The new vehicle licence regulation specifies that no motor vehicle can be bought or sold with an expired licence disc. This means that, insurers, cannot write a vehicle off if it has an expired licence disc on the write-off date. Please take note of the below process as it will take immediate effect on all write-off claims.

What this means for your clients Insurers cannot renew a licence disc on behalf of a client. As a result, as the client you must assist in renewing the licence disc if it has already expired or expires during the claim process. What happens when the licence disc expires after the date of loss? If the licence disc expires after the date of loss, but before the claim is settled,as the client you will will need to renew the licence disc and send proof of renewal to insurer before they settle the claim. Insurer will reimburse the cost of the renewal in the claim settlement amount. What happens if the licence disc expired before the loss date? If the licence disc expired before the claim event, it is the client’s responsibility to renew licence disc. Insurer will settle the claim once the client has sent proof of renewal. To get assistance with a claim, quote as well a reviewing policy schedule for your vehicle, home and business contact Jan in our Short-Term Department; email shortterm@daberistic.com ,tel (011)658 -1333 Source: Discovery insure

0 Comments

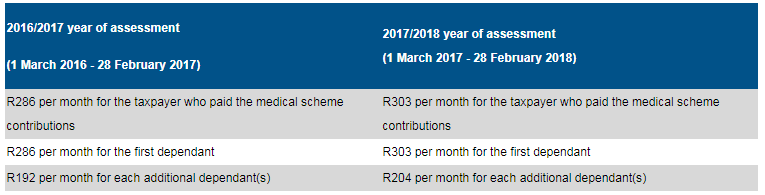

What is it? A Medical Scheme Fees Tax Credit (also known as an “MTC”) is a rebate which reduces the normal tax a person pays. This rebate is non-refundable and any portion that is not allowed in the current year can’t be carried over to the next year of assessment. It applies for years of assessment starting on or after 1 March 2012 (from the 2013 year of assessment). Who is it for? The MTC effectively replaced part of the tax deduction that was specifically allowed for medical scheme contributions, and applies to fees paid by a taxpayer to a registered medical scheme (or similar registered scheme outside South Africa) for that taxpayer and his or her "dependants" (as defined in the Medical Schemes Act). This MTC seeks to bring about greater fairness and help achieve greater equality in the treatment of medical expenses across all income groups. The MTC is a fixed monthly amount which increases according to the number of dependants:  How does it work?

The MTC will effectively impact both the employer and the employee. This credit must be taken into account by the employer when calculating the amount of Employees’ Tax to be deducted from the employees’ remuneration. Individuals who have not had their MTC taken into account by an employer (for example, an individual who is retired and receives a pension; or an individual who is self-employed) can claim the MTC on assessment by submission of an annual income tax return. If you need assistance with getting your medical aid tax certificate please contact Namhla in our Health department, email health@daberistic.com , tel (011)658-1333 Source: Sars  Many people believe that only the family breadwinner needs to have life, disability and severe illness cover. This view is fundamentally flawed, a financial planning professional says.

Craig Torr, director at Cape Town-based financial planning practice Crue Invest, says that just because the stay-at-home partner does not earn an income does not mean the family would not suffer financial loss if that person were to die or become disabled. “According to our financial planning principles, we believe in preparing a joint financial plan for both spouses – irrespective of who works, who doesn’t, or how much each earns,” Torr says. “Regardless of income, qualification or career, the couple is running a joint household and is jointly responsible for the financial future of the family.” Torr takes as an example a family of four, where the wife is the sole breadwinner and, by mutual agreement, the husband is a stay-at-home father to the couple’s two small children. The natural, and correct, assumption is that the wife would require assurance in the event of her own death or disability, Torr says. If she were to die, she would need her life cover so that her husband could maintain the family’s standard of living , invest for the children’s education and fund his retirement. If she were to become disabled, she would need her disability cover to pay her a monthly income until she reaches retirement age. And if she were to suffer a debilitating illness, she’d probably also require lump-sum severe illness cover to provide capital to cover the additional expenses. “However, many couples fail to ask the question: what would happen to the working partner and children if something happened to the stay-at-home partner – in this case, the father?” Torr says. A host of functions would have to be replaced, he says. The stay-at-home parent’s job description is likely to include performing household chores, grocery shopping, paying and managing domestic workers, lifting children to and from school and extra-murals, liaising with schools and teachers, supervising homework, and preparing meals and school lunches. “The reality is that a full-time father might not earn an income, but he does work. His role is the most important job on Earth,” Torr says. If the husband were to die, questions the breadwinner wife would need to consider are: • Would I have to hire an au pair or a child-minder to take care of the children in the afternoons? • Would I need to hire a tutor to help my children with homework? • What would happen during school holidays? Would the children go into holiday care, or could I rely on other members of the family to look after them? • Would I need to hire a domestic worker (or increase domestic help) to prepare meals ? • Would I consider cutting back on my hours of work in order to spend more time with my children?. • Would I consider having my parents (or in-laws) move in with me to assist with the children? Torr says: “Our society, in general, undervalues the role of the stay-at-home-parent, and this is never more evident than in the field of financial planning. In the words of GK Chesterton, ‘How can it be a small career to tell one’s own children about the universe? How can it be broad to be the same thing to everyone and narrow to be everything to someone? No, a [stay-at-home parent’s] function is laborious, but because it is gigantic, not because it is minute.’” The reality is that the loss of a stay-at-home parent is greater than anyone can quantify, and you need to consider risk cover for that person too, Torr says. Needs-matched cover for stay-at-home parents Schalk Malan, the chief executive of life assurer BrightRock, says although his company is not the only provider to insure stay-at-home parents, its needs-matched approach to life and disability assurance makes it well suited to do so. “With BrightRock’s needs-matched product structure, disability and income protection cover for a stay-at-home parent can be uniquely tailored in terms of cover amounts, premium increases and pay-out structure to meet the family’s household, childcare, healthcare and debt needs. Unique features include the ability to choose between a lump sum and a recurring income at the point of claim, when the family better understands the stay-at-home parent’s prognosis and their financial needs. Families can also buy additional cover or change cover when their needs change, without medical underwriting. “BrightRock will calculate the stay-at-home parent’s ‘income’ at a maximum of half of the working spouse’s income, and maximum rand limits apply. Income-earning clients who choose to become stay-at-home parents, take time off work or take extended maternity leave will keep all their BrightRock cover in force at their existing cover amounts for up to 12 months. In both of these scenarios, clients will continue to have access to the additional features of our product offering, which enables them to change their cover as their needs change. “We believe it is worth protecting income for stay-at-home parents, given the role they play in families’ financial well-being,” Malan says. Request for a quote for your family life cover, please contact Kevin or Thato in our Life Department, email life@daberistic.com, tel (011)658-1333 Source: Personal Finance |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|