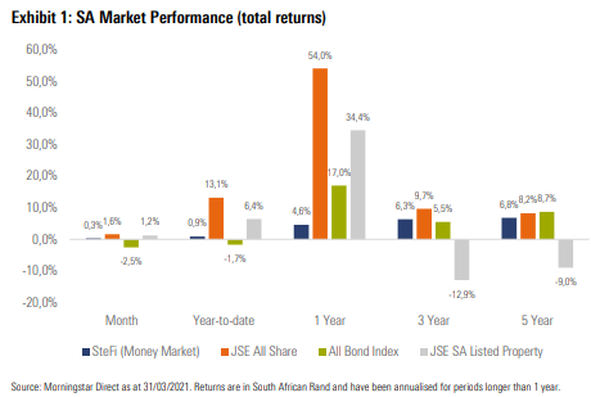

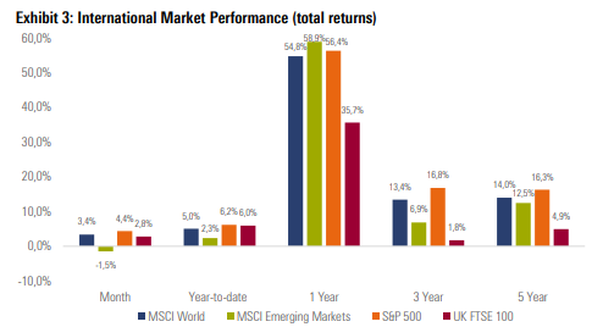

South African Market Update South African equities ended higher for a fifth consecutive month, with positive performance across all three major local equity sectors. Local bonds ended the month lower, despite positive news on lower-than-expected inflation, a reduction in government bond auctions, a lower-than-expected budget deficit and a stronger rand. The weak performance from bonds was largely driven by SA yields drifting higher (moving prices lower) in reaction to movements in global bond markets. Local listed property ended the month higher, however, weak performance from some of the larger counters including Growthpoint and Redefine led to muted returns from the SA Listed Property Index. The rand was stronger against most major developed market currencies, despite weakening significantly against the US dollar at the beginning of March, only to recover the lost ground towards the end of the month. South African Economic Update The South African Reserve Bank’s Monetary Policy Committee (MPC) announced during the month that it will leave the repo rate unchanged at 3.5%. This was the fourth consecutive meeting where the MPC decided to leave the rate unchanged, however, unlike recent meetings, the decision was unanimous, with all five members voting to keep rates on hold. Available data for Q1 2021 appears to indicate a slow start to the year for economic growth, which can largely be attributed to the introduction of adjusted level 3 lockdown restrictions during January in reaction to the second Covid-19 wave in the country. SA headline CPI moved lower to a year-on-year figure of 2.9% for February (from 3.2% in January). This was only the third time in over a decade that year-on-year inflation has fallen below the bottom end of the target band and was largely driven by the contribution of lower medical insurance costs.  Global Market and Economic Update Most major global equity markets ended the month with positive returns, as economic data reflecting the recovery from the Covid-19 pandemic continued to surprise on the upside. Equity investors continue to remain bullish, with another US stimulus package on the horizon, despite concerns around a ship stuck in the Suez Canal, which disrupted a major global shipping route for a few days during the month. March was dominated by market participants taking note of movements in global bond markets, as yields continued to move higher (moving prices lower), led by US Treasuries, as global bonds ended the quarter with their worst return in decades. The uptick in global bond yields appears to be connected to inflation expectations, with fixed income markets pricing in higher inflation in the medium term, which is likely to lead to interest rate increases from the US Federal Reserve (Fed). This, despite the Fed’s insistence that they will continue to keep monetary policy accommodative as the US economy continues its recovery from the shock of the Covid-19 pandemic.  Source: Morningstar

0 Comments

Leave a Reply. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|