Several South African insurance companies are excluding damages related to the possible failure of Eskom’s national grid, which could result in a catastrophic event.

“This decision has arisen as reinsurers have indicated they would not provide coverage in event of a total grid failure. This effectively leaves insurance companies with no option but to consider grid failure as an uninsurable risk,” says Guy Jameson, Sales Operation Consultant at GIB. Sasria has also stated that it would not be liable for any pay-outs in the event of a total grid failure, because loadshedding is not an insurable risk. Although the country has not suffered a total grid failure, insurers are seeing increasing claims following loadshedding to clients’ equipment. Loadshedding is different from a grid failure, so some insurers have not excluded claims following a power surge, even though loadshedding is not an insured peril. Companies need to start thinking about disaster management plans in the event of total grid collapse. There are warnings of possible looting and civil unrest, with the consequences of severe damage to infrastructure across the country and where Eskom would likely face difficulties in getting the grid operational due to its extensive national footprint. Although the likelihood of a total blackout is low, the consequences of such an incident could be devastating, making it worth preparing for. Although a total blackout presents several dangers, the primary threat is the time it takes to bring a system back up from that total collapse with estimates stretching into weeks rather than days. Major considerations for organisations developing blackout plans are the eventual failure of South Africa’s telecommunications networks and financial systems together with water and fuel shortages. “This scenario could see current logistics and supply chains becoming unstable, increasing the potential for fuel shortages. Generators requiring diesel could become less reliable than backup solutions such as solar-powered systems. From an IT perspective, regular data backups are always a must for any business but considering possible eventualities, they are now more important than ever,” adds Jameson. Experts are suggesting that business continuity planning for load-shedding and grid failure are very different. The first can usually be managed within the business premises, with on-site power, water and other backups which will allow the business to continue to operate efficiently for a few hours. However, in the case of a large-scale outage, the same is required but for a greatly extended period and in addition to backups for critical resources that cover tech, telecoms, water supply and logistics. GIB says initial commentary from insurers has been somewhat ambiguous in terms of what is covered and what is not. What seems to be clear is that there is a definite push to avoid any losses associated with grid failure. “This raises questions around consequential loss and whether it can be directly associated with a particular claim. If grid failure results in any other public supply being affected (for example, water), then any consequential loss might also not be covered,” he says. So, what exactly will be covered? “If a defined event takes place at your premises as a direct result of grid failure (fire, stock deterioration that has caused financial loss to the business), there will be no cover. Should this occur, you need to consider the consequences of this with your insurance advisor so that a well-considered and structured response is in place,” says Jameson. Glossary of terms: The different terminology relating to power failures can become quite confusing, so in short: Loadshedding is a controlled interruption of the electricity supply to the public, to prevent damage to the electricity grid. Grid failure occurs when there is more electricity demand on a network than available supply, which loadshedding has helped to avoid for years. When demand exceeds supply, it will cause an imbalance in the system, resulting in the grid operating at a lower frequency than what it is designed for, resulting in a total or partial interruption, interference, suspension, blackout, and/or failure of the electricity grid supply. A power surge is a sudden rapid variation of the voltage magnitude / electrical transient voltage or a power spike in any electrical system. Due to its sudden unforeseen nature, insurers invariably cover losses due to these occurrences if so, stated in their insurance schedule and mainly relating to mainly domestic, but have capped their exposures to certain limit. Source: FA News Written by: Guy Jameson, Sales Operation Consultant at GIB

0 Comments

Imagine submitting a claim to your insurance company, only to have it rejected based on information you don’t understand. What should you do, when the insurer just does not understand your view? Well, meet the insurance ombudsman – it is his job to care about your dispute!

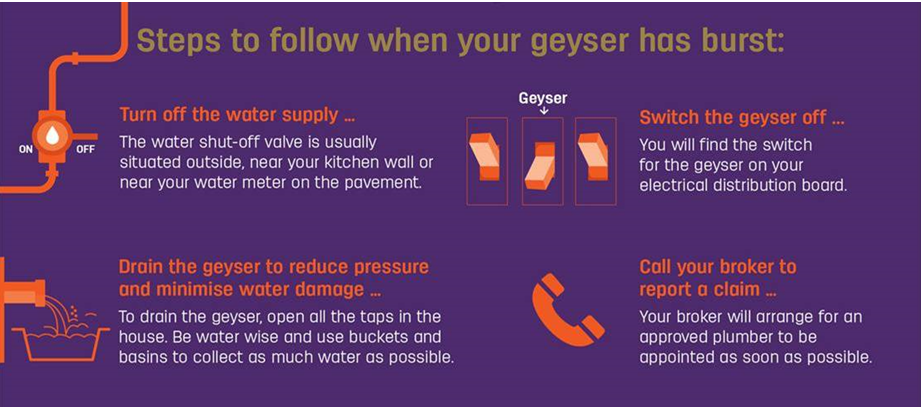

An ombudsman is an official whose duty it is to represent the interests of the public, by investigating and addressing complaints of maladministration or a violation of rights; are usually appointed by the government or parliament; and is not supposed to be influenced by political parties or affiliations, but should be able to conduct an independent investigation into the complaint that was laid. In short, the ombudsman serves as a mediator. South Africa has the various ombudsman available to its citizens, but today we will focus on the short term and long term insurance ombudsman and its roles and responsibilities; both of which are recognised in terms of the provisons of the Financial Services Ombud Schemes Act. Every short-term insurer has agreed to abide by the decision of the Ombudsman and this can relate to any of the following personal lines of short-term insurance: motor; house owners (building insurance); householders (content insurance); cell phone; travel; disability; credit protection insurance; commercial insurance; claims disputes; etc. The Ombudsman for Long-Term Insurance has the main duty of resolving complaints through mediation, recommendation and then, as a last resort, determination (or rulings). These determinations or rulings are legally binding on the contributing insurer, but not on the complainant, who has the option to go to court if unsatisfied with the ruling. The essential characteristics of an ombudsman are important, as it determines its impartiality. The insurance ombudsman should be free from interference in the performance of its duties and it should be independent from influence. They must also produce decisions that are seen to be fair, by making decisions based on the information available and having pre-set criteria for reaching a decision. Accountability to the public is ensured by having its decisions published and made available to the public. Lastly, the ombudsman should work effectively by following informal and cost-effective procedures, supported by sufficient human, financial and operational resources. So, what procedure should be followed once you realise you’ll need the ombudsman? Well, firstly, you should have tried to resolve the matter with the company concerned, by following their internal grievance procedure. If this did not solve your problem, you should contact the Ombudsman; who will require that you submit a complaint (preferably in writing) and provide them with the necessary information such as the insurance company’s name, policy number, contact details and a factual summary of your complaint. You should submit all relevant supporting documents available, including proof of your attempted resolution with the company. The ombudsman will then start its investigation and guide you through the rest of the process. Isn’t it great to know that there is someone out there who can assist you when it seems you’ve run out of options?! Make sure you have the relevant contact details of the ombudsman you need to help you solve your problem as soon as possible! By clicking on the below you will be able to get the various Ombudsman contact details: Long Term Insurance Ombudsman Short Term Insurance Ombudsman Health Ombudsman Pension Fund Adjudicator (PFA) FAIS Ombudsman ( For Investments) If you have any queries for Short-term insurance please email service@daberistic.com Source: Hollard  We continue to share a 5-part series on Home Insurance Tips. In this article we share on Solving your geyser problems. We usually don’t dwell on things that can go wrong with the geyser, the reality is that something will, at some point. Most electrical geyser manufacturers supply a warranty for the actual geyser for between five and ten years, but its individual components only carry a warranty of one to two years. What are geyser components? These are items that generally wear, such as thermostats, elements, pressure control valves, vacuum breakers, seals and gaskets. When a geyser component fails, it doesn’t necessarily mean the geyser needs to be replaced. If something goes wrong with one of these components, check with your broker if your insurance policy covers it. Most importantly, if you suspect that your geyser is leaking or has burst, report your claim to your broker so that they can appoint a qualified plumber to see to the problem. If you don’t, you may find yourself out of pocket due to limits on your policy when not using an approved plumber. Did you know?

What to look out for

If you like us to review your Home cover contact William our Short-term department email service@daberistic.com tel (011)658-1333

Source: Hollard  It’s been a challenging time for South Africans: recovering from the effects of the COVID-19 pandemic, unprecedented vehicle inflation, rising fuel prices, devastating floods and over 50 days of continual loadshedding. All citizens and businesses have been impacted by these events and this is also true for the insurance industry.

During lockdown, most insurers experienced saw a decline in the frequency of claims as a direct result of the restrictions imposed on the movement of our clients. Motor was impacted positively, and insurers saw a significant decline in accident, glass, and theft claims. Similar trends were experienced with regard to home contents, with a decline in burglary and theft claims. During this period, some insurers provided premium relief, reduced renewal increases, and refunded a portion of premiums. As restrictions have eased, there has been a return to a more normalised claims frequency trend, with adverse weather conditions in many parts of the country adding incremental pressure to claims volumes. Vehicle repair costs have increased well above inflation and the nature of vehicle thefts has changed, with newer and more expensive vehicles now being stolen. Similarly, the average cost of contents and building claims has increased to new levels, with a particular increase experienced in the number of power-surge claims. While you will be aware that rate and sum insured adjustments are routinely performed in our business, the significance of the above claims experience will unfortunately result in incremental increase adjustments over the coming months. As always, increases will remain highly segmented by policyholder and every effort has been made to limit the extent of increases as far as possible. The following excess adjustments have been implemented for Santam & Discovery Insure. Santam Vehicles: Compulsory (basic) vehicle excesses will be increased by R1 000 for all our products. The R0 excess for policyholders over 55 years will remain unaltered. Vehicle glass excesses will remain unaltered. Contents: Excesses for lightning/thunderbolt, power surge, accidental damage, mechanical/electrical/electronic damage will increase by R500 for all our products. Discovery Insure

If you would like us to review your policy please contact William in our Short-term department email: service@daberistic.com Source: Discovery & Santam |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|