Last month I talked about Step 2 - Do Not Spend More Than You Earn. Let's continue with Step 3 - Do Not Take On Credit.

South Africa is a westernised economy, its financial system is modelled on the European and American credit system. If you have a steady income and a good credit score, it is easy for you to get credit. Credit is generally defined as a contractual agreement in which a borrower receives something of value now and agrees to repay the lender at a later date—generally with interest. Simply put, when you buy something now and pay it later, you are using credit. Examples are when you use your credit card to buy furniture and TV and put it on budget over 12 months. Based on your income and good credit score, the banks will want you to apply for credit card and give you a credit limit. As you manage the card well, pay the amount due in time, and your income rises, the banks determine that you are creditworthy and increase your credit limit. The banks advertise that the advantage of a credit card is you can get 55 days free of interest, that is the maximum interest-free period you can get. When you receive your monthly credit card statement (by now most banks send the statements electronically), you need to pay attention to: credit limit - the amount granted to you by the bank closing balance - the amount you owe on the credit card at statement date minimum amount due - the minimum amount you need to pay the bank payment date - the date by which you need the pay the bank It is very important to note: IF YOU DON"T PAY THE FULL BALANCE DUE BY THE PAYMENT DATE, YOU WILL PAY INTEREST Many clients I have consulted don't understand this, and they think it's OK to pay interest on their credit card, as they only pay the minimum amount due. But this is not OK! This is poor financial behaviour. Financially smart people understand how credit cards work. They use credit cards to their advantage. They buy things on credit. They pay the full closing balance on or before the Payment Date. They don't pay interest on their credit cards. You need to inspect your credit card statements for the last three to six months. If you pay interest every month, then you need to reset. Reduce or stop spending using your credit card, work on paying off the full balance. Once you have done that, then you get into the habit of paying the full balance by the payment date every month. Set up a reminder or have an automatic debit order to settle the balance. Remember, the amount you owe on your credit card, to you it is credit card debt. To the bank it is credit card asset. It is an asset because they earn interest from you. Currently the banks charge you between 12% to 18% interest on your credit card debt. That's a lot of interest to pay! You don't even earn this kind of return on your long-term investments. Stop giving more money to the bank than you need to! Rather keep that money in your pocket. I have some rules for credit cards, which I advise my clients to follow:

Don't take on credit, it means you get into debt. Apart from financing high-value items such as a property, a car, business or study loans, you should not take on credit.

0 Comments

Discovery Health shares notes to guide clients on the steps to take in registering on the necessary portals for your vaccination journey. As part of the national vaccination programme, the National Department of Health’s Electronic Vaccination Data System (EVDS) is imminently expected to open to the public. What do you need to do? Everyone in South Africa who wishes to receive the COVID-19 vaccination must register on the National Department of Health’s EVDS. This registration process will be communicated and managed by the National Department of Health. You will have access to additional functionality and tailored support through the Discovery COVID-19 Vaccination Portal. Guidance about this portal and how to register with us will be sent to you next week. Why should you register with both systems?

Registration for citizens 60 years and above opens at 16.00 on Friday, 16 April 2021. EVDS registration guideline and who must resgister All Healthcare workers (public & private), citizens 60 years and above or persons under 18 with co-mobilities whom intend to be vaccinated in Phase 1 and 2 must enroll on the Electronic Vaccination Data System (EVDS). Please click on the below button to take you to Government's EVDS Self Registration Portal User Manual. Source: Discovery Health

With healthcare costs growing at an average of 8-10% each year, beyond inflation, which leaves medical aid clients with little choice but to downgrade their scheme benefit options to manage their cost of living. The downgrade of scheme option results in less benefits covered. This is often met with an unexpected and unaffordable bill after consultation or procedures. This has given Gap cover insurance critical spotlight to ensure medical aid clients are not faced with exorbitant amount of out-of-pocket expenses. Gap cover pays the client back policy which provides shortfall cover where doctors and specialists charge above medical aid rates of cover. Gap cover works in conjunction with your medical aid. Gap cover cannot provide cover where medical aid does not pay towards a procedure or covers the full amount for a procedure. For example, if your medical scheme option only pays out at 100% of scheme rate, you will then be liable to pay the shortfall of the other 200% to 400% charged by your healthcare provider as an “out of pocket” expense. Here is a testimonial of one of our clients Mrs K I gave birth in a private hospital in Johannesburg. The hospital bill was R15,000, Doctor’s bill was R14,500 and the anaesthesiologist R4000. Medical Aid made the following payments:

I had to pay the shortfall of R9,000 and luckily, I was able to claim from my Sirago gap cover and got my R9,000 back. *Please note we changed the name to keep identity private Gap cover may cover the following instances:

At Daberistic, our preferred provider is Sirago. Why Choose Sirago?

2021 Sirago Gap Cover Premium  To apply for Gap cover contact Tammy in our Health department, email service@daberistic.com, Tel 011-6581333, Option 2 for Medical Aid.

Discovery Insure is celebrating 10 years of bringing clients the very best in innovative and rewarding car and home insurance. Now Discovery Insure is bringing more rich enhancements to clients, while continuing to reward clients for driving less and driving well. These enhancements include benefits to protect the whole family, such as updates to our car seat benefit, a unique safety feature, new tools for driving safely, and more. 1. Keeping our children safe on the road with enhanced car seat discounts. Having the correct car seat can significantly reduce your child's risk of injury or fatality if you are involved in a vehicle accident. Discovery has DOUBLED the discounts on car seats from partners: Toys R Us and Born Fabulous. Vitality Drive clients can get up to 50% off car seats, based on their Vitality Drive status. In addition, you will also have access to a wider range of car seats, making child safety on the roads much more accessible. There is also an extension on the benefit to give clients the opportunity to replace a damaged car seat in the event of a motor vehicle accident at no additional cost The increased discount is available from June 2021 onwards. The car seat replacement benefit will be available in 2021, quarter 3. Read more about the car seat benefit and how to redeem your voucher. 2. The Discovery Insure Driving Academy Being at the forefront of innovation and technology, the Discovery Driving Academy places the driver in an artificial environment which is designed to mimic an actual driving experience. The simulator itself mimics a real car and includes an accelerator, brake, clutch, gearbox, indicators and windscreen wipers. The Discovery Driving Academy allows drivers to have:

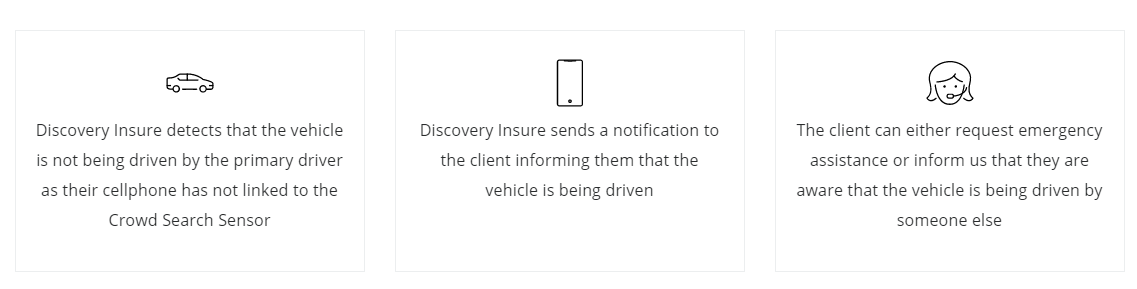

Courses available The Discovery Driving Academy is available to all members of the public. Discovery clients get 25% off the course fees but as a Discovery Insure client, you get a 50% discount. Other courses for other levels of experience will soon be added. The Driving Academy can be found at 1 Discovery Place, and will be available from April 2021. Bookings we will be available on the Discovery website. 3. Additional protection with Motion Alert for the Crowd Search Sensor Vitality Drive clients automatically have access to state-of-the-art safety features. The Crowd Search Sensor now offers an additional layer of protection using new telematics technology. How it works Motion Alert uses the latest telematics technology to identify when your phone is not in the vehicle at the time that the vehicle is moving, thus alerting you to possible theft of your vehicle.  4. New services with Vitality Drive Vitality Drive is Discovery Insure's unique driver behaviour programme that rewards you for driving well. In order to help you manage your driving behaviour even better, Discovery has upgraded the monthly Vitality Drive performance dashboard effective from May 2021. What's new on your Dashboard? You will be able to view:

At the Drive Centres, you can:

Keep an eye out for your new personalised Dashboardand visit www.discovery.co.za to find the location of the Discovery Drive Centre closest to you. 5. Upgrade to the latest Apple or Samsung cellphone every year With our Purple Plan, you can upgrade to the latest Apple or Samsung cellphone every year! We are excited to announce that we have a brand new partnership with Cellucity in addition to our partnership with iStore. To qualify for the cellphone upgrade, you must have:

If you qualify, email the Discovery Insure Partners team at dipartners@discovery.co.za and Discovery Insure will provide you with a voucher of R10 000 which you can use at any iStore or Cellucity. You will need to pay any amounts that are more than the R10 000. If you choose to trade in your existing cellphone, it will contribute towards the cost of the new cellphone. We are excited to give you this update and we are sure that you will get great value from it. Get more information about Discovery Insure's Purple Plan cellphone upgrade benefit. 6. Keeping your personal information safe As a valued client we would like to make sure you experience the best service, stay informed and have access to all the information pertaining to your insurance plan. This is why we are gradually changing the way we communicate with you in accordance with the POPI Act. Going forward, all communication that contains personal information will be accessed via a secure log in on the website or on the app. Follow this guide on your personal information to make sure you have updated your contact details and security settings on the website and mobile app. Source: Discovery Insure

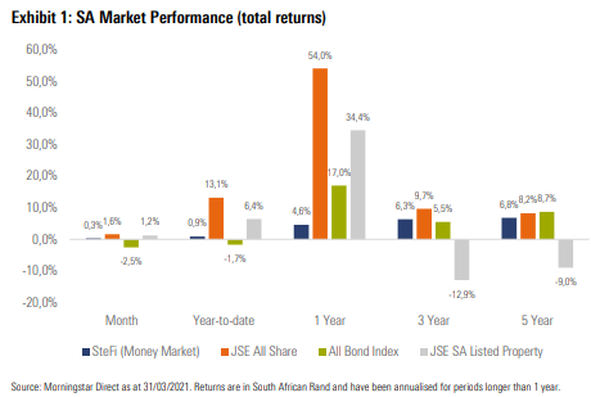

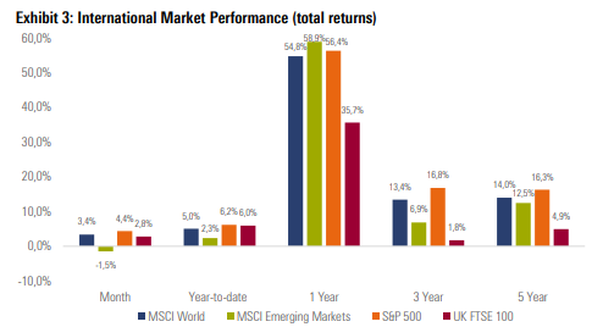

South African Market Update South African equities ended higher for a fifth consecutive month, with positive performance across all three major local equity sectors. Local bonds ended the month lower, despite positive news on lower-than-expected inflation, a reduction in government bond auctions, a lower-than-expected budget deficit and a stronger rand. The weak performance from bonds was largely driven by SA yields drifting higher (moving prices lower) in reaction to movements in global bond markets. Local listed property ended the month higher, however, weak performance from some of the larger counters including Growthpoint and Redefine led to muted returns from the SA Listed Property Index. The rand was stronger against most major developed market currencies, despite weakening significantly against the US dollar at the beginning of March, only to recover the lost ground towards the end of the month. South African Economic Update The South African Reserve Bank’s Monetary Policy Committee (MPC) announced during the month that it will leave the repo rate unchanged at 3.5%. This was the fourth consecutive meeting where the MPC decided to leave the rate unchanged, however, unlike recent meetings, the decision was unanimous, with all five members voting to keep rates on hold. Available data for Q1 2021 appears to indicate a slow start to the year for economic growth, which can largely be attributed to the introduction of adjusted level 3 lockdown restrictions during January in reaction to the second Covid-19 wave in the country. SA headline CPI moved lower to a year-on-year figure of 2.9% for February (from 3.2% in January). This was only the third time in over a decade that year-on-year inflation has fallen below the bottom end of the target band and was largely driven by the contribution of lower medical insurance costs.  Global Market and Economic Update Most major global equity markets ended the month with positive returns, as economic data reflecting the recovery from the Covid-19 pandemic continued to surprise on the upside. Equity investors continue to remain bullish, with another US stimulus package on the horizon, despite concerns around a ship stuck in the Suez Canal, which disrupted a major global shipping route for a few days during the month. March was dominated by market participants taking note of movements in global bond markets, as yields continued to move higher (moving prices lower), led by US Treasuries, as global bonds ended the quarter with their worst return in decades. The uptick in global bond yields appears to be connected to inflation expectations, with fixed income markets pricing in higher inflation in the medium term, which is likely to lead to interest rate increases from the US Federal Reserve (Fed). This, despite the Fed’s insistence that they will continue to keep monetary policy accommodative as the US economy continues its recovery from the shock of the Covid-19 pandemic.  Source: Morningstar

Hi everyone, this is Uncle Kevin. Today I would like to encourage you to start investing today.

Have you developed a savings habit? Are you saving money every month? Do you know that by consistently investing money every month, you are going to reap the rewards in the long term? Investing is not a short-term game like a 100 metre sprint, but rather a long-term game like a 42km marathon. I would like to use two real-life client examples to demonstrate how you will reap rewards in the long run. Zane is now 43 years old. 10 years ago when he was 33, he had a financial planning meeting with me. He wanted to invest for his child's education. At that time I advised him to take up a Discovery Invest Endowment Plan, R1,000 per month, with the contribution increasing at CPI inflation rate every year. He started the investment on the 1st of April 2011. He has continued with the investment plan without fail. In year 10, his monthly contribution was R1,639. Now 10 years later, at the beginning of April 2021, the investment plan value, after deducting income tax, is R 223,691. The internal rate of return, IRR is 8.39%. Now internal rate of return is the net return received by the investor, net of fees, charges and taxes. So over the 10-year period, Zane has received on average 8.39% return per annum. Which is a good return. The second client, Ken is now 49 years ago. 10 years ago when he was 39, he also had a financial planning meeting with me about the same time, and he wanted to invest for long-term. At that time I advised him to take up a Discovery Invest Endowment Plan, R1,000 per month, with the contribution increasing at CPI inflation rate every year. In year 10, his monthly contribution was R1,639. Now 10 years later, at the beginning of April 2021, the investment plan value, after deducting income tax, is R202,116. The internal rate of return, IRR is 7.13%. There are 3 points I would like to focus on:

Use this link to book a FREE Financial Planning session with Kevin, using Microsoft Teams Online Meeting: https://calendly.com/daberisti... |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|