Being involved in an accident is an awful experience that every driver is never prepared for. Are you aware of what you can claim for and your procedures going forward?

It’s stressful enough if your is car written off by insurance, but if you’re unsure the processes involved, it’s even worse. Barend Smit, Marketing Director of MotorHappy, a supplier of motor management solutions and car insurance options, explains that your car is considered a “write off” when, after an accident, your insurer deems the cost of repairs higher than the insured value of your car. Smit says: "When you’re involved in an accident it’s obviously a highly stressful situation, especially if anyone has been hurt. Try to keep calm and ensure you get all the necessary information required." The following steps are important, if you’ve been involved in an accident:

“In some cases, it’s viable to repair the car, and in others it is safer and more economical to write it off. If your car is written off, and it’s still under financing, you must let your financing company know. Technically, the car is still owned by the financier until your insurance company settles the claim and pays the outstanding financing amounts to them,” says Smit. Your payout from your insurance company will largely depend on your excess (the amount you pay first when you make a claim), the amount you still owe if your car is being financed and the depreciation of your car (the decreasing value of your car based on wear and tear). "If you believe your car can be repaired economically and that it shouldn’t be written off, you can either escalate the issue at your insurance company to find a resolution, or you can appeal to the Ombudsman for Short Term Insurance," advises Smit. MotorHappy has partnered with some of South Africa’s top insurance companies to provide vehicle insurance. Various options are available but the most extensive option available is comprehensive car insurance, which covers you in the event of accidental damage, theft and hijacking. It also covers your car for damage caused by weather conditions such as storms and floods. Comprehensive insurance also covers you if you are responsible for an accident and need to pay for the repair of damages to the other car. "Comprehensive insurance might be the most expensive type of insurance, but it offers the most cover," says Smit. "Insurance might be deemed as a ‘grudge purchase’ but it can protect you from disastrous financial loss if you’re involved in a vehicle that’s not covered by insurance. It’s a fact that many cars on South African roads are not insured so it’s important to protect yourself by investing in insurance." Third Party: Another type of car insurance available to South Africans. Third Party only does not give you any protection or financial assistance if your vehicle is damaged but it does protect you if you cause damage to someone else’s vehicle, or if you injure another person. This type of coverage is the most affordable because of how limited the coverage is. Third Party with Fire and Theft protects you for damage you cause to other people and/or their vehicles, and your vehicle is also covered in the event of fire, theft or hijacking. There is no coverage if your vehicle is involved in an accident with another vehicle. If you would like to register a claim Contact Rethabile in our Short-term department, email shortterm@daberistic.com , tel (011)658-1333 Written by: DLeigh-Ann Londtrop Source: Wheels24

0 Comments

What happens when my benefits start and what do I need to know?

The following benefits needs pre-authorisation

The following benefits do not need pre-authorisation

How to get pre-authorization • Please call 0860102 493 to get an authorisation number • Please ensure that you have the information regarding the treatment required- E.g. Policy Number/ date of treatment/ Dr or Hospital practice number/ ICD10 Code, and Procedure Code Day-to- Day Benefits These are the benefits that are only available from your chosen Ingwe Active Primary Care network doctor. Chronic benefits to a list of medicine, referred to as s Network-entry-level formulary Day-to-day benefits are subjected to the network’s protocols, which are the rules and provisions set by the Network. Benefits are also subjected to the Network’s list of applicable tariff codes. What to do when wanting to see a doctor? You may visit any Doctor on the Ingwe Active primary care network. To check which doctors are in the area, you can call 0860 102 493 or visit Momentum website at Ingwehealth.co.za Momentum allows members to use any doctor on the Ingwe Active Primary Care network doctor. If you visit a non-Network doctor, you will have to use the emergency / casualty visit and pay R100 co-pay, this visit is covered at 100% of the Momentum health rate. There is no limit to the number of times that may visits the Ingwe Active Primary Care network doctor, however all the visits for the 11th onwards must be pre-authorised by contacting the call centre on 086 0102 493 How and where to find Doctor near your area To check which doctors, you can call 0860 102 493 or visit the website ingwehealth.co.za To apply for the Ingwe option for your chid please contact Nmahla or Tammy in our Health Department, email health@daberistic.com ,  Financial planners advise clients on how best to save, invest, and grow their money. They can help you tackle a specific financial goal—such as readying yourself to buy a house—or give you a macro view of your money and the interplay of your various assets. Some specialise in retirement or estate planning, while some others consult on a range of financial matters.

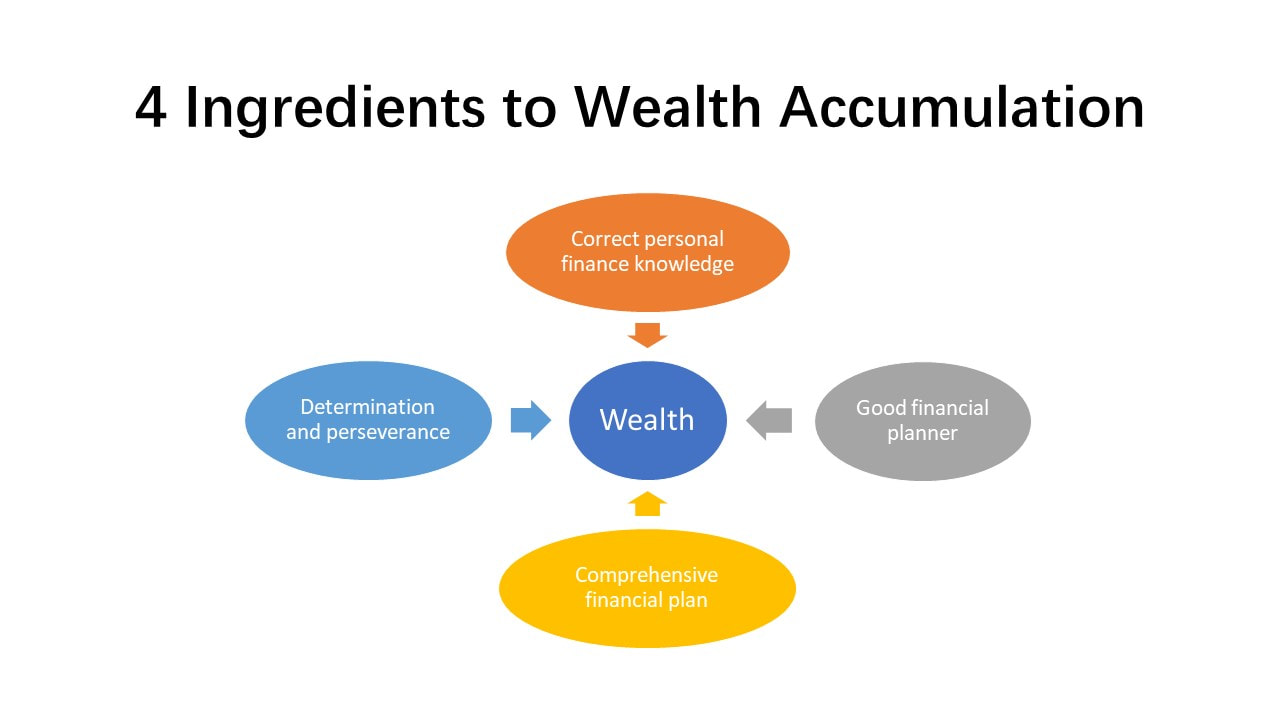

Don’t confuse planners with stockbrokers — the market mavens people call to trade stocks. Financial planners also differ from accountants who can help you lower your tax bill, life insurance agents who might lure you in with complicated life insurance policies. Anyone can hang out a shingle as a financial planner, but that doesn’t make that person an expert. They may tack on an alphabet soup of letters after their names, but CFP (short for certified financial planner) is the most significant credential. A CFP has passed a rigorous board exam administered by the Certified Financial Planner Board of Standards about the specifics of personal finance. CFPs must also commit to continuing education on financial matters and ethics classes to maintain their designation. The CFP credential is a good sign that a prospective planner will give sound financial advice. Still, even those who pass the exam may come up short on skills and credibility. As with all things pertaining to your money, be meticulous in choosing the right planner. Typically, financial planners earn their living either from commissions or by charging hourly or flat rates for their services. A commission is a fee paid by a life insurance company whenever someone buys a policy. For reasons we’ll explain later, you may want to avoid financial planners who rely on commissions for their income. These advisers may not be the most unbiased source of advice if they profit from steering you into particular products. A growing number of financial planners make money only when you pay them a fee for their counsel. These independent financial planners don’t get a cut from life insurers or fund companies on investment products. You might pay them a flat fee, such as R25,000, for a financial plan. Or you could pay an annual fee, up to 1% of all the assets—investment, preservation fund, retirement annuity, education fund and tax-free investments — they’re minding for you. Others charge by the hour, like lawyers. Yes others charge a monthly subscription. You might also encounter financial planners who cater exclusively to the rich and refuse clients with less than R5,000,000 to invest. Don’t take it personally - hugely successful planners would just prefer to deal with big accounts rather than beginner clients. You want a planner who’ll make the time to focus on your concerns and is interested in growing with you. Should You Use a Financial Planner? You can certainly go it alone when it comes to managing your money. But you could also try to do it yourself when it comes to auto repair. In both areas, doing it yourself is a brilliant idea for some, and a flawed plan for many, many others. Mastering personal finance requires many hours of research and learning. For most, it’s not worth the time and ongoing effort. As you get older, busier and (it is hoped) more wealthy, your financial goals – and options – get more complicated. A financial helper can save you time. Financial planners can also help you remain disciplined about your financial strategies. They’ll make the moves for you or badger you until you make them yourself. Procrastination can cause all sorts of money problems or unrealised potential, so it pays to have someone riding you to stay on track. We’re not suggesting that you ignore personal finance and turn over all your concerns to an adviser. But even if you know the basics, it’s a comfort to know that you have someone keeping watch over your money. Any good, independent financial planner considers a vast range of laws and regulations, together with the relevant range of products to give you customised advice, while keeping your personal circumstances in mind. Financial planners therefore need to understand tax implications and product offerings available in the market. They need to keep abreast of ever-changing financial landscapes and legislation, while always being mindful of politics and the economy. But ultimately, your financial planner needs to put you, your goals and your needs first, above all else. By using an independent planner you have the peace of mind that the planner is not under pressure to punt products of certain product suppliers. It may sound crazy to give someone 1% of your annual assets to manage them, but you get a buffet of advice about almost anything related to personal finance. The price becomes sensible when you consider that you’re paying to establish a comfortable retirement, save for your child’s college or choose the right mortgage when borrowing millions of rands. How to Find the Right Financial Planner It’s best to go with a certified financial planner (CFP), which is an instant signal of credibility – but not a guarantee of same. To start, ask people like you if they can recommend a planner. If you have kids, ask a colleague who also has children. If you’re single and just out of college, check with a friend in the same boat. If possible, you want to find a planner with successful experience advising clients in the same stage of life as you. For more leads, check the Financial Planning Institute of Southern Africa. A few more tips for finding the best planner for your situation: Consider the planner’s pay structure. You typically want to avoid commission-based advisers. Planners who work on commission may have less than altruistic incentives to push a certain life insurance package or investment product if they’re getting a cut of that revenue. But fee-based advisers aren’t perfect. Advisers earning 1% of your annual assets might be disinclined to encourage you to liquidate your investments or buy a big house, even if those are the right moves at a particular point in your life, because their fee would shrink. If you’re starting out and don’t have a trove of assets, a planner who charges by the hour or a fixed fee could be the best fit. These planners are best for when your needs are fairly simple. Typically, hourly planners are just building their practice, but that usually means they’ll take the care to get your finances right. After all, they’re relying on your recommendation to grow their business. Finally, many experienced advisers do hourly work because they enjoy working with younger clients who can only afford to hire someone at that rate. Run a background check on your planner. Start with these two questions: Have you ever been convicted of a crime? Has any regulatory body or investment-industry group ever put you under investigation, even if you weren’t found guilty or responsible? Then ask for references of current clients whose goals and finances match yours. Check to ensure the credentials the person claims to have are current. Google them, see who administers the designation, then call that administrator to verify that the credential is valid. Beware of market-beating brags. Warren Buffet outperforms the market averages. There aren’t a lot of people like him. If you have an initial meeting with an adviser and you hear predictions of market-beating performance, get up and walk away. No one can safely make such guarantees, and anyone who’s trying may be taking risks that you don’t want to take. Asking someone whether they’ll beat the market is a pretty good litmus test for whether you want to work with them. What they should be promising is good advice across a range of issues, not just investments. And inside your portfolio, they should be asking you about how many risks you want to take, how long your time horizon is and bragging about their ability to help you achieve your goals while keeping you from losing your shirt when the economy or the markets sag. Source: Adapted from WSJ.com  There are 4 ingredients to successful financial management and wealth accumulation:

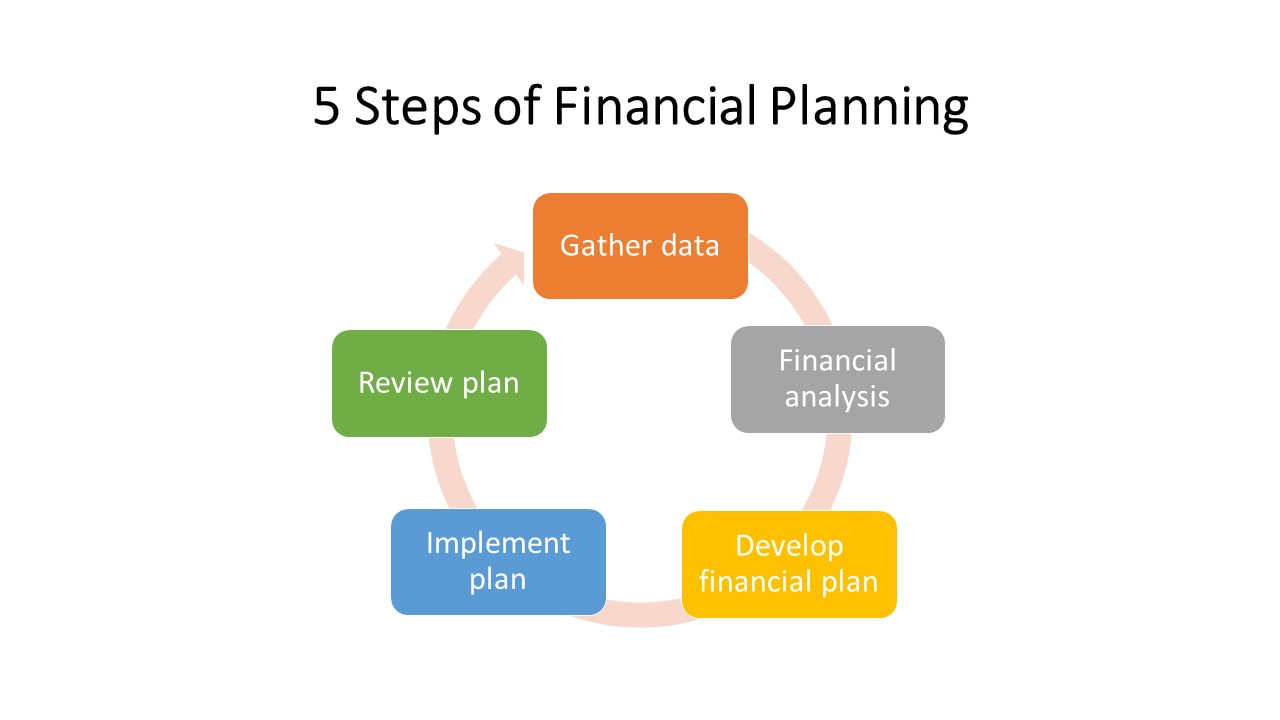

1. Correct personal finance concepts and knowledge. The right financial management concept ensures your finances are built on a solid foundation, while the right financial management knowledge enables you to manage money effectively in your daily life. Previously we talked about the concept of money. I will share with you the knowledge of financial planning and financial management tools in the future. 2. A good financial planner. Today there is plethora of investment and insurance products to meet the diverse needs of the public. The laws governing finance, investments, insurance, taxation and personal property are cumbersome and complicated. To a layman, it is like finding the right path in a labyrinth. In this environment, if a person has high income or high wealth, wants to accumulate wealth, or wants to create a big business, he needs a good financial planner and advisors to give advice and services in financial investment. A good financial planner is your trusted coach and your partner on the road to getting rich. In the future, I will share with you how to choose a financial planner. 3. A sound financial plan. A good plan gives us goals and directions, so that we can be on the right path to disciplined financial management. Last time we talked about the financial planning process. 4. Determination and perseverance. Focus on the goals, the end outcomes. No matter what happens along the journey, adapt, make a plan, persevere. Persistent implementation of your financial plan will help you achieve your goals. For Christian readers, the ultimate factor in successful financial management is trust and obedience to God. God is the Lord of our lives, and He will supply us with all that is needed in Christ Jesus. The Bible exhorts us to "just rely on the God who gives us all things to enjoy."  There are five steps in the financial planning process:

1. Gather data. This includes the short-, medium- and long-term lifestyle and financial goals for you and your family; personal balance sheet (a list of your assets and liabilities), personal income statement (monthly income and expense items), the stability of your income, and your financial portfolio (listing all your investments and policies). 2. Financial analysis. Based on the information and numbers you have, analyse and identify gaps in your personal financial planning. This could be about balancing your books every month (expenses not greater than your income), save a specific amount every month, life insurance, medical aid, car and household insurance, investments, wills and estate planning. 3. Develop a financial plan. Based on your analyses, develop a comprehensive plan that is clear, has specific goals and targets and action items. This will help you focus your mind on where you want to go, and how you are going to get there. 4. Implement the financial plan. This is about doing, taking action. This may be about keeping a monthly budget, money and budget management, buy financial products that help you achieve the various parts of your financial plan. 5. Regularly checking in and revising your plan. Your job, your work, your income, your family, your circumstances and needs are likely to change over time. Review your plan to check if there are any goals or details you need to change, and if you are on track to reaching your financial targets. The plan needs to be personalised and adapted for you. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|