A minor can in fact be registered as a taxpayer in South Africa. This is in terms of section 67(1) of the Income Tax Act that "every person who at any time becomes liable for any normal tax or who becomes liable to submit any return contemplated in section 66 must apply to the Commissioner to be registered as a taxpayer in accordance with Chapter 3 of the Tax Administration Act.” If the minor therefore becomes liable to submit a return or becomes liable for any normal tax, the minor must be registered as a taxpayer.

Section 68. Income and capital gain of married persons and minor children.—(1) Any-- (a) income received by or accrued to or in favour of any person married in or out of community of property which in terms of section 7 (2) is deemed to be income received by or accrued to such person’s spouse; or (b) capital gain which is in terms of paragraph 68 of the Eighth Schedule taken into account in the determination of the aggregate capital gain or aggregate capital loss of such person’s spouse, shall be included by such spouse in returns of income required to be rendered by that spouse under this Act. (2) In the event of the death of any person during any year in respect of which such income is chargeable or in which such capital gain is taken into account, the income or capital gain of such person’s spouse for the period elapsing between the date of such death and the last day of the year of assessment shall be returned as the separate income of such spouse. (3) (a) Every parent shall be required to include in his return-- (i) any income received by or accrued to or in favour of any of that parent’s minor children either directly or indirectly from that parent; or (ii) any capital gain or capital loss in respect of any transaction entered into directly or indirectly by that parent, which is taken into account in the determination of the aggregate capital gain or aggregate capital loss of any of that parent’s minor children, together with such particulars as may be required by the Commissioner. (b) Every parent shall be required to include in that parent’s return any income deemed to be that parent’s income in terms of subsection (3) or (4) of section 7 or any capital gain deemed to be that parent’s capital gain in terms of paragraph 69 of the Eighth Schedule. Income of Minor children A taxpayer is liable for the payment of tax on any income which has been received by or accrued to or in favour of any minor children if such income arises from a donation, settlement, or other disposition by – (i) the taxpayer; or (ii) any other person, if the taxpayer made a donation, settlement or gave some consideration directly or indirectly in favour of the other person or his family. A minor child will, however, be liable for tax on income which is received or accrues to him/her independently of him/herself; in his own right, for example, bona fide salary and investment income derived from his/her own funds i.e. from money inherited by him/her or received as a gift from any person other than the person mentioned in (i) and (ii) above or from any other source. Should a minor child’s taxable income be sufficient to render him/her liable for tax, the taxpayer, as the legal guardian, must register him/her for income tax purposes and obtain and submit a return on his/her behalf. All investment income received by or accrued to a taxpayer or his/her minor children must be declared (including investment income which has not been paid but has been utilised, accumulated or re-invested for the taxpayer or his/her minor children’s benefit). Where interest is claimed as a deduction against investment income received, full particulars (i.e. amounts invested/borrowed, interest rates, date of each loan and investment) must retained for a period of five years after submission of the return. Courtesy of: Fedgroup

0 Comments

[The tax e-filing season is upon us. If you need a tax consultant to help you with your e-filing, please contact Daberistic Accountants at 011-658-1333, email tax@daberistic.com.]

During a media briefing in Pretoria on Tuesday, new SARS Commissioner Edward Kieswetter told the South African public that the tax threshold for those who have to submit returns will be increased this season. Kieswetter’s announcement was initially delayed due to a massive power outage across the city. However, when the lights returned, the new tax chief dished out some encouraging news for those earning a low-to-mid range income. SARS tax threshold: Am I exempt from filing a tax return? Instead of requiring tax returns from everyone who earns R350 000 a year, that minimum figure has been increased to R500 000 a year. In monthly terms, the parameters have shifted from R29 166 to R41 666. However, it’s not all plain sailing for those of us making less than half-a-million per annum. The new threshold laws only apply to citizens if they meet the following set of criteria:

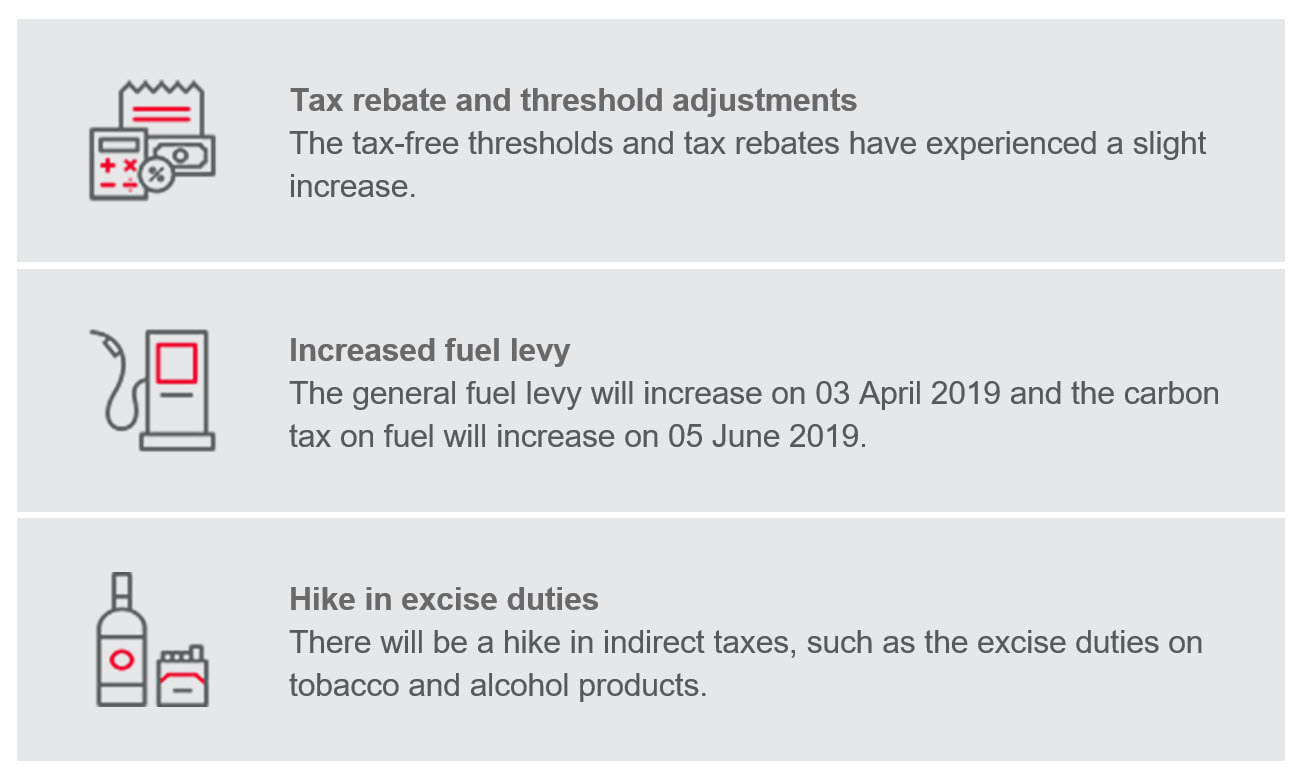

When is tax season in South Africa for 2019? Kieswetter was also keen to encourage more citizens to start using SARS’ e-filing systems. He revealed to tax-paying South Africans that the programme has gone through several updates, and more improvements will be in place by August. One of the incentives for using the e-filing systems is that they help with time management. Yes, tax season will start on 1 August and end on 31 October, but electronic applications start at the beginning of July and remain open all the way through until the last day of January 2020. It’s also worth noting that returns filed via SARS’ app have a deadline of 4 December 2019. Depending on what you’re earning and the new tax threshold, this could be a trouble-free season for many of SA’s workers. Source: thesouthafrican Allan Gray has provided an excellent summary of the 2019 budget speech. We would like to share with you here: What were the key changes?  SARS would to remind taxpayers of their obligation to submit outstanding tax returns.

Taxpayers who do not submit their returns are charged a penalty, which can range from R250 to R16 000 per month, depending on the taxable income of the taxpayer. It is a criminal offence not to submit a return, and continuous non-compliance will lead to criminal prosecution. SARS’ responsibility is to collect tax and customs duties on behalf of the country, and is committed to ensuring that each and every taxpayer pays their fair share towards the growth of our country. The Revenue Authority will be taking a tougher stance on those who do not submit their returns and deliberately seek to avoid their tax obligations. If you have any queries on your personal or business tax, contact our Finance Department, email finance@daberistic.com, tel (011)658-1333 Source: SARS Kevin Lings is the Chief Economist of Stanlib. He is a well know economist in the financial services industry, has an approach that makes complicated economic matters easy to understand. Attached is his presentation on the economic outlook of South Africa.

Click here to download presentation Source : Stanlib The SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2017/18.

Click here to download For any of your Tax or Vat queries please contact Su-Chin or Su-Lan, email finance@daberistic.com, tel 011 658 1333 . Source: SARS  Discovery Vitality encouraged by the revised sugar tax design announced by Finance Minister Pravin Gordhan in his 2017 Budget Speech. In response to the proposed sugar tax, Dr Craig Nossel, Head of Vitality Wellness said: “We believe that action is required to reduce the intake of sugary drinks, and support the proposed sugar tax. From a health point of view, it is excellent news that sugar content will remain the base on which the tax is applied – this encourages reformulation and the availability of drinks with a lower sugar content. We are also pleased to hear that some of the revenue generated from the proposed tax will be used to support health-promotion programmes aimed at non-communicable diseases. We have much to do as South Africans to combat the increasing prevalence of obesity in our country, and the sugar tax is a step in the right direction.” There are a number of reasons Discovery Vitality supports the Government’s proposed introduction of a sugar tax. In South Africa, obesity is ranked as one of the top five risk factors for early death, and years lived with disabilities[i]. Excess sugar consumption is clearly linked to obesity[ii], which is the number one risk factor for chronic diseases of lifestyle, also known as non-communicable diseases (NCDs), like diabetes and heart disease. It is estimated that NCD-related deaths globally will outnumber deaths from communicable, maternal, and perinatal deaths by 2030. South Africans are among the top 10 consumers of sugary drinks in the world[iii]. Studies also show that we continue to increase our consumption of sugary drinks: A study on Food consumption changes in South Africa since 1994’[iv] shows that the total intake of sugary drinks – carbonated and fruit juice – increased by 68.9% between 1999 and 2012. Research shows that drinking too many sugary beverages leads to an increased risk for obesity, particularly concerning for children and adolescents. This is because sugary drinks are a significant source of added sugar but do not make you full. Generally, people do not eat less to compensate for the extra calories they drink[v]. Obesity is rising Between 1980 and 2008, the prevalence of obesity worldwide doubled. With almost 40% of women and 11% of men classified as obese[vi], South Africa has the highest obesity rate in Sub-Saharan Africa. Rising obesity rates, which evidence demonstrates is the key cause of the pandemic of NCDs, are mainly caused by changes in our diet, work and leisure time. Specific drivers include energy-dense, nutrient-poor diets, physical inactivity, large portion sizes and irresponsible food advertising. Obese individuals incur 30% higher medical costs than their counterparts with a healthy weight Research published in the South African Medical Journal on the relationship between levels of obesity and medical expenses[vii] among South Africans on a medical scheme show that obesity is strongly associated with significantly increased healthcare expenditure. Severe obesity, this study indicated, increased healthcare expenditure by R4 425 for each person, split between inpatient and outpatient care. Recent Discovery Vitality research gathered from HealthyFood Benefit data, which specifically looked at the impact of sugar purchasing (specifically from sugary drinks) on healthcare costs, supports the findings of the medical scheme study. The analysis showed that an increase in sugar purchasing (from sugary drinks) was associated with a 4.1% increase in healthcare costs over a 3-year period from 2014 to 2016. The research also showed that members who started off consuming a greater amount of sugar had healthcare costs that were 2.9% higher than for the rest of the members by the end of the period. Cooperative efforts are needed to ensure policy changes are effective A multi-pronged approach is required to achieve a change in population behaviour and health. Discovery Vitality has gathered a significant amount of scientific and anecdotal evidence over the last twenty years, which points to the successful application of behavioural economics, and the power of education and wellness intervention programmes. The HealthyFood Benefit, which offers members up to 25% cash back on a range of healthy foods (specifically selected to address high risk dietary practices that are associated with NCDs including diabetes, high blood pressure and high cholesterol), is one such example. Over time, Discovery Vitality has found that incentivising members to make healthier choices positively influences their purchasing behaviour; an increase in the purchasing of fruit, vegetables, and whole-grain foods, and a reduction in the purchasing of high-sugar, high-salt, processed, and fried foods[ Apply for your Vitality or the Healthy food benefit on Vitality contact Namhla in our Health, email health@daberistic.com, tel (011)658-1333 Source: Discovery |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|