|

Here are useful guidelines when making a complaint to an insurance company in order to try to resolve the complaint before going to the Ombudsman:

* It is usually best to complain in writing. But if you phone, ask for the name of the person to whom you speak, as well as the reference number for the call. Keep a note of this information, with details such as the date and time of your call and what was said. With the smartphone technology available nowadays, you may also make a recording of the telephone call. This may be required at a later stage. * Remain calm and polite, however emotional, angry or upset you may be. You are more likely to explain your complaint clearly and effectively if you can stay calm. * Initially attempt to contact the person with whom you originally dealt. If he/she cannot help, indicate that the matter will be taken further. Seek details of the insurer’s complaints procedure. Attempt to take up the matter with a senior official at the insurer. * When you write a letter of complaint, set out the facts as clearly as possible. * Write down the facts in a logical order and stick to what is relevant. Include important details such as your claim number or your policy number. * Keep copies of any letters between you and the insurer. This may be in the form of email, electronic documents, scanned copies or hard copy.

R1050 R1300 R2 650 R3 300 R5 250 R6 500 Source: Bonitas  Discovery is bringing some of these great enhancements and additions in 2017:

Click here for detailed enhancement overview  Nowadays most medical schemes have a new-generation option that will typically be a hospital plan with a small savings portion. This means the consumer has the peace of mind that he can go to a private hospital for procedures and has a small savings account for day-to-day expenses. (Tip: Check at which rate your scheme covers hospitalisation.

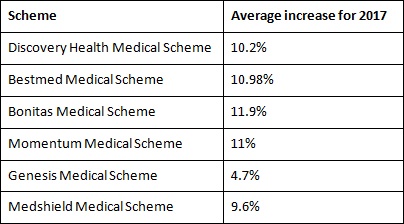

What is a medical savings account? The medical savings plan is designed to cover day-to-day expenses. The consumer gets a total annual amount that is available in advance in his savings account for medical expenses. If a consumer joins the medical scheme during the year, this amount will be calculated pro rata. In terms of legislation this amount may not exceed 25% of his annual premium. Once the benefit has been exhausted, the consumer will be responsible for any further day-to-day expenses. Any positive balance in the savings account at the end of the year will be carried over to the next year. If the member exhausts his savings component before the end of the year and switches to a new scheme or resigns from the scheme, the scheme may expect the member to repay the difference in savings to the scheme. The amount repayable by the member is the monthly savings multiplied by the number of months left in the year. Hospital plans with a savings component work on the same principle as the hospital plan, the only difference being that day-to-day expenses such as visits to doctors or dentists are paid from the savings component. This savings component forms part of the premium – you are actually saving your own money to cover day-to-day expenses. Please contact Namhla or Judy in our Health Department, email health@daberistic.com , to find out about different Medical aid options Source: medicalaid.co.za  The pressures of the current economic climate, a rise in claims from members, the high cost of healthcare technology, and the fact that medical schemes have to pay for the treatment of PMBs at private hospitals and private doctors at cost all contribute to a spike in medical scheme contribution costs. Many schemes are under pressure, and are forced to increase their member contributions, while trimming their benefits – always an unpopular thing with scheme members. Bestmed announced a 10.98% average increase on 7 October for the year 2017. The increases range from 9.89% and 12.35% on the various options. CEO of Bestmed Dries la Grange called the increase "very competitive" and said that Bestmed was somewhat less affected than other schemes by a high claims pattern. He also said that Bestmed benefited from being a member-owned administrator with a huge focus on wellness. Bonitas announced an 11.9% increase for all Bonitas options on 29 September. Poor economic growth, increased interest rates, inflation and basic costs of living put pressure on consumers, said Dr Bobby Ramasia, principal executive officer of Bonitas. He also mentioned other contributing factors to the financial pressure, which are a falling rand, the rising cost of hospital admissions, fraud, wastage and abuse, and the cost and increased use of Prescribed Minimum Benefits (PMBs). The table below details of some of the announcements on contribution increases from some of the schemes (not all schemes have announced their increases):  Please contact Namhla or Judy in our Health Department, email health@daberistic.com , to find out what your increase will be for 2017.

Source: Finance24 Please note that our Short Term service providers will not be accepting new applications from 15 November 2016 - 15 January 2017 for any Commercial and Domestic policies. The service providers are :

If you are a medical aid holder and would like an option upgrade from 1 January 2017,please note that all option upgrades have to be submitted by latest 30 November 2016 to us as your Broker. This applies for the following service providers:

|

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|