Taking control of your medical expenses has become increasingly vital as healthcare costs continue to climb. Finding the right healthcare cover, one that is affordable and aligns with your healthcare needs, is the initial step.

We offer insights into how you can save on healthcare costs by leveraging networks, Designated Service Providers (DSPs), opting for virtual care, and choosing generics to maximise your benefits. Utilising Networks One effective method to reduce monthly medical aid contributions without compromising care is opting for a network plan. Generally 15% to 20% cheaper, these plans require members to use network hospitals. Networks negotiate favorable tariffs to minimise out-of-pocket expenses and enhance value. If you choose a network plan, ensure there are doctors and facilities in your area. Be aware of co-payments for not using a DSP or network, but note that network options are waived for emergencies. Co-payments Practitioners and hospitals often charge above medical aid rates, resulting in co-payments, the portion for which you're responsible. These vary among schemes. Tariffs and Payment Rates Each scheme has a rate of payment for services rendered. Understanding this is crucial to avoid surprises. Notably, 100% of the scheme tariff doesn't necessarily cover the entire bill. Virtual Care Technology-driven innovations like virtual integration offer convenient healthcare access while minimising monthly contribution costs. Designated Service Providers (DSPs) By using DSPs, you limit out-of-pocket expenses, co-payments, and maximise annual benefits. Generic Medicines Generics offer cost-effective alternatives to brand-name drugs, often 30% to 80% cheaper, with equivalent efficacy and safety. Benefits Plan benefits vary, so read the fine print to understand coverage. Gap Cover This insurance policy covers the difference between what the medical scheme pays and the provider charges for treatments. Medical Savings Schemes allocate an annual fixed amount for medical savings. Ensure this suits your needs. Managed Care Addressing lifestyle diseases, Managed Care programs help manage chronic conditions like cancer, diabetes, and mental health. By utilising supplementary benefits smartly, you can save significantly on day-to-day expenses such as medication and screenings. Maximise your medical aid benefits wisely to access quality healthcare and extend your coverage effectively.

0 Comments

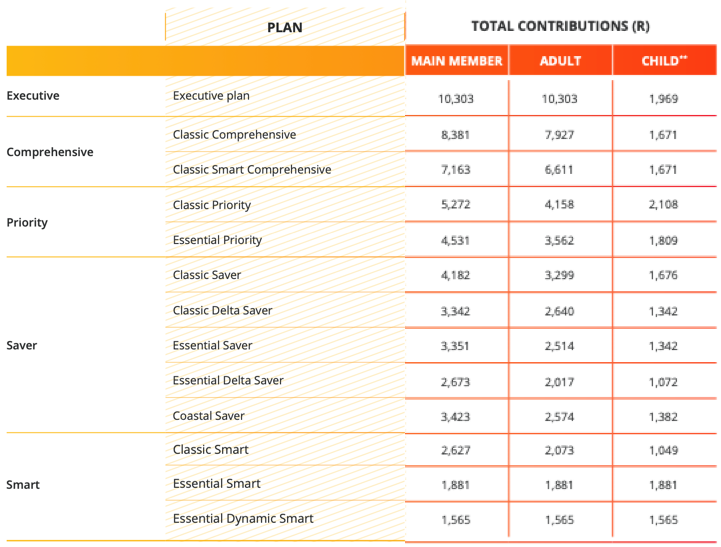

On the 26th of September, Discovery announced its Discovery Health update for 2024. Below are the highlights: 1. Transforming members’ healthcare experience with the new Discovery Health app Your gateway to a personalised, end-to- end healthcare journey. Conveniently access care and manage your health and health plan benefits in a single app. The new app also enables new benefits for all members of Discovery Health Medical Scheme including Virtual Urgent Care, Virtual Physical Therapy, the Mental Health Assessment Benefit and digital therapeutics for mental health. You can already download the app from the App Store and Google Play.  2. Balancing affordability, sustainability and value for members in 2024 and beyond Increases to contributions for 2024 will be plan specific and will range from 0% to 12.9%, to maintain contributions in line with expected claims experience, while supporting affordability for members. Targeted plan and benefit updates for the Comprehensive series and KeyCare series ensures long-term sustainability of the benefits offered by these plans. The Comprehensive series currently has five plans. It will be consolidated into two options in 2024: Classic Comprehensive and Classic Smart Comprehensive. 3. Creating personal health pathways for all members In 2024, all Discovery Health Medical Scheme members will have access to a personal health pathway that predicts the most important actions they can take to improve their health. Members are encouraged to complete actions through an intelligent, gamified experience, which has been personalised for every adult member on the Scheme. 4. Expanding access to healthcare cover with Flexicare Flexicare is a health insurance product designed to provide a wide range of day-to-day healthcare benefits with optional add-ons, such as such as unlimited GP consultations, medicine, dentistry, optometry and so much more. Flexicare will be enhancing its primary healthcare offering in 2024 to include a nurse-led clinic pathway that provides increased access to quality primary healthcare at an affordable price point. The 2024 Discovey Health contribution table is as follows:   The most affordable medical aid plan independent of income is Essential Dynamic Smart, R1,565 per month.

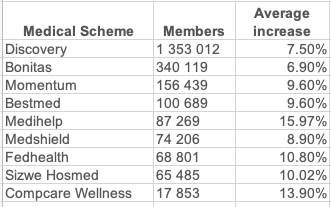

The most expensive plan, which provides the most comprehensive benefits, is the Executive Plan, which costs R10,303 per month. If you want to get or review the medical aid for your employees, please call our Health Department on 011-658-1333 or email service@daberistic.com. All the large open medical schemes in South Africa have announced their contribution increases for 2024. Below is the list.  Discovery Health says the average weighted increase across DHMS plans is 7.5% for 2024. Excluding the Medical Savings Accounts, the increase on Risk Contributions is 10.5%.

If you want to review your medical aid plan, please call our Health Department on 011-658-1333, Option 2 or email service@daberistic.com.  More and more South Africans are experiencing financial problems leading them to try to cut costs and thus leading them to cancel their medical aid. As Daberistic we advise you that you do not have to stay without cover and there are other affordable solutions that will give you peace of mind. We share below about Health Insurance. What is Health insurance? Is a type of insurance coverage that pays for medical, surgical, and sometimes dental expenses incurred by the insured. Health insurance can reimburse the insured for expenses incurred from illness or injury, or pay the care provider directly. The benefit could either be a fixed sum of money per day or a maximum lump sum of money which is paid if a specified health event takes place (e.g. a specific health condition develops). Health insurance policies usually only pay out if certain specific health-related events happen and do not pay your medical expenses as a medical aid scheme would. Unique Principles 1. Limitations and prohibitions: A hospitalisation policy may not cover medical expenses. A health policy, other than a Gap cover policy, may not require the policyholder or insured person to be a member of a medical aid scheme. 2. Waiting period: A hospitalisation policy, gap cover policy and HIV/Aids, tuberculosis and malaria testing and treatment policy may provide for a – general waiting period of up to 3 months; and A condition-specific waiting period of up to 12 months. An insurer may not impose a condition-specific waiting period on a policyholder’s health insurance policy if that policyholder, for at least 90 days before entering into a health policy with the insurer, had a health policy with materially similar benefits and had completed the condition-specific waiting period in respect of that health policy. Where a waiting period of a policyholder under a previous health policy had not expired at the time that that policyholder enters into a new health policy with materially similar benefits, the insurer may only impose a waiting period equalling the unexpired part of the waiting period in respect of that previous policy. 3. Disclosure requirements: A hospitalisation policy, gap cover policy and HIV/Aids, tuberculosis and malaria testing and treatment policy may not create the impression that it is a substitute for medical aid scheme membership. A hospitalisation policy may not create the impression that it covers you for medical expenses. Three areas where Medical Aid Schemes and Health Insurance differ:  If you would like to apply for health insurance, contact Jo in our Health department tel: (011)658-1333 email: service@daberistic.com

Source: CMS  Due to pandemic, rising costs and high taxes are eroding pensions and retirement savings in South Africa. Many are forced to use the state-funded healthcare services which is already under pressure, causing long queues and even longer waiting lists.

There is no doubt that we want the best medical attention for our elderly parents when they fall ill therefore private health care is our solution. It is important to understand what options is best suited for your aging parent’s needs. Where do you start? You would need to sit down and discuss with your parents and obtain the following information:

Once you have answers to the above, the next set of questions you need to discuss is to do a realistic budget to finance the plan.

What if your parents cannot contribute? If your aging parents are financially dependent on you and you happen to be main member of a medical aid policy, you may consider adding them as your dependent as this means they can pay a reduced rate. However, they will be on the same option plan as you, should your option not be sufficient to cover their needs, your option is to upgrade your plan. If you’re on an option that includes savings, they become eligible for using your savings. You will need to be prepared for savings being exhausted due to extensive care required. What happens when parents don’t qualify as your dependent? If you decide to not add parents as Dependants or due to parents not qualifying to be your dependent, they can always choose a medical option according to budget and below are things to consider for when choosing your option. Full medical cover (with savings): On a comprehensive option, most elements are covered for. Such as hospital admission, chronic medication and day to day expenses, medical equipment, and possibly dentistry and optometry. These plans vary widely therefore, read through entire plan before signing up to make sure it qualifies all your parent’s needs. Basic hospital plan: These covers around 90% of hospital procedures, basic prescribed minimum benefit (PMB) condition and cancer benefit. It excludes expenses such as none PMB approved medication, equipment, doctor’s visits, optometry, or dentistry. This may not be a full coverage but highly affordable option. Gap cover is always recommended by Daberistic as this boosts your unforeseen gap payment by 500%. To read more about gap cover click here. What else to keep in mind?

If you would like cover for your parents, please contact Namhla or Tammy in our health department, email Service@daberistic.com, Tel 011-658 1333, option 2 for Medical Aid.  Medical cover has become expensive. These days, even a minor operation can have you digging into your long-term savings. The high cost of hospital stays, specialist fees and other medical expenses makes it important to have at least some form of medical cover. With all this need for cover a friend or family member might mention to you, different medical aid options or that you must consider medical insurance. This may then get you to ask yourself, what is the difference between Medical Aid and Medical Insurance? Below we provide all the information you’ll need to make the right choice for you and your family.

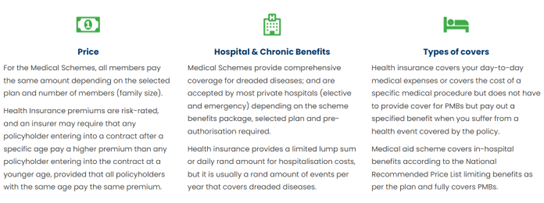

Regulation In South Africa, all medical aid schemes are regulated by the Medical Schemes Act and governed by the Council for Medical Schemes. Health insurance, on the other hand, is regulated by the long-term insurance act and governed by the Financial Services Board. Price One of the most noticeable differences between the two types of cover is the price. Medical aid schemes are notably more expensive, with higher monthly contributions. Medical insurance, however, is far more affordable, but this means there are limitations when it comes to what is covered. You should always consider your health needs when deciding which is best for you. Benefits Medical aids provide Prescribed Minimum Benefits (PMBs) for a list of chronic disorders. Medical insurance plans usually focus on daily health care, such as doctors’ visits and short-term medication. A more comprehensive health insurance plan may offer hospital care in the event of an accident or emergency, to a fixed sum. Although a medical aid plan provides more comprehensive cover, it doesn’t generally include personal accident disability or cover for loss of limbs. Health insurance does. It may also include death and funeral cover, which medical aid schemes do not offer. Medical aid schemes offer comprehensive hospital cover, usually for a large variety of in-hospital treatments, depending on your plan. However, there is often a shortfall between medical aid rates and the rates charged by the medical practitioners. (Therefore, Gap cover is always recommended, so to cover for any shortfalls that may occur) Medical insurance does not cover extensive hospital benefits. Hospitalisation is usually limited to accidents and emergencies and only covers specified costs. If costs exceed the limits, members will have to pay for the extra. Medical aids are also required to cover chronic medication, while medical insurance is not. Tax benefits Medical aid contributions are deductible for tax purposes whereas health insurance premiums are not. To apply for cover, contact our healthcare consultant Tammy email: service@daberistic.com tel:(011)658-1333 Given that COVID-19 is a global pandemic, all governments are required to coordinate and manage the response to the disease in the best way they can. As is the case in other countries, the South African Government has decided that it will source, distribute and oversee the rollout of the vaccination programme, and will therefore be the sole purchaser and distributor of the COVID-19 vaccines to provincial governments and the private sector, including medical schemes.

With the roll-out of the COVID vaccine, the South African government has also had relevant regulation, and different Medical Aid companies have their own relative ways to cooperate. The vaccines provided by the government are Johnson and Johnson (one dose) and Pfizer (two doses), and the Medical Scheme must be carried out according to the Government’s progress and allocation phase. As of 16 May 2021, people over the age of 60 are allowed to register on EVDS. South Africans must register on the Department of Health (EVDs) at the following website, when their age group is open to register: https://vaccine.enroll.health.gov.za/ Discovery Health In addition to the Department of health's online registration (EVDs), Discovery has launched its own registration and tracking program. Please refer to our article about the process and registration steps: https://www.daberistic.com/discovery_covid_vaccine_english.html Momentum Health Momentum is preparing to provide vaccines in an efficient way to assist members and the public to obtain vaccines in their allocated phase, the following has been established:

Momentum will communicate exact locations of the health care centres. Bonitas Health Bonitas Health did not give any special instructions, but for members who are qualified to register on EVDS, Bonitas has sent a SMS and an e-mail directly to the members. After receiving the invitation, they can register on the website of the Department of Health, and follow the process further. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|