|

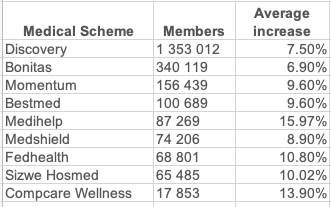

All the large open medical schemes in South Africa have announced their contribution increases for 2024. Below is the list.  Discovery Health says the average weighted increase across DHMS plans is 7.5% for 2024. Excluding the Medical Savings Accounts, the increase on Risk Contributions is 10.5%.

If you want to review your medical aid plan, please call our Health Department on 011-658-1333, Option 2 or email service@daberistic.com.

0 Comments

The flu season is here again and with this year’s flu season expected to be more severe, South Africans should seriously consider getting their influenza (flu) vaccine, a local disease expert warns. We are here to remind our Medical Aid Members that use this time to get the flu vaccine, to strengthen immunity, and let you enjoy this winter in the healthiest way possible.

Since Covid 19 came into our lives, its very hard distinguish the difference between the two. It is rather important to note that Flu and COVID-19 are very different diseases. Although Flu and COVID-19 may present similar symptoms, the viruses that cause them are not the same. COVID-19 is caused by infection with SARS-CoV-2, and flu is caused by infection with influenza viruses. To gain protection against each, you need to have the vaccine developed against each disease. You don't have to wait between COVID-19 and flu vaccinations. You can have them at the same time and, if you've had COVID-19 and recovered, it's safe to have the flu vaccine. Remember to give the healthcare provider your Medical aid company name and your Medical Aid number. Below we indicate with the different medical aid Providers , you can go about getting the vaccine through your Medical Aid Provider. Discovery Flu shot is paid from savings, or if you are on the Smart Plan, it is paid from your OTC benefit; if you are on the Core Plan, you then will need to pay from your pocket. You may go to: Medirite + Pharmacy (No dispensing and admin fees), ICPA (independent community pharmacy association), Clicks or Dis-chem. Momentum Flu vaccine is paid from Health Platform Benefit, you can either contact Momentum via WhatsApp (+27860117859), Momentum App, access your Momentum profile or call 0860117959 to notify Momentum. Bonitas Bonitas offers all members a free flu vaccine once a year. Simply go to Dis-chem, Clicks, or Pick n Pay Pharmacies. FedHealth FedHealth offers all members a free flu vaccine once a year, you need to pay R36 for admin fee. Fedhealth covers both flu vaccines, namely quadrivalent (QIV) and trivalent (TIV) vaccines. Profmed One flu vaccine per person per year is covered by Profmed Scheme. You must use a Designated Service Provider (DSP). If you want to know more about preventative benefits, please contact Namhla in our Health Department, email service@daberistic.com , Tel (011)658-1333  Due to pandemic, rising costs and high taxes are eroding pensions and retirement savings in South Africa. Many are forced to use the state-funded healthcare services which is already under pressure, causing long queues and even longer waiting lists.

There is no doubt that we want the best medical attention for our elderly parents when they fall ill therefore private health care is our solution. It is important to understand what options is best suited for your aging parent’s needs. Where do you start? You would need to sit down and discuss with your parents and obtain the following information:

Once you have answers to the above, the next set of questions you need to discuss is to do a realistic budget to finance the plan.

What if your parents cannot contribute? If your aging parents are financially dependent on you and you happen to be main member of a medical aid policy, you may consider adding them as your dependent as this means they can pay a reduced rate. However, they will be on the same option plan as you, should your option not be sufficient to cover their needs, your option is to upgrade your plan. If you’re on an option that includes savings, they become eligible for using your savings. You will need to be prepared for savings being exhausted due to extensive care required. What happens when parents don’t qualify as your dependent? If you decide to not add parents as Dependants or due to parents not qualifying to be your dependent, they can always choose a medical option according to budget and below are things to consider for when choosing your option. Full medical cover (with savings): On a comprehensive option, most elements are covered for. Such as hospital admission, chronic medication and day to day expenses, medical equipment, and possibly dentistry and optometry. These plans vary widely therefore, read through entire plan before signing up to make sure it qualifies all your parent’s needs. Basic hospital plan: These covers around 90% of hospital procedures, basic prescribed minimum benefit (PMB) condition and cancer benefit. It excludes expenses such as none PMB approved medication, equipment, doctor’s visits, optometry, or dentistry. This may not be a full coverage but highly affordable option. Gap cover is always recommended by Daberistic as this boosts your unforeseen gap payment by 500%. To read more about gap cover click here. What else to keep in mind?

If you would like cover for your parents, please contact Namhla or Tammy in our health department, email Service@daberistic.com, Tel 011-658 1333, option 2 for Medical Aid.  It’s now time to review your medical aid scheme cover for 2020. This means you have a window within which you can switch to a different plan for the new year. This window usually closes at the end of November (depending on your current provider), so don’t delay collecting the necessary information. This is not a decision to be rushed.

Why do I have to decide now? Medical aid providers allow you to switch to a higher plans once a year (at the end of the year) without penalties or consequences. If you want to save on premiums or you need to increase benefits, now is the time to do it. What if I want to change providers altogether? If you are unhappy with your medical aid provider, you can switch to another at any time of the year. But before you do, consider the following: Waiting Periods Medical Aids by law must accept anyone who applies to join their scheme. To protect themselves from older or sickly members that join without having contributed to the risk pool, they usually impose a waiting period of between 3 and 12 months. Waiting periods will apply if 1) you have not been a member of another South African medical aid for the past three months or more, 2) if you change medical schemes before 2 years of being covered with your previous medical aid provider and 3) if you have a pre-existing medical condition. Finding out about any waiting periods is extremely important before deciding to change providers. Late joiner penalty As an additional means to manage the risk of older or sickly members joining without having contributed to the risk pool, medical schemes (according to the Medical Schemes Act) are entitles to add a late joiner penalty to your premium if you were not part of a medical scheme before 01 April 2001. The late joiner penalty is calculated (using a prescribed formula) based on the number of years that you were not on a registered South African medical scheme. The late joiner fee can range between 5% and 75% of the total contribution, depending on the number of years that you were not covered by a medical scheme. Please contact Namhla or Tammy in our Health Department, email health@daberistic.com, to find out about different Medical aid options Source: Medicalaid.co.za  Medical schemes have various benefit plans available to members. Members have to choose between hospital plans, hospital plans with a savings component (New Generation Options), traditional plans, comprehensive plans and network plans.

If your savings benefit is quickly depleted at the beginning of the year and you have to pay for expenses out of your own pocket, or if your option is too expensive, it would be worthwhile to reconsider your particular medical plan. Certain schemes allow migration to other options mid-year, while others allow such changes only at the end of the year. Traditional Plans Cover almost all medical expenses and include benefits for in-hospital, day-to-day expenses and chronic medication, subject to the rules of the scheme. These plans are recommended for individuals or a family who wants comprehensive cover, but does not want a savings benefit on there option. These options still cover emergencies, hospitalisation, day-to-day expenses and chronic medication. Comprehensive Plans These options have a savings component and cover almost all medical expenses and include benefits for in-hospital, day-to-day expenses and chronic medication, subject to the rules of the scheme. These plans are recommended for individuals or a family who want comprehensive cover for emergencies, hospitalisation and day-to-day expenses and that makes use of quote a lot of chronic medication. Basic Hospital Plans Cover accounts submitted by service providers only for in-hospital expenses. You are responsible for your own day-to-day medical expenses, including emergency ward treatment. Hospital plans cost considerably less than comprehensive medical plans. However, Heydenrych recommends that you first determine the difference between the premium of a hospital plan and that of a comprehensive plan before making your choice. Please contact Namhla or Tammy in our Health Department, email health@daberistic.com , to find out about different Medical aid options Source: medicalaid.co.za  It’s tempting to want to splurge on over-the-counter vitamins and supplements or some other lifestyle item when medical aid benefits, limits and savings accounts get renewed come 1 January each year, especially after the costly festive season spending.

GTC’s Head of Healthcare Consulting, Jill Larkan, cautions however that members should spend medical aid savings prudently and use benefits wisely, particularly in the early part of the New Year. “The governing body of this sector - the Council for Medical Schemes (CMS) - recently released commentary urging members to make medical aid benefits last longer,” says Larkan. “We completely concur with the CMS. Spending sensibly from the outset helps to extend the availability of funds later in the year, while ensuring you are able to retain a positive balance in your savings account for as long as possible.” The acting Chief Executive and Registrar at the CMS, Mr Daniel Lehutjo, said in his statement that “members should resist the urge to spend all their benefits in the first couple of months” and “not to use your benefits to buy sunglasses, multivitamins or other lifestyle items over the counter.” All South African medical aids run financial years concurrent with the calendar year. This means that all the benefits (with the exception of oncology), limits and savings accounts are “renewed” on 1 January each year. When the New Year comes around a bulk lump sum of money is allocated to every member’s medical aid savings accounts and this sum is the accumulation of the next twelve, savings allocation portions, of the monthly premiums. “The lump sum of advanced annual savings needs to last until the end of December, and any non-essential items purchased now may unnecessarily increase any self-payment gaps which may require attention later in the year, once your savings are exhausted,” continues Larkan. Some additional tips from Larkan and the CMS which would help to extend members’ medical aid savings include: • Check if your medical aid has a formulary list of medications and if they do have one, request that your doctor, as far as possible, only dispenses listed medicines. A formulary is a list of prescribed medications – both generic and branded, for which your medical aid scheme will pay. The formulary helps to guide you to the most cost-effective medications that are effective for treating a particular condition. • If your scheme offers preventative screening tests, paid for by the scheme, get a list of these, and have as many done as possible, ensuring that any potential health issues are detected and addressed as early as possible. • If you take chronic medication, check that you are registered as a chronic medication member with your scheme, ensuring that as much of your monthly costs as possible are covered, by your scheme. If there is a Chronic Management program for your ailment, register for this and follow the program to improve, monitor and maintain your health. • Ensure that you know whether there is a designated service provider stipulated by your medical aid which you are required to use for various medical procedures. These service providers may include pharmacies, hospitals, doctors, specialists and even optometrist networks. Ensuring the designated service providers are used will help to curb additional expenses which service providers not in the network/s may be charging. • Obtain procedure codes and confirm authorisation and cover levels provided by your scheme. Understand what your portion of payment will be. Discuss these rates/tariffs with your doctor and negotiate these wherever possible. “By incorporating as many of these strategies as possible, members will be well on their way to maximising valuable medical aid savings. Professional advice from experienced medical aid consultants and advisors should be sought – whether through one’s employer or in a personal capacity – to ensure the retention of as much of your savings as possible,” Larkan concludes. To find out more on what your savings are from our different medical scheme providers please contact Namhla or Judy in our Health and Wellness Department, email health@daberistic.com, tel (011)658-1333 Source: FANews |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|