|

South African investors have a love-hate relationship with listed property, with significant shifts in sentiment and demand evident over the last 10 years. Before 2017, it was quite common for multi-asset funds to have healthy allocations to the S.A. listed opportunity set mostly due to the appeal of property companies offering relatively stable dividends. The S.A. property market demonstrated strong performance between 2013 and 2017, attracting significant investment flows into the sector, as depicted in the chart below. Source: Morningstar

0 Comments

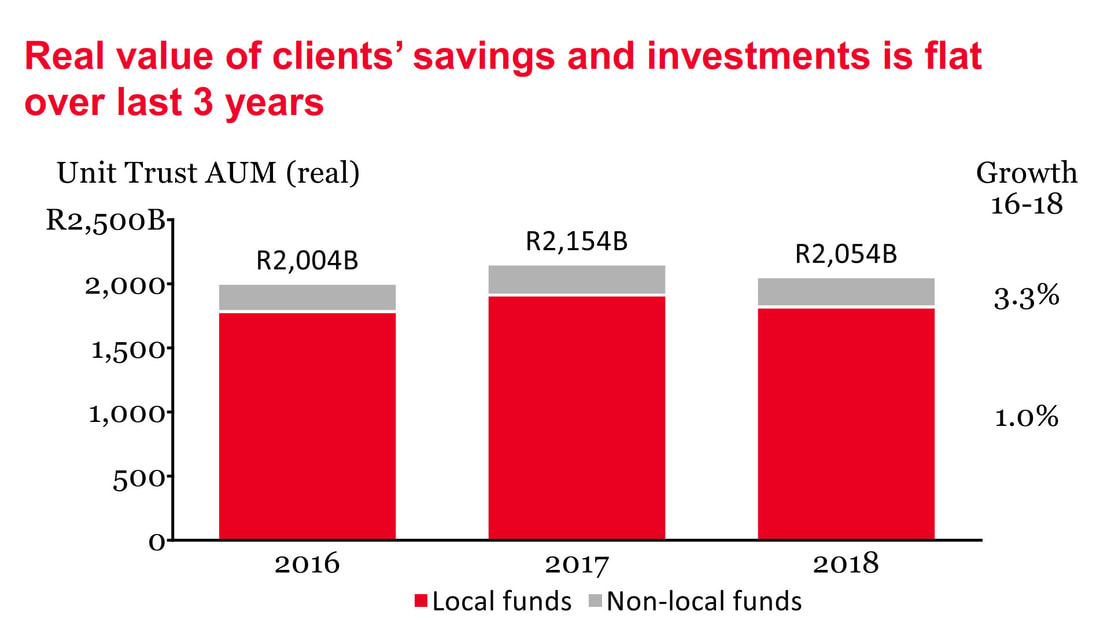

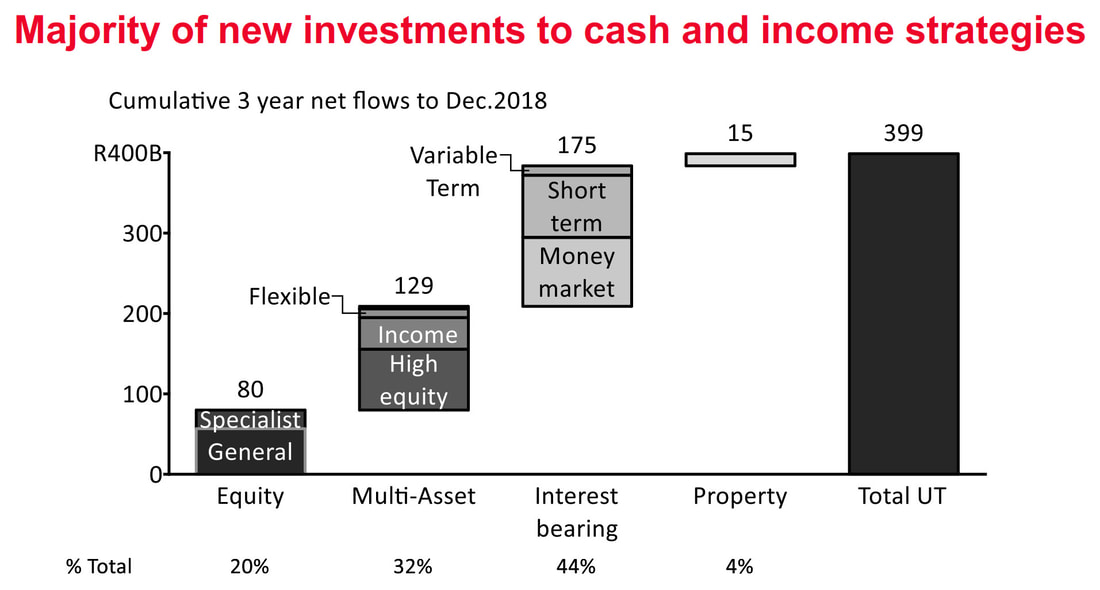

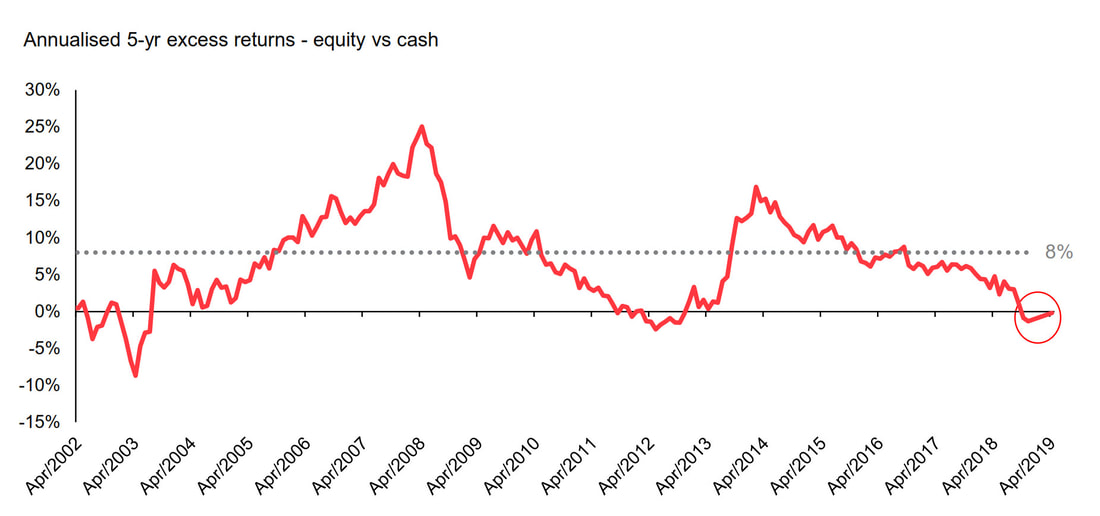

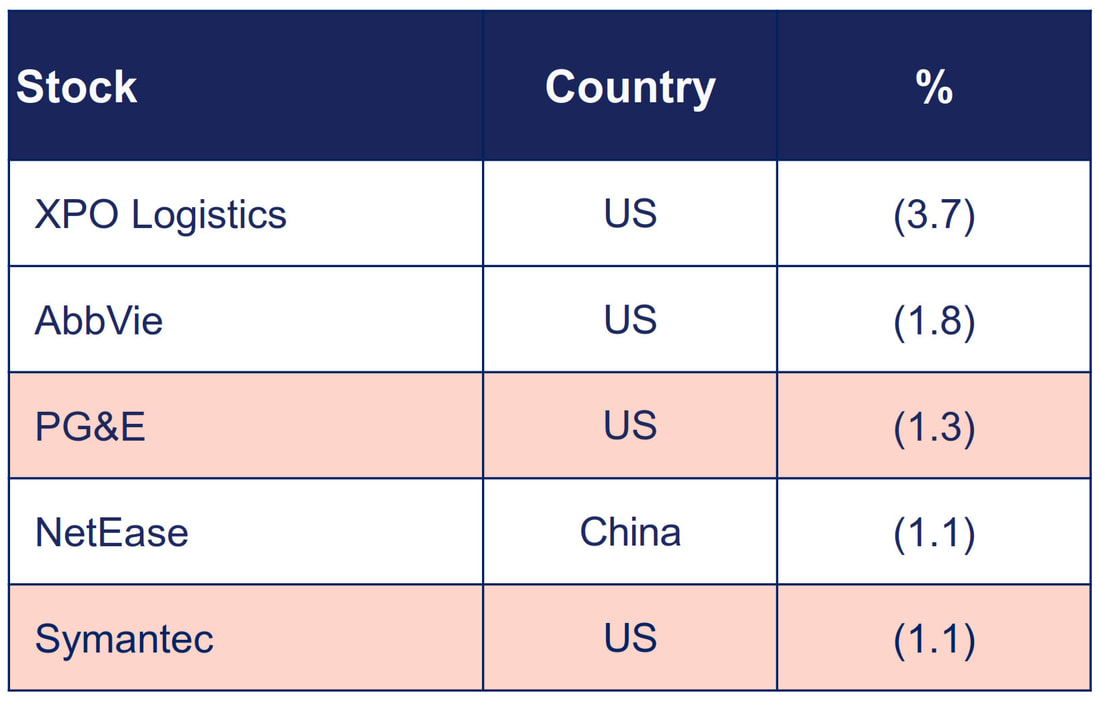

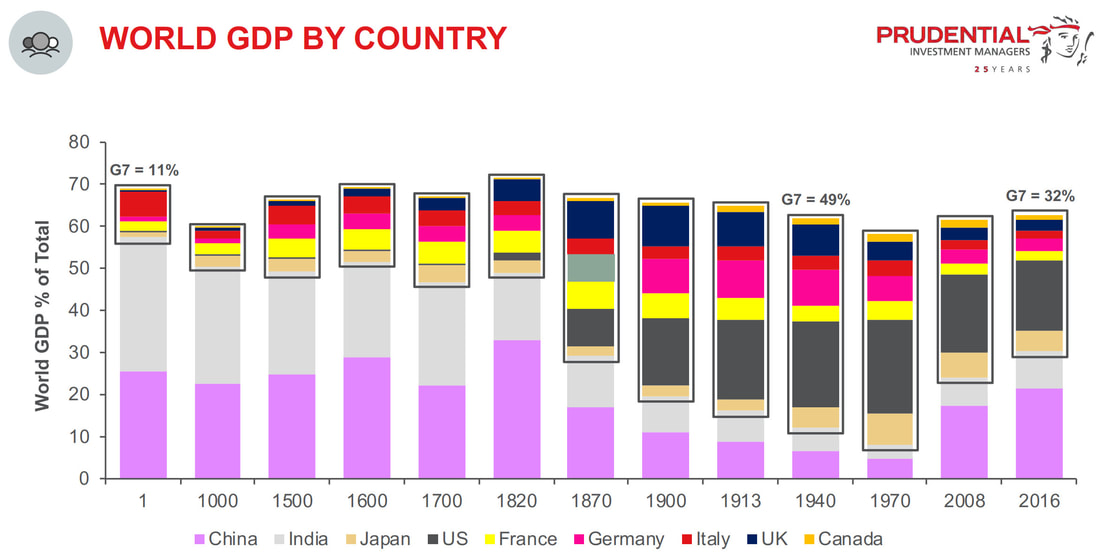

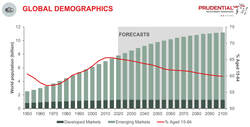

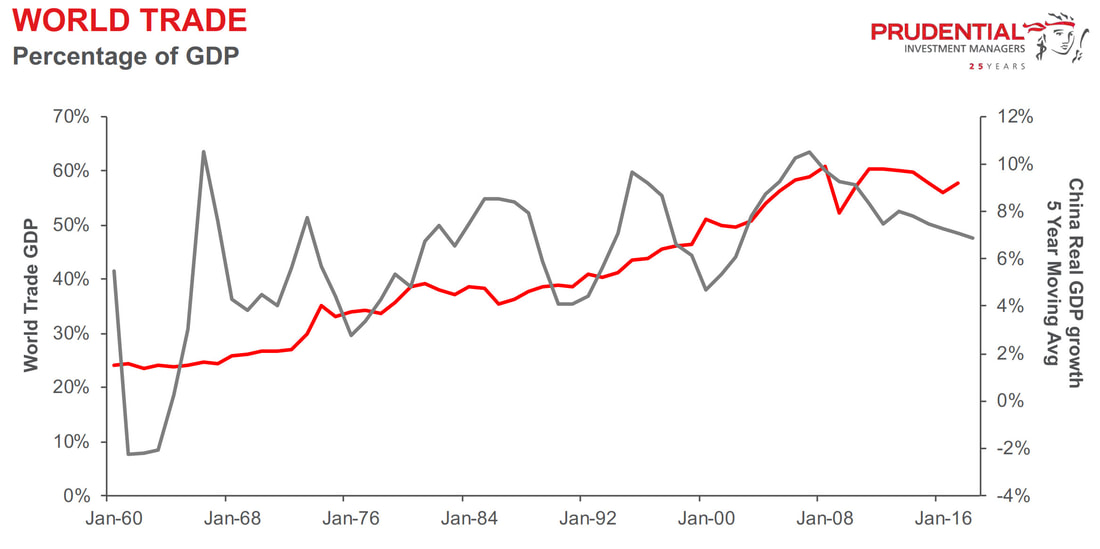

In the past three weeks, I have attended investment briefings by four well-known asset management companies in South Africa. The four fund managers are PSG, Allan Gray, Coronation, and Prudential. Allan Gray ranked first and PSG ranked second in the Raging Bulls Award. Prudential Prudential is the number one Larger Manager according to Morningstar, it also celebrates 25 years of asset management in South Africa this year. Coronation is a JSE listed fund manager that celebrated asset management in South Africa for 25 years last year. I will tell the reader my summary first: 1. These four fund managers have excellent long-term track record. Many of their funds are suitable for different types of investors, ranging from short-term high-yield, secure capital funds, to equity funds and multi-asset allocation funds for long-term growth. 2. No one has escaped the effect of political corruption (namely State Capture) in South Africa in the past five years, which has led to the economic downturn and the flat stock market. Fund managers have also been affected by the ongoing US-China trade war on the global economy and investment market since last year. The annualized return on equity funds over the past five years has been 5%. 3. Looking ahead, all fund managers are optimistic about the return on the South African stock market in the next three to four years, Japan and emerging markets such as China. At this stage, they also like the high yield on South African bonds, giving investors a yield of 9% to 10%. They are negative on European and American bonds, especially the negative interest rate on 10-year German bonds. Investors investing in German bonds are destined to receive less than the principal after 10 years. 4. Allan Gray and Coronation are South Africa's largest fund companies, with large amounts of assets under management and relatively conservative investment style. Prudential and PSG manage assets on a smaller scale, and they are able to be more flexible. Prudential always likes some exposure to listed property, and PSG is now favoring small and mid caps in South Africa and certain Japanese companies. ***** I have been dealing with asset management companies in South Africa for nearly 20 years. I have seen the growth and changes of the asset management industry, and experienced the ups and downs of the investment market: The Dot Com bubble in 2000, the global financial crisis in 2008, the European debt crisis, the emerging market crisis in 2014, and the US-China trade war from 2018 to the present. In South Africa we have seen the shocking firing of Minister of Finance Nene in 2015. During this period, South Africa's asset management industry flourished and there are now more than one hundred fund managers. It is very challenging in choosing the funds to invest in, as the market changes, portfolio managers change, and many funds appear and disappear in these two decades. However, patient investors investing in good funds of reputable fund managers will have been rewarded over the long term. Let compound interest be your good friend and work for you. 1. PSG Asset Management The PSG Asset Management's investment philosophy is 3M – Moat, Management and Margin of Safety. Moat is a company's competitive advantage, that acts as high barrier to entry, such as technology, systems, talent, and markets. Management refers to the track record of the company's management and how they allocate the company's funds. Margin of safety refers to whether the stock price is lower than the assessed intrinsic value of the company, this provides investors with downside protection against the risk of over-estimated intrinsic value. PSG has a 20-year history, was previously run by successful manager Jan Mouton and then handed over to Chief Investment Officer Greg Hopkins, who has 18 years of experience. Shaun le Roux has been with the company 18 years, managing PSG Equity Fund and PSG Flexible Fund. However, it has lost two senior portfolio managers in the past three years, the performance of new managers Justin Floor and Dirk Jooste remains to be seen. PSG's philosophy is to find investment opportunities in areas that everyone hates, and to avoid everyone's favourite stocks. This is value investing. Therefore, PSG currently does not invest in technology companies or defensive stocks, but favours South African small and mid caps. Below are the latest PSG investment update videos: How we think about and manage risk Is SA Inc even investible? Opportunities in local markets Opportunities in global markets 2. Allan Gray Allan Gray has a 45-year history in South Africa and its sister company Orbis has a 29-year history of managing global assets in Bermuda. Both companies share the same founder, Allan Gray, and have the same value investment philosophy. Like PSG, it is also a contrarian investor, looking for investment opportunities in areas that people don't like. However, because of the large scale of assets under management, Allen Gray must invest in large blue chip companies. Allan Gray's strengths are equity research and asset allocation. Its weakness is its long-term dislike for real estate, which currently works in its favour, but it missed the long-term listed property boom before 2018. Allan Gray's portfolio managers are pretty stable, with an average of more than a decade of experience at Allan Gray, giving investors invested in their funds certainty and peace of mind. Allan Gray pointed out that the total assets under management of the South African fund industry in the past three years were virtually flat, indicating that the South African stock market has been dull in the past five years and that the general public under economic and tax strains has no money to invest more.  It is no surprise that, over the past three years, The fund category receiving the most new money flows is money market and income funds. Because of the lacklustre returns from the South African stock market in the past five years, investors have turned to income funds for high yields.  Indeed, the chart below confirms the equity return has been below the cash return over the last five years.  But the stock markets do work in cycles. If history repeats itself, the return of the SA stock market in the next three to four years will far exceed the bank deposit interest rate. The chart above shows that during the past 17 years, between 2002-03 and 2012-13, the five-year JSE total return was lower than the deposit rate. It is also the case from the second half of last year. However, after the stock market rebounded, the return for the next three to four years was better than the bank deposit. According to Allan Gray's data analysis, cash deposits only has a 13% chance of outperforming the stock market in the next four years. In other words, the stock market has an 87% chance of outperforming cash deposits in the next four years. The odds are now in investors' favour to hold and enter the stock market, not to exit. Allan Gray's foreign investment is handled by its sister company Orbis. Orbis has long-standing admirable performance, but it has fallen 20% in the last one and a half years, making it a bottom performer last year, and slightly behind its sector average in the past five years. This is due to its contrarian investment style, sometimes allowing it to greatly exceed the market, and sometimes falling far behind. I remember that in 2012-13, Allan Gray also had a period of under-performance, but it laid the foundation for its subsequent performance in 2014-2016. In the past year, Orbis has more stocks losing money than stocks that make money. What has happened? According to its analysis, the top five detractors of performance are as follows:  Orbis spent some time explaining the largest detractor XPO. XPO is a US logistics and transportation company that aims to help companies enter the e-commerce sector and compete with Amazon. It is committed to the vertical integration within the logistics industry, offering small and medium-sized enterprises one-stop service. It acquired a truck fleet company Conway four years ago. In the second half of last year, the profit announcement disappointed, then short-sellers attacked the company with damaging reports. Its stock price subsequently fell 30%. Orbis met with the management and thought that the founder Bradley Jacobs and his management team were still very good, and the market was wrong in punishing the stock, so it increased its investment in XPO. Abbvie is a US pharmaceutical company, and Orbis is convinced of the future of the US healthcare industry, so it has added another pharmaceutical company, Celgene. After reviewing the investment case for Netease, it has increased its holding, now it is the largest position in the fund, with a weighting of 9.1%. PG&E is an electricity and gas company in California, USA, it sold out at a loss. It also sold out Symantec, an internet security company, at a loss. For the Chinese market, Orbis is optimistic about the future of tech companies, mainly holding shares in NetEase, Tencent and Autohome. Orbis has a long-term track record, I suggest investors buy on current dips. 3. Coronation Asset Management Coronation is 26 years old in South Africa and is South Africa's largest listed fund manager. I was invited to participate in the annual Face to Face event in Cape Town, as due diligence, and listened to its economist and 8 portfolio manager briefings throughout the day, from Top 20 Fund, Balanced Plus Fund, Strategic Income Fund. Capital Plus, Balanced Defensive, Property, Global and Emerging Markets, The day ended with a Q&A session with Chief Investment Officer Karl Leinberger. Coronation employs 300 people, one-third of whom are investment analysts and fund managers, a strong investment management team in South Africa. It follows a valuation driven investment process and invests in undervalued companies or assets. The difference between Allan Gray and Coronation is that Coronation is more likely to invest in riskier industries in the stock market. In recent years, it has invested in mining stocks, which initially caused the its equity funds to fall, then helped investors make money when share prices recovered and rose. Coronation also likes real estate, and for a long time there has always been an exposure to listed property in South Africa and abroad. However, Coronation has also stepped on many of the so-called landmine stocks in recent years, such as Steinhoff and MTN, so the returns from its equity exposed funds have been market average for the past five years. The Coronation investment management team is stable and reputable. They have been incorporating ESG (environmental, social, governance, environmental, social and corporate governance) principles in evaluating investment opportunities for many years. On the whole, their standouts are income-based funds, where risk management is robust, and opportunities are captured for clients to enhance yield. the other area is global Emerging Markets. Many analysts visit the CEOs of listed companies around the world, they really work hard to find investment opportunities for clients. Other funds are expected to have similar returns relative to other larger managers in the long term. 4. Prudential Prudential Prudential Investment Management celebrates 25 years in South Africa. Similar to Coronation, the valuation investment method is also used, but because it belongs to Prudential, a global financial services group headquartered in the UK, it tends to have a more macro, top-down approach, to assess the relative value of each country and asset class, thereby overweight the undervalued assets and underweight the overvalued assets. It does not take big bets, but rather a large number of small bets. It uses a team-based investment management model. Its investment performance is more market neutral, unlike Coronation, which sometimes experiences large ups and downs due to its conviction calls. Although the investment management team is not large, it is also very stable. Chief investment officer David Knee has more than 20 years of investment experience, mainly fixed income assets, worked in the UK and moved to South Africa in 2008. Head of Equity Johny Lambridis is an actuary and has many years of investment management experience. Prudential's macro data analysis has three points that caught my attention: First, China and India accounted for about 50% of global GDP before 1820. The G7 industrial countries rose rapidly during the industrial revolution of the 19th century, and reached the peak of 49% of global GDP in 1940. The rise of China and India over the past 40 years is just a return to its former status. It now accounts for 30%, which is equivalent to 32% of G7 countries.  2. The global population continues to grow, but the growth rate is slowing. The global population is expected to reach 11 billion in 2100. The population continues to be aging, which has a huge impact on social welfare, government borrowing, caring for the elderly, and political landscape.  3. The rise of China is closely related to the liberalisation of world trade. The left axis of the chart below shows the world trade as a percentage of GDP, and the right axis is the growth rate of China's economy. World trade has increased from 25% in the 1960s to nearly 60% in 2008, but since then it has plateaued. The ongoing US-China trade war is threatening world trade, which in turn will slow down China's economic growth.  Prudential's leading funds are Equity Fund, Balanced Fund, Inflation Plus Fund, and Enhanced SA Property Tracker Fund. These funds have outperformed the average fund in their respective sectors over the long term. However, Inflation Plus Fund has fallen behind in the past three years.

Property investment is high on many investors’ list. Many investors like property as it consists of land and buildings, has physical presence. Property offers capital protection, its value increases over time.

Buying real estate is about more than just finding a place to call home. Investing in real estate has become increasingly popular and has become a common investment vehicle. Although the real estate market has plenty of opportunities for making big gains, buying and owning real estate can be a lot more complicated than investing in stocks and bonds. Owning your own home that you live in is not a property investment. Property investment is something that provides you with regular income over time. There are generally four ways of investing in property:

Ideally, the landlord charges enough rent to cover all of the aforementioned costs. A landlord may also charge more in order to produce a monthly profit, but the most common strategy is to be patient and only charge enough rent to cover expenses until the mortgage has been paid, at which time the majority of the rent becomes profit. The disadvantages of buy-to-let properties is firstly you need to manage tenants. You need to find a good tenant that will pay rent on time and look after your property. If you have a bad tenant that doesn’t pay or damage your property, it can be costly and stressful to the landlord. Worse still, there can be times when you end up having no tenant at all. Also you need to continuously maintain the property, fix things that are out of order, to maintain the use and value of the property. Lastly, property is not a liquid investment: you cannot sell property and get your money in a matter of days. Doing research and finding property in the right location are important in the success of buy-to-let properties. Also be aware of the costs associated with acquiring a property, such as Conveyancer’s Fee, Bond Registration Fee, Deeds Office Registry Fee and Transfer Duty. 2. Real estate trading Real estate traders buy properties with the intention of holding them for a short period of time, often no more than three to four months, whereupon they hope to sell them for a profit. This technique is also called flipping properties and is based on buying properties that are either significantly undervalued or are in a very hot market. Pure property flippers will not put any money into a house for improvements; the investment has to have the intrinsic value to turn a profit without alteration or they won't consider it. Flipping in this manner is a short-term cash investment. If a property flipper gets caught in a situation where he or she can't offload a property, it can be devastating because these investors generally don't keep enough ready cash to pay the mortgage on a property for the long term. This can lead to continued losses for a real estate trader who is unable to offload the property in a bad market. A second class of property flipper also exists. These investors make their money by buying reasonably priced properties and adding value by renovating them. This can be a longer-term investment depending on the extent of the improvements. The limiting feature of this investment is that it is time intensive and often only allows investors to take on one property at a time. 3. Real Estate Investment Trust (REIT) A Real Estate Investment Trust - REIT (pronounced ‘reet’) - is a company that owns, and often operates, income-producing property. The REIT is the international standard. More than 25 countries in the world use a similar REIT model like the US, Australia, Belgium, France, Hong Kong, Japan, Singapore and the UK. A South African REIT - SA REIT (pronounced 'essay reet') - is a listed property investment vehicle that is similar to internationally recognised REIT structures from around the world. Listed Company REITs or Trust REITs are publicly traded on the JSE REIT board and qualify for the REIT tax dispensation. A JSE-listed SA REIT must:

If you like property but do not like the hassles of managing properties, then property unit trusts are for you. Property unit trusts are unit trusts that invest in listed property stocks and REITs, which in turn invest in office, retail and industrial properties. Property unit trusts allow investors into non-residential investments such as malls or office buildings and are highly liquid. They offer investors instant diversification benefit, by investing in a number of property companies. Property unit trusts distribute the income it receives quarterly to investors. You can also benefit from capital growth through rising unit price over time. Over the last 20 years property unit trusts have given investors an annualised return of 20%, making it one of the best investment vehicles over the long term. 5. Leverage This is probably the biggest advantage of investing in properties. With the exception of REITs and property unit trusts, you can borrow money on your property. Banks are willing to give you a home loan, as they can secure their lending with the value of the property. Most mortgages require 10% to 30% deposit, however, depending on your financial standing and credit score, some home loan providers may give you up to 100% bond, meaning you don’t have to put down a deposit. This means that you can control the whole property and the equity it holds by only paying a fraction of the total value. Of course, your mortgage will eventually pay the total value of the house at the time you purchased it, but you control it the minute the property is transferred to your name. This is what emboldens real estate flippers and landlords alike. Whether they rent these out so that tenants pay the mortgage or they wait for an opportunity to sell for a profit, they control these assets, despite having only paid for a small part of the total value.  A very interesting question almost every investor asks themselves is: "If I want to invest money, do I need to buy a property, keep my money in the bank to earn fixed interest rates or invest in stocks?" This is a difficult question to answer simply. All of us have an ambition to invest our hard-earned funds as optimally as possible to ensure we maximise returns. This question is particularly important considering that a one or two percent difference in annual returns significantly impacts the longer-term result. A look at the figures To try to answer this question, the figures should be thoroughly investigated. The following table shows the annual average returns of shares (measured by the FTSE / JSE All Share Index), money market yields (SteFI Composite Index) and direct residential real estate (average prices of South Africa). This draws a comparison between the potential returns that an investor in the stock market can earn in a bank account versus direct property.  Once the figures are taken into account, it is clear that an investment in equities over the long term provides the highest yield. Also, we saw that direct property prices experienced a boom period during 2002-2007 with an average annual return of 18.2%, and began to show signs of slowing (2008-2016) by delivering an average return of 3.8%.

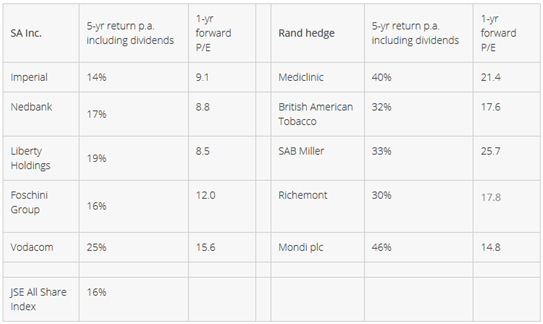

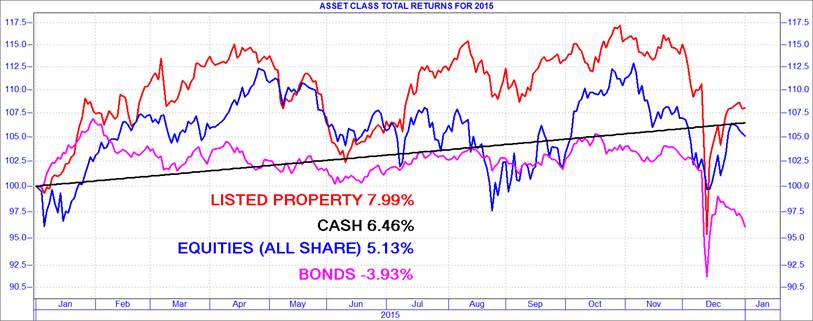

However, the choice is more complicated than simply considering returns over different time periods. Every South African knows that Cape Town property growth will be more attractive than property yields in smaller towns up-country. So geographical location must be taken into account. If the average annual return of the Eastern Cape (7.8%) is compared with that of the Western Cape (9.3%), it is clear that location plays an important role. This phenomenon is further accentuated with the stagnation of the overall residential property market compared to metropolitan areas, especially Cape Town which still experiences a boom in house prices. The impact of rental income It is also important to understand that the above figures exclude rental income. This component ensures, on average, 5% - 8% additional returns per year in rental yield. The issue of rental yields is more applicable if direct property is bought with cash as opposed to using bank financing. If the rental income is taken into account (at the lower limit of 5%), property falls into the same category of return as equities over the long term (14.65% vs. 14.79%). The choice of investment vehicle will depend on a set of additional factors. These factors are briefly highlighted below. If you would like to invest in a Unit Trust or find out more information, please contact Kevin or Thato, email: invest@daberistic.com tel no: (011 658-1333) Written by: Jan Vlok Source: Sanlam  Website: www.daberistic.com Email: invest@daberistic.com Tel: 011 658 1333/1391 Dear Client / Business Associate Compliments of the News Season In our first edition of Investment Focus 2016 we plan ahead for the year on how to handle Investments, the article on Best direction for your investments in 2016 gives a guide on the market share and which markets to target as well as how the past five years’ share performance and current valuation of five well-run rand hedge companies versus five well-run SA Inc companies listed on the JSE. The one thing that is the hottest news in South Africa currently is, the New Tax law in regards to Tax incentives, with National Treasury encouraging us to save more for retirement by significantly increasing the tax incentives, the article More for the future you, less for the tax man is able to clearly explain the new Tax law. Our articles on 2015 Asset Class Total Returns - Listed Property the best performer in a volatile year, Prudential December Fund Fact Sheets help us look back at how markets performed in 2015. We hope that 2016 be a great year with great Financial return for all our Clients ….All the best Best direction for your investments in 2016 It may come as a surprise that, when viewed from a foreigner’s perspective, the JSE All-share index has not increased in US dollar terms since October 2007. In rand terms, the prices of local equities more than doubled over this period. It’s also worth noting that since 2011 our local market has underperformed the world’s developed markets, as measured by the MSCI World Index, by 119% as the rand depreciated from R6.61 to R14.20 per dollar. Given the rand weakness and superior performance by developed market equities, our clients regularly ask us whether they should take more money offshore. At our client roadshow in early 2011, we advised clients to shift their portfolios towards developed market shares given the over-valued rand at the time and relatively attractive valuations of these markets. This was met with some reluctance given that South African shares had outperformed developed markets by more than 500% over the previous decade. The superior economic growth prospects of emerging markets relative to the developed world were also emphasised, while many investors remembered the painful consequences of moving money offshore at the worst possible time after the rand collapsed in 2001. Recent experiences and performances influence investor sentiment, but our investment philosophy takes us back to valuation/price as the primary consideration for investment decisions, while taking account of the prevailing trends and perspectives in the market. In line with what we have advocated since 2011, our asset allocation portfolios have invested the maximum weight in offshore markets that prudential legislation allows. In our equity selection, we have tilted our portfolios towards ‘rand-hedge’ companies that derive the majority of their earnings offshore and away from so-called SA Inc companies whose fortunes depend on the domestic economy. This has benefited portfolio performance, but we continuously reassess our positioning. The table below shows the past five years’ share performance and current valuation of five well-run rand hedge companies versus five well-run SA Inc companies listed on the JSE.  Click here to read more Please contact Kevin or Thato, email: invest@daberistic.com, if you have any queries about investments Source: Finance24 More for the future you, less for the tax man The tides are changing in the retirement savings space, with National Treasury encouraging us to save more for retirement by significantly increasing the tax incentives. This is one of several important changes that will go ahead from March this year, now that the President has approved the Taxation Laws Amendment Bill, 2015, which was passed by both Houses of Parliament at the end of last year. Gifts from SARS The wait is over for retirement fund members, who will enjoy increased tax deductions from their contributions to retirement funds. This includes provident funds, for which members were not previously able to claim a deduction. The tax deduction of up to 27.5% of the greater of taxable income or employment income, subject to an annual ceiling of R350 000, will come into effect. Another change is that employer contributions to occupational pension and provident funds will be included in the gross income of employees as a fringe benefit. This means that employees will be able to treat these contributions as their own when calculating their tax deductions. These deductions are subject to the limits mentioned above. You will have to buy an income-providing product…Retirement funds will also be aligned, ironing out some of the differences between the different products. One of the key changes is around ‘annuitisation’ – the process of converting retirement savings into a stream of future income. From 1 March, provident fund members, like retirement annuity and pension fund members, will only be allowed to take one-third of their retirement savings as cash and they will have to use the rest of their nest egg to buy a product that pays them an income during retirement. “Treasury has stressed that vested rights will be protected –i.e. the new rules will not apply to historic savings or to growth on those contributions.” …unless you are about to turn 55…If a provident fund member is 55 or older on 1 March, the new requirement will not apply. Any accumulated retirement savings as at 1 March, as well as new contributions and growth after 1 March, can still be taken as a cash lump sumat retirement. …or you have saved under R247 500 Members with a retirement benefit at retirement less thanor equal to R247 500 will be allowed to withdraw the entireamount without the need to purchase an annuity, as of March.This is an increase on the current value of R75 000. Click here to read more Please contact Kevin or Thato, email: invest@daberistic.com, if you have any queries about retirement funds or Allen Gray offerings Source: Allan Gray 2015 Asset Class Total Returns - Listed Property the best performer in a volatile year SA listed property was the best performer with a total return (income and capital) of 7.99% in ZAR in 2015  Global Listed Property (Developed Markets)

Please contact Kevin or Thato, email: invest@daberistic.com, if you have any queries about any investing Source: I-Net Bridge Prudential December fund fact sheets In December the US Federal Reserve finally raised interest rates for the first time since the 2007 Financial Crisis amid supportive economic data, easing some of the uncertainty hanging over global investors and pushing the US dollar still stronger. Chinese economic data also improved, partly relieving another source of uncertainty. However, global growth prospects, particularly emerging markets, continued to be revised downward, driving commodity prices, EM currencies and EM financial markets weaker (Brent crude lose 17.2% during the month). Assets continued to flow back to the US from riskier destinations. Most equity markets lost ground, as did bonds. Developed market equities produced a total return of -1.7% (MSCI World Free Index) and the MSCI Emerging Markets Index fell 2.2%. Global bonds were largely flat as the Barclays Global Aggregate Bond Index (US$) returned 0.6%, while precious metal prices fell: gold was down 0.34%, platinum -15.9% and palladium -20.5% (all in US dollars). South African bonds, listed property and the rand fell sharply amid the global environment and were all punished by "Nene-gate" on 10 and 11 December. Equities also lost ground as financial shares were hard-hit. The average equity fund returned -2.2% for the month, while the average high equity balanced fund delivered -0.2% (according to Morningstar, using ASISA categories). Multi-asset low-equity funds averaged -0.1%, and multi-asset income funds produced -0.3% on average. SA equities were lower in December in line with other developing markets: the FTSE/JSE All Share Index posted a total return of -1.7%. The All Bond Index suffered a 6.7% loss, and SA listed property returned -6.1%. Inflation-linked bonds were down 1.8%, while cash returned 0.5%. Over the month the rand weakened by 6.9% against the US dollar, by 5.0% against the pound sterling, and by 9.5% against the euro, making offshore assets the best performing for December. Prudential High Yield Bond Fund – The fund has returned -5.0% over 1 year and 1.4% over 3 years. This compares to -3.9% for the All Bond Index over 1 year. Long-dated bond yields have become even more attractive in the wake of December's weakness, rising to over 10%, so that the fund remains overweight duration. Please contact Kevin or Thato, email: invest@daberistic.com, for any queries about Prudential investments Source: Prudential Daberistic contacts details Kindly note the following to ensure you get the correct person to assist you with your insurance and investment queries. Life insurance and investments: Kevin Yeh, Thato Merementsi, Nicole Smith Tel 011 658 1333, email life@daberistic.com Medical aid / gap cover:Namhla Zwane,Sophie SuTel 011 658 1333, email health@daberistic.com Short-term insurance (Personal and Business): Thomas Mooke, Calvin Yen, Tel 011 658 1333, email shortterm@daberistic.com Retirement funds: Kevin Yeh, Tel 011 658 1333, email employeebenefits@daberistic.com Tax, Accountancy and Auditors: Su-Lan Chen or Su-Chin Chen, Tel 011 658 1333, email finance@daberistic.com 24-hour emergency cellphone number: 076 200 5488. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|