an attempt to again bring IP transactions under its control." The 2017 Budget Review that National Treasury issued in February 2017 states that government proposes that companies and individuals no longer need SARB’s approval for standard intellectual property transactions. It is also proposed that the "loop structure" restriction for all intellectual property transactions be lifted, provided they are at arms-length and at a fair market price. Loop structure restrictions prohibit residents from holding any South African asset indirectly through a non-resident entity. In terms of a subsequent IP Circular by SARB, authorised dealers may now approve the outright sale, transfer and assignment of IP by South African residents to unrelated non-resident parties at an arm’s length and a fair and market related price. So, approval from SARB is no longer required. Strauss cautioned about certain aspects: - The authorised dealers must view the sale, transfer or assignment agreement; - The authorised dealers must view an auditor’s letter or IP valuation certificate confirming the basis for calculating the royalty or licence fee; - The transferors may not transfer the IP offshore and then license it back into SA; - The person transferring the IP must repatriate the funds arising from the transaction to SA within a period of 30 days from accrual; - The transaction is subject to appropriate tax treatment. "The relaxations on the transfer of IP should be welcomed. However, there is still much red tape: the transferor must obtain an auditor’s letter or IP valuation supporting the price. Obtaining such a certificate or valuation will potentially be a costly and time-consuming exercise," explained Strauss. Exchange traded funds There was also good news for South African resident investors and financial services providers in the 2017 Budget Review. Regulated local collective investment scheme management companies may now list exchange traded funds (ETFs) which relate to offshore assets on South African securities exchanges. These funds will be able to invest as much as they like offshore, subject to the restrictions on their offshore portfolio allowances. The funds will still have to obtain prior written SARB approval to list. Local individuals will be able to invest as much as they want in these funds in South Africa. The investments should not count towards their foreign capital allowances. To get recommendations on offshore investment options, please contact Kevin or Thato, email: invest@daberistic.com tel no: (011 658-1333) Source: Finance24  Tax free savings is an investment option if you are investing for the long term, or if you are already paying income or capital gains tax on your existing investments, you can invest in unit trusts via our tax-free investment account and benefit from tax savings on your investment return. It is also a useful product for estate planning purposes.

How it works

To get a quote for a Tax free policy, please contact Kevin or Thato, email: invest@daberistic.com tel no: (011 658-1333) Source: SARS |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|