|

Warren Buffett, the famous billionaire investor and CEO of Berkshire Hathaway, has been held in very high regard by investors. Every year Berkshire Hathaway holds its annual shareholders meeting, and investors gather to hear what Warren has to say. This year the meeting took place on YouTube on 1 May. Let's read about what Morningstar says about Warren and his partner Charlie Munger's comments.

0 Comments

South African Market Update Global equity markets ended the month in positive territory, despite rather modest gains in certain major markets, as global economies continued to show signs of recovery despite new Covid-19 restrictions in certain countries. There continues to be optimism around the US economic recovery, as strong economic data and the high likelihood of further stimulus measures continues to bode well for risk appetite. This, despite Republicans in the Senate unveiling a $928 billion infrastructure proposal, well below US President Joe Biden’s original $1.7 trillion plan. Inflation continues to be a talking point for investors, as the US Federal Reserve’s (Fed) preferred inflation measure, core personal consumption expenditure (PCE), advanced 0.7% month on month in April, bringing the year-on-year figure to the end of April to 3.1%. The Fed continues to reiterate its belief that inflation pressures are transitory and that they intend to keep monetary policy conditions accommodative for the foreseeable future. South African equities ended higher for a seventh consecutive month, largely driven by strong performance from Financials, gold and retail counters. Local bonds had a strong month, as foreigners returned to the SA market (foreigners bought R9.3 billion of local bonds in May) and the yield curve flattened following strong performance from long dated SA government bonds. Local listed property gave back some gains during the month, as the asset class took a breather after strong performance in April. Uncertainty caused by the implications of a third wave of Covid-19 infections acted as a headwind for the asset class. The rand continued its impressive run,finishing the month stronger against most major developed market currencies, supported by strong commodity prices and a weaker US dollar. The South African Reserve Bank’s (SARB) Monetary Policy Committee (MPC) left interest rates unchanged for a fifth consecutive meeting in a unanimous decision, with the MPC revising its growth forecast higher for 2021 from 3.8% to 4.2% following the strong rebound in Q1 2021. SA headline CPI moved significantly higher to a year-on-year figure of 4.4% for April (from 3.2% in March), the largest monthly change in annual inflation since 2009. The increase was largely driven by the base effects of higher fuel and food prices. SA’s trade surplus continues to provide support to the rand, with the surplus for April (R51 billion) following a revised surplus for March of R52.5 billion. Following higher daily Covid-19 cases across the country, President Cyril Ramaphosa announced that South Africa would move to a level two lockdown (effective 31 May), largely in response to a third wave of infections in certain provinces across the country. The JSE All Share Index (+1.6%) ended higher for a seventh consecutive month, largely driven by positive moves in banks, gold counters and retailers. Local equity sectors had mixed performance for the month, with Financials (+9.3%) outperforming both Industrials (+1.6%) and Resources (-1.2%). The top performing shares amongst the largest 60 companies on the JSE in May were Mr Price Group (+28.3%), Gold Fields (+26.5%) and Pepkor (+24.0%). The worst performing shares in May were Sappi (-11.6%), Prosus (-9.7%) and Quilter (-9.5%). Listed property (-2.9%) ended the month lower, with weak performance from some large index constituents and profit taking (after strong performance in April) acting as a headwind for the asset class. Local bonds (+3.7%) had a strong month, supported by foreign buying of SA bonds and a flattening of the yield curve. Cash delivered a stable return of +0.3% for the month. The rand was stronger against most major developed market currencies for the month. The rand appreciated against the US dollar (+5.7%), the euro (+4.1%) and the pound sterling (+3.0%) over the month. Click here to read more.  Global Market Summary

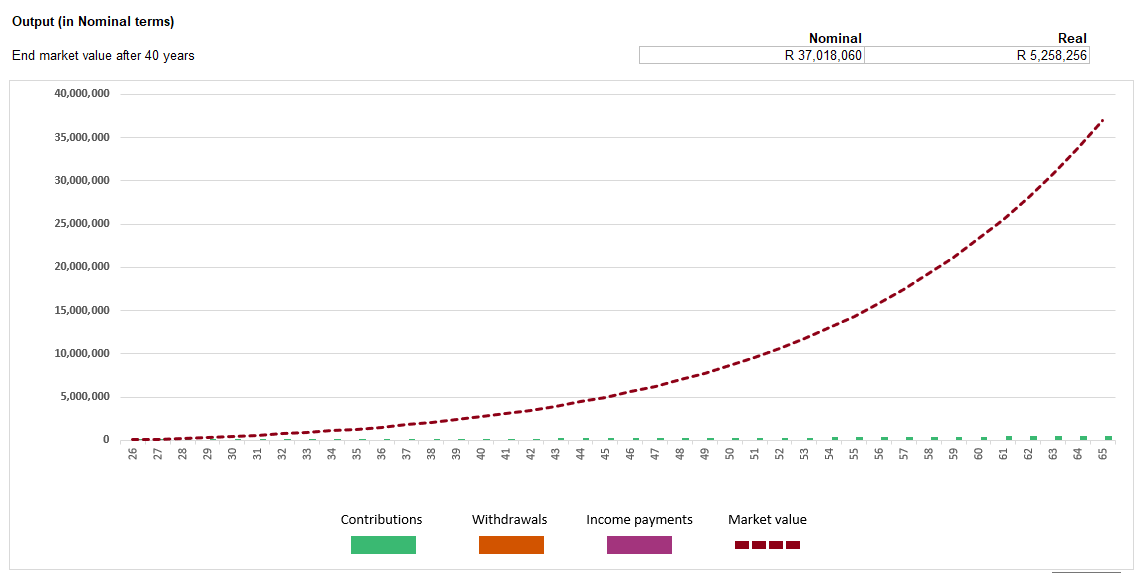

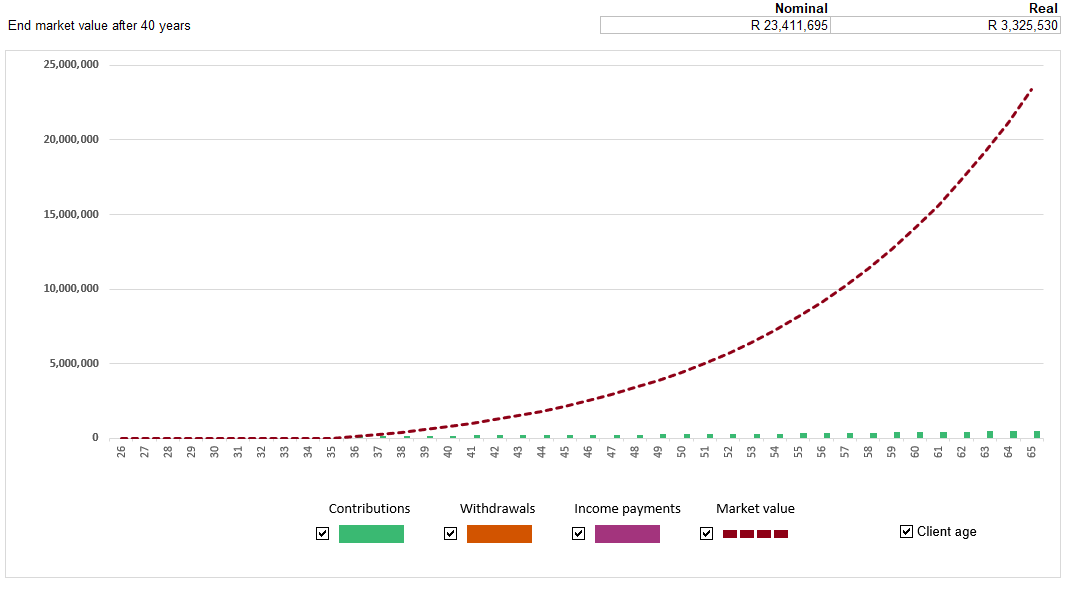

Global equity markets had another good month, largely on the back of continued optimism over a recovery in the US economy. Vaccination efforts remained apace, with estimates suggesting that over 50% of the US population has now been vaccinated. The picture was similar in other developed markets (DM’s), where the vaccination rates continue to improve. Emerging markets on the other hand, continue to lag DM’s in the inoculation drive and there has been a resurgence in new cases in countries such as India and South Africa. From an economic data point of view, May releases were a bit mixed. The Chicago PMI came in higher than expected at 75.2, reaching its highest reading since 1973, whilst consumer confidence on the other hand, as measured by the University of Michigan marginally declined to 82.9 in May from the previous reading of 88.3. Personal income declined by 13.1%, lower than the 14% estimate, as the effect of the stimulus measures started to diminish. The savings rate, however, remained elevated at 14.9%, highlighting the robustness of the US consumer. Turning to inflation, the Core PCE (the Fed’s preferred measure of inflation) surprised to the upside, with May’s reading surpassing the market estimate of 2.9%, as it reached 3.1%, its highest annual reading since 1996. Despite continued evidence of a sustained economic recovery and the ensuing inflationary surprises, the Fed remained steadfast in its monetary policy stance, maintaining the mainstream central banking view that the current inflationary pressures were transitory and attributable to supply bottlenecks. Moves in the bond market were also largely muted following the inflation data releases. Turning to equity markets, the US continued to trail its European counterparts, despite the end of an impressive earnings season. In the US, the S&P 500 (+0.7%) outperformed the technology heavy NASDAQ 100 (-1.2%). The UK’s FTSE 100 (+3.8%) had a very good month, whilst Germany’s FSE DAX (+3.5%) was a standout within the major European markets. In Asia, China’s Shanghai SE Composite (+6.7%) was amongst the best performing markets for the month and Japan’s Nikkei 225 (+0.1%) fared better than the previous month. Emerging markets had another good month, with the MSCI Emerging Markets Index (+2.3%) ending on a strong footing. Overall, global equities ended marginally higher, with the MSCI World Index delivering a return of +1.5% for the month, reflective of the broad positive performances across its constituents. On the commodities front, performance was mixed for the month. Gold (+7.5%) and Oil (+3.1%) built on the performances from the previous month, whilst Platinum (-3.9%) gave up some of its gains from the previous month. The performance of the US dollar was mixed against most of the major currencies for the month. The greenback depreciated against the pound sterling (-2.6%) and the euro (-1.5%), but was largely flat against the Japanese Yen (+0.1%). Click here to read more Source: Morningstar  Last month I talked about Step 4 - Keep a record of your spend. Let's continue with Step 5 - Invest 15% of your earnings. Robert Kiyosaki, a leading personal finance and business coach of our time, advocates "Pay yourself first". People who choose to pay themselves first allocate money to the asset column of their balance sheet before they’ve paid their monthly expenses. Essentially, you set aside a specific amount of money right off the bat, and then live off what’s leftover. And that’s how wealth grows. In South Africa, this means putting 15% of your monthly pay into a retirement annuity, a tax-free investment, an offshore investment, or getting a business education or subscription. Let's unpack this. When I have my first meeting with new financial planning clients, one of the areas we cover is Personal Balance Sheet. Personal Balance Sheet essentially is a list of a person's assets and liabilities. At the end we calculate a person's Net Asset Value (NAV) by subtracting liabilities from assets. Many people have no ideas of what are assets, what are liabilities, and the differences between the two. They work hard, they try to get a better income. After many years, they wonder why they have little to show for it, and where money has gone to. They are busy paying everyone else, the taxman, banks, credit card companies, municipality, Eskom, DSTV, cellular providers. Then they have no money to pay themselves. So they go through their life, by the time they get to 40s or 50s, then realise they don't have enough saved up for retirement. It is important for us to instill in our teenage children, young adults the importance of savings, that they should start saving 15% of their income when they start their first job or business venture. Don't rely on what your employer would do for you. In the past, many corporates in South Africa would provide generous employee benefits, including a pension after retirement. Due to changes in accounting standards, increased competition and tougher economic environment, many corporates have cut back on employee benefits. Just about all have moved to Defined-Contribution arrangements, they no longer guarantee employees a pension after retirement. We need to educate our children (and ourselves) to create that financial nest egg ourselves. No one else is going to do it for us. Not the employer, not the government, not your parents. Starting early is key. If a young person in their twenties start their first job, and save 15% of their income every month, invest wisely, then by the time she gets to 65, she should have built up a retirement capital, a sum of money to draw an income from. What we call "comfortable retirement." Below is a chart illustrating a 25-year old earning R40,000 a month, saving 15% of her income per month (i.e. R6,000). Assume her income increases at 5% per annum, and she keeps her savings rate at 15%. Also assume she gets 8% return on her investments. At 65, the projected capital she will built up is R37 million.  If she delays the decision to invest until age 35, i.e. she only starts saving 10 years later, then at 65, the projected capital she will build up is R23.4 million. See the chart below. While still significant, it is 37% less than if she had started at age 25.  So a 10-year delay will cause her wealth at age 65 to reduce by 37%! Investment products for long-term investmentYou may consider using the following products for investing for long-term: Tax-free investment account: while limited to R3,000 per month or R36,000 per year contribution, you invest tax-free, and you can invest up to 100% offshore. Watch this video to get the basics of a Tax-Free Investment account: Retirement annuity: This is designed for saving for retirement, offers great tax benefits. Watch this video to understand the basics of a Retirement Annuity: Offshore investment: This allows you to invest in hard currencies such as the US Dollar, Euros and Pounds, by converting your Rands into these currencies and investing offshore. This is great for diversification, and accessing investment opportunities not available in South Africa. Unit trusts: This allows you to invest in a wide range of collective investment schemes. You should invest in a number of funds for diversification, and your portfolio should be suitable for your risk profile. Endowment policy: This forces you to invest for a minimum period of five years, investment growth is taxed within the policy, so when it pays out you receive the proceeds tax free. Watch this video to understand the basics of an endowment policy: Contact us today at service@daberistic.com if you would like to speak to a Financial Advisor, on how best you can invest 15% of your money, to create your wealth.

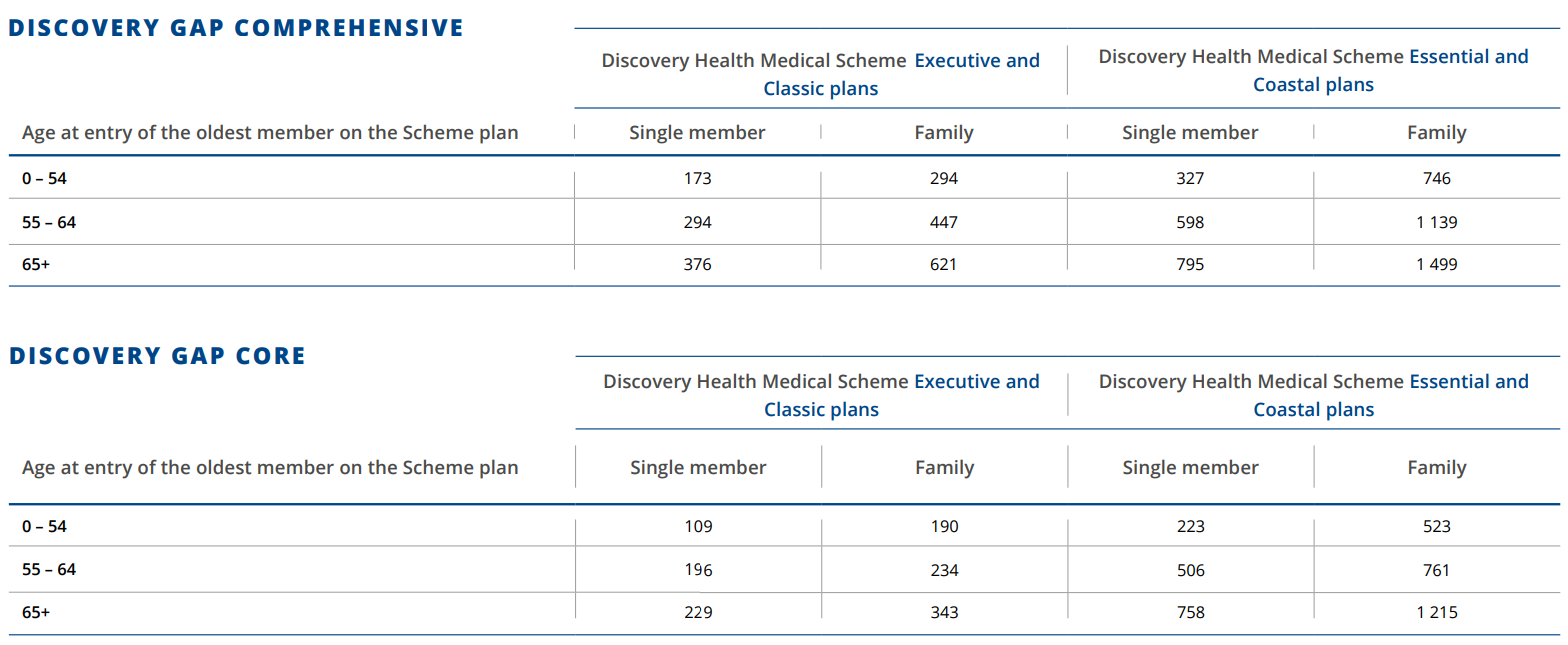

In our last month’s newsletter, we have mentioned Discovery is currently running a special offer, where members who join Discovery Gap before 30 June you get the first 3 month’s premium free (Subject to underwriting). Should you have no break in gap cover and have proof when you move over to Discovery Gap, underwriting will be waived. Unexpected medical costs can place financial strain on a family. Especially when service providers charge more than what your medical scheme pays. Hence why Discovery Gap cover is your gateway solution to protect you against unforeseen financial burdens. Discovery Gap cover provides shortfall cover where doctors, specialists charge above medical aid rates and works seamlessly with your Discovery medical aid. When both your medical aid and gap is with Discovery, and in an event where gap does occur, the claim is seamless, as no paperwork is required. However, gap cover cannot provide cover where medical aid does not pay towards a procedure. For example, if your medical scheme option only pays out at 100% of scheme rate, you will then be liable to pay the shortfall of the other 200% to 400% charged by your service provider as an “out of pocket” expense. If you have Discovery Gap, the system will pick up at claim stage and automatically process and settle the gap portion. Here is a testimonial of one of our clients Mrs Jenzie (Not real name) I gave birth in a private hospital in Johannesburg. The hospital bill was R32,620, Gynaes bill was R12,800 and the anaesthesiologist R4,850. Medical Aid made the following payments:

Other reasons to choose Discovery gap cover:

To apply for Gap cover contact Tammy in our Health department, email service@daberistic.com, Tel 011-6581333, Option 2 for Medical Aid.

As many South Africans are taking note of their spending habits and looking for the best ways to save money. We understand you may want to cut back on a few things, but one thing you should never cut back on is quality insurance. Cheaper insurance options could save you some cash in the short-term, but will usually end up costing more in the long run, especially if you aren’t properly covered. You can still get affordable cover without compromising on quality. Here are some savings tips to ensure you enjoy affordable car insurance, house insurance and building insurance. Get the best car insurance premiums

More affordable home insurance

Budget building insurance cover

Check in regularly on your insurance cover It’s very important to do a regular run-through of your lifestyle, profile and assets as these are the factors that determine how much you are charged every month. Things change all the time – for example, you may have installed extra security measures around your home and not told us, changed jobs, gotten married or had a child move to university. Simply by updating your profile, you may find that your premium decreases or that your risk profile has changed. Remember that a car depreciates in value every year. Ensure that the insured amount reflects the reasonable market value of your vehicle as you will only be paid the insured amount or reasonable market value (whichever is the lesser of the two). To review your current policy or get a comparative quote contact Marizka from our Short-term department, Tel: 011 658-1333, email service@daberistic.com Source: Santam

The Protection of Personal Information Act (POPIA) The Protection of Personal Information Act (POPIA) is the comprehensive data protection legislation that obliges organisations to deal with the processing of personal information by applying specific principles and conditions. POPIA deals with your constitutional right to privacy and the right to access of information. POPIA was signed into law by our President on 1 July 2020 to be effective by 1 July 2021 and much work has taken place behind the scenes in preparation for this deadline.

What does POPIA mean for you as a client? Daberistic has always been committed to treating client information in an ethical manner and POPIA provides the legal framework and requirements for this treatment. All companies, including Daberistic, are now obliged by law to deal with client information with far more diligence than ever before. This includes how and why information is collected, how it is processed, shared, stored as well as access to this information. What does it mean for Daberistic? Any company that processes personal information of clients, members, suppliers, and employees, is required to comply with POPIA. This means that we need everyone to be on board no matter what their role or job level is within Daberistic. It also means that the internal compliance Officer and Information Officer in Daberistic, are currently doing all that is required to ensure that our business process and/or systems that is affected by the obligations imposed on us by POPIA are compliant. Daberistic Privacy Policy on our website Our Privacy Policy provides the details of how we deal with the personal information of our clients and it is available on our website at the following address: https://www.daberistic.com/privacypolicy.html  Dear client,

I thought it would be useful to explain the way we think about inflation and your investments as I’m not sure I’ve fully elaborated on this before. So, to start, let’s talk about inflation. Inflation is a relatively simple concept, used to describe the gradual rise in the cost of goods and services. For example, a loaf of bread or the cost of petrol. Inflation is generally healthy if it’s in the 2-3% per year range, but it is considered to be unhealthy if it falls too low or rises too high (the idea is that we make steady progress over time). For this reason, the central bank will adjust interest rates to control it. Inflation is important today because it is currently rising from a very low base, but it’s perhaps rising too quickly. This is understandable, given the reopening of the economy, yet is garnering headlines and has caused some volatility among certain assets. We should also keep in mind that the job of your total portfolio is to increase your purchasing power over time. Some assets we hold will do better in a period of higher inflation and some will do better in a period of lower inflation. The key is to strike the right balance for your long-term goals and risk tolerance, which is a core part of your financial plan. On this, the return on cash (interest) typically fails to keep pace with the rising prices of goods (inflation). Therefore, as a long-term pursuit, cash is actually a very bad investment. Hence, unless we have absolute certainty that the markets are nearing the peak, which is extremely difficult, putting everything in cash is rarely a good idea. We therefore use cash selectively as an investment tool. This is already done within your portfolio, where cash is treated as any other asset class available for allocation. This means that as the attractiveness of other available assets rises relative to cash, cash allocations should fall and vice versa. Therefore, cash plays both offense and defense, by being used as ‘dry powder’ for adding undervalued assets to the portfolio and by buffering against rich valuations. This brings us to a crucial aspect of wealth creation and preservation – we need to be a step ahead of our own emotions as well as other participants emotions. So yes, cash may feel like the best place in the darkest moments (so-called “cash is king”), but it is a poor choice when considered as a long-term pursuit and only tends to work if we increase it before the market decline occurs. At heart, we remain confident that your portfolio is well positioned to navigate different inflation environments. We can’t rule out the odd setback (whether due to inflation, covid, or otherwise), but wealth creation is often about avoiding the biggest mistakes, which is why we’re diversified across different assets. We want to “be greedy when others are fearful and fearful when others are greedy”, but we also want to manage risks along the way. Bringing this together, we want to reiterate that we are aware of the current inflation discussions and your portfolio has been thoughtfully considered in this light. If you would like me to elaborate further on this, or any other matter, I’d be delighted to chat. Regards Kevin Yeh, CFP® |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|