|

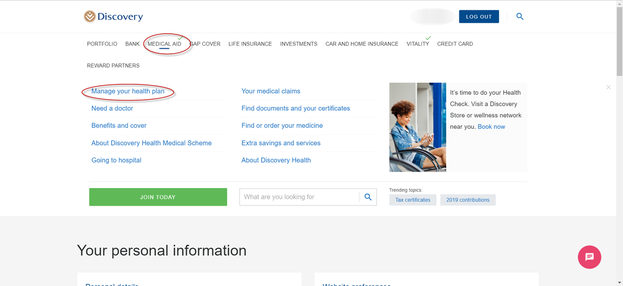

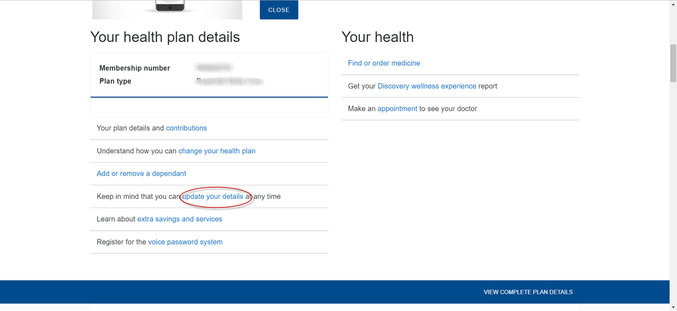

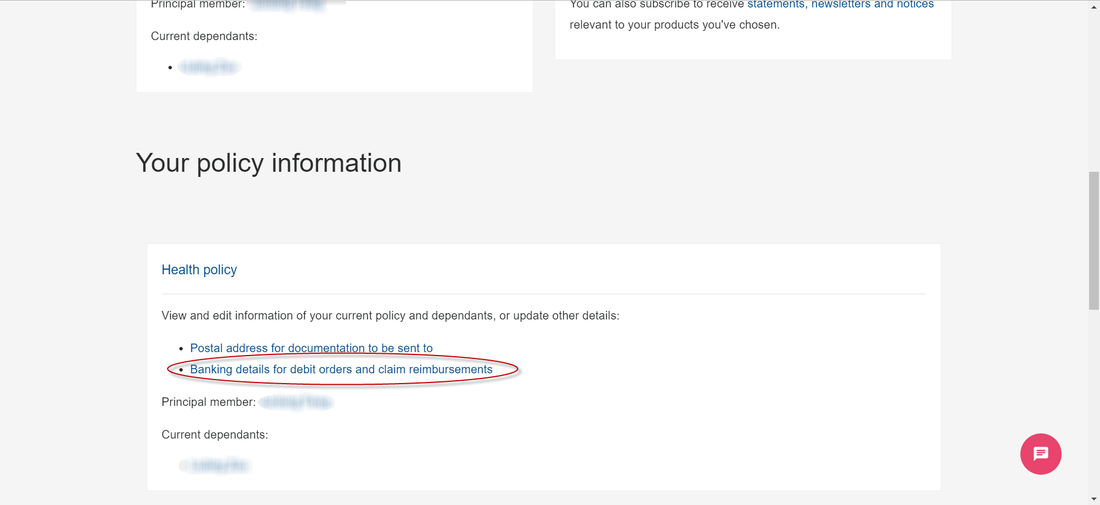

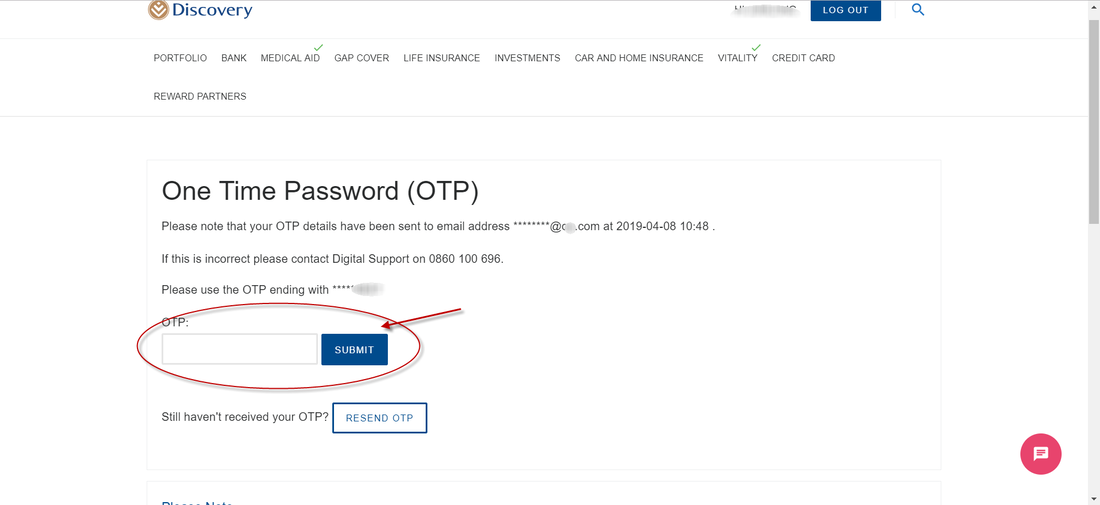

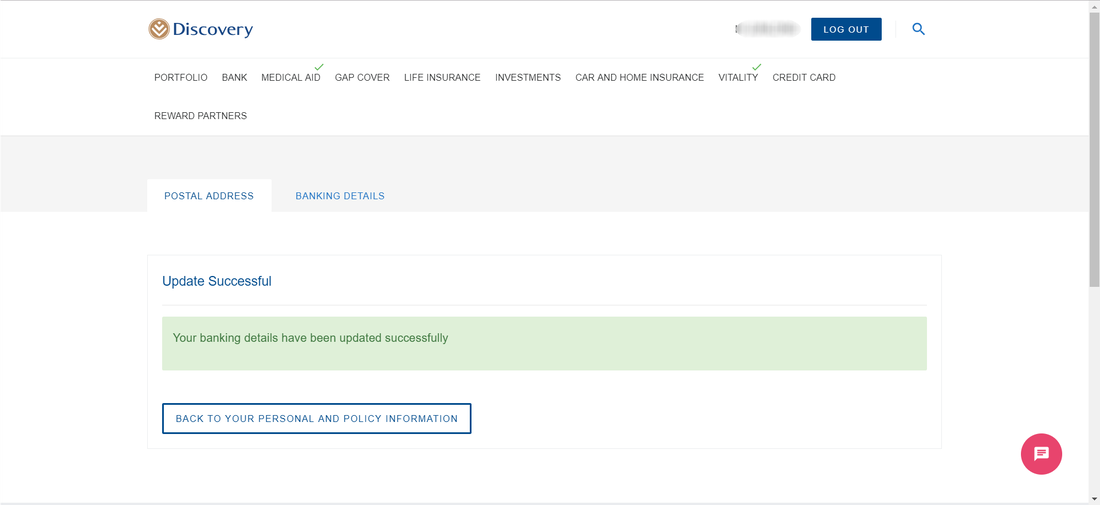

Many people may have failed to get insurance premiums because of changes to their bank accounts or problems with their bank accounts, resulting in temporary suspension of medical insurance. Beginning in 2019, Discovery has changed its online information to online instead of submitting changes in writing. The advantage of changing bank information online is: no waiting time! The system of the insurance company will be updated immediately after the change. Note: Bank information can be changed only on the system of the principal. Here are the steps to update online: Step 1: After logging in to the website, click on "manage your health plan" under Medical Insurance.  Step 2: Update your profile  Step 3: Click to change bank information  Step 4: At this time, the insurance company will send a verification code to your mobile phone or email address, fill in the verification code, and click Send.  Step 5: At this time, you will enter the page for changing the bank account. The insurance company may send a confirmation request to your mobile phone. Please select the account to change the bank account on the mobile phone. The first one is the banking account. ), the second is the banking details for debit order, please make sure to change the part that needs to be changed, and finally click to send it. Step 6: After the change is successful, the following screen will appear  For any queries please contact Namhla or Tammy in our health and wellness department email :health@daberistic.com tel no: (011) 658 - 1333

0 Comments

In this month’s article, we focus on a question which our client often asks us: why is my claim taking so long? We will provide insights into the claims process and some of the key factors that affect the its duration.

With “Nowism” being an integral part of our lives - where people want things now more than ever - many clients often get frustrated with the claims process which can be a lengthy one, due to the multiple stakeholders and steps involved. Although its intention is to ensure that the claim is settled in the most fair and reasonable manner for both clients and insurers alike, the clients are often not aware of the continuous effort happening in the background while the clock ticks away. To explain why the claims process takes long, let’s use motor repair claim as an example. Firstly, it is important to acknowledge that there are many stakeholders involved in a motor claim, namely client, broker, third party, police, claims handler, assessor, repairer, parts supplier, and quality assurer. At times, an investigator may also be involved if the insurer wants additional verification to be done. Due to this, a few days here, a few days there, the claims process becomes an inherently long process. Secondly, there are various due diligence in place. For example, a damage assessment is done by an independent assessor to check for all damages on the vehicle, after which an assessment report is sent to an insurer in three to five days. The insurer would then proceed to authorise the claim after they are satisfied with all the information at hand from various parties, including the clients themselves. If needed, the insurer may request the assessor to review certain aspects to ensure that all damages and repair values are accurate. Once authorisation is granted, the repairer would then proceed to order parts and start the repair process. The repairer strips the car and conducts a more thorough review, and more often than not, the repairer would find other damages which mean they need further authorisation from the insurer before any additional repair can be conducted. Thirdly, the duration of the repair depends on parts availability as well. For more popular brands such as Toyota and Volkswagen, parts are more readily available, but for other cars or models that require imported parts, it may take up to three weeks just to get the parts. The repair usually takes about one to two weeks for minor repairs, and two to eight weeks for major repairs. This process is technical in nature and involves various steps and divisions, such as panel beating, fitment, spray painting and quality assurance – all of which are done to ensure that the car is restored to its previous glory. In this regard, the insurer carefully screens and selects their approved repairers to provide peace of mind to the client. In certain cases, the insurers also send their own quality assurers to ensure that the repairs are indeed done to the approved specifications. The above outlines the reason behind a lengthy motor repair process. For a write-off and other losses, the process and stakeholders are very different, but the underlying principle remains the same. Although many people believe that insurers use different tactics to delay a claim, insurers actually want to settle claims as quickly as possible, because there are additional costs involved (many of them are outside of the insurers’ control) when claims take longer than expected. Hence we always advise our clients to include 60-day car hire as part of their cover, so that they are in no way inconvenienced by the claims process. We at Daberistic believe that by providing the right advice and solution to clients, we can create win-win relationships which will ultimately benefit everyone. If you are looking for advice on your short-term insurance needs, you can contact us on the following channels: -WeChat: daberistic -Email: ShortTerm@Daberistic.com -Phone: 011 658 1333  outh Africa has a relatively small equities market with a handful of dominant shares, spread across a few sectors, which are available to invest in. This presents a significant risk for investors: a highly concentrated portfolio.

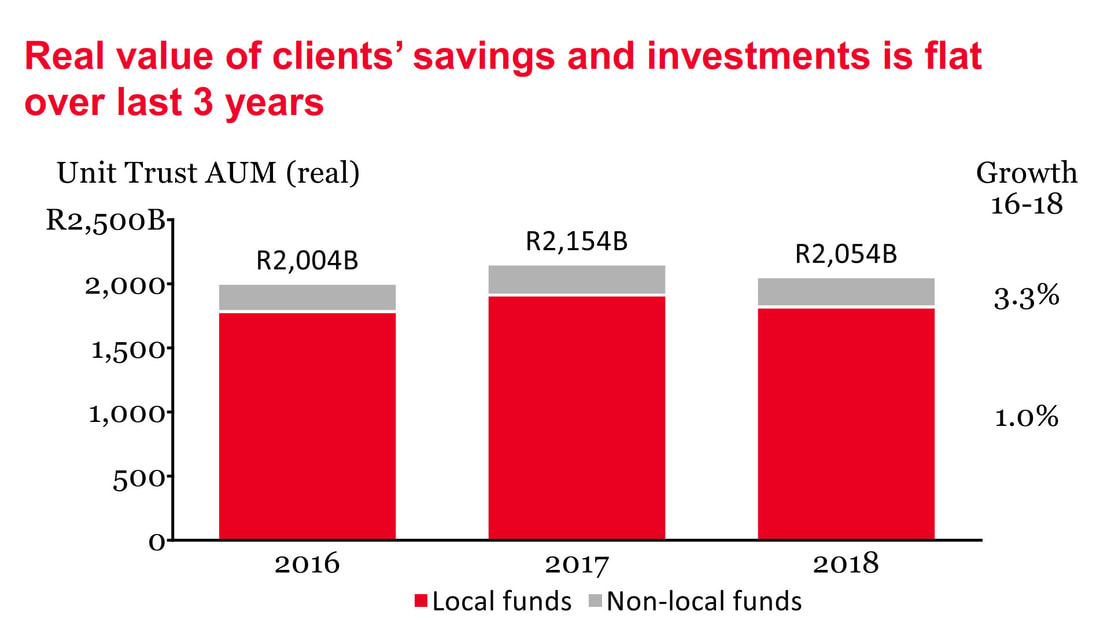

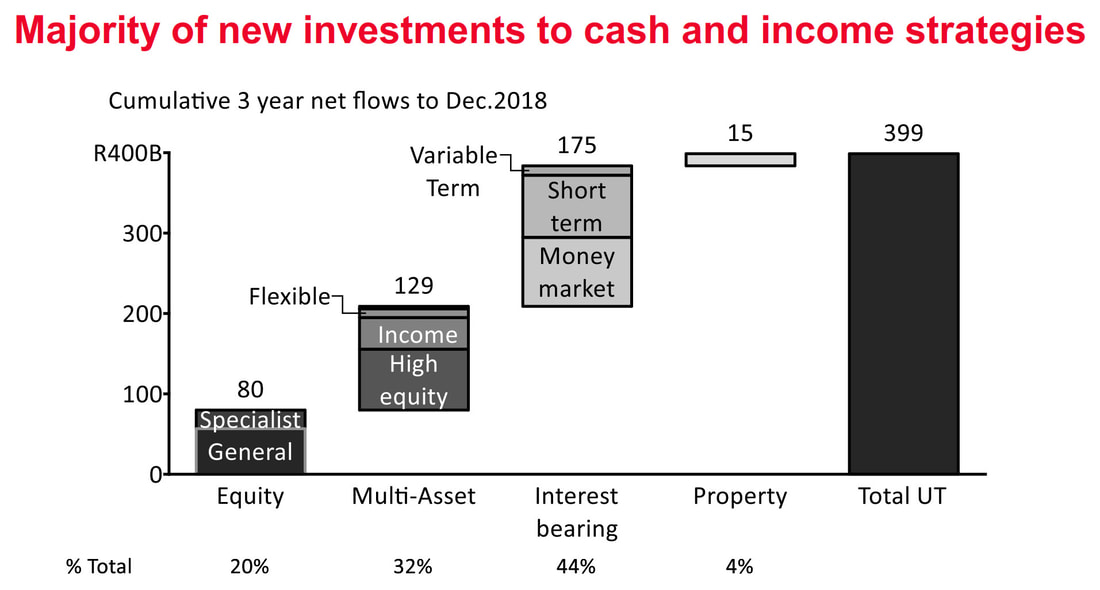

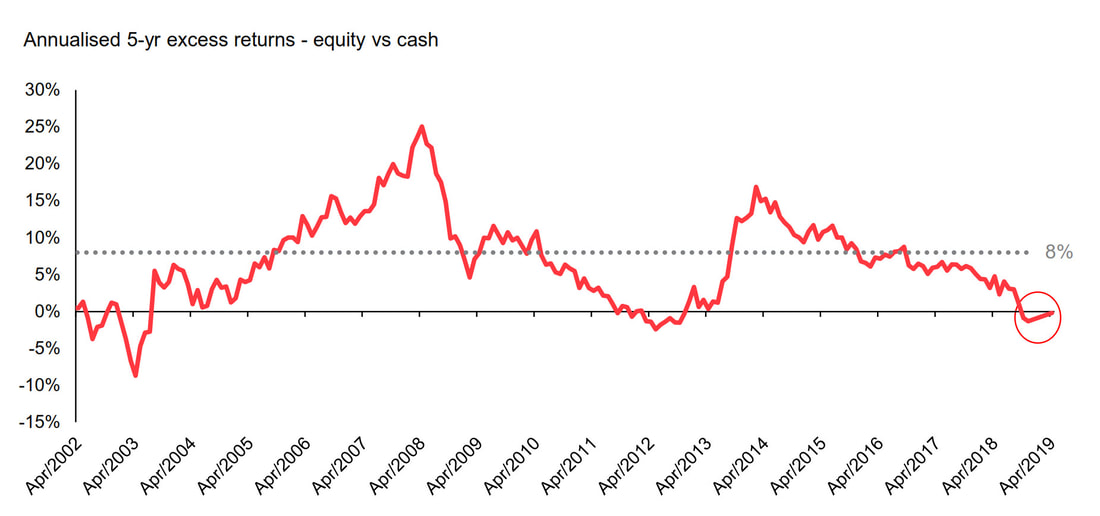

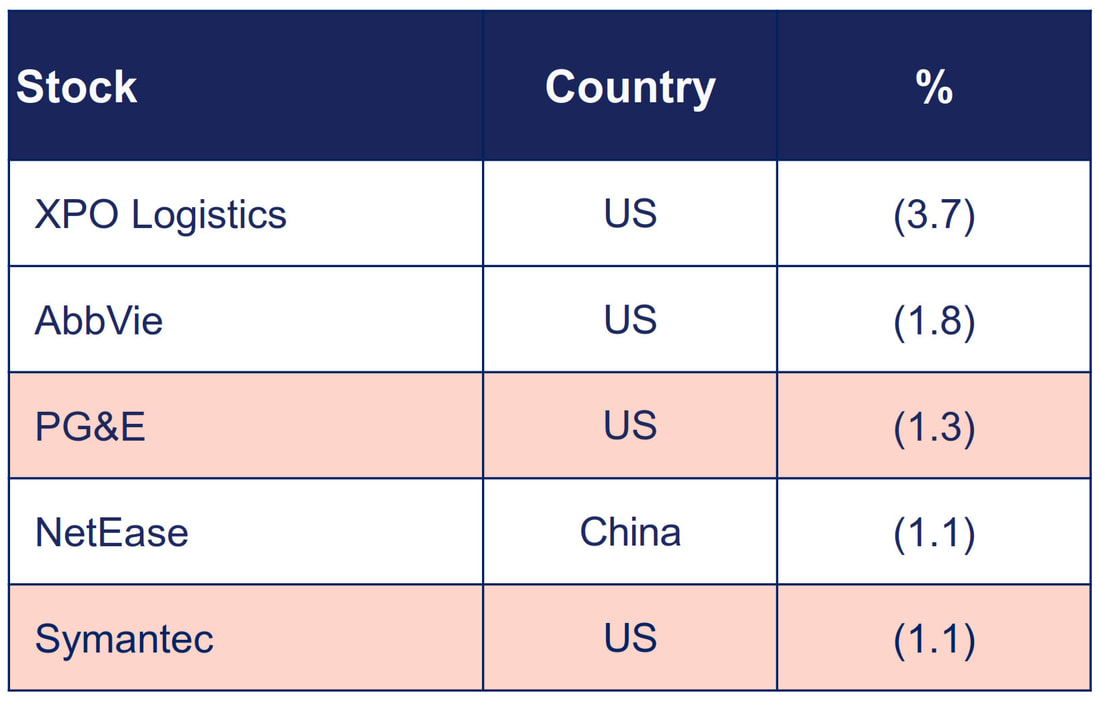

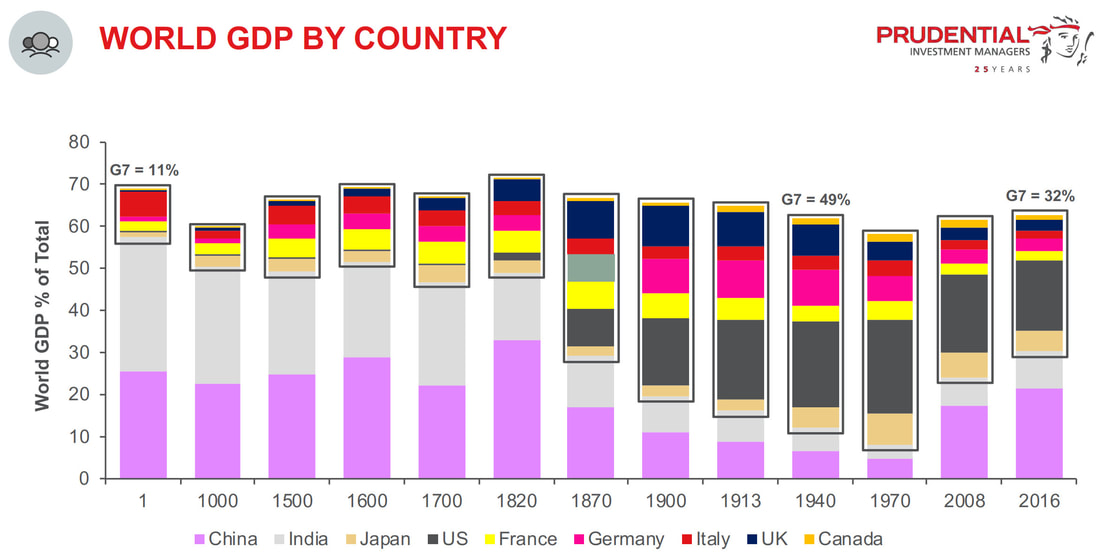

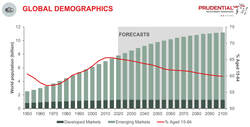

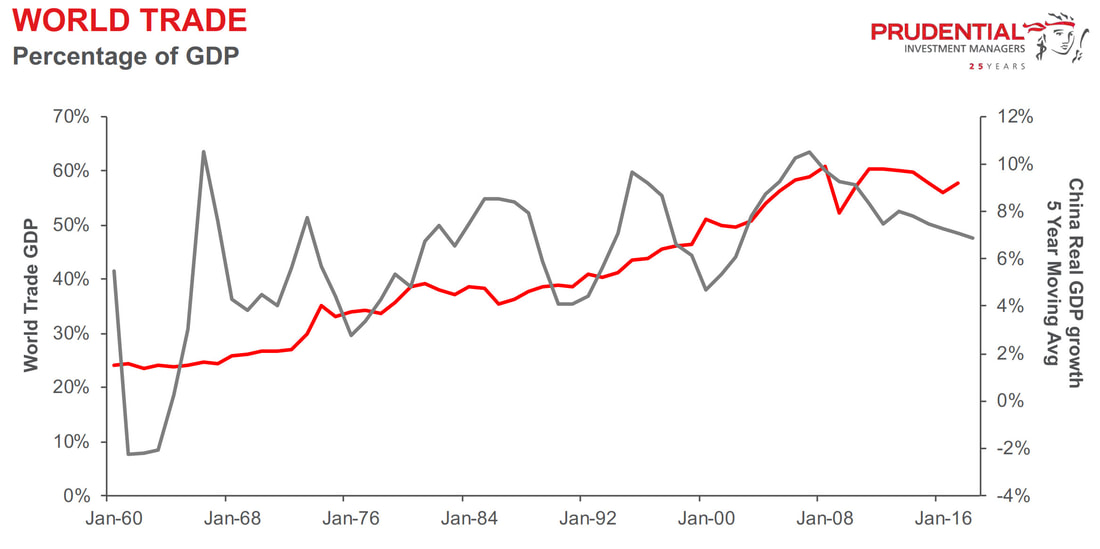

When compared to global markets, the Johannesburg Stock Exchange (JSE) is relatively small, comprising less than 1% of the total global investing universe. It is also highly concentrated, with the top 10 shares on the FTSE/JSE All Share Index (ALSI) making up between 50% and 60% of the index. In contrast, the top 10 shares in one of the world’s major indices, the S&P 500, make up just over 20% of the index. Most of the ALSI’s concentration comes from one share: technology giant Naspers, which makes up 20% of the index. Naspers’ dominance in recent years has increased concentration risk for investors, making portfolios overly sensitive to the factors that drive its value. In general, most investors are happy to contend with the exposure, as long as they are still generating positive returns. But what happens when the proverbial goose stops laying the golden eggs; when the dominant share(s) in your portfolio begins to perform poorly? How you can mitigate your concentration risk As famously stated by American economist Harry Markowitz, who received a Nobel Memorial Prize in Economic Sciences: “Diversification is the only free lunch in finance.” The best way to reduce your concentration risk, without losing out on the potential to earn good returns, is to make sure that you are invested in a combination of assets that have little correlation to one another – essentially, having a diversified portfolio where you generate returns from a wider spread of assets, industries and markets with an acceptable level of risk. To construct a diversified portfolio, one has to consider correlation and volatility. Correlation measures the strength of the relationship between the returns of two assets. A positive correlation indicates a strong positive relationship, i.e. the two assets tend to have higher and lower returns at the same time – this is indicative of an undiversified portfolio. A negative correlation implies the opposite, i.e. returns of the two assets move in opposite directions at any given time. A correlation of zero implies that no relationship (positive or negative) exists between the returns of the two assets. By adding assets with zero, or negative correlation, a portfolio becomes more diversified. You should also look at the overall volatility of your investment to gauge how well your portfolio is diversified. Intuitively, a portfolio consisting of correlated assets should show a larger deviation in its overall returns (i.e. high volatility), while a portfolio that has uncorrelated or negatively correlated assets should show smaller deviations in its overall returns (i.e. low volatility). In essence, if you have a well-diversified portfolio, then your investment should generate returns at lower levels of volatility over the long term. Diversify your portfolio If all this sounds very complicated, you could consider investing in a balanced fund. These are available both locally and internationally and offer a good solution to those investors who want to create a diversified portfolio without the hassle. Your chosen investment manager will carefully select a basket of uncorrelated assets from different markets, companies and industries to ensure that you generate good returns with minimal concentration risk. Local balanced funds offer South African investors some offshore diversification, but remember that Regulation 28 of the Pension Funds Act limits their foreign asset allocation to a maximum of 30% of the fund, with an additional 10% for investments in Africa outside of South Africa. This may not be enough offshore exposure for your needs – in which case you can also invest directly with offshore fund managers of your choice or through an offshore platform, such as the one Allan Gray offers. Every South African resident can use up to R11 million offshore for all foreign expenditure including travel, foreign exchange and for investing purposes. The first R1 million, called the single discretionary allowance, can be used without having to obtain permission from the South African Revenue Services (SARS) and the Reserve Bank. If you want to spend above this allowance, up to R10 million, you would need to get a tax clearance certificate from SARS. To further diversify, many investors choose to invest in more than one of the same type of fund from different managers. If you go this route, it is important to check that the underlying investments are different; otherwise, the combined weighting of the duplicate shares may increase your portfolio’s concentration. Building a diversified portfolio can be complicated and requires a solid understanding of markets and companies. But the good news is that you don’t have to go at it alone. An independent financial adviser (IFA) can help you assess the concentration risk in your portfolio and advise accordingly. It can be tempting to ignore concentration risk when the going is good, and returns are attractive. However, an undiversified portfolio can quickly become a problem if your most concentrated shares begin to perform poorly. Source: Vuyo Nogantshi , Allan Gray  In the past three weeks, I have attended investment briefings by four well-known asset management companies in South Africa. The four fund managers are PSG, Allan Gray, Coronation, and Prudential. Allan Gray ranked first and PSG ranked second in the Raging Bulls Award. Prudential Prudential is the number one Larger Manager according to Morningstar, it also celebrates 25 years of asset management in South Africa this year. Coronation is a JSE listed fund manager that celebrated asset management in South Africa for 25 years last year. I will tell the reader my summary first: 1. These four fund managers have excellent long-term track record. Many of their funds are suitable for different types of investors, ranging from short-term high-yield, secure capital funds, to equity funds and multi-asset allocation funds for long-term growth. 2. No one has escaped the effect of political corruption (namely State Capture) in South Africa in the past five years, which has led to the economic downturn and the flat stock market. Fund managers have also been affected by the ongoing US-China trade war on the global economy and investment market since last year. The annualized return on equity funds over the past five years has been 5%. 3. Looking ahead, all fund managers are optimistic about the return on the South African stock market in the next three to four years, Japan and emerging markets such as China. At this stage, they also like the high yield on South African bonds, giving investors a yield of 9% to 10%. They are negative on European and American bonds, especially the negative interest rate on 10-year German bonds. Investors investing in German bonds are destined to receive less than the principal after 10 years. 4. Allan Gray and Coronation are South Africa's largest fund companies, with large amounts of assets under management and relatively conservative investment style. Prudential and PSG manage assets on a smaller scale, and they are able to be more flexible. Prudential always likes some exposure to listed property, and PSG is now favoring small and mid caps in South Africa and certain Japanese companies. ***** I have been dealing with asset management companies in South Africa for nearly 20 years. I have seen the growth and changes of the asset management industry, and experienced the ups and downs of the investment market: The Dot Com bubble in 2000, the global financial crisis in 2008, the European debt crisis, the emerging market crisis in 2014, and the US-China trade war from 2018 to the present. In South Africa we have seen the shocking firing of Minister of Finance Nene in 2015. During this period, South Africa's asset management industry flourished and there are now more than one hundred fund managers. It is very challenging in choosing the funds to invest in, as the market changes, portfolio managers change, and many funds appear and disappear in these two decades. However, patient investors investing in good funds of reputable fund managers will have been rewarded over the long term. Let compound interest be your good friend and work for you. 1. PSG Asset Management The PSG Asset Management's investment philosophy is 3M – Moat, Management and Margin of Safety. Moat is a company's competitive advantage, that acts as high barrier to entry, such as technology, systems, talent, and markets. Management refers to the track record of the company's management and how they allocate the company's funds. Margin of safety refers to whether the stock price is lower than the assessed intrinsic value of the company, this provides investors with downside protection against the risk of over-estimated intrinsic value. PSG has a 20-year history, was previously run by successful manager Jan Mouton and then handed over to Chief Investment Officer Greg Hopkins, who has 18 years of experience. Shaun le Roux has been with the company 18 years, managing PSG Equity Fund and PSG Flexible Fund. However, it has lost two senior portfolio managers in the past three years, the performance of new managers Justin Floor and Dirk Jooste remains to be seen. PSG's philosophy is to find investment opportunities in areas that everyone hates, and to avoid everyone's favourite stocks. This is value investing. Therefore, PSG currently does not invest in technology companies or defensive stocks, but favours South African small and mid caps. Below are the latest PSG investment update videos: How we think about and manage risk Is SA Inc even investible? Opportunities in local markets Opportunities in global markets 2. Allan Gray Allan Gray has a 45-year history in South Africa and its sister company Orbis has a 29-year history of managing global assets in Bermuda. Both companies share the same founder, Allan Gray, and have the same value investment philosophy. Like PSG, it is also a contrarian investor, looking for investment opportunities in areas that people don't like. However, because of the large scale of assets under management, Allen Gray must invest in large blue chip companies. Allan Gray's strengths are equity research and asset allocation. Its weakness is its long-term dislike for real estate, which currently works in its favour, but it missed the long-term listed property boom before 2018. Allan Gray's portfolio managers are pretty stable, with an average of more than a decade of experience at Allan Gray, giving investors invested in their funds certainty and peace of mind. Allan Gray pointed out that the total assets under management of the South African fund industry in the past three years were virtually flat, indicating that the South African stock market has been dull in the past five years and that the general public under economic and tax strains has no money to invest more.  It is no surprise that, over the past three years, The fund category receiving the most new money flows is money market and income funds. Because of the lacklustre returns from the South African stock market in the past five years, investors have turned to income funds for high yields.  Indeed, the chart below confirms the equity return has been below the cash return over the last five years.  But the stock markets do work in cycles. If history repeats itself, the return of the SA stock market in the next three to four years will far exceed the bank deposit interest rate. The chart above shows that during the past 17 years, between 2002-03 and 2012-13, the five-year JSE total return was lower than the deposit rate. It is also the case from the second half of last year. However, after the stock market rebounded, the return for the next three to four years was better than the bank deposit. According to Allan Gray's data analysis, cash deposits only has a 13% chance of outperforming the stock market in the next four years. In other words, the stock market has an 87% chance of outperforming cash deposits in the next four years. The odds are now in investors' favour to hold and enter the stock market, not to exit. Allan Gray's foreign investment is handled by its sister company Orbis. Orbis has long-standing admirable performance, but it has fallen 20% in the last one and a half years, making it a bottom performer last year, and slightly behind its sector average in the past five years. This is due to its contrarian investment style, sometimes allowing it to greatly exceed the market, and sometimes falling far behind. I remember that in 2012-13, Allan Gray also had a period of under-performance, but it laid the foundation for its subsequent performance in 2014-2016. In the past year, Orbis has more stocks losing money than stocks that make money. What has happened? According to its analysis, the top five detractors of performance are as follows:  Orbis spent some time explaining the largest detractor XPO. XPO is a US logistics and transportation company that aims to help companies enter the e-commerce sector and compete with Amazon. It is committed to the vertical integration within the logistics industry, offering small and medium-sized enterprises one-stop service. It acquired a truck fleet company Conway four years ago. In the second half of last year, the profit announcement disappointed, then short-sellers attacked the company with damaging reports. Its stock price subsequently fell 30%. Orbis met with the management and thought that the founder Bradley Jacobs and his management team were still very good, and the market was wrong in punishing the stock, so it increased its investment in XPO. Abbvie is a US pharmaceutical company, and Orbis is convinced of the future of the US healthcare industry, so it has added another pharmaceutical company, Celgene. After reviewing the investment case for Netease, it has increased its holding, now it is the largest position in the fund, with a weighting of 9.1%. PG&E is an electricity and gas company in California, USA, it sold out at a loss. It also sold out Symantec, an internet security company, at a loss. For the Chinese market, Orbis is optimistic about the future of tech companies, mainly holding shares in NetEase, Tencent and Autohome. Orbis has a long-term track record, I suggest investors buy on current dips. 3. Coronation Asset Management Coronation is 26 years old in South Africa and is South Africa's largest listed fund manager. I was invited to participate in the annual Face to Face event in Cape Town, as due diligence, and listened to its economist and 8 portfolio manager briefings throughout the day, from Top 20 Fund, Balanced Plus Fund, Strategic Income Fund. Capital Plus, Balanced Defensive, Property, Global and Emerging Markets, The day ended with a Q&A session with Chief Investment Officer Karl Leinberger. Coronation employs 300 people, one-third of whom are investment analysts and fund managers, a strong investment management team in South Africa. It follows a valuation driven investment process and invests in undervalued companies or assets. The difference between Allan Gray and Coronation is that Coronation is more likely to invest in riskier industries in the stock market. In recent years, it has invested in mining stocks, which initially caused the its equity funds to fall, then helped investors make money when share prices recovered and rose. Coronation also likes real estate, and for a long time there has always been an exposure to listed property in South Africa and abroad. However, Coronation has also stepped on many of the so-called landmine stocks in recent years, such as Steinhoff and MTN, so the returns from its equity exposed funds have been market average for the past five years. The Coronation investment management team is stable and reputable. They have been incorporating ESG (environmental, social, governance, environmental, social and corporate governance) principles in evaluating investment opportunities for many years. On the whole, their standouts are income-based funds, where risk management is robust, and opportunities are captured for clients to enhance yield. the other area is global Emerging Markets. Many analysts visit the CEOs of listed companies around the world, they really work hard to find investment opportunities for clients. Other funds are expected to have similar returns relative to other larger managers in the long term. 4. Prudential Prudential Prudential Investment Management celebrates 25 years in South Africa. Similar to Coronation, the valuation investment method is also used, but because it belongs to Prudential, a global financial services group headquartered in the UK, it tends to have a more macro, top-down approach, to assess the relative value of each country and asset class, thereby overweight the undervalued assets and underweight the overvalued assets. It does not take big bets, but rather a large number of small bets. It uses a team-based investment management model. Its investment performance is more market neutral, unlike Coronation, which sometimes experiences large ups and downs due to its conviction calls. Although the investment management team is not large, it is also very stable. Chief investment officer David Knee has more than 20 years of investment experience, mainly fixed income assets, worked in the UK and moved to South Africa in 2008. Head of Equity Johny Lambridis is an actuary and has many years of investment management experience. Prudential's macro data analysis has three points that caught my attention: First, China and India accounted for about 50% of global GDP before 1820. The G7 industrial countries rose rapidly during the industrial revolution of the 19th century, and reached the peak of 49% of global GDP in 1940. The rise of China and India over the past 40 years is just a return to its former status. It now accounts for 30%, which is equivalent to 32% of G7 countries.  2. The global population continues to grow, but the growth rate is slowing. The global population is expected to reach 11 billion in 2100. The population continues to be aging, which has a huge impact on social welfare, government borrowing, caring for the elderly, and political landscape.  3. The rise of China is closely related to the liberalisation of world trade. The left axis of the chart below shows the world trade as a percentage of GDP, and the right axis is the growth rate of China's economy. World trade has increased from 25% in the 1960s to nearly 60% in 2008, but since then it has plateaued. The ongoing US-China trade war is threatening world trade, which in turn will slow down China's economic growth.  Prudential's leading funds are Equity Fund, Balanced Fund, Inflation Plus Fund, and Enhanced SA Property Tracker Fund. These funds have outperformed the average fund in their respective sectors over the long term. However, Inflation Plus Fund has fallen behind in the past three years.

[The tax e-filing season is upon us. If you need a tax consultant to help you with your e-filing, please contact Daberistic Accountants at 011-658-1333, email tax@daberistic.com.]

During a media briefing in Pretoria on Tuesday, new SARS Commissioner Edward Kieswetter told the South African public that the tax threshold for those who have to submit returns will be increased this season. Kieswetter’s announcement was initially delayed due to a massive power outage across the city. However, when the lights returned, the new tax chief dished out some encouraging news for those earning a low-to-mid range income. SARS tax threshold: Am I exempt from filing a tax return? Instead of requiring tax returns from everyone who earns R350 000 a year, that minimum figure has been increased to R500 000 a year. In monthly terms, the parameters have shifted from R29 166 to R41 666. However, it’s not all plain sailing for those of us making less than half-a-million per annum. The new threshold laws only apply to citizens if they meet the following set of criteria:

When is tax season in South Africa for 2019? Kieswetter was also keen to encourage more citizens to start using SARS’ e-filing systems. He revealed to tax-paying South Africans that the programme has gone through several updates, and more improvements will be in place by August. One of the incentives for using the e-filing systems is that they help with time management. Yes, tax season will start on 1 August and end on 31 October, but electronic applications start at the beginning of July and remain open all the way through until the last day of January 2020. It’s also worth noting that returns filed via SARS’ app have a deadline of 4 December 2019. Depending on what you’re earning and the new tax threshold, this could be a trouble-free season for many of SA’s workers. Source: thesouthafrican |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|