Last Month we shared our pocket guide to money. This month let's focus on Step 1 - Make as much money as you can. For most people, most of our money or wealth comes from our ability to work, to earn an income. Most of us were not born into a rich family. Many in South Africa were born into abject poverty. We had to learn, acquire skills, find a job or start a business, to provide for ourselves and our family. It is therefore important to improve your education, knowledge and skills, to network with the right people, to enhance your employability, or be equipped to have your own business. 1. Formal education This is the official way of certifying that you have a certain level of education. While a matric certificate is probably the minimum requirement when looking for employment, many young people study further, to get a degree, honours, or even masters and doctorate, to gain in-depth knowledge in certain discipline, to increase his job and income prospects. An example is a medical doctor. A student will need to complete a 5 year Bachelor's degree in Medicine and Surgery. he then works 2 years as a Clinical Intern. Then he becomes a Medical Doctor. A Medical Doctor has an income of R50,000 to R110,000 per month. If he studies further for 5 years to become a specialist, he can expect to have an income of R100,000 to R300,000 per month. So by studying further, a medical doctor increases his income potential. What you study is important. You will want to study something that you enjoy, that has applications in real-life work. 2. Study to become a skilled tradesman This is so underrated, but skilled tradesman like plumbers, electricians, handyman, carpenters, builders are in demand and earn a good income. If you don't like studying but like doing things with your hands, this may be the job for you! 3. Learn something new and useful YouTube is arguably the undisputed largest video library in the world. 1.3 billion people use YouTube. 300 hours of video are uploaded to YouTube every minute! Almost 5 billion videos are watched on YouTube every single day. Instead of just watching fun, entertainment, sports and gaming videos, choose a topic you want to learn and watch videos on that topic. Over the last 12 months I have watched videos on cooking (and that helped me make delicious bolognese and chicken biryani); technology and financial planner coaching (and that helped me transform my business to be remote working ready); chess (thanks to Agadmator channel, I have improved my chess game); news (in English and in Mandarin, to understand how the world is evolving); investing and book summaries. Recently I have decided to become a YouTuber, so I have been watching tons of videos on how to develop a YouTube channel and contents, and video editing. There is so much to learn out there, but focus on one thing at a time. Watch videos that are related to your work or business. I highly recommend anyone watching lots of YouTube to subscribe to YouTube Premium. It costs R71.99 per month, and the family plan costs R109.99 per month. It gives you ad-free viewing. Consider this as an investment in yourself and your family. Why try save the (little) cost and waste all the time watching/enduring the ads, not to mention the interruptions. 4. Start a business While starting a business is not for the faint-hearted, it can be rewarding. A successful business can meet a customers' need, create employment, contribute to the economy, and generate sustainable income to its owners.  When I was in my university years, I was already fascinated by the idea of starting my own business one day. In 1991 I bought my first book in this pursuit, Small Business Opportunities in South Africa by Ian Clark and Eric Louw. Over the years I bought or received many business books. Only in 2006 I stepped into starting my own business, a financial advisory business. I had a plan, I wanted to focus on investments only, but after I got into contact with my target market, I quickly realised I had to broaden my offering to one-stop shop, covering life insurance, medical aid, car insurance, business insurance and investments. 15 years later, in 2021, I have a viable financial advisory and insurance brokerage with a sustainable annuity income, providing income to 12 families. Along the way I have made mistakes, faced challenges and setbacks, had to learn quickly, continuously adapt to ever-changing regulatory and business environment. During this period we went through at least three global crises: The 1997 Asian financial crisis, 2008 Global Financial Crisis, and 2020 Coronavirus pandemic crisis. If you want to start a business, you need to do at least 4 things well:

5. Networking In business, it's about who you know. Whether you are a salaries employee or business owner, it is important to network with the right people, to learn, to exchange ideas and to get exposure. You should consider networking with:

I hope this gives you some ideas you can implement. What is the one thing you want to do? Write it down, stick on your wall, and do it. Next time, I will talk about "Do not spend more than you earn."

0 Comments

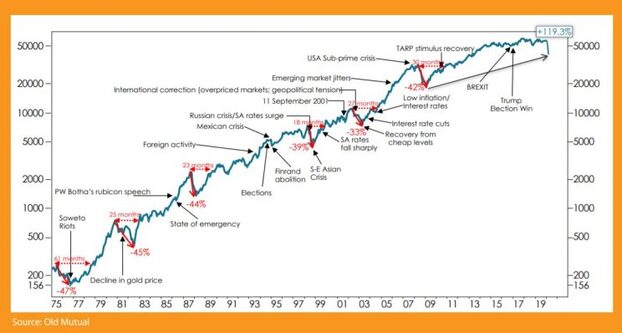

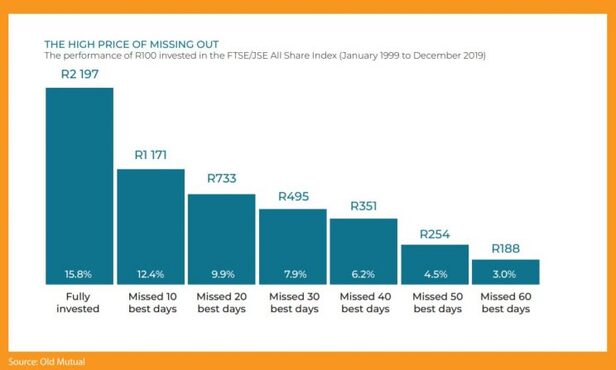

The Covid-19 global pandemic has caused ripples through global financial markets as the virus continues to spread across the globe and governments battle to find the right measures to contain it. We still do not know what the eventual impact will be, and how the pandemic will impact countries, markets and families. From a financial and investment perspective, we can stand back from the current crisis and reflect on the anatomy of a crash and how markets behave during and subsequent to a crash. We should expect a market crash every six years. A market crash or bear market is defined as a market correction where the market falls by more than 20% from its previous high. Looking at the biggest stock market in the world, the US, the S&P 500 (the broad measure of the US market) has experienced 16 bear markets since 1926, averaging one bear market or correction every six years. The average of these market losses has been an eye opening 39%!  From the above, it is clear that South Africa is part of the global village and we are exposed to global market shocks. Except for the Soweto riots, it has taken between 18 and 30 months for the market to recover back to their previous highs following a shock. Lesson 1. Markets have historically recovered from a crash Markets are erratic It is impossible to predict market returns, specifically during a crash when markets are reacting emotionally and erratically. This is clear in looking at share prices during the last week and by merely looking at the headline of one share, Sasol. • March 12: Sasol loses another 40% of its value in an hour • March 13: Sasol surges 45% after announcing sale of stocks and assets The above is an example of how erratic the market can behave during a stock market crash, thus in a few days you could have lost 40% or made 45%. If we stand back from a specific share, and look at the market as a whole, the US sub prime crisis (also know as the financial crisis) resulted in the JSE correcting by 42%. In 2008 alone, the South African market fell by just over 30%. Even though it was impossible at the time to determine when the market would recover, the crash of 2007/2008 was followed by exceptional returns in 2009 with the market recovering by more than 20%, followed by double digit returns in; 2010, 2012 and 2013. Investors where thus rewarded for staying the course, as per their financial plan and objectives. The extreme volatility is also evident in returns the last week, amidst the Covid-19 pandemic: • March 11:US (S&P) selloff approaches 20%, what next? • March 13: US market scores biggest gain since 2008, S&P 500 jumps by 9.28% It is important to remember that in disinvesting from the market, there are two decisions to get right; the right time to disinvest and the right time to reinvest in the market. Thus, investors must get both the exit and entry prices correct which is extremely difficult. The probability of timing the markets is summarised in a research study conducted by Vanguard (one of the world’s largest asset managers): “The biggest takeaway from our analysis is that the probability of being lucky and outperforming the benchmark is already less than 50% when taking just a few days out of the market. This probability then decays rapidly as the number of days out of the market increases. Unless an investor has great skill and/or luck and the conviction to act on these insights, the most effective approach is to remain invested.” The risks in attempting to time the market are further illustrated by the research conducted by Old Mutual Investment Group.  Lesson 2. Markets can be crazy during a crash and are impossible to time. Stay invested. Your portfolio should reflect your financial personality. It is often said that diversification is the only free lunch in investments. The principle behind diversification is investing in several different asset classes or investment types i.e. South African: equities, fixed interest and property and international: equities, fixed interest and property. The spread of investment risk (diversification), reduces the exposure to any one asset class significantly underperforming. Diversifying into international assets acts as a handbrake during global market uncertainty or market corrections. As investors withdraw from emerging markets (which are perceived as risky) and invest into developed market bonds (which are a safe haven in times of uncertainty) emerging market currencies depreciate. In such a scenario the offshore exposure in an investor’s portfolio benefits from rand depreciation, even though the underlying asset prices may be falling. The below illustrates the benefits of diversification by investing in a balanced portfolio during the financial crisis in 2008:  Balanced low equity funds represent a portfolio for conservative investors where the equity exposure is limited to 40%, the equity exposure can go up to 75% in the balanced high equity funds, which is more suited for moderate or growth investors. In both the aforementioned funds, the offshore equity exposure may be up to 30%.

The above analysis illustrates a few important investment principles, that will apply in most market corrections or crashes: • Markets recover after sharp losses or bear markets • Balanced funds provide investors with protection against market corrections. • Balanced low equity funds provide significant protection during periods of uncertainty. They do however significantly lag during the “recovery phase”. Investors often switch to low equity balanced funds during times of uncertainty, this can result in them missing the market recovery and only switching back to higher risk balanced funds subsequent to the market recovery. Timing is a mugs game, investors need to stay true to their specific risk profile and appetite; through both bull and bear markets. Lesson 3. Diversification is the only free lunch and protects investors during a crash Your money personality (risk profile) should not change during a crash. Guaranteed annuities (pensions) provide a sense of comfort during bear markets. During recent years we have seen an increase in the interest in traditional or guaranteed life annuities. Guaranteed life annuities are provided by insurance companies including Old Mutual, Sanlam, Discovery, Liberty and Just SA who guarantee an income for life. There is a wide variety of guaranteed annuities, with the most popular being inflation linked and with profit annuities. Investors’ pensions payments are protected through very strict governances and regulation requiring that insurers hold sufficient capital to back their liabilities i.e. pensions owed to investors. These capital adequacy ratios require that insurers hold enough capital to make provision for market shocks or corrections. Thus a “normal” market correction should have very little impact on insurers’ ability to continue paying pensions. Investors invested in life annuities that provide inflation-linked increases have little reason for concern as their future increases remain linked to inflation. The annual increase of with-profit annuities is linked to the performance of the markets and, depending on the insurer, is linked to market returns over i.e. a five to six-year period. It remains difficult to determine the impact of the current market turmoil on investors invested in with-profit annuities. Should the turmoil continue, and markets not recover, they may be faced with zero increases. For many retirees, with-profit annuities provide an effective annuity or pension strategy, if used appropriately with other annuities or the provision of an emergency fund. The benefit of with-profit annuities is higher pension over time. Globally the flight to safety has had a negative impact on retirees wanting to invest into life annuities. Annuity rates largely depend on bond yields. Global bond yields (which were already low) have fallen even lower as investors pile into bonds which are perceived as a safe haven investment. This has resulted in a decrease in annuity/pensions for retirees in many developed markets. We have not yet seen the same impact in South Africa, with long bond yields remaining relatively stable, thus the SA life annuity yields (starting pension) have remained relatively stable during the last two months. Lesson 4. Traditional life annuities or hybrid annuities provide some comfort during a market crash What should investors do? It is almost impossible to predict how the markets will react or recover during this pandemic. The following are a few principles that investors can follow during this time: Stick to your plan Your financial plan should be developed to consider your personal objectives and your risk profile. It is important to review your plan to ensure this still aligns to your objectives. However, be wary of changing your “money personality” due to the noise and the crisis, your risk profile should remain intact during both bull and bear markets. Let the professional money managers do their job A diversified investment portfolio should include several investment managers and investment mandates aligned to your risk profile. The investment managers will align the underlying portfolio to the current market conditions and increase or decrease the equity exposure within the parameters of the mandates to mange your portfolio and risk on your behalf. Now is the time to be frugal If you have not made provision for an emergency fund, now is the time to be cautious, save on luxuries and where possible build up a buffer or emergency fund. Given the continued uncertainty it is important to diligently manage expenses and increase the allocation to your emergency fund. It is now more prudent to be conservative with your finances than to overextend during these times of uncertainty. The Covid-19 market crash is a shock, and we are all concerned about how this virus will be contained. From a financial perspective, it is important to remind ourselves that this is not the first crash we have seen, and certainly won’t be the last crash that most investors will experience. A well-structured financial plan, implemented through a diversified portfolio, will assist in delivering on investors long-term objectives through difficult markets. Wrritten by Wynand Gouws Source: Moneyweb  Firstly, let me dedicate this report to my Lord and Saviour Jesus Christ, may honour and glory be to Him forever and ever! As a Financial Advisor with actuarial qualifications, I am particularly fascinated by investments. I have spent lots of time over the last 21 years studying the subject of investment. I have learnt and analysed all kinds of financial instruments, including shares, unit trusts, CFDs, futures, warrants and ETFs. Over the years the investment markets have taught me a lot of things. It has taught me to be humble. It has taught me to be a ready student, to continue to learn, think and reflect. In the past I have written about share analysis, technical analysis, and general investment advice. This is the first time I write and share a comprehensive report on unit trusts. Over the years I have appreciated the way good unit trusts, or Collective Investment Schemes, has helped me and my clients grow my wealth. They have provided many investors an excellent way of investing in a diversified portfolio of assets, that over the long term have demonstrated significant real returns. This first comprehensive report on unit trusts focuses on high-growth unit trusts. I share this report with my fellow financial advisors in the hope of helping you help your clients make better, independent, informed investment decisions. If you like this report and think this report has helped you, please like it on LinkedIn and share it with financial advisors. Please also comment on this report, so that I can know whether I am on the right track, and how I can continue to refine my investment thinking. Click the link below to download the report.

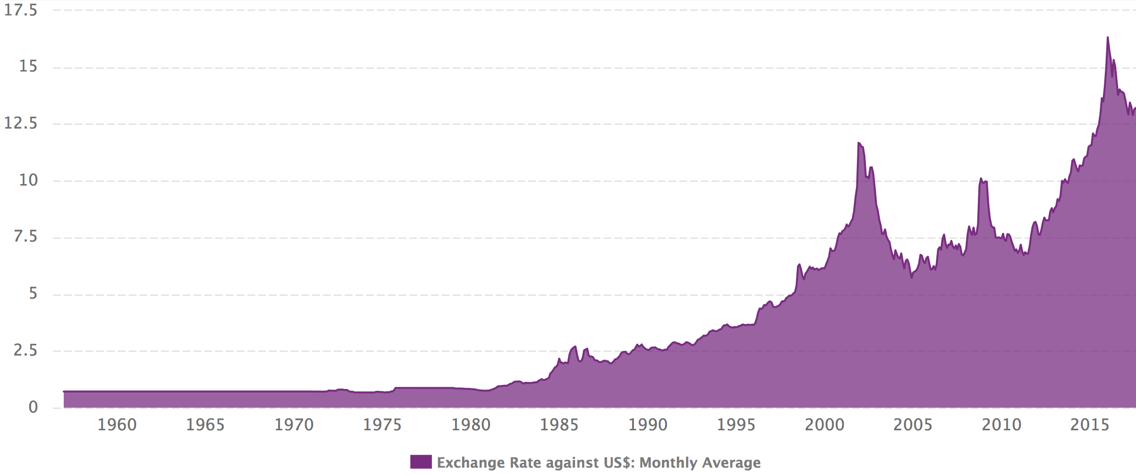

Investors can buy and sell currencies to profit from the changes in exchange rates. The most used currencies for forex trading are US Dollars (USD), Euro (EUR), British Pound (GBP), Japanese Yen, Swiss Franc and Canadian Dollar. Investors can get exposure to foreign currencies using currency funds (unit trusts), reputable online forex dealers, or foreign currency accounts offered by local banks. In South Africa we can consider forex as a viable investment option. This is because the Rand will depreciate against the US Dollar over the long term, based on the relative purchasing power parity theory. The theory says that the Rand should depreciate against the US Dollar in line with the differential in the two countries’ inflation rates. The USD to ZAR exchange rate was R3.40 in 1994. Currently the exchange rate is R13.00 as of September 2017. This means over the last 23 or so years the Rand depreciates against the US Dollar at a rate of 5.8% per annum. Holding US Dollars will protect you against Rand depreciation over the long term.  Holding US Dollars has an opportunity cost, as you will lose out on the higher interest you would otherwise earn in a bank deposit in South Africa. Investing in a bank deposit would give you an interest rate of 7%, whereas a USD account may only give you an interest rate of 1%. The opportunity cost is a loss of 6% in interest per annum.

Who is it suitable for:

A word of advice: If you would like to invest offshore over the long term, rather invest in offshore equity unit trusts than foreign currencies. It will reward you much more handsomely over the long term.  An endowment is a type of investment plan that can hold a variety of underlying investment options, including unit trusts and a share portfolio. It requires an investor to invest for a minimum period of five years. It provides investors with full access to their money after five years or when the policyholder dies. In South Africa, endowment plans are taxed at reduced rates (compared to the typical tax rate of an individual in the highest income tax brackets). When you do decide to withdraw your money, you won’t have to pay any further tax on your investment.

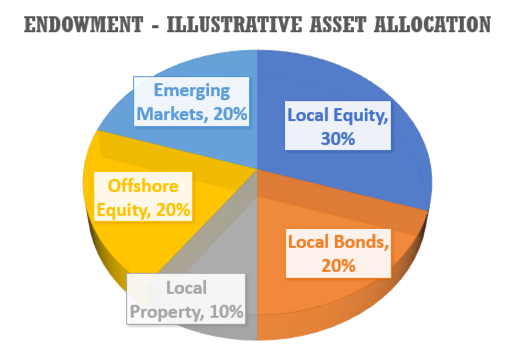

There are two main considerations around endowments: tax and estate planning benefits. Income received in an endowment is taxed at a flat rate of 30% for individuals and trusts, while capital gains is taxed at 12%. 20% dividend withholding tax also applies. Tax on returns is deducted and administered by the product provider. The Long-term Insurance Act that regulates endowments imposes a few restrictions: During the first five years of your investment, known as the restriction period, you may only make one withdrawal. The maximum withdrawal during this period is limited to the amount invested plus interest at 5%. The balance may be withdrawn after five years However, when you are not in a restriction period, you may withdraw from your investment at any time, or schedule regular withdrawals. Your five-year restriction period may be extended if you invest more over one year than 120% of your investments over either of the past two years. Most life insurance companies and investment platforms offer endowments. In the event of your death, your beneficiaries can receive your investment immediately and there are no executor's fees. This amounts to a saving of up to 3.99% of fund value. Tax administration is taken care of on your behalf (the insurance company calculates, deducts and pays the taxman). The entire value of the endowment will be protected against creditors after three years. This protection will continue until five years after the termination of the endowment. You are not restricted to maximum levels of equities and offshore investments, as in the case of retirement annuity. You can also use an endowment to draw income upon retirement, as long as the five-year restricted period has passed. You can do this on an ad-hoc basis, without being forced to draw income at specific intervals. Return profile: It will depend on the type of unit trust you invest in. If your underlying investments are income unit trusts, you may expect a net annualised return of 4% after fees and tax. If your underlying investments are high growth unit trusts, you may expect a net annualised return of 6.5% to 9% after fees and tax. Who is it suitable for:

Property investment is high on many investors’ list. Many investors like property as it consists of land and buildings, has physical presence. Property offers capital protection, its value increases over time.

Buying real estate is about more than just finding a place to call home. Investing in real estate has become increasingly popular and has become a common investment vehicle. Although the real estate market has plenty of opportunities for making big gains, buying and owning real estate can be a lot more complicated than investing in stocks and bonds. Owning your own home that you live in is not a property investment. Property investment is something that provides you with regular income over time. There are generally four ways of investing in property:

Ideally, the landlord charges enough rent to cover all of the aforementioned costs. A landlord may also charge more in order to produce a monthly profit, but the most common strategy is to be patient and only charge enough rent to cover expenses until the mortgage has been paid, at which time the majority of the rent becomes profit. The disadvantages of buy-to-let properties is firstly you need to manage tenants. You need to find a good tenant that will pay rent on time and look after your property. If you have a bad tenant that doesn’t pay or damage your property, it can be costly and stressful to the landlord. Worse still, there can be times when you end up having no tenant at all. Also you need to continuously maintain the property, fix things that are out of order, to maintain the use and value of the property. Lastly, property is not a liquid investment: you cannot sell property and get your money in a matter of days. Doing research and finding property in the right location are important in the success of buy-to-let properties. Also be aware of the costs associated with acquiring a property, such as Conveyancer’s Fee, Bond Registration Fee, Deeds Office Registry Fee and Transfer Duty. 2. Real estate trading Real estate traders buy properties with the intention of holding them for a short period of time, often no more than three to four months, whereupon they hope to sell them for a profit. This technique is also called flipping properties and is based on buying properties that are either significantly undervalued or are in a very hot market. Pure property flippers will not put any money into a house for improvements; the investment has to have the intrinsic value to turn a profit without alteration or they won't consider it. Flipping in this manner is a short-term cash investment. If a property flipper gets caught in a situation where he or she can't offload a property, it can be devastating because these investors generally don't keep enough ready cash to pay the mortgage on a property for the long term. This can lead to continued losses for a real estate trader who is unable to offload the property in a bad market. A second class of property flipper also exists. These investors make their money by buying reasonably priced properties and adding value by renovating them. This can be a longer-term investment depending on the extent of the improvements. The limiting feature of this investment is that it is time intensive and often only allows investors to take on one property at a time. 3. Real Estate Investment Trust (REIT) A Real Estate Investment Trust - REIT (pronounced ‘reet’) - is a company that owns, and often operates, income-producing property. The REIT is the international standard. More than 25 countries in the world use a similar REIT model like the US, Australia, Belgium, France, Hong Kong, Japan, Singapore and the UK. A South African REIT - SA REIT (pronounced 'essay reet') - is a listed property investment vehicle that is similar to internationally recognised REIT structures from around the world. Listed Company REITs or Trust REITs are publicly traded on the JSE REIT board and qualify for the REIT tax dispensation. A JSE-listed SA REIT must:

If you like property but do not like the hassles of managing properties, then property unit trusts are for you. Property unit trusts are unit trusts that invest in listed property stocks and REITs, which in turn invest in office, retail and industrial properties. Property unit trusts allow investors into non-residential investments such as malls or office buildings and are highly liquid. They offer investors instant diversification benefit, by investing in a number of property companies. Property unit trusts distribute the income it receives quarterly to investors. You can also benefit from capital growth through rising unit price over time. Over the last 20 years property unit trusts have given investors an annualised return of 20%, making it one of the best investment vehicles over the long term. 5. Leverage This is probably the biggest advantage of investing in properties. With the exception of REITs and property unit trusts, you can borrow money on your property. Banks are willing to give you a home loan, as they can secure their lending with the value of the property. Most mortgages require 10% to 30% deposit, however, depending on your financial standing and credit score, some home loan providers may give you up to 100% bond, meaning you don’t have to put down a deposit. This means that you can control the whole property and the equity it holds by only paying a fraction of the total value. Of course, your mortgage will eventually pay the total value of the house at the time you purchased it, but you control it the minute the property is transferred to your name. This is what emboldens real estate flippers and landlords alike. Whether they rent these out so that tenants pay the mortgage or they wait for an opportunity to sell for a profit, they control these assets, despite having only paid for a small part of the total value.  An ETF, or exchange-traded fund, is a marketable security that tracks an index, a commodity, bonds, or a basket of assets like an index fund. Unlike unit trusts, an ETF trades like a common stock on a stock exchange. ETFs experience price changes throughout the day as they are bought and sold. ETFs typically have higher daily liquidity and lower fees than unit trusts, making them an attractive alternative for individual investors.

Because it trades like a stock, an ETF does not have its net asset value (NAV) calculated once at the end of every day like a unit trust does. ETF investors are entitled to a proportion of the profits, such as earned interest or dividends paid, and they may get a residual value in case the fund is liquidated. The ownership of the fund can easily be bought, sold or transferred in much the same was as shares of stock, since ETF shares are traded on public stock exchanges. There are now over 5,000 ETFs worldwide. In South Africa there are 57 ETFs listed on the JSE. The ETFs available in South Africa can be classified into seven categories: South African Equity International Equity Bond Commodity Money Market Multi-Asset Class Property Equity You can buy ETFs listed on a stock exchange, such as JSE, through a reputable stockbroker or an ETF platform such as etfsa.co.za. Your return from owning ETFs comes from two sources: dividends or interest paid to you, and increase in share price (capital gains). Dividends received are subject to 20% Dividend Withholding Tax; capital gains are subject to Capital Gains Tax. ETF share price can go up or down. When share price goes up, you make a profit on paper. When share price goes down, you make a loss on paper. Before you invest in ETFs, you must do your research. You should identify the ETFs you would like to invest in, read the factsheets (Minimum Disclosure Documents), have a good understanding of their underlying assets, prospects and financials. After you have bought an ETF, you need to continue to monitor its performance, changes to underlying assets and future prospects, to determine whether it is appropriate to stay invested. Working with an advisor specialising in ETFs will add value to your ETF investing process. Having a good understanding of technical analysis may help buying ETFs at better prices. ETF investing is a long-term activity. It is NOT buying and selling ETF shares regularly in the hope of making quick profits. A word of advice: I consider the International Equity, Commodity and Property Equity ETFs to be the most interesting for investors to consider as part of their diversified portfolio. But remember, don’t base your investment decisions on looking at past performance figures only. You need to be forward looking, thinking about what is likely to do better going forward. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

||

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|