|

This comes as no surprise, but us as human beings prefer immediate gratification. In fact, research indicates that 55% of people will prioritise immediate consumption over putting money away for the future. This is known as ‘present bias’ – we don’t like thinking about the future and we mistakenly assume we will have time to make up any deficit by startingto save and invest later. I am sure that this sounds very familiar to you as a financial adviser, and you probably encounter this too often with your clients.

0 Comments

In 2024, South Africa will finally see another major change to our retirement system. Although known as the “Two Pot system”, in reality, and for most, it will be a new three pot system. All retirement savings invested before 1 September 2024 will vest in a vested pot (pot 1), while all new contributions after 1 September 2024 will be allocated between a savings pot (pot 2) and a retirement pot (pot 3). Investors aged 55 and older as of 1 September 2024 will only have one pot - if you so choose.  Around this time of the year, we would like to remind you to consider topping up your retirement annuity fund and tax-free investment.

Retirement Annuity According to the current legislation, you may contribute up to 27.5% of your taxable income to a retirement annuity fund and enjoy tax deductions, subject to a limit of R350,000. As the 29th February is the end of the tax year, you must calculate and pay the additional amount to your retirement annuity prior to this date, in order to qualify for tax deductions and tax refunds. Here is an example: Ms Rama has a monthly salary of R80,000. In December she received a bonus of R100,000. Every month she contributes R5,000 to a personal retirement annuity fund. Her annual income is then R1,060,000. The maximum tax-deductible contribution to retirement annuity is R291,500. Over the year she has contributed R60,000 to her retirement annuity fund, so the additional amount she may top up in her RA is R231,500. Tax-Free Savings Account You may contribute up to R36,000 to a tax-free savings account in a tax year. You must calculate how much you have contributed so far, R36,000 is total contribution across investment platforms for member not per investment. You can pay the additional amount to your tax-free savings account prior to the 29th of February, in order to make use of current tax year's allowance. You can also start a tax-free investment in the name of your children. If you would like to speak to a Financial advisor, contact In our previous living annuity article, we discussed the impact of drawdowns and volatility in a living annuity portfolio, and how to choose an acceptable drawdown rate. This was done to provide context about choosing the right drawdown, so you do not run out of funds. It’s every retiree’s goal to not run out of money in retirement. Without the comfort of a defined-benefit plan that pays out guaranteed income, many retirees are left to generate cash flows from their investments exposed to the market. It is therefore important to have a portfolio that is geared towards generating healthy growth and returns, offers protection and is cost-effective, to ensure a long-term capital pool to draw an income from. As with the very best sporting teams, every asset in a portfolio plays a role—some assets are more proficient at defence and others press forward to attack—but they need to work together. It is also this cohesion that makes great portfolios. Morningstar Investment Management has informed us of managed portfolio changes. Please click below to view the letter.

“South Africans are not saving enough for retirement!” screech the headlines at least once a year, followed by industry pundits such as myself citing shocking statistics such as “90% of retirees are unable to maintain their standard of living after retirement”.

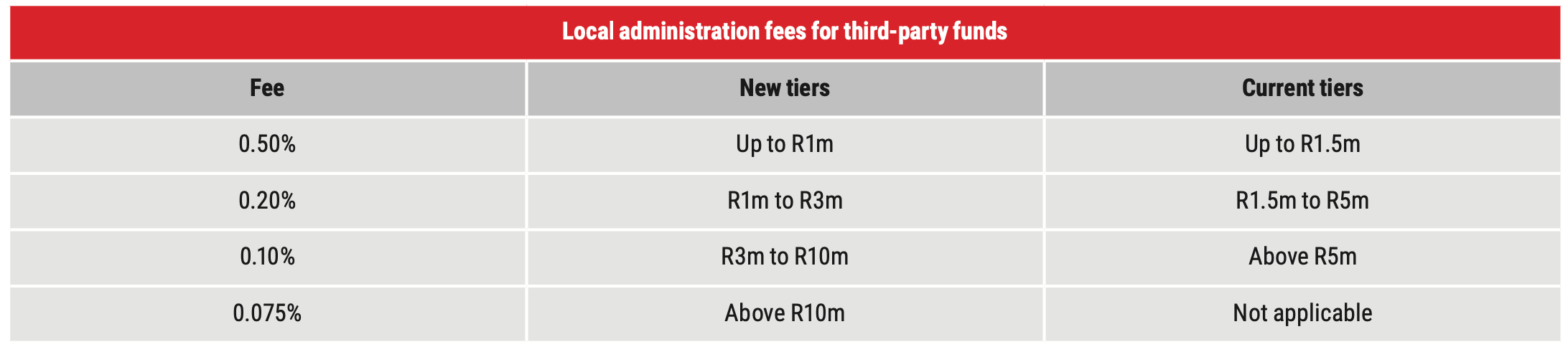

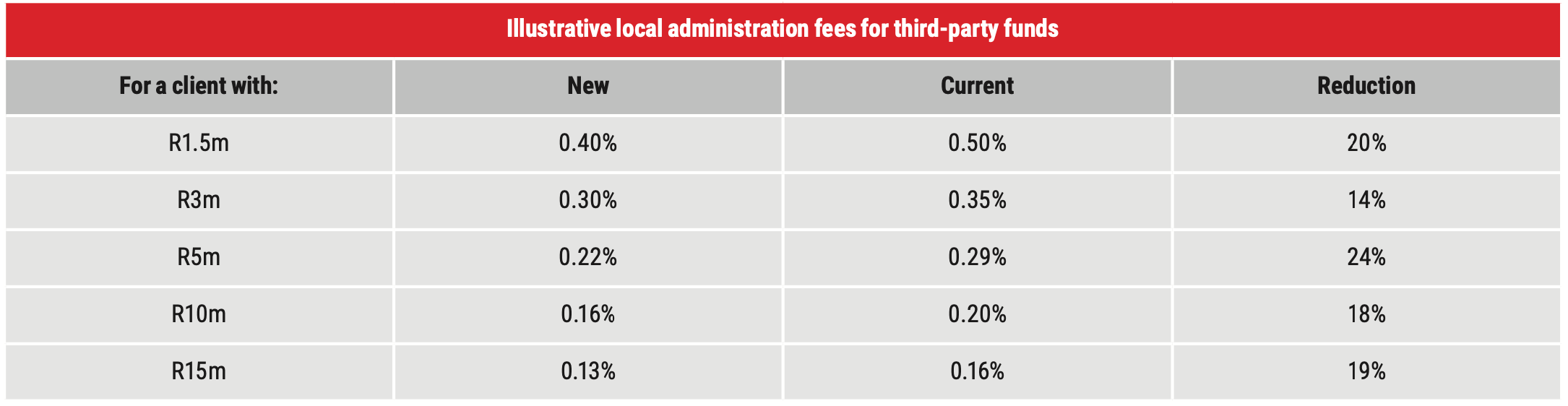

Hair-raising stats like this, taken from a January 2022 study by Genesis Analytics and the Financial Sector Conduct Authority (FSCA), are published year after year but have done little to scare under-saving South Africans to change their ways. This is evidenced by the same study’s finding that two-thirds of retirement fund members have less than R50,000 saved. If the definition of insanity, according to the wisdom of Albert Einstein, is doing the same thing over and over and expecting different results, we need to try something new to incentivise 90% of South Africans to save adequately for retirement. This is why I welcome the government’s new “two-pot” retirement system, which is now set to be introduced on March 1 2024 as opposed to the initial and somewhat unrealistic date of March 1 2023. It is a long-overdue revamp of a system that is clearly not effective, a fact that was reiterated in November when SA slipped even further down in the Mercer CFA Institute Global Pension Index. SA dropped three places this year: down to 34 out of the 44 pensions systems the index benchmarks. There are still many details that need to be finalised before the new two-pot system is promulgated along with the annual budget in March 2023, but the broad aims already agreed on will put structures in place to entice South Africans not only to save for retirement, but preserve these savings until retirement age. And it will provide South Africans with another accessible tax-free savings vehicle once they’ve maxed out their annual or lifetime tax-free savings allowance. Enforced preservation with more flexibility The two-pot system will apply to all members of pension and provident funds, umbrella funds and retirement annuity funds who were under the age of 55 as of March 1 2021. It is designed to address the achilles heel of the current retirement system: members are able to cash in their entire savings if they change or lose jobs. This all-or-nothing preretirement withdrawal rule radically reduces members’ chances of achieving their retirement goals. And since early withdrawals count towards each member’s one-off R500,000 tax-free lump sum withdrawal allowance, large preretirement withdrawals sabotage a member’s retirement outcome. The two-pot system will change this by splitting retirement savings: two-thirds of contributions will go into a retirement pot and one-third into a savings pot. The retirement pot cannot be touched until retirement, even if you lose or change your job, and must be annuitised at retirement. “The new 'two-pot' retirement system is designed to address the Achilles' heel of the current retirement system, which allows large preretirement withdrawals that sabotage a member’s retirement outcome.” Kyle Hulett, head of investments at Sygnia Asset Management If you would like to set up an appointment with our Financial Advisor contact Sandra, email: service@daberistic.com tel (011)658-1333 Written by: Kyle Hulett Source: Timeslive  We are pleased to share that Allan Gray, one of the largest linked investment service providers (LISPs) in South Africa, has reduced its adminsitration fees. Allan Gray have reduced their local administration fees for third-party funds, effective 1 October 2022. In early 2023, they will combine a client’s local and offshore platform assets for the purposes of calculating their applicable administration fees on each platform, enabling clients to benefit from lower fees. In early 2023, they will introduce a step fee for new clients investing below their lump sum minimum of R50,000. Allan Gray reducing local administration fees for third-party funds Allan Gray's new fees, which are effective 1 October 2022, are outlined below.  The administration fee charged for local Allan Gray funds will remain unchanged at 0.20% per annum (excl. VAT).  Combining local and offshore platform assets to calculate administration fees (from 2023)

Allan Gray will combine your local and offshore platform assets when calculating your administration fees which will result in more of your assets being subject to the lower fee tiers. Currently, your local administration fees are based on the market value of all local platform assets linked to your investor number and applied to the local administration fee tiers. Your offshore administration fees are calculated separately based on the market value of all offshore platform assets linked to your investor number and applied to the offshore administration fee tiers. The effective date of this change will be communicated ahead of implementation in early 2023. What does this all mean for you as an investor? For clients with assets more than R1 million with Allan Gray, they will enjoy reduced administration fees, so they will keep more of the investment returns. We applaud Allan Gray for reducing costs of investing for clients. For clients with assets less than R1 million with Allan Gray, the 0.5% administration fee stays the same. For new clients with less than R50,000 invested, they will have to pay a step administration fee of 1.0% per annum (excl. VAT), until their investment value has reached R50,000. So Allan Gray is not so cost effective towards smaller investors. This cost is understandable, as there is a base cost of opening and maintaining an investor account. If you have any questions or feedback, email us at service@daberistic.com |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

||

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|