In our last month’s newsletter, we have mentioned Discovery is currently running a special offer, where members who join Discovery Gap before 30 June you get the first 3 month’s premium free (Subject to underwriting). Should you have no break in gap cover and have proof when you move over to Discovery Gap, underwriting will be waived. Unexpected medical costs can place financial strain on a family. Especially when service providers charge more than what your medical scheme pays. Hence why Discovery Gap cover is your gateway solution to protect you against unforeseen financial burdens. Discovery Gap cover provides shortfall cover where doctors, specialists charge above medical aid rates and works seamlessly with your Discovery medical aid. When both your medical aid and gap is with Discovery, and in an event where gap does occur, the claim is seamless, as no paperwork is required. However, gap cover cannot provide cover where medical aid does not pay towards a procedure. For example, if your medical scheme option only pays out at 100% of scheme rate, you will then be liable to pay the shortfall of the other 200% to 400% charged by your service provider as an “out of pocket” expense. If you have Discovery Gap, the system will pick up at claim stage and automatically process and settle the gap portion. Here is a testimonial of one of our clients Mrs Jenzie (Not real name) I gave birth in a private hospital in Johannesburg. The hospital bill was R32,620, Gynaes bill was R12,800 and the anaesthesiologist R4,850. Medical Aid made the following payments:

Other reasons to choose Discovery gap cover:

To apply for Gap cover contact Tammy in our Health department, email service@daberistic.com, Tel 011-6581333, Option 2 for Medical Aid.

0 Comments

With healthcare costs growing at an average of 8-10% each year, beyond inflation, which leaves medical aid clients with little choice but to downgrade their scheme benefit options to manage their cost of living. The downgrade of scheme option results in less benefits covered. This is often met with an unexpected and unaffordable bill after consultation or procedures. This has given Gap cover insurance critical spotlight to ensure medical aid clients are not faced with exorbitant amount of out-of-pocket expenses. Gap cover pays the client back policy which provides shortfall cover where doctors and specialists charge above medical aid rates of cover. Gap cover works in conjunction with your medical aid. Gap cover cannot provide cover where medical aid does not pay towards a procedure or covers the full amount for a procedure. For example, if your medical scheme option only pays out at 100% of scheme rate, you will then be liable to pay the shortfall of the other 200% to 400% charged by your healthcare provider as an “out of pocket” expense. Here is a testimonial of one of our clients Mrs K I gave birth in a private hospital in Johannesburg. The hospital bill was R15,000, Doctor’s bill was R14,500 and the anaesthesiologist R4000. Medical Aid made the following payments:

I had to pay the shortfall of R9,000 and luckily, I was able to claim from my Sirago gap cover and got my R9,000 back. *Please note we changed the name to keep identity private Gap cover may cover the following instances:

At Daberistic, our preferred provider is Sirago. Why Choose Sirago?

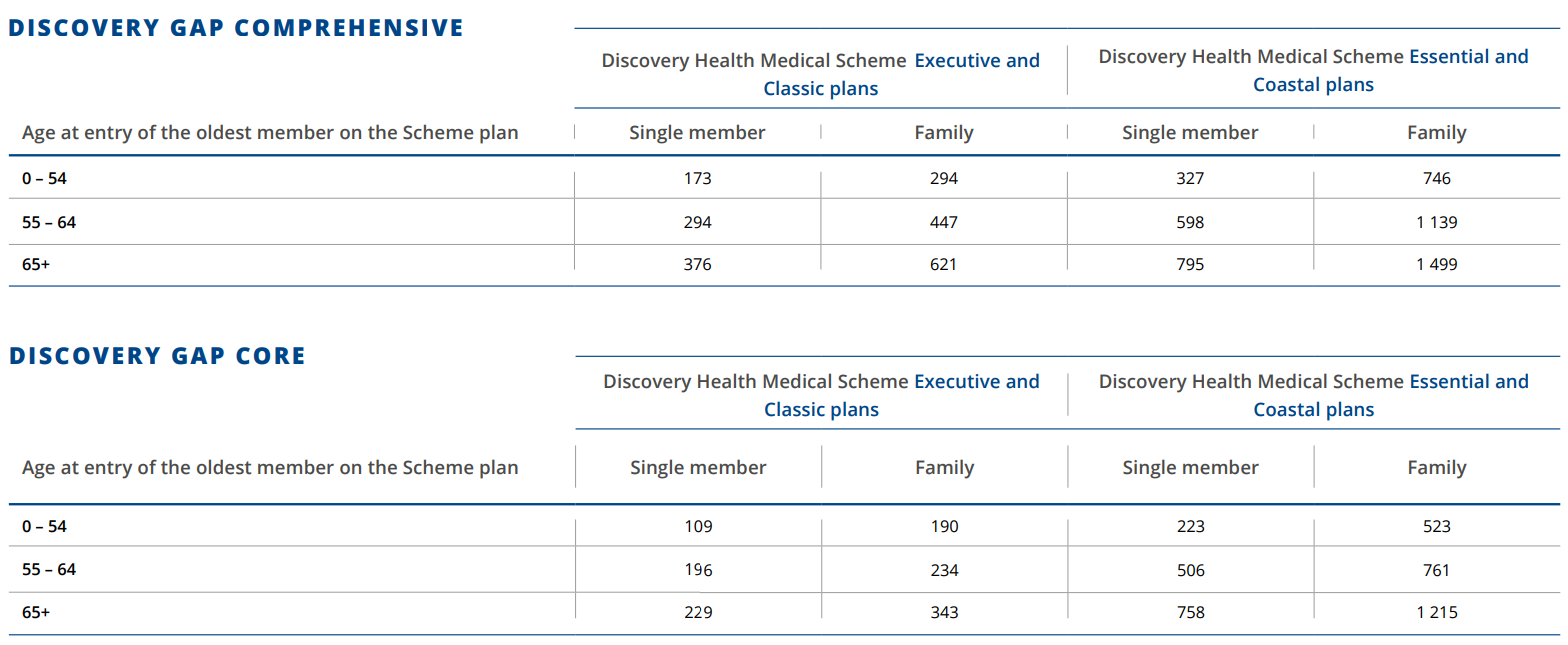

2021 Sirago Gap Cover Premium  To apply for Gap cover contact Tammy in our Health department, email service@daberistic.com, Tel 011-6581333, Option 2 for Medical Aid.

“Our Pandemic Shield policy is the first of its kind on the African continent, providing an affordable solution that pays out a lump sum stated benefit if the policyholder is hospitalised as a result of being positively diagnosed with COVID-19 – or any other World Health Organisation declared pandemic illness in the future. The benefit trigger is a hospital admission longer than 48 hours,” adds Martin. Who is Pandemic shield for? Anyone can apply. There are no medicals, and no person will be excluded. Why emplyees need Pandemic Shield Cover? Employees get a lump sum benefit and daily cash amounts if they are hospitalised because of any disease or health event declared as pandemic by World Health Organisation (WHO) What about COVID-19? Any hopitalisation longer than 48 hours, as a result of COVID-19, or SARS-CoV-2 is covered as long as you have been tested positive. Vaccinate your employees' financial wellbeing against COVID-19

*No initial waiting period will be applied but subseqient claims will be subjected to a 21 day waiting period after discharge. *Compulsory groups on Gold and Diamond larger than 50 employees will receive a discount. *Premium and benefits are not gauranteed for the duration of cover and may be reviewed from time to time based on risk factors. *This is not a medical scheme and the cover is not the same as that of a medical scheme. *This policy is not a substitute for medical scheme membership. To speak to a Medical Aid Consultant, please email service@daberistic.com,

Tel 011-6581333, Option 2 for Medical Aid.  Please be reminded that Medical aid upgrades for 2021 will end soon, please make sure you have submitted your change by 30 November. For clients on Discovery KeyCare plan, Momentum Ingwe plan, Bonitas Boncap plan and have been selected to do income verification, please make sure all required documents are submitted to prevent your service provider resulting to default to the highest income band and therefore the highest contribution will apply.

Please note: Members joining Momentum health Ingwe option with effect 01 October 2020 onwards will not be required to submit information for income verification (declaration and proof of income). They will remain on their current income bracket moving into 2021 and the new premium will automatically be applicable from 01 January 2021. For more information on medical aid plans, please see below videos, brochures and links to assist you with change of option decision. Discovery Plan series and videos

Below are Discovery Health Plan Guides Brochures for 2021

To help you stay healthy and informed on the COVID-19 situation, Discovery will continue to provide the most up-to-date information and guidance through COVID-19 Information Hub Below are Momentum Health Plan Guides Brochures for 2021 Below are Bonitas Plan Guides Brochures for 2021  It is now time to review your medical aid scheme cover for 2021. This means you have a window within which you can switch to a different plan for the new year. This window usually closes at the end of November (depending on your current provider), so don’t delay collecting the necessary information. This is not a decision to be rushed.

Why do I have to decide now? Medical aid providers allow you to switch to a higher plan once a year (at the end of the year) without penalties or consequences. If you want to save on premiums or you need to increase benefits, now is the time to do it. Generally, medical schemes give you until the end of the year to change your plan. What if I want to change providers altogether? If you are unhappy with your medical aid provider, you can switch to another at any time of the year. But before you do, consider the following: Waiting Periods Medical Aids by law must accept anyone who applies to join their scheme. To protect themselves from older or sickly members that join without having contributed to the risk pool, they usually impose a waiting period of between 3 and 12 months. Waiting periods will apply if 1) you have not been a member of another South African medical aid for the past three months or more, 2) if you change medical schemes before 2 years of being covered with your previous medical aid provider and 3) if you have a pre-existing medical condition. Finding out about any waiting periods is extremely important before deciding to change providers. Late joiner penalty As an additional means to manage the risk of older or sickly members joining without having contributed to the risk pool, medical schemes (according to the Medical Schemes Act) are entitles to add a late joiner penalty to your premium if you were not part of a medical scheme before 01 April 2001. The late joiner penalty is calculated (using a prescribed formula) based on the number of years that you were not on a registered South African medical scheme. The late joiner fee can range between 5% and 75% of the total contribution, depending on the number of years that you were not covered by a medical scheme. It is important to keep proof of all your previous medical scheme membership, as it would help reduce or remove the Late Joiner Penalty. General considerations When reviewing your medical aid plan, you should consider the following factors: - benefits - exclusions - co-payments and deductibles - provider network restrictions - financial soundness of the medical scheme - the medical scheme's service and ability to pay claims - premium (affordability) - gap cover product to supplement your medical aid. Please contact our health team, Tel 011-658-1333, Option 2, or email service@daberistic.com , to find out about different medical aid options.  Sirago has some great great updates and additions in 2020 which are:

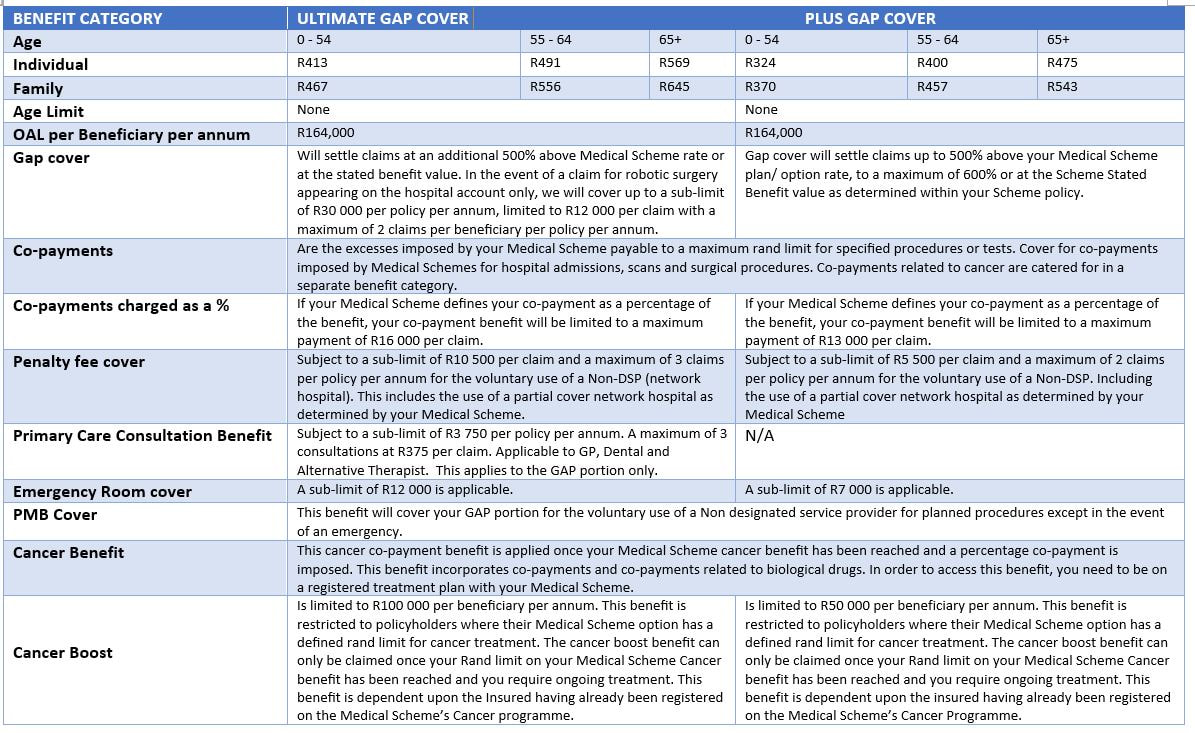

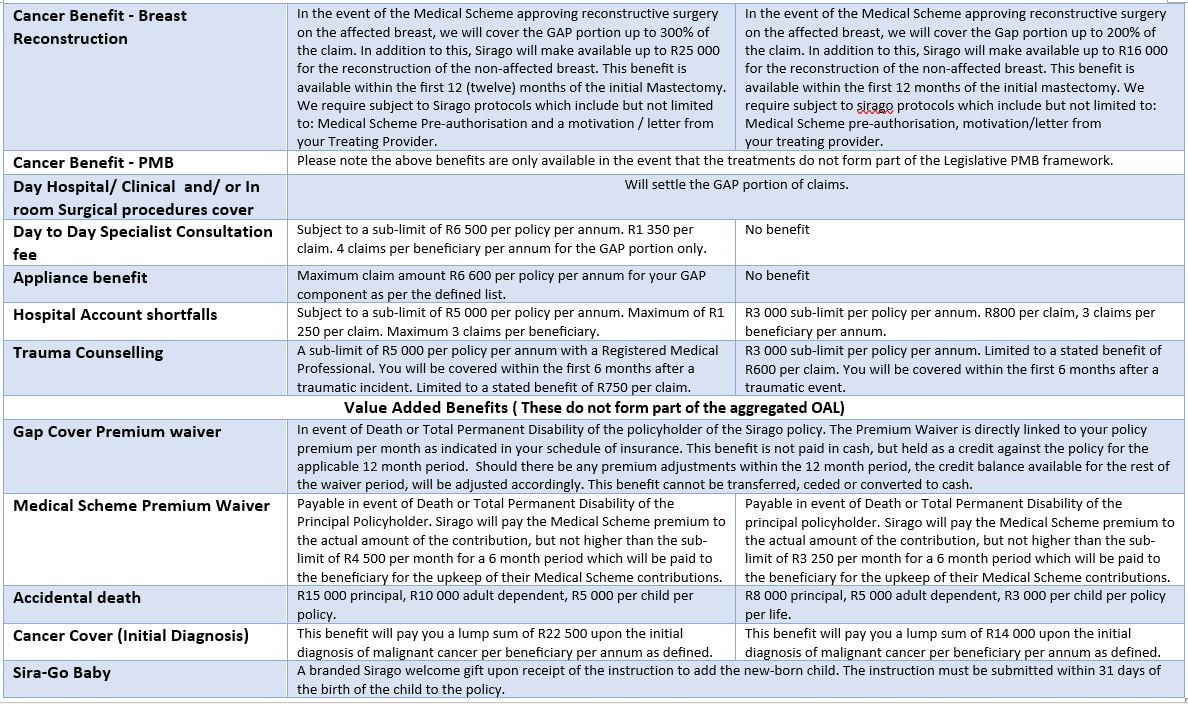

Below are the benefit comparison update for Ultimate Gap cover & Plus Gap cover for 2020:    It’s now time to review your medical aid scheme cover for 2020. This means you have a window within which you can switch to a different plan for the new year. This window usually closes at the end of November (depending on your current provider), so don’t delay collecting the necessary information. This is not a decision to be rushed.

Why do I have to decide now? Medical aid providers allow you to switch to a higher plans once a year (at the end of the year) without penalties or consequences. If you want to save on premiums or you need to increase benefits, now is the time to do it. What if I want to change providers altogether? If you are unhappy with your medical aid provider, you can switch to another at any time of the year. But before you do, consider the following: Waiting Periods Medical Aids by law must accept anyone who applies to join their scheme. To protect themselves from older or sickly members that join without having contributed to the risk pool, they usually impose a waiting period of between 3 and 12 months. Waiting periods will apply if 1) you have not been a member of another South African medical aid for the past three months or more, 2) if you change medical schemes before 2 years of being covered with your previous medical aid provider and 3) if you have a pre-existing medical condition. Finding out about any waiting periods is extremely important before deciding to change providers. Late joiner penalty As an additional means to manage the risk of older or sickly members joining without having contributed to the risk pool, medical schemes (according to the Medical Schemes Act) are entitles to add a late joiner penalty to your premium if you were not part of a medical scheme before 01 April 2001. The late joiner penalty is calculated (using a prescribed formula) based on the number of years that you were not on a registered South African medical scheme. The late joiner fee can range between 5% and 75% of the total contribution, depending on the number of years that you were not covered by a medical scheme. Please contact Namhla or Tammy in our Health Department, email health@daberistic.com, to find out about different Medical aid options Source: Medicalaid.co.za |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|