|

There are several factors to consider when determining how much life insurance coverage you need. Here are some steps you can follow to calculate your coverage needs:

1. Determine your financial obligations: Make a list of your current and future financial obligations, such as outstanding debts, mortgages, and tuition payments. 2. Calculate your income: Consider your current income and any future income you anticipate receiving, such as raises or promotions. 3. Consider the length of your coverage: Determine how long you need your coverage to last, taking into account the length of time your dependents will need financial support. 4. Calculate your expenses: Estimate your living expenses, including housing, food, transportation, and any other recurring costs. 5. Consider any additional expenses: Think about any one-time expenses that your dependents may incur in the event of your death, such as funeral and burial costs. 6. Add up your obligations and expenses: Add up all of your financial obligations and living expenses to get a total amount of coverage you need. It's good idea to review your coverage needs periodically to make sure they are still adequate as your circumstances change.

0 Comments

Smartphones nowadays are a supercomputer in a small form factor. Premium smartphones can cost a lot of money. iPhone 12 Pro Max and Samsung Galaxy Z Fold 2 can easily cost more than R30,000. It is important to insure these expensive items. I have been waiting patiently for the arrival of iPhone 12 in South Africa (alas, we are always last in line in the world). Finally, it arrived on 18 December, and I upgraded from iPhone 6s Plus to a iPhone 12 128GB, which cost R19,999. I contacted a couple of insurers to get a quote to insure my new phone. Company D quoted R350 per month premium with an excess of R750. Company O quoted R255.60 per month premium, with an excess of R1,660. Both for all risks, which means if my phone is accidentally damaged, stolen, screen is cracked, mechanical failure, it's covered. It is important to note that, if you leave your phone in your car, it must be concealed, hidden, e.g. in a glove compartment, centre console, or car boot, with your car locked. Too often we just leave the phone lying around in the car. If our car is broken into and our phone stolen, the insurer will reject the claim. Based on my back-of-envelope calculation, below will be the reasonable price range to insure your smartphone at various price points:

Remember to backup your apps, data and settings in iCloud for iPhones and Google Drive for Android phones, irrespective of whether you insure your phone or not. Backing up your apps and data will make restoring your phone much easier when you upgrade your phone or get a new phone. Your precious data and photos are not something insurance can buy or backup.

Need to insure your expensive smartphone? Contact Marizka in our Short-term Insurance Department to get quotes and advice, on 011-658-1333, or service@daberistic.com.  It is now time to review your medical aid scheme cover for 2021. This means you have a window within which you can switch to a different plan for the new year. This window usually closes at the end of November (depending on your current provider), so don’t delay collecting the necessary information. This is not a decision to be rushed.

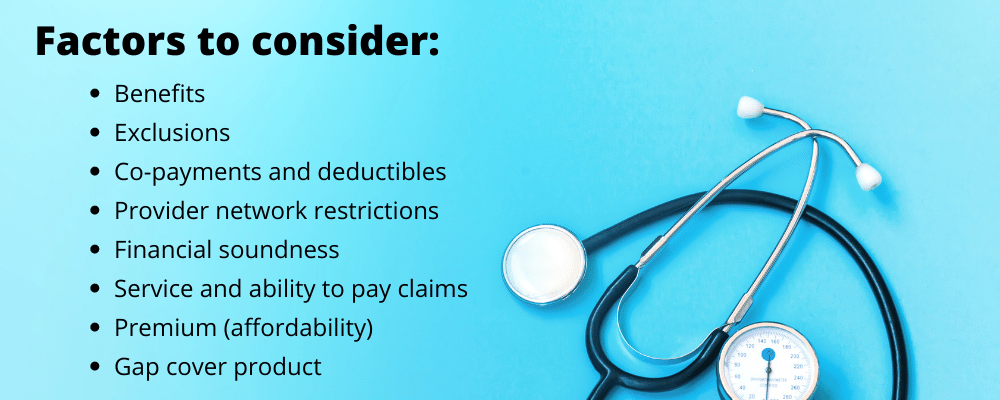

Why do I have to decide now? Medical aid providers allow you to switch to a higher plan once a year (at the end of the year) without penalties or consequences. If you want to save on premiums or you need to increase benefits, now is the time to do it. Generally, medical schemes give you until the end of the year to change your plan. What if I want to change providers altogether? If you are unhappy with your medical aid provider, you can switch to another at any time of the year. But before you do, consider the following: Waiting Periods Medical Aids by law must accept anyone who applies to join their scheme. To protect themselves from older or sickly members that join without having contributed to the risk pool, they usually impose a waiting period of between 3 and 12 months. Waiting periods will apply if 1) you have not been a member of another South African medical aid for the past three months or more, 2) if you change medical schemes before 2 years of being covered with your previous medical aid provider and 3) if you have a pre-existing medical condition. Finding out about any waiting periods is extremely important before deciding to change providers. Late joiner penalty As an additional means to manage the risk of older or sickly members joining without having contributed to the risk pool, medical schemes (according to the Medical Schemes Act) are entitles to add a late joiner penalty to your premium if you were not part of a medical scheme before 01 April 2001. The late joiner penalty is calculated (using a prescribed formula) based on the number of years that you were not on a registered South African medical scheme. The late joiner fee can range between 5% and 75% of the total contribution, depending on the number of years that you were not covered by a medical scheme. It is important to keep proof of all your previous medical scheme membership, as it would help reduce or remove the Late Joiner Penalty. General considerations When reviewing your medical aid plan, you should consider the following factors: - benefits - exclusions - co-payments and deductibles - provider network restrictions - financial soundness of the medical scheme - the medical scheme's service and ability to pay claims - premium (affordability) - gap cover product to supplement your medical aid. Please contact our health team, Tel 011-658-1333, Option 2, or email service@daberistic.com , to find out about different medical aid options.  Momentum Medical Scheme focuses more than ever on keeping benefit design stable and ensuring that their members continue to enjoy comprehensive and affordable benefits. The 3rd largest open medical aid scheme in South Africa, Momentum Medical Scheme has announced an average annual contribution increase of 3.9% for 2021. This is substantially lower that the weighted average annual contribution increase of 8.2% for 2020.

If you have any queries or are interested in joining Momentum Medical Scheme, please contact us on 011-658-1333, 076-200-5488 or email service@daberistic.com.  Author: Marizka Esterhuizen, Insurance Broker The main function of insurance is to put the insured into the same position as they were before a loss or accident. Santam states on their website that: “The retail value of a car (which is usually the higher value of the two) is the average price a car dealer would sell it for. In insurance terms, this means that if your car is covered for its retail value and it is written off in an accident or stolen without being recovered, the settlement amount will be based on the car’s retail value. If your car is insured for its retail value, it will be much easier to replace a damaged or stolen car with a similar make and model. The market value of a car is almost always lower than the retail value and takes into account a number of variables, including mileage, vehicle condition, service history and accident reports. If you were to sell your car privately, the market value would be the price that you could likely sell it for. Because this figure can vary from car to car, short-term insurers need to find a way to standardise the market value. The reasonable market value uses the retail value as the base and takes into account the amount of kilometres on your car’s odometer, the condition of the car as well as any extra items added to the car.” Therefore, if you insure your vehicle at market value you will not be able to replace the vehicle with a similar vehicle, leaving you in a worse position than before the loss or accident. You can use the calculator on Santam’s website to calculate the retail value of your vehicle by using the Auto Dealer Code, or your vehicles exact specifications, e.g. year, make, module etc. The Auto Dealer code was developed by TransUnion to specify vehicles. TransUnion has been gathering data over five decades and updates their data monthly to ensure that they provide accurate information in their guides. These guides are used by insurance, financing, and motor trader companies. “Can you please also explain why the Honda Jazz is insured for a less value, but the monthly insurance is higher than the Jeep Compass?”Insurance companies uses various factor that impact the rate at which the insurance premiums are calculated. These factors include, but are not limited to, the regular driver, vehicle specifications and the claims history.

Insurance premium rates are calculated by actuaries every year using data collected over the previous years. With today’s technologies and the vast well of data available, insurance companies have moved over to a client specific risk-based approach. Meaning that insurance rates are calculated per individual with vehicle insurance, insurance companies look at the regular driver, taking into account the following factors: • Age • Marital status • Gender • Occupation The vehicles specifications also play a role in calculation the rate. For example, older vehicles have been on the road longer and are therefore more prone to breakdowns, the parts are harder to find and therefore more expensive even if their retail value is lower than other vehicles. Hijacking statistics are also used, as a result vehicle like VW Polo’s that are more likely to be hijacked, have higher insurance rates. Insurance companies look at the following factors: • Year the vehicle was manufactured • Vehicle module • Vehicle make • The colour of the vehicle • Extras on the vehicle • Vehicle security • Where the vehicle is parked in the day and at night The claims history of the driver is used in calculating the rate for the premium, a higher loss ratio will result in a higher premium. • Your loss ratio, which is the losses an insurer incurs due to paid claims as a percentage of premiums earned. • Your loss ratio is calculated by dividing the claim amount by the annual premium. In conclusion, there are various factors that can result in the premium for the Honda Jazz being higher than the Jeep. To get help and advice on your car insurance, please contact 011-658-1333, Option 3, email service@daberistic.com to speak to one of our insurance brokers.  Bonitas, the second-largest open medical scheme in South Africa, has recently released their 2021 updates and increment across all plans. Bonitas recognises that it has been a tough year. It has settled on lowest increase possible to maintain consistent service to the clients for 2021. With the guideline from the Council for Medical Schemes, Bonitas has settled on an average increase of 4.6% across all plans which will range between 0% and 7.1%. The BonFit Select plan has 0% increase. It is to ensure affordability and sustainability for all the members going forth as Bonitas has noted that 7 of its current options are priced between R1500 and R3000 per month, which is where the medical scheme market is experiencing growth currently. "Member behaviour has changed significantly, and demand is for innovation, accessibility and technology. This has the benefit of attracting, a younger, target audience and driving sustainability,” it said.  Bonitas has introduced 2 new medical aid plans for 2021, these plans are induced by technology, called Edge.

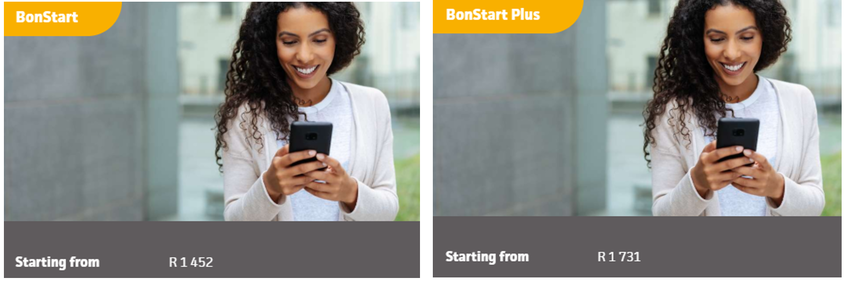

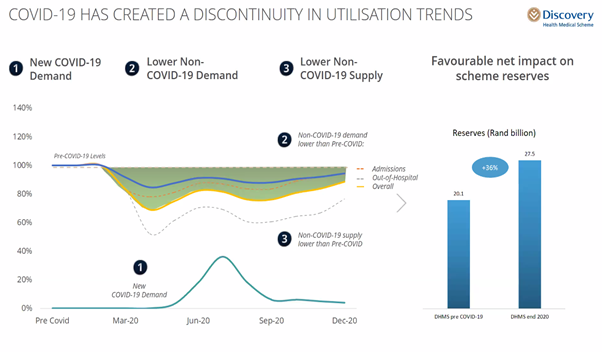

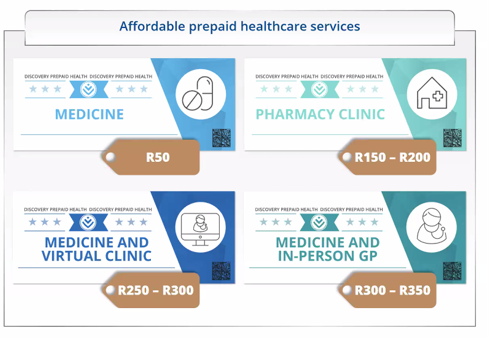

BonStart and Bonstart Plus, are designed for economically active singles or couples, living in the larger metros, which include access to: • Private hospital network and full cover for emergencies • PMB chronic medicine • Day to day benefits including unlimited GP consultations • Layers of virtual care, dental and optical benefits; preventative care • Wellness screenings • Contraceptives and so much more… The above monthly premium is R1452 and R1731 for principal member respectively. This year has been a challenging year for most due to global pandemic hence personal assurance on safety is where Bonitas will develop and focus their core services like home-based care and day hospitals to reduce risks. Other developments for 2021 include: • Developing its WhatsApp channel and virtual technology platforms • Continuing with the virtual care platform, which provides access to GP consultations and free delivery of chronic medicine • Promoting mental health and mental wellbeing, with screening via the app and providing effective care where necessary • Using the Wellness Extender benefit to pay for up to three months of subscription fees for Run/Walk for life to help members get healthier. To speak to a Medical Aid Consultant, please email service@daberistic.com, Tel 011-658-1333, Option 2 for Medical Aid.  On 30 September 2020, Discovery hosted its first ever virtual workshop with over 10,000 brokers, to announce Discovery Health's benefits and contribution update for 2021. Discovery reiterates that its core purpose is to make people healthier and enhance and protect their lives. 2020 has been a very challenging year from the healthcare perspective. According to Discovery Health's statistics, during the lockdown period over the last few months, the number of elective surgeries has drastically reduced as members chose to delay these treatments and avoid going to the hospital. The COVID pandemic meant most of the healthcare resources were directed towards the testing and treating COVID patients. No increase in contributions up until 30 June 2021Discovery Health understands that everyone has gone through financial strain during the lockdown, so we are excited to announce that Discovery has decided to freeze all scheme contribution increase across all plans for the first 6 months of 2021. However, this alleviation is not long term, thus the contribution increase will be announced during the second quarter of the year and implemented on 1 July 2021. The expected increase will be CPI + 2%, capped at 5.9%. Doing so, they are looking to assist members in affordability, sustainability and spreading the financial impact everyone has gone through during 2020. Based on its data analysis and observations during the pandemic, four trends have emerged: Utilisaiton discontinuity - how the COVID pandemic has disrupted the normal medical utilisation pattern. Technology - the pandemic has pushed the use of technology to the fore, to enable digital healthcare services from the comfort of one's home. Quality care Access - recognising that millions of South Africans don't have medical aid, Discovery announces a solution to make healthcare affordable and accessible to all. We use a few infographics to illustrate these trends:  Discovery Health's experience shows the COVID pandemic peaked around June to August. What has helped the scheme was from late March to now the number of non-COVID hospital admissions have reduced by 20% to 30% compared to last year.  Discovery Health has always been innovative and progressive with technology. Since the lockdown began, virtual consultations have increased by 8-fold. Discovery Health now introduces Connected Care, where it enables a range of appropriate home-based healthcare services for all levels of care. The picture above shows the TytoHome diagnostic device Discovery is bringing into the country and offering its members.  Discovery's research shows 50% of South Africans are on "pre-paid" healthcare. They have launched Prepaid Health to cater for all South Africans. This new offering launching at the end of December 2020 is one of the exciting products where good healthcare is available to anyone on a pay-as-your-go basis. Discovery leverages on its network, so you have access to good healthcare at a discounted rate. For members on hospital plans only, they can also purchase these vouchers for their day-to-day benefits. Discovery Health Plan Guides 2021Below are the Discovery Health Plan Guide brochures for 2021 (note these are still subject to approval by the Council for Medical Schemes): Next: Other highlights in Discovery Health Product Update 2021

|

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|