As you approach retirement age, you will be looking to your financial advisor to guide you in selecting the right retirement income solution to provide a sustainable income for the rest of your life.

Life or Living Annuity? Living annuities allow you to retain full control over your retirement capital: You can control your investment allocation, change your income drawdown annually (within a legislated range), and leave any remaining capital to your appointed beneficiaries upon your death. You will also need to manage the risks that come with this control by choosing an appropriate investment allocation and a suitably prudent income drawdown. Life annuities (or fixed annuities) allow you to receive a guaranteed income for life, with an insurer taking on some or all of the risks that you live longer than expected or returns are lower than required. You pass control of your retirement capital to the insurer, and typically, there will be lower or no capital for beneficiaries upon your death. You can add a guarantee option of 10 or 20 years to ensure income for your beneficiaries after you death for the remainder of the guaranteed period. Determining Income Drawdowns for Living Annuities The general rule of thumb for individuals retiring at around 60 to 65 years of age and drawing income from a living annuity suggests that you withdraw 4% of your capital in the first year of retirement and adjust for inflation only each year thereafter. This is based on investing and maintaining at least 50% in equities, which has been needed to sustain this income over 30 plus years in retirement. Ready to Plan Your Retirement Income Strategy? Speak to your financial advisor today to discuss your retirement goals and find the best income solution tailored to your needs. Your advisor can help you navigate the options and make informed decisions to secure a comfortable and sustainable retirement. Email service@daberistic.com or schedule a meeting with Kevin using this link: calendly.com/daberistic/60min

0 Comments

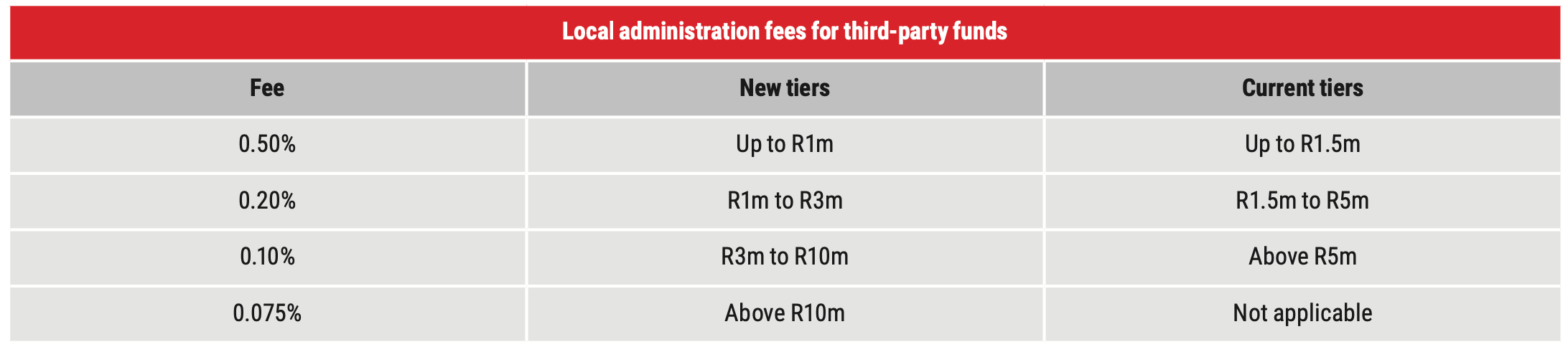

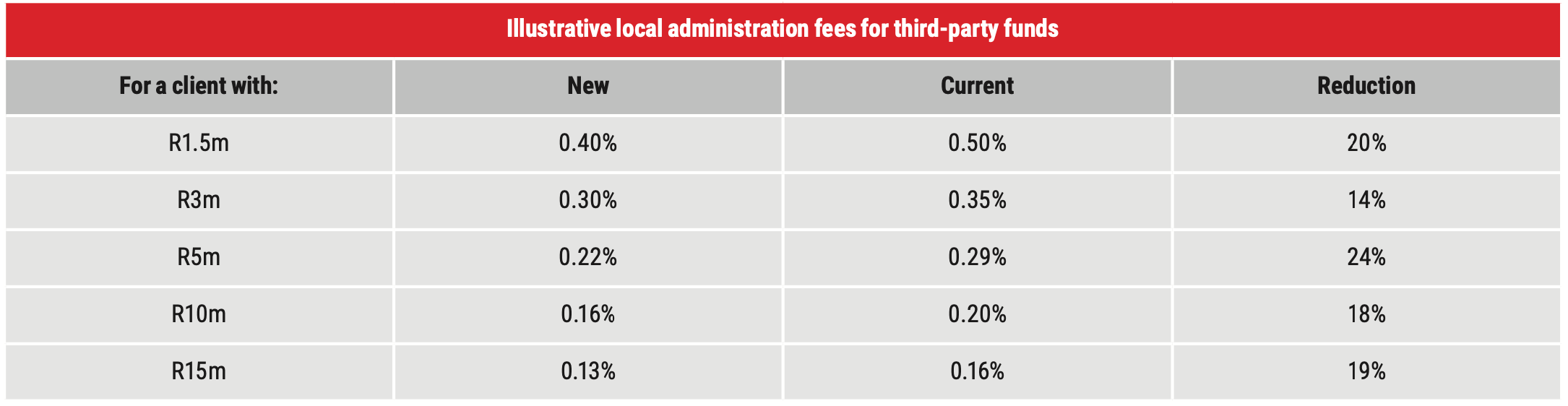

In our previous living annuity article, we discussed the impact of drawdowns and volatility in a living annuity portfolio, and how to choose an acceptable drawdown rate. This was done to provide context about choosing the right drawdown, so you do not run out of funds. It’s every retiree’s goal to not run out of money in retirement. Without the comfort of a defined-benefit plan that pays out guaranteed income, many retirees are left to generate cash flows from their investments exposed to the market. It is therefore important to have a portfolio that is geared towards generating healthy growth and returns, offers protection and is cost-effective, to ensure a long-term capital pool to draw an income from. As with the very best sporting teams, every asset in a portfolio plays a role—some assets are more proficient at defence and others press forward to attack—but they need to work together. It is also this cohesion that makes great portfolios.  We are pleased to share that Allan Gray, one of the largest linked investment service providers (LISPs) in South Africa, has reduced its adminsitration fees. Allan Gray have reduced their local administration fees for third-party funds, effective 1 October 2022. In early 2023, they will combine a client’s local and offshore platform assets for the purposes of calculating their applicable administration fees on each platform, enabling clients to benefit from lower fees. In early 2023, they will introduce a step fee for new clients investing below their lump sum minimum of R50,000. Allan Gray reducing local administration fees for third-party funds Allan Gray's new fees, which are effective 1 October 2022, are outlined below.  The administration fee charged for local Allan Gray funds will remain unchanged at 0.20% per annum (excl. VAT).  Combining local and offshore platform assets to calculate administration fees (from 2023)

Allan Gray will combine your local and offshore platform assets when calculating your administration fees which will result in more of your assets being subject to the lower fee tiers. Currently, your local administration fees are based on the market value of all local platform assets linked to your investor number and applied to the local administration fee tiers. Your offshore administration fees are calculated separately based on the market value of all offshore platform assets linked to your investor number and applied to the offshore administration fee tiers. The effective date of this change will be communicated ahead of implementation in early 2023. What does this all mean for you as an investor? For clients with assets more than R1 million with Allan Gray, they will enjoy reduced administration fees, so they will keep more of the investment returns. We applaud Allan Gray for reducing costs of investing for clients. For clients with assets less than R1 million with Allan Gray, the 0.5% administration fee stays the same. For new clients with less than R50,000 invested, they will have to pay a step administration fee of 1.0% per annum (excl. VAT), until their investment value has reached R50,000. So Allan Gray is not so cost effective towards smaller investors. This cost is understandable, as there is a base cost of opening and maintaining an investor account. If you have any questions or feedback, email us at service@daberistic.com In partnership with Morningstar: When comparing current markets to that of a year ago, it is hard to believe that we are already in a completely different place in such a short amount of time. What started as a strong recovery (after the March 2020 crash), synchronized global growth and supportive monetary policy has turned due to war, mentions of a potential recession approaching, four-decade high inflation, a rise in bond yields and rising interest rates across most markets. Planning how to manage your capital after retirement is probably one of the most complex problems in financial planning, especially when markets are turbulent.  According to a study, 90% of people who retire with money from their retirement funds buy living annuities to provide them with a regular income in retirement. So what are living annuities? And what are life annuities? Are life annuities dead? I would like to explain these two types of products for provision of retirement income. It would be very beneficial for you to generate a more detailed financial plan to give you a better understanding of your options. You can use this tool from 10x. Life annuities and living annuities are the two main products that can provide you with an income from your retirement savings. A life annuity is an insurance-type product and a living annuity is an investment-type product. Each of these meets different needs so you will need to decide which will best meet your particular goals. Life Annuity Life annuity is also called fixed annuity or guaranteed annuity. A life annuity is a contract between you and a life insurance company. You give the life insurance company a retirement capital lump sum. In return, it secures you a pre-determined income for the rest of your life. There are different types of guaranteed annuities. Some provide an income that increases with inflation, others pay a level income and others yet may increase over time, subject to market returns. In order to ensure a level of income that sustains your lifestyle needs, you should consider an inflation-linked life annuity, which provides an income that keeps pace with inflation. Although your income is guaranteed for your whole life, your income ceases when you die. Your heirs won't be able to inherit whatever is left on the death. In other words, the capital dies with the investor. For the sake of guaranteeing value for money, I suggest you purchase a life annuity with an underlying guarantee of income for a minimum period, typically between 10 to 20 years. This period is called a guarantee period. A life annuity with a guarantee period will pay a slightly lower retirement income than one without a guaranteed period. Typically, you also have no say over the initial income and no flexibility to change your income or to move to another annuity or service provider once you've purchased the product. It is wise to use a financial advisor to get quotes from reputable annuity providers, to get the best initial income, terms and conditions. Living annuity On the other hand, a living annuity provides investors with flexibility to choose their income each year (subject to regulatory limits) and where their money is invested. This will give you the flexibility to draw a lower or higher income as and when your needs change. It will provide you with the flexibility to change service providers or purchase a guaranteed annuity at any time. Any remaining capital upon death passes to your heirs. However, in exchange for this flexibility, you take on the risk that the income may not last for your retirement years (on average about 30 years), as well as the risk that their investment returns are poor. This means that your future income could fail to keep up with inflation, or even that you outlive your savings. Below is a table summarising the difference between an inflation-linked guaranteed annuity and a living annuity:

Tax At retirement you may cash in up to 100% of the value of your provident fund, up to one-third of the value of your pension fund, and up to one-third of the value of your retirement annuity. However, there are potentially tax implications to taking a portion in cash. The table below shows you the tax rates for various cash amounts taken at retirement.

In addition to the tax above, the income you receive from either a life or living annuity would be taxed as per the applicable income tax table.

Which one should you buy? There are three possible options: A life annuity, a living annuity, or a combination of the two. Yes, it is possible to deploy your retirement capital to both types of products at the same time. There are two important factors to consider when you buy annuities: Health and flexibility. If you are healthy and your family exhibits a history of longevity, you should consider buying a life annuity with at least part, if not all of your retirement capital, with the balance in a living annuity. People that live longer will score with a life annuity, as they will get (a lot) more than they put in. While the liviing annuity gives you the flexibility to adjust your income as and when your needs change. If you are not healthy, e.g. having chronic conditions such as diabetes, heart conditions, hypertension, you may want to put most, if not all of your retirement capital into a living annuity. This way, you can enjoy the fruits of your years of hard work and savings while still alive, and able to leave the balance to your loved ones when you die. The balance is invested in a life annuity, to provide you with some guaranteed income. With a living annuity, the recommended drawdown rate, the percentage of the capital you draw as income, is 5% per annum. This would ensure the money should last you for up to 30 years in retirement. If you need a higher level of income, you should buy a living annuity, which allows you to withdraw up to 17.5% of your capital as income. Bear in mind that the more you withdraw, the quicker the money in a living annuity runs out. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|