|

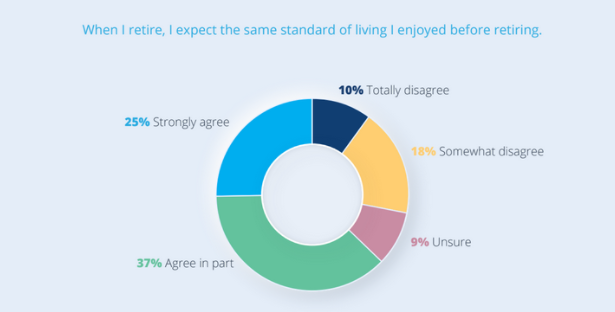

The 2021 edition of the 10X Retirement Reality Report points to a deteriorating pension outlook for South Africans. In the wake of the Covid-19 pandemic, even fewer now look forward to a comfortable retirement, says Chris Eddy, head of investments at 10X Investments. This is evident across all age groups, demographics and income levels. The 10X report is based on the annual Brand Atlas Survey, which tracks the lifestyles of the 15 million economically active South Africans in households earning more than R8,000 per month. Alarmingly, this modest cut-off already excludes two-thirds of households in the country. In total, 71% of respondents indicated they had no retirement savings plan at all, or just a vague idea of one. That is a lot of people who could be forced to rely on the kindness of family and friends, or to live off South Africa’s meagre older person’s grant (state pension) of R1,890 per month (R1,910 for those older than 75), said Eddy. Within the ‘fortunate’ minority, half the respondents still don’t save because they have nothing left at the end of the month. And even among those who are saving, just 7% anticipate a comfortable retirement; 79% fear they won’t have enough or feel unsure. Most survey respondents (74%) believe they will have to generate some income after they retire. Another 19% are not very sure, leaving just 7% of respondents feeling confident that they are on course for what is increasingly becoming an outdated notion of retirement, based on full financial independence. Breaking this down into different income groups: a mere 6% of those with a household income of R50,000 and above feel sure they will not have to keep earning after they retire. For both other income groups, it was just 7%. This highlights once more that achieving a financially secure retirement is less about how much we earn, and more about how much we engage in the process, inform ourselves and save.  But how much is enough, and how do we start a savings plan to get there? Several leading financial services firms weigh-in: The 80% rule Schalk Louw, portfolio manager at PSG Wealth, notes that many experts recommend using the 80% rule as a benchmark for what you will need to cover your monthly expenses once retired. “I won’t personally guarantee the accuracy of this figure, but it does give us a basis to start from,” said Louw. If you currently earn R15,000 per month, and apply the 80% rule, you will need at least R12,000 per month after retirement to maintain your current living standard. Unlike food products, human beings don’t have a “use by” date, so we have to rely on a safe withdrawal rate to ensure that we do not outlive our savings, said Louw. According to this rate, you should be able to withdraw 5% of your portfolio yearly without having to use any of your remaining capital, he said. “This approach is based on the fact that the historical return on the South African stock market (since 1964) was about 8% higher than the local inflation rate and that you would expect to earn slightly less than that in a typical balanced fund portfolio. “By limiting your withdrawals to 5% of your portfolio, you should still have an additional 5% to 6% growth to cover inflation in the long run.” Based on a 5% annual withdrawal rate after retirement, Louw said that the amount you will need to save in rand terms would look something like this: R12,000 x 12 months = R144,000 (annual income) ÷ 0.05 (5% safe withdrawal rate) = R2,880,000. If you don’t properly compensate for inflation in your portfolio, you may fall short of your required total after retirement, said Louw. “Let’s assume that you are 40 years old and you plan to retire at age 65 (25 years). By using the top of the South African Reserve Bank’s target range, the best-calculated guess we can offer on annual inflation is around 6%. The 4% rule Traditionally, financial advisers, savers and retirees have relied on the 4% rule when working out how much to save for retirement and what kind of annual income retirement savings would provide, noted financial services group Discovery. Simply put, the rule says that if retirees withdraw 4% of their savings annually (adjusting this amount for inflation every year thereafter), their nest egg will last at least 30 years. The rule also requires retirement savings to be split equally between shares and bonds. This method, Discovery said, is also used to determine the lump sum investors need to provide an acceptable annual income when they retire. For example, if you retire with a final salary of R480,000 a year, you need a replacement ratio of 90% of your final salary, which amounts to R432,000. To ensure you do not use all your saved retirement capital in 30 years, R432,000 should be 4% of your total savings, Discovery said. This means you would need R10.8 million saved to draw 4% or R432,000 annually. Put another way:

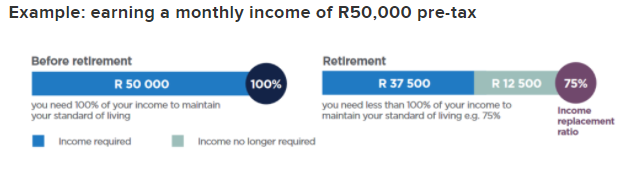

For example, Bengen’s rule is based on the average long-term annual returns (since 1926) of shares and bonds being 10% and 5.3%, respectively.  75% rule Plan to have 75% of your current pre-tax income, says financial services firm, Sanlam. “You will most likely need less than 100% of your current income to live comfortably when you retire as some expenses fall away once you retire.” Ask yourself these questions:

Allan Gray offers a similar guideline around saving. Aim for an income of 75% of your final salary.

It is widely held that a retirement income equal to 75% of your final salary will allow you to live comfortably during retirement, it said. “This figure accounts for the adjustments many people make as they age, for example, no further retirement savings contributions but higher medical costs.” To assess how much you will potentially need, consider the following factors:

Aim to put away at least 17% of your salary from age 25 “Assuming that you will be comfortable living off 75% of your pre-retirement salary, our research indicates that saving 17% of your salary is a reasonable starting point for the 25-year old saver. “This amount increases dramatically the later you start. You need to save 22% if you start saving at 30, up to 42% if you start at 40, and up to 59% if you start at 45,” Allan Gray said. It is important to note that these numbers are simply averages and assume a consistent, inflationary salary increase each year, that you retire at 65 and that you earn an average return of consumer price inflation (CPI) plus 5%, it said. The 15% rule The general rule of thumb for a comfortable retirement is 15%, noted Gus Van Der Spek, a developer of upmarket retirement village Wytham Estate. “15% of your salary should be put aside for your entire working career of around 40 years. For those wanting to retire in luxury, 20%-plus is advised. Also, bear in mind that what R1 is worth now will differ by the time that you retire,” he said. Van Der Spek shared the advice given to him by financial planners saying, “multiply your needs by 300. Simply put, if you currently live on R50,000 per month, multiply this by 300 to determine what you will need to maintain a luxury lifestyle post the age of 60.” Van Der Spek’s comments dovetail retirement expert Andre Tuck, a senior Investment consultant at 10X Investments. Tuck pointed to three old school ways to ‘guesstimate’ your retirement goal:

He added, however, that if you are hoping to do things you didn’t do during your working years, for example, travel, you should rather multiply your final salary by 17, or even 20.

“The more money you have available to invest once you retire, the better your lifestyle will be and the more likely you will be to withstand the impact of unexpected events, such as the current pandemic,” he said. If you would like to speak to a Financial advisor about planning for your retirement contact Kevin tel(011)658-1333 email: service@daberistic.com Source: Businesstech

0 Comments

Last month we talked about setting long-term goals. This month we focus on the next step: Focus on building assets. This is a topic I am very passionate about, and I have helped many clients do this.

The accounting definition of an asset is this: Things that are resources owned by a company and which have future economic value that can be measured and can be expressed in Rands. Examples include cash, investments, accounts receivable, inventory, supplies, land, buildings, equipment, and vehicles. I prefer Robert Kiyosaki's definition of an asset: An asset is something that puts money in your pocket. Examples are buy-to-let property, cash-generating businesses, shares, unit trusts, investments that pay you interest, gold, silver. You should spend your lifetime accumulating assets that put money in your pocket. Understanding assets and investing in good assets are a lifetime journey. Let’s unpack in some detail the type of assets that put money in your pocket. Bank deposits: This is an asset that is familiar to most people. The common types of bank deposits are call deposit, notice deposit, fixed deposit and money market account. Bank deposits quote an interest rate and pay you a monthly interest, as your money stays invested. The interest rate is linked to the Reserve Bank’s Repo rate. When the Repo rate goes up, the interest you receive increases. When the Repo rate goes down, the interest you receive decreases. Click here to watch the episode on bank savings and investment products RSA Retail Savings Bond: This is a type of government bond offered to the general public, the term is 2-, 3-, 5- and 10 years. The interest rate is between 7.25% and 9.5%. Participation bond: Fedgroup is famous for offering this type of investment. A participation bond is a regulated collective investment scheme, it offers you an attractive fixed interest rate in a five-year term investment. Click here to watch the episode on Fedgroup Participation Bond Unit trusts: This is popular among retail investors and institutional investors alike. Unit trusts are also known as collective investment schemes in South Africa. They are registered, approved and regulated by the financial conduct regulatory FSCA. There are over 2,000 unit trusts in South Africa and over 120,000 funds in the world. In North America and other parts of the world, unit trusts are known as mutual funds. Unit trusts are a convenient way to invest, offering investors many choices, ranging from local equities, offshore equities, property, bonds, income, money market, regions, industries such as technology, single country. Exchanged traded funds (ETFs): It has gained huge popularity and attracted a lot of money around the world over the last twenty years. It is also growing fast in South Africa. Exchanged traded funds are like unit trusts, the main differences are they are listed on a stock exchange, so it is freely traded throughout the day, its price fluctuates during the day, and it generally follows some type of benchmark. These funds are rules based, or passively managed, and they have lower fund management fees compared to actively managed unit trust funds. Shares: You can buy shares using a stockbroking account. When you buy shares in a company, you become a shareholder of that company, even if you only own one share. You are entitled to receive dividends declared and paid by the company. If the company does well and it share price rises, you benefit from the capital gain. Pension fund/provident fund: If your company or business has a pension/provident fund, your contributions and your employer’s contributions are invested in Regulation 28 compliant funds, to grow your retirement savings. Preservation fund: When you leave an employer, it is advisable to preserve your pension/provident fund money in a preservation fund, to preserve tax benefits and continue to invest your money, instead of cashing money out. Most product providers now require a minimum sum of R50,000. You can transfer your money from your pension/provident fund to a preservation fund. Tax-free investment: This is an investment vehicle that allows you to invest tax-free. You may invest up to R36,000 in a tax-free investment account in a tax year, all your growth within the account is tax free for life. This is what I recommend to most clients as their first investment building blocks. Click here to watch the episode on tax-free investment Retirement annuity: Retirement annuity allows you to contribute to a fund pre-retirement and enjoys tax deductions, to build up your retirement capital. All your investment growth before retirement age is tax free. Your contributions are invested in Regulation 28 compliant funds. Cick here to watch the episode on retirement annuity Endowment: This is an investment product with an initial five-year term. You take out an endowment with a life insurance company. Your investment growth is taxed within the product, the life insurance company will calculate the tax applicable and deduct the tax from your growth. When you withdraw or surrender your policy, you will receive the money tax free. Endowments have certain tax advantages for high-income individuals. It also offers protection against creditors. Click here to watch the episode on endowment Living annuity: When a member's pension fund, provident fund or retirement annuity fund reaches retirement age, he is obliged to use part of the proceeds (a minimum of two thirds) to invest in an annuity, to receive a monthly income. In a living annuity, an investor essentially has a retirement investment account. He can invest in a portfolio of unit trusts, and he can determine the level of drawdown to provide him with an income. The annual drawdown rate can be between 2.5% and 17.5%. Life annuity: With life annuity, a person enters into a contract with a life insurance company. In return for a lump sum paid to the life insurance company, the life insurance company pays the person (life assured) a monthly income. The life insurance company guarantees that income until the life assured's death. Certain options can be effected at the outset, to prolong the payment period to the beneficiary. Alternative investment: An alternative investment is a financial asset that does not fall into one of the conventional investment categories. Conventional categories include stocks, bonds, and cash. Alternative investments include private equity or venture capital, hedge funds, managed futures, art and antiques, commodities, and derivatives contracts. Hedge funds: A hedge fund is an investment vehicle that caters to high-net-worth individuals, institutional investors, and other accredited investors. The term “hedge” is used because these funds historically focused on hedging risk by simultaneously buying and shorting assets in a long-short equity strategy. Section 12J investment: Section 12J of the Income Tax Act was introduced in 2009 by the South African Government to encourage South African taxpayers to invest in local companies and receive a 100% tax deduction of the value of their investment. The investor receives a share certificate and a tax certificate, allowing the invested amount to be deducted from the investor’s taxable income, in the year the investment is made. Gold and silver: Precious metals have been the store of value since the ancient of days. While it does not give you interest or pay you dividends, it protects you against inflation, or central banks unlimited money printing. You can buy gold and silver coins from reputable precious metals dealers online. Cash-generating business: Starting your own business can be scary, but also exciting. Businesses have proven a sure way for many people to generate wealth, for some generational wealth. By having your own business, working on it with your sweat, tears and grit, you benefit from the fruit of your Labour. There is no guarantee for success. In fact, statistics show that 95% of businesses fail within the first five years. With the right mindset, goal setting, planning, the right mentors and advisors, you can greatly improve your chance of success. REITS: REITs, or real estate investment trusts, are companies that own or finance income-producing real estate across a range of property sectors. These real estate companies have to meet a number of requirements to qualify as REITs. Most REITs trade on major stock exchanges, and they offer a number of benefits to investors. Buy-to-let property: Buy-to-let refers to the purchase of a property specifically to let out, that is to rent it out. A buy-to-let mortgage is a mortgage loan specifically designed for this purpose. Buy-to-let properties are usually residential but the term also encompasses student property investments and hotel room investments. Cryptocurrency: In this day and age, we have to consider cryptocurrency as a viable asset. While it is highly speculative, it is backed by a very useful Techonology called Blockchain. Given people’s suspicion of governments and central banks, there has been a move to decentralize currencies and financial transactions. There are thousands of crypto currencies in the world, while many of them are just scams, the main ones like Bitcoin, Etherium, Binance Coin, Ripple and USD Coin look like they are here to stay. As you can see, there are a plethora of asset choices and investment options. Take time to do you research to properly understand an asset class. Work with a qualified financial advisor as your financial coach, to decide on which assets may be best for you to accumulate. It is not one size fits all. it is not one asset class fits all. For all clients, I advise them to diversify across a few asset classes.  Festive season is finally approaching and that means it’s time for holidays. After many countries being on lockdown for the past 18 months and more people getting the vaccine, we can see that more and more countries are opening up for tourists. In the time of such a pandemic it also reminds us how important it is to have medical cover abroad. This cover is known as, The International Travel Benefit covers costs associated with a relevant health service obtained outside of South Africa for a condition or health event that occurs as a result of an accident or emergency.

Most medical schemes include International Travel Benefit for members. With some medical schemes you need to ensure that you need to activate your International Travel Benefit before you travel. With Discovery Health you do not need are to phone ahead to “activate” this benefit, all you need is your departure and re-entry stamps in your passport as proof! Depending on your chosen medical aid option, your cover limit will either be R5 Million or $1 Million and that will alleviate the burden off your shoulders knowing that you will be able to receive the best medical attention whilst on your travel adventures. Principal members and beneficiaries are covered for up to 90 days from the date of departure. Benefits apply to medical emergencies, and are limited to between R5 million and R10 million per trip. Cover can extend to an emergency medical evacuation or repatriation. It's important to note that International Travel Benefit is often excluded from low cost entry level plans. Members of the Discovery Health KeyCare Series and the BonCap option by Bonitas, for instance, are not covered, and will have to make alternative arrangements. What's excluded from cover? There are certain instances when medical aids will not pay for emergency treatment overseas. Common exclusions are:

The medical emergencies claims process If a medical emergency requires surgery, expensive procedures and/or an extended stay in hospital, you need to get authorisation and a payment guarantee from your medical aid's travel partner. In less expensive scenarios, you'll usually be expected to pay the costs from your own pocket, and claim the money back from your medical aid on your return to South Africa. A nominal co-payment may apply for treatment conducted out of hospital. Travel insurance Whether your medical aid option offers international travel benefits or not, it's a good idea to optimise your cover. In some cases – like when you pay for your air ticket with your credit card – you'll automatically get free travel insurance. If you'll be travelling for more than 90 days, or are planning to go dividing, skiing, summit a mountain peak or visit potentially dangerous areas, it's best to purchase comprehensive travel insurance as a separate product. This also means you'll enjoy benefits such as cover for lost baggage, stolen goods and cancelled flights. Important when travelling during Pandemic You may require a vaccine certificate, you may download on website https://vaccine.certificate.health.gov.za/ or contact EVDS tel: 0800 029 999 to request a vaccine certificate. They will need the below information:

If you would like to activate your International Travel Benefit, please contact Namhla or Jo in our Health department, email service@daberistic.com, Tel 011-6581333, Option 2 for Medical Aid. Source: IFC  The nightmare of load shedding continues in South Africa and we share in this article the risks that can affect your insurance during load shedding, advice how to prepare for loadshedding and how ensure that that you are accurately covered if you need to claim for a loadshedding or power surge related incident. Risks that can affect your insurance during load shedding 1. Generator and other alternative power sources It’s vital that alternative power supplies like generators are installed and certified by accredited electricians. If these devices are installed or used incorrectly, you might not be covered for any damages that may result. Before rushing off to buy your own alternative power supply first check how it’ll affect your home insurance. 2. Power surges Power surges that blow your appliances usually occur when the power come backs on. During load shedding, you can switch off all your appliances to prevent them from being damaged when that surge happens. The quickest and least expensive solution for protecting appliances is plugging them into a power strip with a built-in surge protector. These power strips are usually equipped with a fuse that is designed to fail in the event of a voltage spike, cutting off power to your appliances and protecting them. There are multiple power strip options available, so we encourage you to speak to a certified electrician about your options before deciding to purchase a specific one. 3. Fire risks when candles are used for lighting Make sure to always be cautious when working with any flammable materials, ensure you keep a handheld fire extinguisher in your home and have it serviced regularly. Also make sure everyone in the house knows where it is kept and how to operate it. 4. Opportunistic robbery, theft and burglary resulting from tripped and false alarm triggers. When there is load shedding there is a good chance that your home security measures may be affected, which may raise concerns around the safety of you and your family. If you secure your home with a motorised gate and a home alarm system, you may wonder if you’re going to be covered for theft and any other type of loss in the event of load shedding. In most cases, most insurance companies recognises that the cause of the loss was ‘beyond your control’ and will consider your claim for theft where your security systems did not function properly because of load shedding. How to prepare for loadshedding 1. Know what your alternative power options are, and the pros and cons of each. Do your homework on what safety requirements there are for installation. Also, research what the costs may be so that you can chose an option that will suite you and your budget.

2. Follow the load shedding schedule and unplug appliances and sensitive equipment: Unplug appliances or electronic devices that may be vulnerable to power surges. This includes cell phones, computers, servers and LCD screens, all of which could be badly damaged when the power comes back on due to a spike in electricity flow. 3. Test your alarm system: During load shedding, alarm power packs and batteries may wear out faster. This may also cause alarm systems to produce false alarm signals or even malfunction altogether. Many insurance policies require that you perform an annual or bi-annual alarm system check, which must be logged by your security company. Failure to do so could impact your claim, Colman warns. 4. Install reserve power: To ensure that electric fencing and gates still work during load shedding, reserve batteries should be installed and maintained. While reserve batteries generally last for six to eight hours when the power goes out, load shedding dramatically decreases a battery’s lifespan. 5. Secure your premises: Not only will this reduce the risk of the theft occurring, but it will also make the claims process a lot easier in the event that a theft or robbery occurs. 6. Light up your premises: Using solar power or battery-operated lighting can reduce the chance of opportunistic crime occurring. Keep them fully charged. 7. Be vigilant: Criminals may see blackouts as an opportune time to strike. Keep a torch in your car should you arrive home in the dark and need to open your perimeter security gate manually. Make sure you are accurately covered

Source: Santam, Businesstech; News 24

In partnership with Morningstar: At the 2021 Morningstar Investment Conference, Victoria Reuvers had the privilege to sit down with Tamryn Lamb, Head of Retail Distribution at Allan Gray and Joanne Baynham, Wealth Manager and AssetTV Presenter to discuss, The evolution of the local and global investment landscape. In partnership with Morningstar: Dan Kemp answers these questions, Will we see slower GDP growth than what we anticipated six months ago? Do we see a slow rise in interest rates on the horizon or a fast one? Will interest rates stay the same or go down? |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|