Discovery Insure’s latest Drive Trends Report reveals that fuel price hikes have implications on South Africans’ daily lives. Many consumers are spending more at the pump than they used to but getting fewer litres of fuel in total. It is no surprise then that many are taking fewer work trips per month. The data also reveals interesting findings into driving behaviour in different provinces and speeding behaviour - showing an increase in speeding incidents, especially on weekends.

The Drive Trends Report, released on 30 November 2023, analysed the driving behaviour of over 240,000 drivers on Discovery Insure’s Vitality Drive programme. The data, gathered between January and October 2023, resoundingly confirms that clients’ purchasing behaviour changes when the fuel price changes. The latest data shows that when the fuel price is around R22 per litre, the average client spends around R1,950 per month. However, when the fuel price increases above R24 per litre, clients spend around R2,150 each month and get almost 3 litres less in fuel. In the current environment, this puts additional financial pressure on clients and by extension, on South Africans. “Discovery Insure is helping clients beat the increasing cost of fuel by rewarding them with up to 50% of their fuel spend back for driving well. So, when the price of fuel goes up clients can earn more in fuel rewards every month,” says Robert Attwell, CEO at Discovery Insure. Given the financial pressure many are facing, it was not surprising to see that there is a change in consumer driving behaviour. On average, clients are now taking 5 less work trips per month compared to one year ago. Provinces with denser traffic conditions have higher fuel consumption. The data also shows that clients in Gauteng, the Western Cape, KwaZulu-Natal and the Eastern Cape have an average fuel consumption that is nearly 1 litre per 100km more than that of clients in the other provinces. This is a result of worse traffic in these regions compared to other provinces. When it comes to fuel efficiency, i.e., how much fuel is consumed per kilometre driven, Limpopo drivers top the charts with an average fuel consumption of 6 litres per 100km. By comparison, if Gauteng drivers had the same fuel efficiency as Limpopo drivers, they could save almost 20% of their fuel bill every month! Western Cape drivers and women speed the least. Discovery Insure’s Vitality Drive programme has been using telematics to measure driver behaviour for more than a decade now. It rewards clients for driving well through incentives that include the most competitive cash back on fuel spend in the market. Vitality Drive clients earn points based on how well they drive. The more Vitality Drive points a client earns, the higher their Vitality Drive status, and the more rewards and benefits they get. Clients start each day with 60 points, and, using the principle of loss aversion, Discovery Insure deducts points throughout the day for poor driving behaviours such accelerating, braking and cornering harshly, as well as cell phone use and speeding. Of these driving behaviours, the Drive Trends Report reveals that speeding is the worst driving behaviour among clients, as drivers lose most of their points for driving too fast compared to other poor driving behaviours. Drivers who claim lose as much as 83% more points from speeding than those who don’t claim. The data also showed that people speed 50% more on weekends compared to weekdays suggesting that less traffic could contribute to this behaviour. People aged between 30 and 35 speed the most. “This data is powerful because it tells a story. Speeding remains stubbornly high. It is concerning to see from the data that many South Africans, particularly those in their early to mid-thirties, still tend to drive too fast on our roads,” says Attwell. Alongside the fuel price and its financial constraints implications, the report also confirms something else many of us already knew: It shows that Western Cape drivers and women, nationally, speed the least. “In fact, women lose 30% less points for speeding compared to men,” says Attwell. Most people leave for work at 6:45am, and they can optimise their ETA. Attwell adds that the Drive Trends Report shows that on weekdays, the peak driving time for the morning is 6:45 am, indicating that most people start work, in-office, between 7am and 8am. He also notes that, using Discovery’s data, South Africans can optimise their workday estimated time of arrival (ETAs) by changing their departure time. Instead of starting a trip between 7am and 8am, drivers can spend 14% less time on the road by leaving the house between 6am and 7am, and 11% if they leave after 8am. We all know that every minute stuck in traffic counts, especially during load-shedding and with the price of fuel. The Vitality Drive programme continues to help shift driving behaviours for the better through clients’ engagement, and not only does Vitality Drive help make our roads safer, but a much-needed fuel cash back benefit also helps clients’ wallets. “Discovery has paid over R1.8 billion in fuel cash back to drivers”, says Attwell. “Along with the latest Drive Trends Report findings – which give valuable insight so we can create better experiences and products for our clients – Vitality Drive provides tangible value, like easing the impact of the fuel price, and ultimately, helping to drive change.” If you would like to add Vitality Drive to your policy please contact Nigel email: service@daberistic.com tel:(011)658-1333 Source: Discovery Insure

0 Comments

Santam has informed us of the latest changes in their policy endorsements regarding Power Surge & Electricity Grid Failure. The last couple of months has been a period of immense challenges for our country. We have seen high levels of load shedding, which impacts our daily lives. The country’s power utility has reassured all of us that it is working hard to protect our electricity grid by balancing supply and demand in a controlled, risk-managed manner. Within this environment, Santam wants to provide you with clarity on your cover, cover changes, and tips on how to reduce your risk. Power Surge cover Load shedding, the temporary switching off of power supply in a scheduled and controlled manner, in itself, is not explicitly covered by insurance policies. However, it does result in the frequent switching on of electricity supply to your premises and, depending on the quality of the network and the components thereof, it could cause power surge that damages your electronic items. Subject to the electricity grid failure or interruption exclusion noted below, Santam continues to provide cover for power surge damage, including after load shedding, if selected on your policy. During the last 12 months, our power surge claims have however increased by around 50%, and more than 200% over the last 3 years. To ensure the sustainability of this power surge cover, with effect from 1 June 2023, the following comes into effect: 1. You will have a compulsory excess amount of minimum 10% of claim , subject to a minimum of R5 000 when claiming for any pow surge damage. This minimum excess amount will also apply to any lightning strike damage under the business all risk, personal all rand electronic equipment sections of cover. 2. The following will be excluded from our power surge cover: - Power surge damage that occurs as a result of switching on electricity, following load shedding in excess of 12 consecutive hours. - Power surge damage that occurs as a result of switching on electricity, following electricity grid failure or interruption. 3. The Accidental Damage section of cover no longer provides cover for damage caused by power surge, as this can be specifically insured under its own specific section of cover. SOME TIPS TO HELP YOU REDUCE OR EVEN ELIMINATE YOUR RISK OF LOSS DUE TO POWER SURGE: It is best to unplug your devices when the power has been switched off. After power has been restored to your premises, it should be safe to plug them back in again. In an electricity grid failure or interruption scenario, this is especially important. Surge arrestors or surge protection devices may provide protection, depending on the type of surge experienced. The following should be considered: - Any device should come with a warranty of at least 5 years, for which you should receive an installation certificate. - Any device should protect against over voltage, under voltage, multiple strikes and lightning surge. Remember to check your policy to confirm your power supply covers, including their insured amounts. You can select, reduce or increase your power surge cover options at any time, with the resultant impact on your premium. Electricity grid failure or interruption Electricity grid failure or interruption means a total or partial interruption; interference; suspension; blackout; failure; of electricity supply in connection with any national; regional; municipal; local; private; grid, in connection with any premises or business of the Insured. With effect from 1 June 2023, Santam’s electricity grid failure or interruption exclusion applies and where already enforced, is extended to incorporate the following: 1. Any damage caused directly or indirectly by electricity grid failure or interruption, except as specifically provided for under the Business Interruption section in respect of elective extensions to other premises, namely: – Public telecommunications – insured perils – Public utilities – insured perils and then further subject to the Electricity grid failure or interruption being to an area not greater than any one single municipal area. Power surge damage as noted by point 2 under Power Surge cover above2. Click here for link on FAQ on these changes Should you have any questions regarding your policy please contact Koketso email:service@daberistic.com tel:(011)658-1333  Imagine submitting a claim to your insurance company, only to have it rejected based on information you don’t understand. What should you do, when the insurer just does not understand your view? Well, meet the insurance ombudsman – it is his job to care about your dispute!

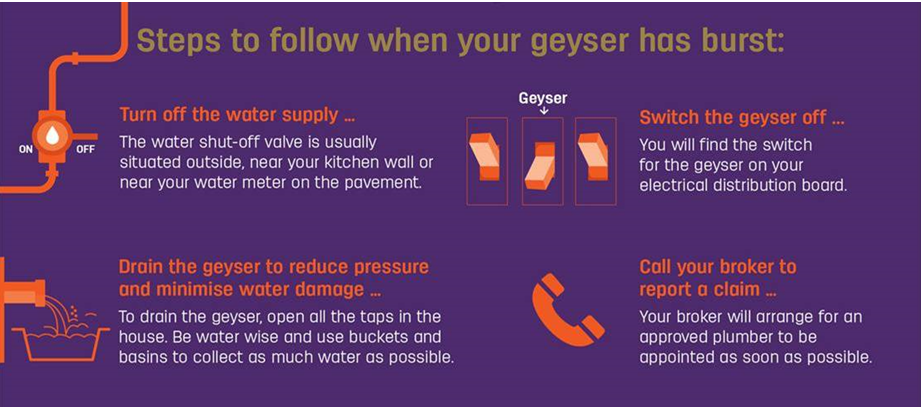

An ombudsman is an official whose duty it is to represent the interests of the public, by investigating and addressing complaints of maladministration or a violation of rights; are usually appointed by the government or parliament; and is not supposed to be influenced by political parties or affiliations, but should be able to conduct an independent investigation into the complaint that was laid. In short, the ombudsman serves as a mediator. South Africa has the various ombudsman available to its citizens, but today we will focus on the short term and long term insurance ombudsman and its roles and responsibilities; both of which are recognised in terms of the provisons of the Financial Services Ombud Schemes Act. Every short-term insurer has agreed to abide by the decision of the Ombudsman and this can relate to any of the following personal lines of short-term insurance: motor; house owners (building insurance); householders (content insurance); cell phone; travel; disability; credit protection insurance; commercial insurance; claims disputes; etc. The Ombudsman for Long-Term Insurance has the main duty of resolving complaints through mediation, recommendation and then, as a last resort, determination (or rulings). These determinations or rulings are legally binding on the contributing insurer, but not on the complainant, who has the option to go to court if unsatisfied with the ruling. The essential characteristics of an ombudsman are important, as it determines its impartiality. The insurance ombudsman should be free from interference in the performance of its duties and it should be independent from influence. They must also produce decisions that are seen to be fair, by making decisions based on the information available and having pre-set criteria for reaching a decision. Accountability to the public is ensured by having its decisions published and made available to the public. Lastly, the ombudsman should work effectively by following informal and cost-effective procedures, supported by sufficient human, financial and operational resources. So, what procedure should be followed once you realise you’ll need the ombudsman? Well, firstly, you should have tried to resolve the matter with the company concerned, by following their internal grievance procedure. If this did not solve your problem, you should contact the Ombudsman; who will require that you submit a complaint (preferably in writing) and provide them with the necessary information such as the insurance company’s name, policy number, contact details and a factual summary of your complaint. You should submit all relevant supporting documents available, including proof of your attempted resolution with the company. The ombudsman will then start its investigation and guide you through the rest of the process. Isn’t it great to know that there is someone out there who can assist you when it seems you’ve run out of options?! Make sure you have the relevant contact details of the ombudsman you need to help you solve your problem as soon as possible! By clicking on the below you will be able to get the various Ombudsman contact details: Long Term Insurance Ombudsman Short Term Insurance Ombudsman Health Ombudsman Pension Fund Adjudicator (PFA) FAIS Ombudsman ( For Investments) If you have any queries for Short-term insurance please email service@daberistic.com Source: Hollard  We continue to share a 5-part series on Home Insurance Tips. In this article we share on Solving your geyser problems. We usually don’t dwell on things that can go wrong with the geyser, the reality is that something will, at some point. Most electrical geyser manufacturers supply a warranty for the actual geyser for between five and ten years, but its individual components only carry a warranty of one to two years. What are geyser components? These are items that generally wear, such as thermostats, elements, pressure control valves, vacuum breakers, seals and gaskets. When a geyser component fails, it doesn’t necessarily mean the geyser needs to be replaced. If something goes wrong with one of these components, check with your broker if your insurance policy covers it. Most importantly, if you suspect that your geyser is leaking or has burst, report your claim to your broker so that they can appoint a qualified plumber to see to the problem. If you don’t, you may find yourself out of pocket due to limits on your policy when not using an approved plumber. Did you know?

What to look out for

If you like us to review your Home cover contact William our Short-term department email service@daberistic.com tel (011)658-1333

Source: Hollard  Record-high fuel prices in South Africa Orlik (2022) states that South Africa has faced one of its toughest economic slumps, due to the COVID-19 pandemic. Lockdown restrictions had a massive impact on the economy of the country. Many consumers are still facing the financial impact and struggling to keep head above water. South Africa has also seen fuel prices hit a record-high in the first six months of 2022. Fuel prices are mainly affected by two components (BusinessTech, 2022): 1. The rand/dollar exchange rate 2. Changes to the costs of international petroleum products, primarily driven by oil prices Russia’s invasion of Ukraine has a massive impact on the fuel price increase as well. According to André Thomashausen, an emeritus professor of international law at Unisa, fuel prices could continue to rise to over R40 per litre, in the worst-case scenario (Prior, 2022). On top of this, consumers also must pay more for public transport, food and other services, all affected by the increase in fuel price. Consumer are facing even more pressure to survive in trying times. 10 tips to help your tank last longer There must surely be ways to save fuel during these tough economic times with fuel prices continuing to rise. Saving fuel is something we can all benefit from. After all, who would not want their tank of fuel to last longer?  Vitality Drive helps clients save on fuel Click here to read more

If you would like to Apply for Vitality Drive or Do a comparative quote contact Ed in our Short-term department email: service@daberistic.com tel (011)658-1333 Source: Discovery Insure  Breaking up is hard to do – but not in the case of your insurance company. You can switch insurance to whichever company you want, whenever you want. It should never be difficult or ‘wrong’ to change insurance companies. You might want to hold out for a no-claims bonus or think that your loyalty will be repaid with lower premiums, however if you feel that your insurance provider no longer has your best interests at heart, it might be time to move on – no matter what time of year or at what point of your policy term you are.

What is a policy and what is a term? Remember that short-term insurance is different from things like medical aid and life insurance in that it doesn’t impose blackout periods or conditions which stipulate when you are allowed to claim. You are 100% covered on your car, home contents or buildings from day one. You don’t get more covered as time goes by. If you pay premiums on a month-to-month basis, you can simply notify your insurer that you want to cancel your policy (your contract). That’s it – simple as that. They may try to woo you with reduced premiums but you are under no obligation to accept their offer. It doesn’t matter if you’re approaching your renewal date or if you are in the middle of your policy term (mid-policy or mid-term). If you’ve paid for a whole year in advance – i.e. for a 12-month term/duration – and you cancel halfway through this period, your insurance company will pay back your premium on a pro rata basis. The only reason why they won’t pay you back is if you’ve claimed to the value of the maximum insured amount. Tip: Remember that all insurance companies look at your claims history to determine your insurability as a client so if you’ve made a lot of claims during your term, a new insurance company might charge you a higher premium than your existing provider. A poor claims history, a previous insurance policy cancelled by the insurer due to excessive/ fraudulent claims and a high risk profile (e.g. geographical location or high performance vehicle combined with an inexperienced driver) are all reasons why you may be refused insurance. Reasons to switch insurers Here are a few common reasons why people decide to call it a day with their insurance company. Have a look to see if any of these apply to you and if it’s time to get a new quote:

Opportunities to relook your insurance Even if you are not unhappy with your current insurer, it might be a good idea to review your cover if: You recently got married or divorced, and you are restructuring your assets, responsibilities and finances. You want to add or remove a driver who no longer lives with you – e.g. a student child who has moved or a child who just got their driver’s licence. You’ve bought a new car or home, or a lot of new and expensive tools/furniture/electronic equipment. You’ve just welcomed a new dog into your home and want to raise your liability cover. You’ve changed jobs and want to update your mileage or where the car is parked, for example. Things to remember before changing Before you make a decision to switch insurers, be sure to compare the extent and limits of cover to your existing policy and check your new policy for excess fees. The deal you are getting may not be as great as you think if you discover that your new insurer offered you a much lower premium at the expense of your type of cover and insured amounts. If you would like us to review your current insurance and cover please contact Marizka in our Short-term department email service@daberistic.com (011)658-1333 Source: Santam  In South Africa, having a car is a necessity which at the same time brings the risk of a motor accident. And let’s face it – motor accident is the last thing on our mind, hence when we encounter it, we often do not know what to do. The purpose of this article is to share some info on the topic, so that you are better prepared in the event of a motor accident.

First and foremost, it is imperative that you remain calm and put safety first. Many people often get out of the car immediately in order to check for damages (or in some cases, argue with the other party), without first checking surroundings. This is very dangerous, particularly on a highway or major roads, hence this must be remembered. If you feel unwell after the incident, limit your movement and wait for paramedics to arrive on the scene. Secondly, you should not admit any liability. This is an accident which no one wanted to happen, so leave the liability matter to the insurer who will represent you in the case. Furthermore, record as much evidence as possible. Fortunately, these days we all have a cell phone, so you can take pictures and record key information such as:

So what should you call the police? If there are no injuries or major blockage of the road, then you don’t have to call the police – you can register the case at the nearest police station within 24 hours. If there are injuries, then the cars can only be moved after police arrives on the scene and takes proper record. In terms of towing, if the car remains drivable, then no towing service is needed. However, if you are worried that driving it may cause further damage (or the car is not drivable at all), then we suggest that you contact your insurer to arrange towing and storage by their appointed service provider to avoid any potential issues. If needed, the police has the right to tow the car for further investigation. Last but not least, remember to inform your insurance advisor after the incident and provide true and accurate information, so that the claim can be processed without delay. If you have any short-term insurance needs, you can contact us on the following channels:

|

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|