|

For our investors investing in Morningstar Managed Portfolios, click below to access the latest performance snapshot, market commentary and market performance summary:

Morningstar SA Managed Portfolios Morningstar Global Managed Portfolios (USD) Market Commentary - SA and Global Market Performance Summary - SA and Global

0 Comments

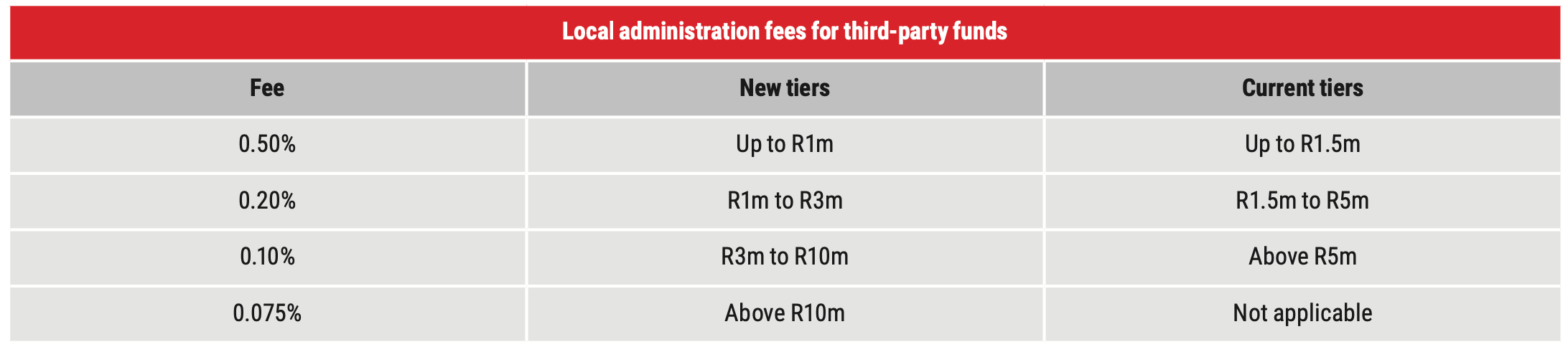

We are pleased to share that Allan Gray, one of the largest linked investment service providers (LISPs) in South Africa, has reduced its adminsitration fees. Allan Gray have reduced their local administration fees for third-party funds, effective 1 October 2022. In early 2023, they will combine a client’s local and offshore platform assets for the purposes of calculating their applicable administration fees on each platform, enabling clients to benefit from lower fees. In early 2023, they will introduce a step fee for new clients investing below their lump sum minimum of R50,000. Allan Gray reducing local administration fees for third-party funds Allan Gray's new fees, which are effective 1 October 2022, are outlined below.  The administration fee charged for local Allan Gray funds will remain unchanged at 0.20% per annum (excl. VAT).  Combining local and offshore platform assets to calculate administration fees (from 2023)

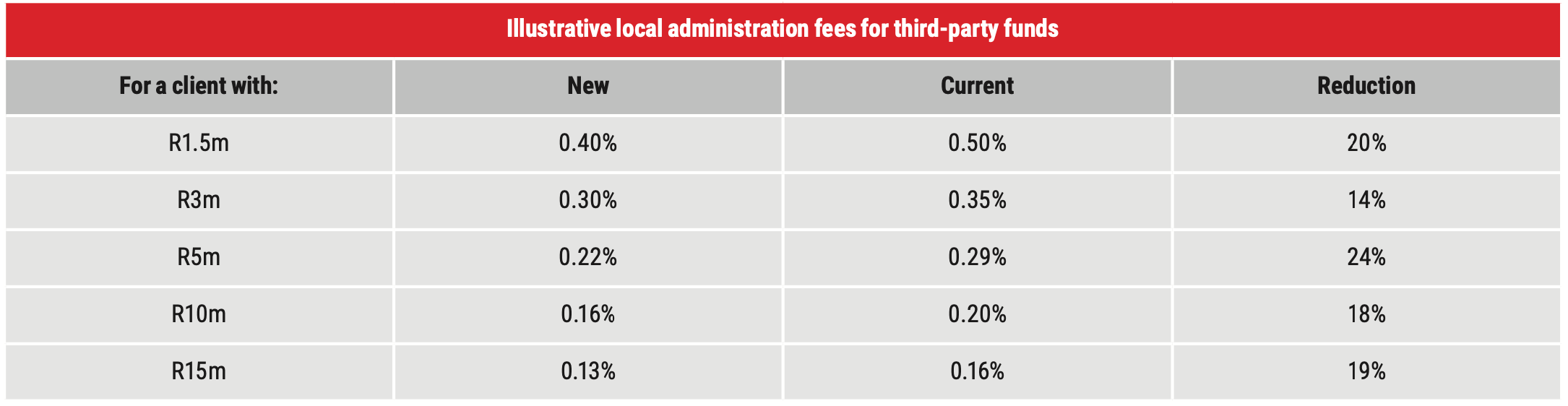

Allan Gray will combine your local and offshore platform assets when calculating your administration fees which will result in more of your assets being subject to the lower fee tiers. Currently, your local administration fees are based on the market value of all local platform assets linked to your investor number and applied to the local administration fee tiers. Your offshore administration fees are calculated separately based on the market value of all offshore platform assets linked to your investor number and applied to the offshore administration fee tiers. The effective date of this change will be communicated ahead of implementation in early 2023. What does this all mean for you as an investor? For clients with assets more than R1 million with Allan Gray, they will enjoy reduced administration fees, so they will keep more of the investment returns. We applaud Allan Gray for reducing costs of investing for clients. For clients with assets less than R1 million with Allan Gray, the 0.5% administration fee stays the same. For new clients with less than R50,000 invested, they will have to pay a step administration fee of 1.0% per annum (excl. VAT), until their investment value has reached R50,000. So Allan Gray is not so cost effective towards smaller investors. This cost is understandable, as there is a base cost of opening and maintaining an investor account. If you have any questions or feedback, email us at service@daberistic.com  Nowadays most medical schemes have a new-generation option that will typically be a hospital plan with a savings portion. This means the consumer has the peace of mind that he can go to a private hospital for procedures and has a small savings account for day-to-day expenses.

What is a medical savings account? The medical savings plan is designed to cover day-to-day expenses while having fewer restrictions on the choice of providers. The consumer gets a total annual amount that is available in advance in his Medical Aid Savings to account for medical expenses. If a consumer joins the medical scheme during the year, this amount will be calculated pro rata. In terms of legislation, this amount may not exceed 25% of his annual premium. Once the savings are exhausted, the consumer will be responsible for any further day-to-day expenses. Any positive balance in the savings account at the end of the year will be carried over to the next year. If the member exhausts his savings component before the end of the year and switches to a new scheme or resigns from the scheme, the scheme may expect the member to repay the difference in savings to the scheme. The amount repayable by the member is the monthly savings multiplied by the number of months left in the year. Here are seven tips to make your medical savings last longer: 1. KNOW YOUR PLAN Understand what you’re covered for, at what rates and with which providers. Does your plan cover you at the medical scheme rate or at a higher rate? Does your plan require you to make use of a hospital or pharmacy network? Refer to the material you receive from your medical scheme, use their website and talk to your financial adviser about what your options are. 2. KNOW YOUR DOCTOR’S RATES Patients are often embarrassed to discuss money with their healthcare provider, but when you make the appointment, ask what rates your doctor charges and whether you’ll be liable for any co-payments. That way, you can make informed decisions about how you’re spending your healthcare funds. If affordability is your greatest concern, it might be better to shop around for a provider who charges scheme rates, but if choice is more important to you and you’re happy to pay more, you’ll know upfront exactly how much. 3. TAP INTO NETWORKS YOUR SCHEME MAY HAVE Some medical schemes have network arrangements in place with healthcare professionals. By using a network, the scheme pays the professional directly, reducing administrative hassle and keeping costs down for you. The Discovery Health Medical Scheme, for example, has an extensive GP network where members are covered in full for doctors’ consultations. We recommend that our members call us or visit our website before they see a healthcare professional, so they know which of these are part of a network. 4. IF YOUR SCHEME OFFERS DIRECT PAYMENTS WITH CERTAIN SPECIALISTS, YOU CAN BENEFIT TOO For example, Discovery Health Medical Scheme has direct payment arrangements in place with most of South Africa’s specialists on most of its plans. If you see one of them, you won’t be liable for any co-payments. If you choose to see another specialist, you may need to pay upfront or pay a portion of the costs yourself – depending on your plan. Find out what your options are. Don’t be afraid to discuss and agreed rates with your specialist. 5. CHECK FOR FULL-COVER ALTERNATIVES In the case of medicine for a chronic illness, schemes often have formularies – lists of medicine that are covered in full by the scheme. Check with your doctor or pharmacist if your prescribed medicine is covered in full and ask about options if not. 6. PAY IN CASH FOR OVER-THE-COUNTER MEDICINES If you have a medical savings account, don’t claim for items not normally covered by medical schemes, for example, over-the-counter headache tablets, cough preparations, etc, from your savings. Paying cash will help the money in your savings account last longer, so you have funds available for more serious, more expensive out-of-hospital treatments. 7. STAY HEALTHY! It seems obvious, but people often overlook the fact that by taking care of their health, they can reduce their healthcare costs in the long term. Make use of your scheme’s preventive screening benefits for regular health checks and live a healthy life. In the case of Discovery Health Medical Scheme, members have access to a range of preventive screenings funded by the scheme. Members can join Vitality, which rewards them for being healthy. Please contact our Health Department, email health@daberistic.com , to find out about different Medical aid options Just as we thought Covid-19 was behind us, 2022 bombarded us with an array of new curve balls. From the war in Ukraine, inflation last seen in the 70s, rising interest rates and global markets experiencing drawdowns that rank as one of the worst on record, investors had very little (if any) place to hide. It almost feels like there’s a new headline about a new disaster happening somewhere around the world every day and quite frankly, it’s rather depressing. In the words of Peter Lynch, “You can’t see the future through a rearview mirror.” Imagine having to drive your car up a steep hill, with numerous bends and turns, not looking through your windshield and only being guided by the view in your rearview mirror – it’s a pretty terrifying thought. Given that we drive by looking out the windscreen and not by looking in the rearview mirror, I want to change how we are looking at this crisis. Allan Gray has informed us that, clients who are active users of secure Allan Gray Online (AGO) accounts will no longer receive the below documents via email. Instead, they will notify you when these documents become available online:

This is with the aim of improving the security of clients’ personal information. How clients can view and download these documents online Once you have logged in to your secure online account at www.allangray.co.za, you can navigate to the ‘Statements & documents’ tab, where you will then be able to select the relevant document you would like to view or download. If you have any questions or feedback, please contact us on 011-658-1333 or email us at service@daberistic.com  Load shedding, or power outages, has become a daily reality. South Africans' favourite app is EskomSePush (ESP) which is used to check the latest load shedding stage and load shedding schedules.

So how does a household cope with load shedding in South Africa? 1. Invest in Backup Power Solutions: Investing in a generator or solar backup power system can help provide electricity to your home during load shedding. Generators are the most common form of immediate power backups and can be set up fairly quickly and easily. Solar backup systems can provide the long-term reliability you need, while using renewable energy sources. 2. Use Power Saving Appliances and Devices: A lot of electricity can be saved by using energy efficient appliances and devices. Switching to LED light bulbs, automated power strips and smart outlets can help save energy and money in the long run. 3. Invest in Uninterruptible Power Supplies: Uninterruptible Power Supplies (UPS) are essential for essential household equipment such as computers, routers and telephones. They provide power for a limited period after a power cut so you can stay connected and work efficiently. 4. Insulating Your Home: Heat sensitive equipment such as freezers and fridges should be insulated with material such as bubble wrap to ensure their contents can remain cool during a power cut and reduce the amount of power required to restart them once the electricity returns. 5. Plan Ahead: Stocking up on essential food items, storing enough water, and setting up a makeshift ‘life support’ system with enough cell phone and laptop chargers, can help you cope with load shedding. Making sure you have all of the necessary items prepared and ready beforehand can really help. Welcome to 2023 – a new year and a blank slate of 12 months, 52 weeks, 365 days, 8760 hours and 525 600 minutes to make changes, take on new opportunities and set new goals. We all kick off a new year with certain resolutions in mind, such as eating healthy and exercising more. More often than not, it’s not just our dress or pants size that feels a bit tighter than before the holiday indulging, but also our purse strings. Too many people are left with more month than money after holiday spending, with January probably feeling the hardest. Whether or not you have an extra dime to spend at the end of a year, or perhaps at the start of this new one - by means of employee rewards (such as a bonus), or by not spending all you set aside for the holiday gifting season - why not use the start of the new year to get that savings mindset into gear. If you have overspent, drawing on the below tips in the new year is even more important. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|