The nightmare of load shedding continues in South Africa and we share in this article the risks that can affect your insurance during load shedding, advice how to prepare for loadshedding and how ensure that that you are accurately covered if you need to claim for a loadshedding or power surge related incident. Risks that can affect your insurance during load shedding 1. Generator and other alternative power sources It’s vital that alternative power supplies like generators are installed and certified by accredited electricians. If these devices are installed or used incorrectly, you might not be covered for any damages that may result. Before rushing off to buy your own alternative power supply first check how it’ll affect your home insurance. 2. Power surges Power surges that blow your appliances usually occur when the power come backs on. During load shedding, you can switch off all your appliances to prevent them from being damaged when that surge happens. The quickest and least expensive solution for protecting appliances is plugging them into a power strip with a built-in surge protector. These power strips are usually equipped with a fuse that is designed to fail in the event of a voltage spike, cutting off power to your appliances and protecting them. There are multiple power strip options available, so we encourage you to speak to a certified electrician about your options before deciding to purchase a specific one. 3. Fire risks when candles are used for lighting Make sure to always be cautious when working with any flammable materials, ensure you keep a handheld fire extinguisher in your home and have it serviced regularly. Also make sure everyone in the house knows where it is kept and how to operate it. 4. Opportunistic robbery, theft and burglary resulting from tripped and false alarm triggers. When there is load shedding there is a good chance that your home security measures may be affected, which may raise concerns around the safety of you and your family. If you secure your home with a motorised gate and a home alarm system, you may wonder if you’re going to be covered for theft and any other type of loss in the event of load shedding. In most cases, most insurance companies recognises that the cause of the loss was ‘beyond your control’ and will consider your claim for theft where your security systems did not function properly because of load shedding. How to prepare for loadshedding 1. Know what your alternative power options are, and the pros and cons of each. Do your homework on what safety requirements there are for installation. Also, research what the costs may be so that you can chose an option that will suite you and your budget.

2. Follow the load shedding schedule and unplug appliances and sensitive equipment: Unplug appliances or electronic devices that may be vulnerable to power surges. This includes cell phones, computers, servers and LCD screens, all of which could be badly damaged when the power comes back on due to a spike in electricity flow. 3. Test your alarm system: During load shedding, alarm power packs and batteries may wear out faster. This may also cause alarm systems to produce false alarm signals or even malfunction altogether. Many insurance policies require that you perform an annual or bi-annual alarm system check, which must be logged by your security company. Failure to do so could impact your claim, Colman warns. 4. Install reserve power: To ensure that electric fencing and gates still work during load shedding, reserve batteries should be installed and maintained. While reserve batteries generally last for six to eight hours when the power goes out, load shedding dramatically decreases a battery’s lifespan. 5. Secure your premises: Not only will this reduce the risk of the theft occurring, but it will also make the claims process a lot easier in the event that a theft or robbery occurs. 6. Light up your premises: Using solar power or battery-operated lighting can reduce the chance of opportunistic crime occurring. Keep them fully charged. 7. Be vigilant: Criminals may see blackouts as an opportune time to strike. Keep a torch in your car should you arrive home in the dark and need to open your perimeter security gate manually. Make sure you are accurately covered

Source: Santam, Businesstech; News 24

0 Comments

The COVID19 Pandemic has undoubtedly affected many people and businesses – particularly many restaurants who had to limit their capacity and even close temporarily for a certain period. Besides the reduced business volume on an ongoing basis, the complete national lockdown resulted in a tremendous loss of income.

Many businesses started asking if short-term insurance cover such loss of income. There were two fundamental issues – first, as per the policy wording, an infectious disease pandemic is not an insured peril, because short-term insurance covers physical risks such as fire, flood, accidental, damage, theft, etc Secondly, the lockdown was a result of direct government intervention instead of the risk. For these reasons, the pandemic was not an insured peril. Insurer Hospitality & Leisure (H&L) – a division of the largest South Africa short-term insurer Santam – saw the devastating impact on their clients in the hospitality sector and decided to offer a Relief Payment to qualifying clients, who had both Business Interruption cover (loss of income) and the Infectious Disease extension. As a result, these clients received payment during the 2020 national lockdown, which boosted their cash flow during the difficult period. Furthermore, H&L emphasized that if the final claim amount ends up being less than the relief payment, the client does not have to refund the additional portion. Some of our own clients at Daberistic essentially benefited from insurance on this very exceptional basis. Testimonial One of our clients XYZ Company (Not real name), were paid R500,000 in 2020 as a relief payment. They then submitted their claim, and the final claim amount was actually R300,000 which means the client got R200, 000 more than what they should have received, and they were not required to pay it back. This once again demonstrates the value of insurance and how sizable and reputable insurers can play a critical role at a time when you need it most. Insurance has an invisible yet crucial role to play in our society, to ensure the stability of our financial system and, more importantly, people’s livelihood. If you would like us to do a quote or do a comparative quote on your current insurance email: service@daberistic.com tel: 011 658 1333 Written by: Edmond Lee (Short-term Broker)  The Financial Sector Conduct Authority (FSCA) and the Prudential Authority (PA), in a statement say they have reached an understanding with non-life insurers that are most affected by business interruption cover claims that they will consider interim relief to their policyholders who have the appropriate contagious disease extension, while legal certainty on this matter is being sought from the courts.

The interim relief will take the form of once-off payments to policyholders to enable them to continue running their businesses while awaiting the outcome of the legal process. This arrangement follows discussions between the authorities and the non-life insurers. The discussions were primarily aimed at addressing two main issues which are of concern to the FSCA. The first is the impact of the repudiation of contingency business interruption cover claims by some non-life insurers (and delays in processing policyholders’ claims) and the second is the impact of this matter on the reputation of the non-life insurance industry, the statement says. The authorities say they acknowledged in previous communications that business interruption cover is a complex issue. There are different business interruption policies. Those that have an extension for infectious/contagious diseases and the latter constitute approximately 3 to 5% of the policies. The FSCA says it is its view that claims in respect of cover with an extension for infectious/diseases in terms of these policies should be honoured where they meet the terms of the contract and that lockdown should not be used as a ground to repudiate these claims. This approach has also been adopted by some international conduct regulators but is being challenged by insurers and reinsurers globally and locally, which means that legal certainty will have to be obtained from the courts. The legal certainty will undoubtedly take time to achieve, with dire consequences for policyholders who have already been impacted severely by Covid-19 and the national lockdown, and it is in their interest that the authorities and the affected non-life insurers have reached understanding that interim relief payments should be made. The interim relief to be provided by non-life insurers will differ from case to case depending on reinsurer support, financial impact and the number and types of policyholders. The FSCA and PA say they have established the following guiding principles to be applied in determining the interim relief: The interim relief should at the very least focus on those businesses most impacted by lockdown (for example, the hospitality industry) and also on small businesses; The funds provided to a policyholder as interim relief shall not be claimed back by any non-life insurer from a policyholder should the courts decide in favour of insurers. However, should the courts find in favour of policyholders, these funds will be deducted from the total claim amount payable to a policyholder by a non-life insurer; and This relief should be on either an interim basis pending legal certainty or if non-life insurers wish to offer a full and final settlement, such settlement should reflect reasonable value to a policyholder and the implications thereof should be clearly explained in writing should a policyholder wish to accept the settlement on this basis. The authorities support the relief measures that will be provided by many of the non-life insurers that offer business interruption with the extension for infectious/diseases in line with these principles and view them as a necessary and appropriate interim response to the current situation, particularly when one considers that the said non-life insurers are providing financial relief to their policyholders without the support of their reinsurers at this stage. The exact details of relief measures by insurers to their policyholders will be communicated directly by each insurer to their brokers and policyholders. ADVERTISING The authorities say they have agreed with the most affected non-life insurers that, despite the time-barring clauses in the business interruption policies, non-life insurers would not raise the defence of prescription should policyholders decide to lodge court actions against non-life insurers at a later stage. For reinsurance purposes, non-life insurers may require policyholders to lodge their claims before certain dates and the authorities request policyholders, their brokers and legal representatives to co-operate with non-life insurers in this regard. “The authorities will continue to work with non-life insurers that are most affected by these business interruption cover claims to ensure that claims are resolved as quickly as possible and that trust and confidence in the non-life insurance industry can be restored. The efforts by these insurers to provide interim relief to their policyholders with no intention of claiming the funds back from their policyholders is appreciated by the authorities,” the statement says. If you would like to get a quote for your Business insurance contact Edmond and Marizka in our Short-term department email shortterm@daberistic.com, tel (011)658-1333 Source: Personal Finance  As a most loved local business, your clients rely on you to keep your doors open - even when disaster strikes. Business interruption insurance is designed to protect your business against lost profits should your property be damaged or destroyed by fire or natural disasters like flooding, earthquakes or tornadoes. Here are five must-know facts about this type of cover to safeguard your profits.

1. It’s cover added on to existing business insurance cover In order to have this type of cover, you need to have fire or property business insurance in place. While property insurance covers physical damages, business interruption insurance covers the profits you would have earned if it was business as usual. 2. Must-have for most types of businesses as part of their survival plan Can you imagine keeping up with orders if your most important piece of machinery burns down? Can you fathom having to close your doors for months – while still paying all your staff and bills? After working so hard to build up a fan base, can you imagine them going to your competitors? Most businesses should see business interruption insurance as a must-have survival plan. Work with your broker to plot out your worst-case-scenario and how you would deal with a disaster, especially for:

3. What business interruption insurance covers...and what it doesn’t A business interruption insurance policy will be tailormade to your business operations and turnover, but typically covers the following: Profit: You will receive funds to cover the profits you would have earned during the time you had to close your doors. This sum is based on the income of previous months and the forecast of trends in the future. Temporary relocation: While your premises are being repaired, it will cover costs for you to move to and operate from a temporary location. Fixed operational expenses: Based on historical costs, the policy would cover any expenses and costs that you continue to incur even though you’re not operating. E.g. wages, water, lights. Fines and penalties: Covering costs to service providers including any fines or penalties for being in breach of contract.

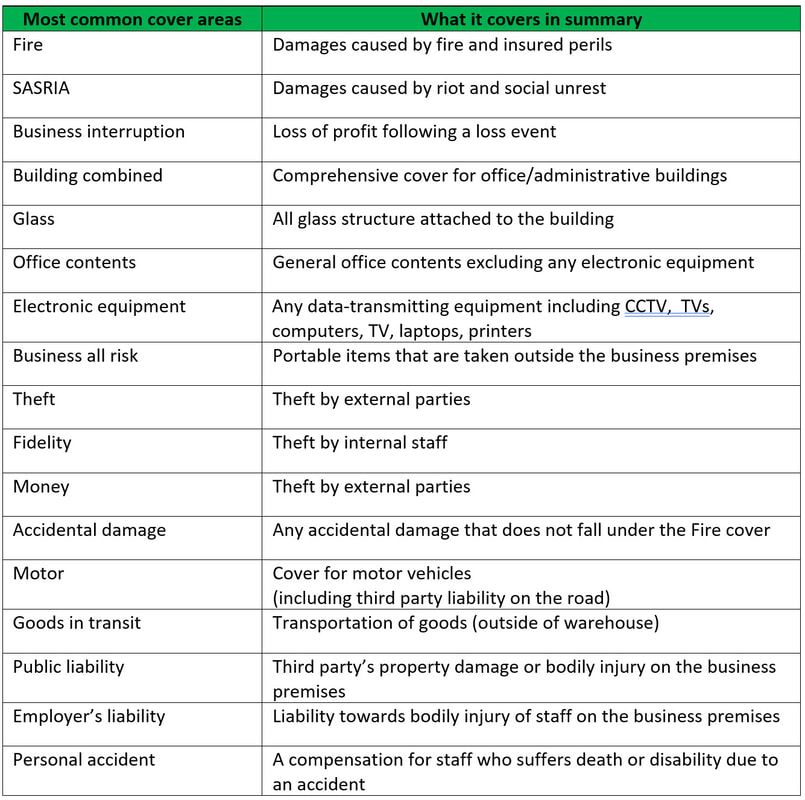

4. Accurately calculate your gross profit One of the common pitfalls of business interruption insurance One of the common pitfalls of business interruption insurance - where businesses find themselves underinsured - is when they don’t properly work out their gross profit. Your broker will help you ensure that this amount includes VAT and reflects either a 12-month period (if your maximum indemnity period is 12 months or less) or multiples of the annual turnover (where the maximum indemnity period is more than 12 months). There is a difference between what you know as a Financial Gross Profit, and an Insurance Gross Profit. The latter excludes costs/expenses that vary in direct proportion to a change in turnover. Examples are purchases, bad debts, discounts allowed and direct commission. If, for example, turnover or sales dropped by 10%, so would each of these costs. 5. Work out a sufficient indemnity period Your broker can help you set the right indemnity period for your business. This should allow you enough time to remove damaged property, replan your business (including getting building plan approval), reorder stock and machinery, rebuild your property (including any installations), recover lost markets and restore your turnover to what it would have been had the disaster not happened. Remember, there is no one-size-fits-all approach to getting a business back on its feet. With Santam’s small business insurance solutions, we can help you protect the business you’ve worked so hard for. Speak to your broker to find out more about the essential insurance cover for your unique business needs. If you would like to get a quote for your Business Interruption , please contact Edmond in our Short-Term department, email shortterm@daberistic.com , tel (011)658-1333 Source: Santam  Author: Edmond Lee Commercial insurance is a necessity for business owners, but at the same time it is a rather complicated area to understand. We at Daberistic believe in simplifying insurance for our clients, so this article will shed some lights on the basic structure of commercial insurance in South Africa. In the early eighties there were many short-term insurers, flooding a variety of commercial insurance policy wordings onto the market. A sensible comparison of benefit between these policies was virtually impossible, which was to the detriment of the small business insurance consumer. Hence the regulator responded by introducing a standard business policy - known as "Multimark" - in 1987. Over time, Multimark was revised, and today we have the Multimark 3 wording available to us. Even though insurers have since introduced various endorsements to differentiate their products, the basic structure remain largely the same, as the Multimark’s risk-based approach is a solid foundation which ensures that various sections in the policy cover various risks and premium are calculated accordingly. As an example, Fire has a low probability of occurrence but high severity (i.e. all stocks can be affected) if it occurs, as opposed to Theft which has a higher probability but lower severity (because robbers or burglars cannot possible steal all your stock), which explains why covers are broken down into various section. Below is a table summarising the various key sections and their cover areas.  The scope of commercial insurance is broader than the above and continues to evolve as the risk landscape changes, resulting in other covers such as Products liability, Directors’ and Officers’ liability, Cyber crime, Commercial crime, Credit insurance – just to name a few. It is therefore crucial that you make use of an insurance advisor who can advise you on your risks and propose covers that meet your needs.

We at Daberistic believe that by providing the right advice and solution to clients, we can create win-win relationships which will ultimately benefit everyone. If you are looking for advice on your short-term insurance needs, you can contact us on the following channels:

Starting a business is a huge achievement, while the greatest challenge is to sustain and develop it.

One of the most important business conversations an entrepreneur can have is with a professional risk advisor who can objectively interrogate the nature of your business, its unique needs, reliance on its supply chain, the range of likely risks and how to mitigate the impact of such in a worst case scenario. Many businesses have the usual property and assets cover for their buildings, vehicles and other essential equipment. All good and well if you have an accident, theft or fire and your policy is able to take care of the replacement of the physical assets, but what happens if you are also unable to trade for weeks, even months and your revenue declines or even stops altogether as a result? If the only road to your luxury B&B in the Drakensberg is blocked off for a month due to a landslide or sinkhole, how would you recoup the lost income of no guest bookings? If your fast-food franchise burnt down and it took three months to rehabilitate the site and rebuild the store, how would you pay staff, rent, taxes, franchise fees and so on? If a multimillion Rand, imported machine in your component factory explodes and the replacement from overseas is three months down the line, how will you pay your creditors? None of these costs stop simply because you’re unable to trade due to a physical disaster or force majeure. Businesses can purchase contingent business interruption coverage, an aspect of business interruption insurance, where the insurance is triggered by property damage at the premises of a supplier or customer, or other trigger such as loss of utility, denial of access or the act of a local authority which results in a financial loss you may suffer. The intention of Business Interruption insurance is to restore the business to the same financial position as if the loss had not occurred as well as to cater for additional increased costs/ expenses incurred to minimise further loss of revenue and lessen the time to do so, subject always to the terms and conditions of the policy. Business interruption claims are normally linked to material damage/property damage. While your property or assets insurance covers the damage to physical property or equipment and replaces the actual assets, business interruption is vitally important to tide your business over in terms of the lost income as a result of physical damage, until you get back to operating your business as usual. What does Business interruption insurance cover? Although the specifics of cover vary from one insurer to another, the basic tenets of BI are:

Finally, it’s important to engage with a qualified, expert broker who can assess how your different business insurance covers mesh together to create a veritable safety net against the many challenges besetting SMES. Business Interruption cover is simply one of a number of important risk products that businesses need to safeguard their continuity. A clear description of a business and its operational environment is central to the drafting of a well-conceived insurance strategy. A comprehensive risk assessment will greatly aid in identifying the potential hazards, in addition to determining what physical precautions and management processes should be in place. It’s also very important to have an accurate assessment of the replacement costs of buildings, contents, vehicles, IT, stock and other assets, particularly in the event of a catastrophic loss. By linking professional advice to an aligned insurance program that covers virtually all the ‘what if’ scenarios of not only physical damage, but the knockon implications for business continuity, Aon clients get to experience the real depth of value of a comprehensive risk analysis backed with professional advice and expertise. Let us assist you do a risk assessment for you or your business contact Jan in our Short-Term Department; email shortterm@daberistic.com, tel (011)658 -1333 Source: Cover magazine |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|