|

Death, while an incredibly difficult subject to confront, is one of life's unavoidable realities. Yet many investors fail to prepare for this eventuality and put their loved ones' financial futures at risk. According to The Fiduciary Institute of Southern Africa, more than 75% of South Africans pass away without a valid will drawn up.

In the spirit of National Wills Week this month, we want to empower you to prepare adequately and help you leave a lasting legacy by posing these questions: • Is your will up to date? Make sure you keep me abreast of any material and life-changing events, such as marriage, the birth of a child, or a death in the family. • Are your retirement fund nominees' details up to date? • Are the beneficiaries of your various policies up to date? If your investments are structured as a life policy, you will need to make sure your service provider has the correct beneficiary appointments on file to ensure speedy payment to your intended beneficiaries. • Have you planned for immediate needs? Make sure you have made provisions for any immediate expenses, such as funeral costs, that may need to be covered before your investments can be accessed. • Have you spoken to your beneficiaries, dependents, and nominees about the contents of your will? Contact us on service@daberistic.com if you want a financial planner to review your financial affairs.

0 Comments

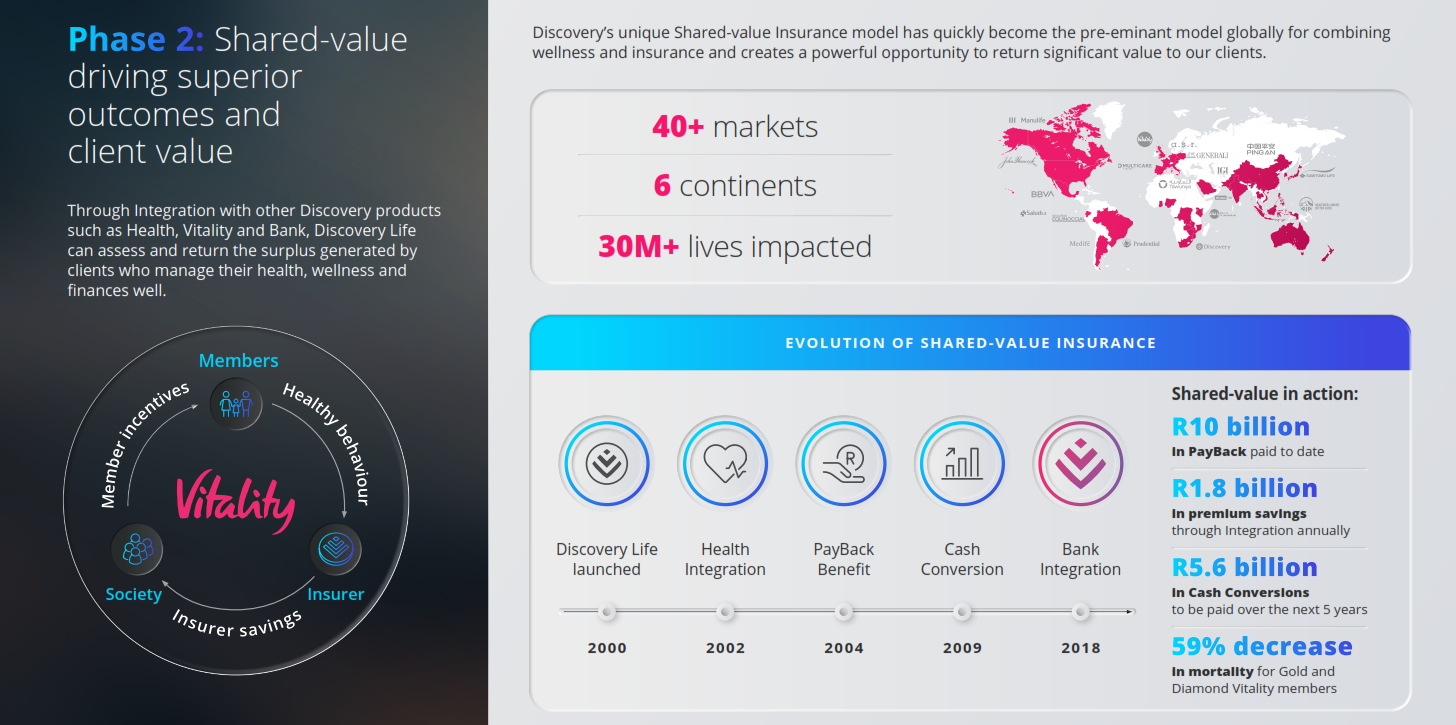

Discovery Life gave us an update on the Evolution of Discovery Life for 2023. Discovery has pioneered the evolution of Life Insurance in three distinct phase: The separation of risk from investment, the introduction of the Shared-value Insurance model, and now, the personalization of the client experience through digitisation. Each phase embodies innovative product that meet Discovery client needs and create unmatched value, while making them healthier, and enhancing and protecting their lives. Discovery Life has introduced the revolutionary new Discovery Life Plan 3.0 – The Future of Life Insurance, Now. On 22nd February 2023 Discovery have introduced the Discovery Life Plan 3.0, which personalises life insurance through digitisation, to deliver a seamless and hassle-free experience for you and your clients. As we move towards the modern digital era, this next-generation life insurance will be accessed on the mobile phone, offering your clients convenience and ease. This plan includes:

If you would like us to prepare on a Life quote for you contact Kevin or Sandra in our Life Department email: service@daberistic.com tel: (011)658-1333

There are several factors to consider when determining how much life insurance coverage you need. Here are some steps you can follow to calculate your coverage needs:

1. Determine your financial obligations: Make a list of your current and future financial obligations, such as outstanding debts, mortgages, and tuition payments. 2. Calculate your income: Consider your current income and any future income you anticipate receiving, such as raises or promotions. 3. Consider the length of your coverage: Determine how long you need your coverage to last, taking into account the length of time your dependents will need financial support. 4. Calculate your expenses: Estimate your living expenses, including housing, food, transportation, and any other recurring costs. 5. Consider any additional expenses: Think about any one-time expenses that your dependents may incur in the event of your death, such as funeral and burial costs. 6. Add up your obligations and expenses: Add up all of your financial obligations and living expenses to get a total amount of coverage you need. It's good idea to review your coverage needs periodically to make sure they are still adequate as your circumstances change. Over the last two years, we have witnessed the COVID-19 pandemic ravaging around the world, causing countless deaths and immeasurable suffering. Thanks to the rapid development and deployment of COVID vaccines, the situation is starting to be brought under control.

Locally, life insurance companies have experienced many COVID related death claims, increasing their claim costs by billions of Rands. As a result, they reviewed life insurance premium rates and informed brokers that, if a life insurance applicant is not vaccinated against COVID or cannot provide proof of COVID vaccinations, they would load the life insurance premium by up the 50%. Recently, as the COVID infection wave starts to stablise and more people are vaccinated, life insurance companies reviewed their underwriting requirements and relax the conditions accordingly. Liberty says the for life insurance applicants not vaccinated, they will not increase their life insurance premium unless the applicant is over the age of 60. Old Mutual says they will not load the life insurance premium for applicants below the age of 50. Discovery Life also confirms they will not load the life insurance premium. In addition, they provide an incentive: If the life insurance applicant can provide proof of vaccination within the first year of life insurance policy, they will refund up to 100% of the first year policy premiums, based on the client's medical and Vitality status. The move by life assurers to proactively review their underwriting conditions is welcomed, especially in the current inflationary economic environment. Written by: Kevin Yeh, CFP® On the 3rd of August, Kevin got a text message telling him R49,432.31 has been paid into his bank account. How did that happen? And would you like to get it as well? You can watch the Youtube video by clicking in the picture above or continue to read below how!

So in the early morning of the 3rd August 2021, this text message came to my iPhone at 2:48am: Congratulations, your Discovery Life Health Integrator Payback benefit of R49,423.31 that rewards you for looking after your health with Vitality has been released successfully.Later that day, at 9:51am, this text message came to my iPhone: Payment for your Discovery Life policy Health Integrator PayBack for R49,432.31 has been made. It will show in your account in the next four working days. Then I checked my FNB bank account, and indeed I have received this money into my bank account! I was ecstatic. This is a lovely bonus to receive. So why Discovery Life pays me this bonus? It relates to my Discovery Life policy. I took up my Discovery Life policy with my then broker Jose Afonso, in 2003. And I have been paying for it since. How a Discovery Life policy works is, if you are a Discovery Health member, and a Vitality member, you can get your Discovery Life policy Health integrated, to get a discounted premium, as well as Health Integrator PayBacks. With my policy, I receive such paybacks every five years. It is based on my Health claims, or medical aid claims, as well as my Vitality status every year. The lower the medical aid claims, and the higher the Vitality status, the higher the percentage of life insurance premiums is paid back to me. Discovery Life calculates the percentage of payback based on medical aid claims and Vitality status every year, then aggregate over five years, to pay me the payback every five years. Since I have been good at keeping medical aid claims low and maintaining Vitality diamond status, the highest Vitality status you can achieve on Vitality, I get up to 50% of my life insurance premiums back. So essentially I only pay half price for my life insurance benefits. Sounds good? So what do you need to do in order to get 50% of your life insurance premiums back in bonuses?

Number 4, stay healthy, engage with Vitality and improve your health. You should work to reach Vitality diamond status and stay a diamond member. If you do step 4 consistently, as part of your lifestyle, then you will reap the best rewards from the Discovery ecosystem and a Discovery Life policy. It is important that you understand how Vitality works, how to get Vitality points, so you can get to the highest diamond level as soon as possible. Vitality rules change all the time, at least annually, so it is important to know the changes and play the game to get your points. Vitality does make it harder and harder every year for you to get points, only recently I found to my dismay that 5,000 steps a day can only accumulate 1,000 points a year, not great as I and my wife need to get 100,000 points this year to maintain our diamond status! If you take out a new DIscovery Life policy, you can choose to have Annual PayBack, whereby you get an amount paid back to you annually, then an additional amount every five years. You can also select the Double PayBack option, where you choose to receive your PayBacks five years later and double your payback amount. So if you have or aspire to have a healthy lifestyle, eat healthy, exercise regularly, keep fit, like technology and gadgets, and like a challenge, Vitality is for you, Discovery Life is for you, and you are well on your way to get the best rewards and paybacks. So who is Discovery Life not for? If you do not like to live healthily, you do not watch what you eat, you don't exercise, you don't like to keep up with technology and gadgets, you don't like the idea of working hard to get something back, keeping up with all the changes of the Vitality programme, or you have many medical aid claims, then Discovery Life is probably not suitable for you. If you have any questions or would like to review your life cover, email service@daberistic.com or WhatsApp 0762005488, and we will contact you.

Based on our own experience and statistics, we have found that more clients enquire about Discovery Life than other life insurance company's products. This is interesting, as we are an independent practice, and we have contracts with no less than 7 life insurance companies:

- Discovery - Hollard - Liberty - Momentum - Old Mutual - PPS - Sanlam As an advisor, the process I go through is to first understand the client, his needs, then match the best product to his needs. Discovery Life does not necessarily meet client needs in every situation. So why do more clients ask me about Discovery Life? When we unpack the trend, I think there are a few things that draw clients to Discovery Life: 1. A client is a Discovery Health member. As Discovery Health is the largest open scheme in the country, with 55% market share, most of our clients are on Discovery Health. They are familiar with the company, and they trust the brand. Hence they ask for Discovery Life when they think about life insurance. 2. Discovery is an expert in marketing. Whether you like Discovery or not, they are a leader in marketing. From its early days, it has been very strong in marketing. You hear and see its advertising everywhere: Online, radio, TV, social media. And it does an excellent job, with beautiful graphics, interesting stories, partnering with sportspeople. In your face everywhere. 3. Discovery excels in mobile engagement. Discovery spends a lot of efforts and money in developing its mobile apps early on. It is a leader in mobile apps. I find myself logging in to Discovery app at least once a week, to check my Vitality Active Rewards, then maybe browse other sections. Discovery has made a lot of information and data easily accessible, at your fingertips literally. You don'g need to log into a website, you don't need a computer. You don't have to call a number. All you need is a phone. Yes all that information is kept secure. 4. Everything under one roof. As Discovery continues to expand its product range, and clients log into Discovery app regularly and see what else Discovery has to offer, they would think, "Why not get this product with Discovery as well, so I have everything in one place?" 5. Social influence. As more and more people become clients of Discovery, when their family and friends talk about life insurance, the name Discovery would come up somewhere in the discussion. 6. The profile of our clientele. As Daberistic focuses on the business owners and professionals market, they tend to be in the more affluent market. Discovery's market positioning speaks to their needs, image and aspirations. Discovery Life has many unique features and benefitsis. It is competitively priced if integrated with Discovery Health and Vitality. It has an attractive payback benefit. Now a Discovery Bank client can get further benefits with the Discovery Bank Integrator. While Discovery Life does have a strong value proposition, it is not for all clients. If a client is not on a medical aid administered by Discovery, does not like to exercise, does not pay attention to healthy living, does not want to spend time engaging with Vitality wellness programme, then he will find Discovery Life to be expensive. And it can become even more expensive over the long term. Naji Haddad is a life insurance agent, successful businessman, a proud MDRT member in Beirut, Lebanon. François du Toit interviewed him, he shared his life story of being positive, overcoming adversity and helping people. As people of Beirut deal with the aftermath of a powerful chemical explosion on 4 August 2020, his story touches many hearts. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|