Last time I outlined what financial planning is. Let us have some correct ideas about money before we dive deeper into financial planning.

1. Money will come and go. We did not bring money into this world, and we will not take money with us into the next world. Money is for us to use in this world. Do not put your hope in wealth. The Chinese have a saying, "a storm may arise from a clear sky; men's fortunes may change overnight." Something unexpected may happen at any time. Money can leave us overnight. The Bible tells us, "Cast but a glance at riches, and they are gone, for they surely sprout wings and fly off to the sky like an eagle." Also says, "... nor to put their hope in wealth, which is so uncertain, but to put their hope in God, who richly provides us with everything for our enjoyment." 2. Money is the medium of exchange for products or services. In ancient times, before the currency was invented, people bartered, exchanging goods for goods. Later, for the convenience of transactions, the currency was invented. In ancient times, shells, gold and silver, and copper coins were used. Today, banknotes and credit cards are used. Knowing this, you will use money instead of just saving money for no purpose. 3. Money is limited. Some people are addicted to money, and even sacrifice their lives for money. But money is not omnipotent. Think about the following: Money can buy food, but can't buy life Money can buy drugs, but can't buy health Money can buy skin care products, but can't buy youth Money can buy a diamond ring, but can't buy a happy marriage. Money should be our servant for us to use. We don't want to be slaves to money and live for money. The Bible tells us not to love money. 4. Make good use of money. We should use money in a legitimate and positive way, not to waste, squander, or use money for illegal things. Let us use a negative example: Some people enter and leave the casinos, gambling with their money, trying their luck in making a big profit, or turning defeat into victory. However, gambling becomes addiction, messing up life and ruining families. At the end a person is faced with a broken home, financial ruin and divorce. 5. Live within your means. Under normal circumstances, our expenditure should not exceed our income and wealth, so as not to lead to debts and financial pressure. Don't abuse credit cards for impulsive shopping. Except for home loans and vehicle finance, which enable big-ticket items such as house and car, we should avoid loans, especially high-interest loans. In the future I will write about the preparation and analysis of personal or household financial statements and the management of income and expenditure, to help you live within your means. Next time, I will share with you the financial planning process.

0 Comments

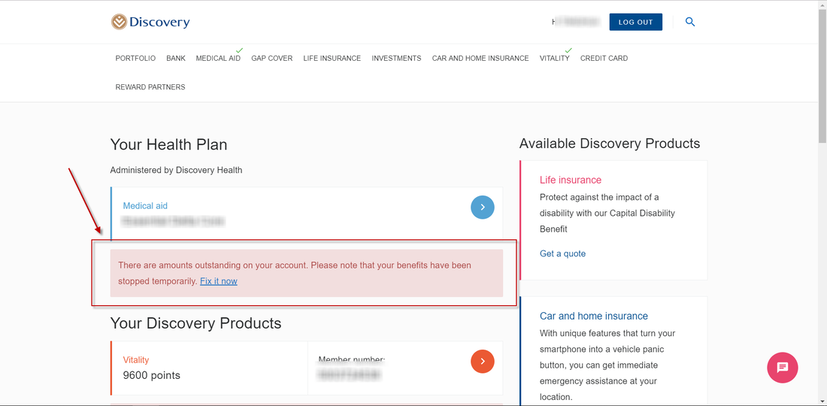

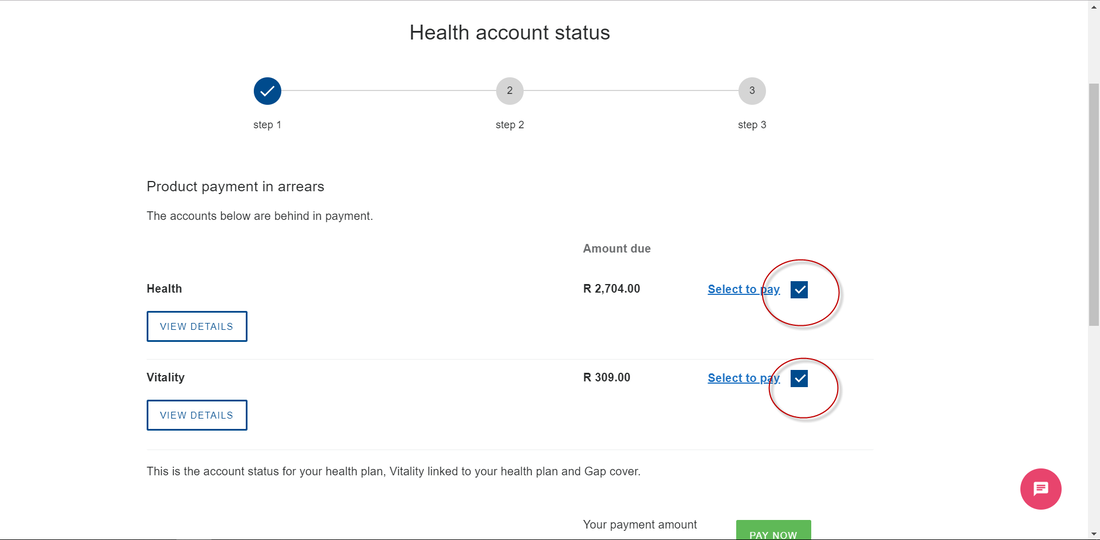

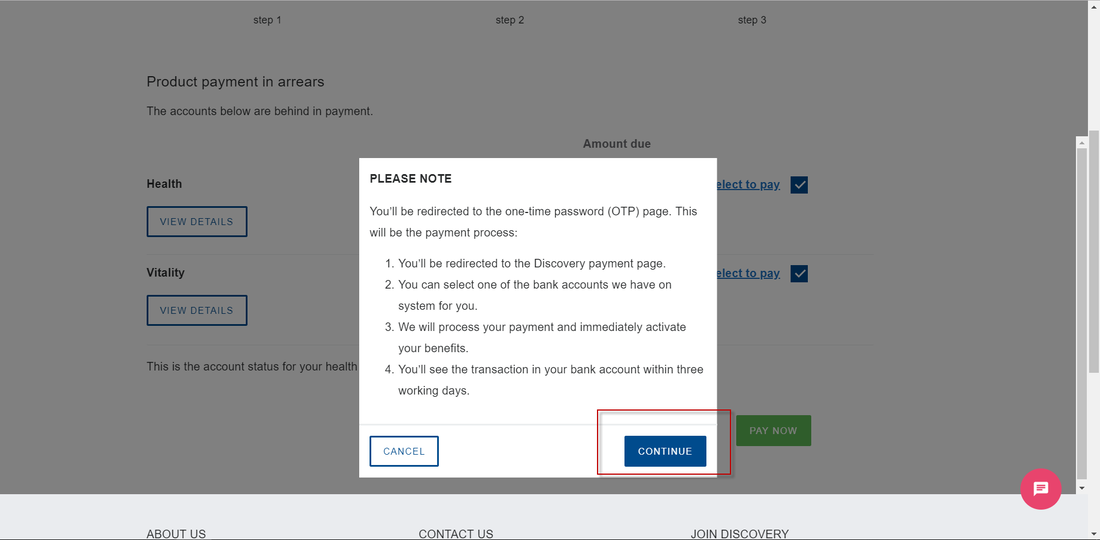

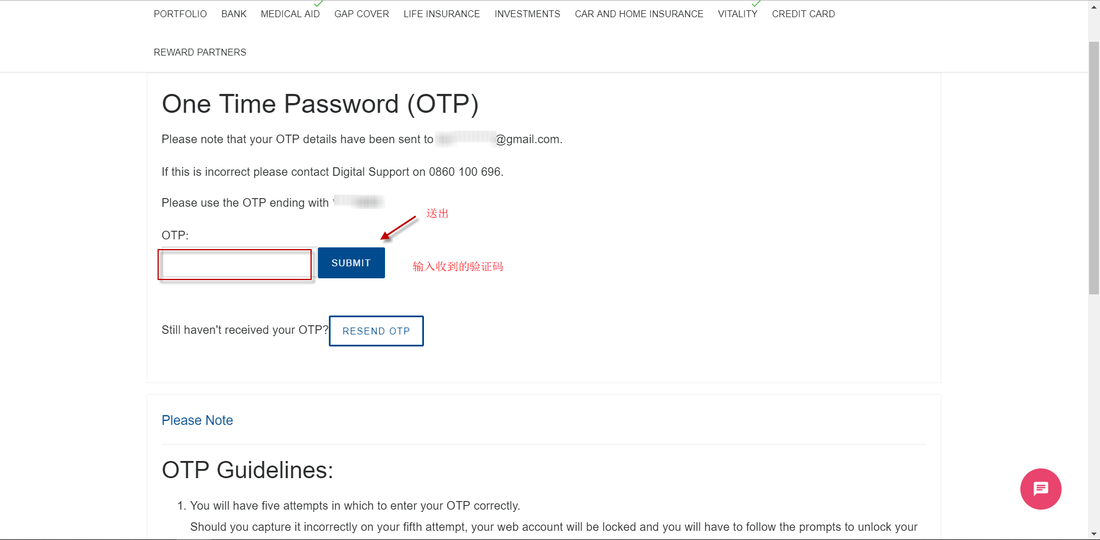

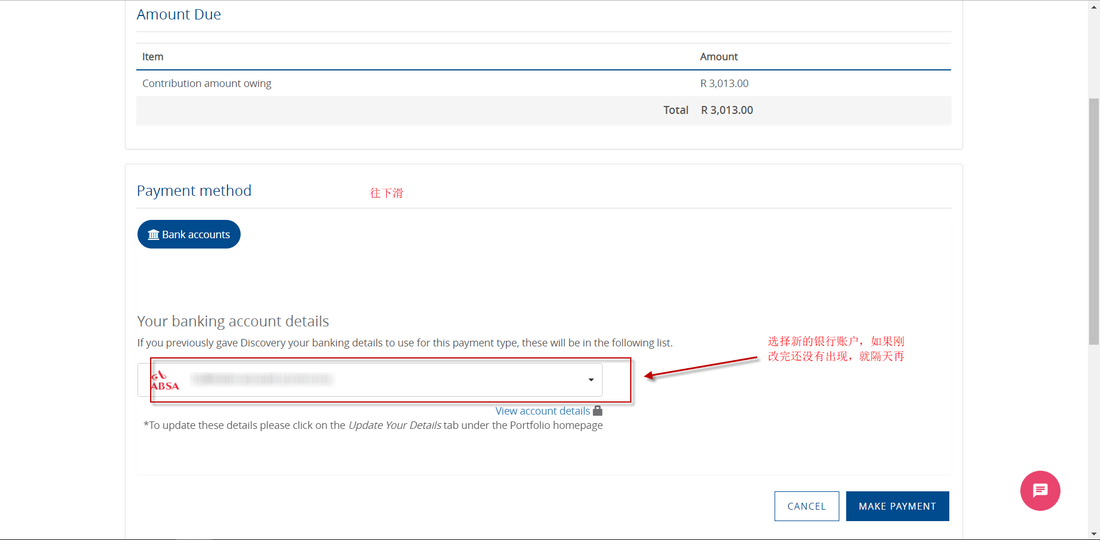

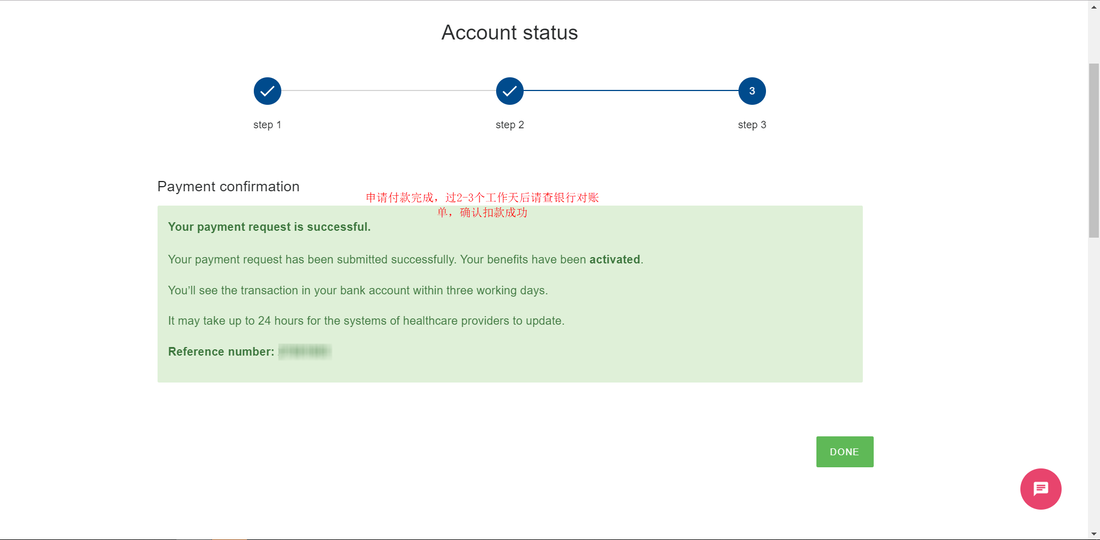

Many people may have failed to get insurance premiums paid because of changes to their bank accounts or problems with their bank accounts, resulting in temporary suspension of medical insurance. Beginning in 2019, Discovery has changed its online information to online instead of submitting changes in writing. The advantage of changing bank information online is no waiting time! The system will be updated immediately after the change. After the change is made, you can apply for a new charge directly online. Note: You can change only the primary guarantor bank information systems. The following are the detailed steps on how to change bank details online. 1. Go to Discovery website www.discovery.co.za and login into profile. 2. Once you are logged in you will see below red box, indicating arrears, "click fix it now to make payment".  3. Click "select to pay", if you have Vitality as well click "select to pay" on Vitality.  4. Then click "continue" to get OTP.  4. Confirm whether OTP they should be sent to the mobile phone or the mailbox. Fill in and submit the order. If the "please note that your OTP details have been sent to" is blank, please go to "Verification Code Settings". For more please go to here to see steps.  5. Select the newly added bank account  6. You will see confirmation of payment   Don’t walk away from your vehicle before checking it is locked in order to mitigate the chances of falling prey to car-jamming, warns Marius Steyn, Santam underwriting manager.

Steyn says, according to the State of Urban Safety in South Africa Report, there has been a 58 percent increase in car-jacking since 2011. He says that remote jamming, or car-jamming, is a practice where criminals use a signal-jamming device to prevent a car’s central locking and alarm systems from being activated, leaving a vehicle vulnerable to theft and vandalism. “Car-jamming continues to be an escalating safety concern for many South Africans. Motorist often walk away from their cars while pressing their remote without ensuring that their vehicles are physically locked. Because of this behaviour, criminals are provided the opportunity to commit a crime like car-jamming,” says Steyn. Asked whether insurers quoted clients higher premiums if, when taking out cover, they indicated that they regularly parked in public parking spaces, he responded: “Currently, at Santam it does not influence the premium.” Steyn says that if motorists do fall victim to car-jamming, they should not get in a “jam” with their insurance. The following conditions usually apply to most policyholders: “In most cases, personal insurance policies covers the theft of insured property from a locked vehicle subject to the limitations and conditions of the policy. To strengthen the success of the claims process, video footage from surrounding CCTV, would support (it). If, however, it is later proved that the vehicle was, in fact, not locked, the insurer has the right to reject the claim.” He says some policies require that theft from an unattended vehicle be accompanied by forcible and violent entry or exit. “The best practice is to understand the conditions of your insurance policy. It also cannot be stressed enough that it is important to always check and double check that your car is secure and that you’ve stored your belongings away in a safe place.” According to Aon insurance, remote jamming involves the blocking of car remotes using a household remote, as both car remotes and household remotes operate on a 400-megahertz frequency and criminals effectively prevent the locking action of the car from being activated and can then have easy access to the vehicle and its contents without any forced entry. “Parking areas outside schools are being targeted, as these are particularly easy pickings for criminals, as many parents leave valuables such as handbags, wallets, iPads and laptops in their cars while they walk their children into school. Quieter shopping centres with less security are also a favourite hunting ground,” says Aon. Steyn says you should check immobiliser devices and security systems regularly. If there are faults, get the devices repaired or replaced. Store items such as sunglasses and cellphones in a glove compartment or locked boot. This reduces the temptation to steal. For any Short-Term queries, please contact Edmond and Po-lin in our Short Term department shortterm@daberistic.com tel no: (011) 658 – 1333 Written by: Jospeh Booysen Source: Personal Finance  Many people like to watch the quadrennial Olympic Games: The best athletes compete for the gold medal. The Olympic medallists not only bring pride for their country, but also make their efforts affirmed on the world stage. They are the best of the best. Behind their awards, there are strict plans developed by the coaches, and they have persevered with the training over the years.

Similarly, if a person wants to achieve financial stability as an individual, a family or in business, to provide for the needs of oneself and family, furthermore to accumulate wealth, a complete and comprehensive financial plan is required. The higher the income of a person, the more his business empire grows, or the more financially dependent family members, the more complicated and detailed financial plan is needed.. So, what is financial planning? In short, financial planning is a s plan based on a person's current financial situation and future lifestyle and financial goals. It is a road map that takes you from Point A (current financial situation) to Point B (where you want to be in the future). Consistently following and implementing this plan, step by step, will enable you to achieve your lifestyle and financial goals. Everyone's personality, preferences, financial situation and ideals are different, so no two people's financial plans are the same. Let us use two examples to illustrate: John is single, works in a large company. His job is stable, and the company's pay and employee benefits are good. He has a small second-hand car and shares an apartment with a friend. He hopes buy a new car of around 300,000 rand, trade in his old car. He wants to buy his own apartment of about R1,000,000. He also plans to travel in Europe for three weeks next year. Andy has two children. He has an import and export business, and his wife works in a small company. They have two children aged 7 and 10 in primary school. They have their own house valued at R4,000,000. The mortgage bond on the house is R2,000,000. They have vehicle finance with an outstanding principal of R550,000, and a personal loan of R100,000. They have some unit trust investments. They hope to send their children to private high school and universities in the future, and pay off their loans within 10 years. John has no financial dependants, his lifestyle goals are relatively short-term, so his financial plan would be relatively simple. In contrast, Andy has a family, has loans. He needs to consider the future education, extracurricular, living expenses of his two children, and the financial impact of unexpected death, disability or illness on his family's finances, so his family financial plan would need to be comprehensive and in-depth. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|