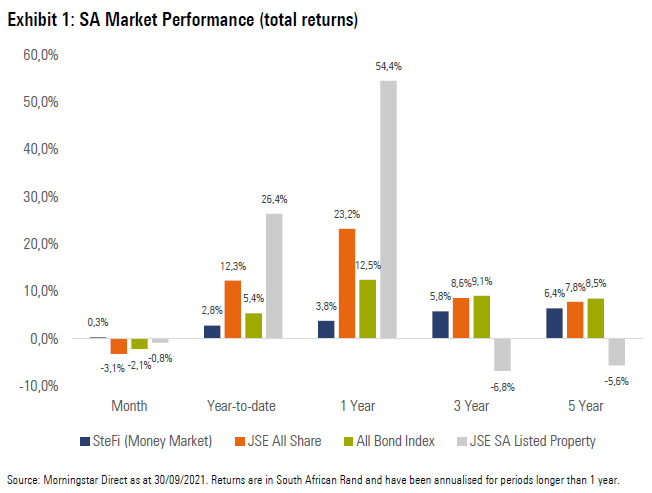

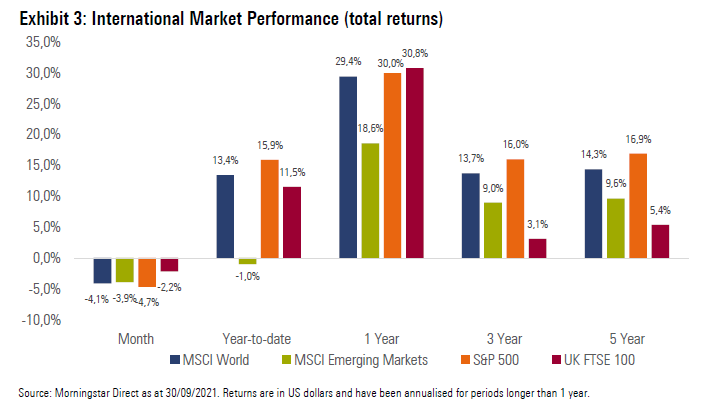

South African Market Commentary South African equities tracked global markets lower during the month, as poor performance from Resource counters and large Industrial index constituents weighed on the performance of the local equity index. Local bonds had a tough month, ending lower, as global risk aversion and expectations of the tapering of asset purchases in the US lead to higher yields (and lower prices) on SA bonds. Local listed property ended the month slightly in the red, as the sector continues its slow recovery from rental relief provided as a result of Covid-19, with many counters prioritising balance sheet improvement, resulting in lower-than-average distribution payments. The rand was weaker against most of the major developed market currencies, as global risk aversion and a stronger US dollar acted as headwind to the performance of emerging market currencies. South Africa moved to an adjusted level 1 lockdown on 1 October, as Covid-19 infections continued to decline across the country, which allowed President Cyril Ramaphosa to lift restrictions slightly. The South African Reserve Bank’s (SARB) Monetary Policy Committee (MPC) announced that interest rates will remain on hold at its meeting in September, which was largely expected, despite the SARB assessing the risks to the short-term inflation outlook to be to the upside. In terms of the GDP growth outlook, the SARB announced that they expect growth for 2021 to be significantly higher at 5.3%, largely due to the stronger Q1 and Q2 GDP prints as well as the impact of historical revisions. What is of more concern, however, is the downward revision of expected GDP growth for 2022 (to 1.7% from 2.3%) and 2023 (to 1.8% from 2.4%), which is indicative of the fragile state of the SA economy. SA headline CPI moved higher to 4.9% year-on-year for August (from 4.6% in July), as rising transport and food prices made up the largest components of the inflation increase during the month, the former affected by the 91c per litre petrol price hike during August  Global Market Summary Global equity markets performed poorly in September, as slowing global growth, concerns around the spread of the Covid-19 Delta variant and liquidity concerns at China’s second largest property developer, Evergrande, dampened risk appetite. Evergrande indicated during the month that the company has cash flow problems, with reports surfacing that it is at risk of defaulting on money borrowed from China’s shadow banking system. This comes on the back of increased regulatory scrutiny in China from the ruling Chinese Communist Party, with the recent issues at Evergrande raising questions about the overall health of the Chinese economy. The US Federal Reserve (Fed) met during the month, with the Fed expected to announce the tapering of asset purchases at its next meeting in early November, with the goal of completing its balance sheet expansion midway through 2022. This would suggest that the Fed will shrink its current $120 billion per month quantitative easing programme by approximately $10-$15 billion per month. Click here to read more.  Source: Morningstar

0 Comments

Last month we talked about Set Up Short-term Goals. This month we focus on Step 9 - Set Up Long-term Goals.

I define long-term goals as something you would like to achieve in the long term, generally in more than 10 years' time, but can also be anything in more than two years. Have your notebook and pen ready at your desk. Think about the things your plan for after the next two years, in five years, ten year or longer. It can be related to your age, for example age 45, 60, 65, important anniversaries, for example 20th wedding anniversary, or milestones for your children, for example age 7 going to primary school, age 18 going to university. Jot them down in your notebook. Speak to your spouse, partner, children, families and friends that you would like to plan things together with, jot down the additional things that are going to happen after the next two years. Be specific in your goals. Visualise what you would like to happen, write down the details of your goals. The more specific your goals are, the more you will be driven to achieve them. So instead of saying "living in a retirement home at the coast", make it more specific by saying "living in a two-bedroom retirement home in a secure estate in Hermanus, Western Cape by age 65". Make your goals more specific by applying the 5W2H method, asking these questions: What? Why? Where? When? Who? How? How much? Examples or ideas are:

You can now develop the list of long-term goals into a spreadsheet in your notebook, or use a spreadsheet such as Excel or Google Sheets, with the following columns: Column 1: Description of the goal Column 2: With whom (you will be doing this with) Column 3: Date (and age) Column 4: Amount required (this is the amount of money required for that goal) Column 5: Bank/investment account for this purpose Column 6: Notes/Comment (this is where you expand, to explain who will contribute, whether you will contribute for someone else, someone else will contribute for you, how you are going to build up the fund, monthly or an ad-hoc lump sum) Column 7: People/skills/resources required Column 8: Status - Not started, in progress, completed For some of these goals, in particular investment or business goals, you should develop a business plan with the necessary details. Access the required skills, such as business, financial, bankers, legal, engineering, investment professionals, to help you develop a proper business plan. Write your goals on colour stickers or magnets, stick them on your wall so they are visible, acting as reminders to you. Work out your monthly and annual plans to attain these goals. Revisit your long-term goals spreadsheet quarterly, or at least annually, to check whether you are on track, or anything you still need to do. Certified Financial Planners are trained to help people develop a holistic financial plan, focused on your long-term financial wellbeing. It is advisable to use the services of a qualified financial planner to develop your financial plan, to identify areas you may have not considered. In partnership with Morningstar, Let’s kick off the comparison with a quote by Ryan Holmes – “You can run a sprint or you can run a marathon but you can’t sprint a marathon.” The same principle can be applied to saving for retirement. Training to run a marathon is very similar to saving for retirement.  In partnership with Morningstar - I came across some recent research and thought you would find it valuable. I therefore share it with you and would love to hear your thoughts.. In short, it does a good job highlighting that true financial success comes from two viewpoints: actual financial progress (the numbers) and financial wellbeing or empowerment (the feeling of success or security). These are both important to me, and hopefully you too, as the evidence shows we must achieve both. Current State It would be great for you to think about your financial success via these two perspectives and let me know where you stand on a scale of 0 to 10 for each. I hope we can agree that we’ve made solid progress on both fronts, especially given the challenging last 18 months, but please let me know if that isn’t the case and I’ll do my best to help. Of course, some clients would rather not be involved in the intricacies of their financial plans. Perhaps simply by having us on your team is enough to feel financially empowered. If so, that is great. The importance of financial empowerment To demonstrate the evidence, the graph below compares people who feel empowered by their finances with people who don’t. It shows that people who feel empowered had mostly positive experiences with their finances, even in the lowest income ranges. Those who felt disempowered were less happy than their peers and didn’t reach the positive range until their annual earnings were well above $100,000 (this is US based, so equates to around R1 500 000).  I

Source: https://www.morningstar.com/lp/when-more-is-less Achieving both sides of financial health As your adviser, my primary job is to crunch the numbers, but I also like to see myself as your partner in prosperity on your road to financial success. The lesson here is fascinating: A sense of financial wellbeing—as well as the money itself—may be the key to success in our financial lives. So, if there are some behavioural traits, such as reinforcing good investing habits, that I can help with – please reach out to me. For example, as it stands, it is likely you have enough assets to withstand a reasonable economic shock, but that doesn’t mean that you can’t and/or won’t be anxious about your finances. On the other end of the spectrum, I sometimes have clients that aren’t in the greatest place economically, and despite their best intentions, they still spend carelessly because they feel fine about their finances. If we want to be truly successful, we must find a balance between the two. I hope you find this different perspective useful. If you would like me to elaborate further on the above, or any other matter—I’d be delighted to chat. If you would to set up a meeting with Financial Planner please contact Kevin emails: service@daberistic.com tel:(011)658-1333 Written by: Kevin Yeh in partnership with Morningstar |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|