|

The festive season is a time to switch off from work, recharge the batteries and spend quality time with friends and loved ones. It is also a time when many people throw caution to the wind, and sometimes, their budgets as well.

You can avoid a financial hangover in the new year by considering the following tips: Create a spending plan. Draw up a financial plan that accounts for your wants and needs between the end of November to January. As many people get paid early in December, the goal should be to stretch the November salary as far as possible into December, so as not to dip into their year-end paycheck too soon. Prioritise debt and savings. If you are fortunate enough to receive a bonus, maximise the windfall by allocating a portion to your savings and investment accounts. Provisions should also be made for paying off outstanding debt. Hide the credit card. If you are ill-disciplined, remove your credit cards from your wallets to avoid unnecessary and costly spending. Beware of festive season scams. Phishing attacks are prevalent at this time of the year. Be sure to examine emails and SMS messages very carefully, and be cautious of clicking on links. Always hover over links before clicking on them and take note of the URLS they direct you to.

0 Comments

Research indicates that women tend to dedicate more time to researching their investment options and are twice as likely as men to rely on financial advisers for guidance in their financial planning decisions. Numerous studies also suggest that women approach investing with a longer-term perspective and are more inclined to hold investments for extended periods rather than attempting to time the market. These characteristics can be leveraged to achieve financial independence and close the investment gap.

As we commemorate Women's Month, here are four tips to empower women to take control of their financial well-being: 1. Establish a budget and define financial goals. Avoid vague objectives and strive for specificity. For example, rather than setting a general goal like "save money for the future," define specific objectives such as "save R10,000 per month for retirement by contributing R5,000 to a retirement fund and R5,000 to a long-term investment portfolio." This level of specificity provides clarity and direction, making it easier for you to track your progress and stay committed to your financial goals. 2. Develop a comprehensive plan. This should encompass both a savings strategy (including an emergency fund) and an investment plan. 3. Automate the process. Set up debit orders for your investments and consider scheduling annual escalations in advance. This will help you invest more every year on autopilot. 4. Allow decisions time and space. Recognise your biases and external influences, and be thoughtful in your decision-making. Here are three common examples of biases: 1. Confirmation Bias: This is the tendency to search for, interpret, favour, and recall information in a way that confirms one's preexisting beliefs or hypotheses. For example, you might be more likely to remember and focus on information that supports your investment decisions while ignoring or downplaying contradictory information. 2. Overconfidence Bias: This bias involves overestimating one's own abilities, knowledge, or judgments. It can lead to taking excessive risks in investments or being overly confident in the success of certain strategies without considering potential downsides. 3. Loss Aversion Bias: Loss aversion refers to the tendency to strongly prefer avoiding losses over acquiring gains of the same or similar value. It can lead to overly conservative investment decisions, such as holding onto losing investments for too long in the hope that they will recover, rather than cutting losses and reallocating funds to more promising opportunities.

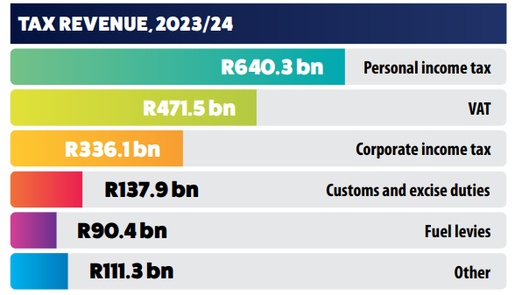

Where The Tax Comes From Highlights Of The BudgetSome of the things that stood out was incentivisation of rooftop solar, energy support packages as well as relief in terms of personal income tax. Energy support package

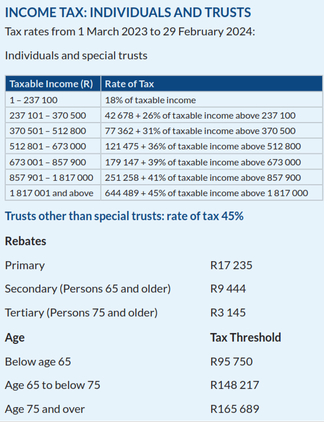

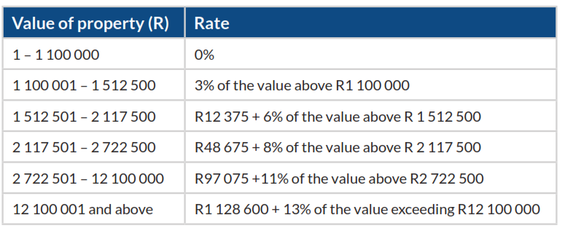

Income Tax - Individuals & Trusts Dividends: Dividends received by individuals from South African companies are generally exempt from income tax, but dividends tax, at a rate of 20%, is withheld by the entities paying the dividends to the individuals. Interest: A final tax at a rate of 15%, is imposed on interest from a South African source, payable to non-residents. Interest is exempt if payable by any sphere of the South African government, a bank, or if the debt is listed on a recognised exchange. Capital Gains Tax: Maximum effective rate of tax: Individuals and special trusts 18%, Companies 21.6%, Other trusts 36% Travelling allowance: Rates per kilometer, which may be used in determining the allowable deduction for business travel against an allowance or advance where actual costs are not claimed, are determined using the table published on the SARS Click here to view Transfer Duty: Transfer duty is payable at the following rates on transactions that are not subject to VAT: Acquisition of property by all persons:  Income Tax - Companies1. Small Business Corporations Taxable Income Rate of Tax 1 – 95 750 0% of taxable income 95 751 – 365 000 7% of taxable income above 95 750 365 001 – 550 000 18 848 + 21% of taxable income above 365 000 550 001 and above 57 698 + 27% of the amount above 550 000 2.Turnover for Tax For Micro Business Taxable turnover (R) Rate of tax (R) 1 – 335 000 0% of taxable turnover 335 001 – 500 000 1% of taxable turnover above 335 000 500 001 – 750 000 1 650 + 2% of taxable turnover above 500 000 750 001 and above 6 650 + 3% of taxable turnover above 750 000 Other Taxes, Duties and LeviesValue-added Tax (VAT): VAT is levied at the standard rate of 15% on the supply of goods and services by registered vendors. A vendor making taxable supplies of more than R1 million per annum must register for VAT. A vendor making taxable supplies of more than R50 000, but not more than R1 million per annum, may apply for voluntary registration. Certain supplies are subject to a zero rate, or are exempt from VAT. Estate Duty: Estate duty is levied on the property of residents and the South African property of non-residents, less allowable deductions. The duty is levied on the dutiable value of an estate, at a rate of 20%, on the first R30 million, and at a rate of 25% above R30 million. A basic deduction of R3.5 million is allowed in the determination of an estate’s liability for estate duty, as well as deductions for liabilities, bequests to public benefit organisations, and property accruing to surviving spouses. Donations Tax: Donations tax is levied at a flat rate of 20% on the cumulative value of property donated since 1 March 2018, not exceeding R30 million, and at a rate of 25% on the cumulative value of property donated since 1 March 2018 exceeding R30 million. The first R100 000 of property donated in each year by a natural person is exempt from donations tax. Securities Transfer Tax: The tax is imposed at a rate of 0.25 % on the transfer of listed or unlisted securities. Securities consist of shares in companies or member’s interests in close corporations. Tax on International Air Travel: R190 per passenger departing on international flights, excluding flights to Botswana, eSwatini, Lesotho and Namibia, in which case the tax is R100. Skills Development Levy: A skills development levy is payable by employers at a rate of 1% of the total remuneration paid to employees. Employers paying an annual remuneration of less than R500 000 are exempt from paying skills development levies. Unemployment Insurance Contributions: Unemployment insurance contributions are payable monthly by employers, on the basis of a contribution of 1% by employers and 1% by employees, based on the employees’ remuneration below a certain amount. Employers not registered for PAYE or SDL must pay the contributions to the Unemployment Insurance Commissioner. GrantsUpdated increases in social grants are as follows:

Welcome to 2023 – a new year and a blank slate of 12 months, 52 weeks, 365 days, 8760 hours and 525 600 minutes to make changes, take on new opportunities and set new goals. We all kick off a new year with certain resolutions in mind, such as eating healthy and exercising more. More often than not, it’s not just our dress or pants size that feels a bit tighter than before the holiday indulging, but also our purse strings. Too many people are left with more month than money after holiday spending, with January probably feeling the hardest. Whether or not you have an extra dime to spend at the end of a year, or perhaps at the start of this new one - by means of employee rewards (such as a bonus), or by not spending all you set aside for the holiday gifting season - why not use the start of the new year to get that savings mindset into gear. If you have overspent, drawing on the below tips in the new year is even more important.  Last month we talked about Money Is A Means To An End. This month we focus on Step 8 - Set Up Short-term Goals.

According to the website www.mindtools.com, the process of setting goals helps you choose where you want to go in life. By knowing precisely what you want to achieve, you know where you have to concentrate your efforts. You'll also quickly spot the distractions that can, so easily, lead you astray. I define short-term goals as something you would like to achieve in the next two years. Depending on your personality and preferences, you may define the short-term as things that happen in the next 12 months. Have your notebook and pen ready at your desk. Think about the things you know are going to happen, or your plan for in the next two years. Jot them down in your notebook. Speak to your spouse, partner, children, families and friends that you would like to plan things together with, jot down the additional things that are going to happen in the next two years. Examples or ideas are: Attend a wedding Getting married Finish my study Finish reading this book Learn to cook a cuisine Learn something new (be specific) Start a family Buy a house Renovate my house Buy a car Pay for my children's education Pay off my credit card debt A weekend away Year-end holiday Overseas holiday (if COVID restrictions allow!) Start a side hustle 30th birthday party Run the Two Oceans Marathon Make a donation to a charity You can now develop the list of short-term goals into a spreadsheet in your notebook, or use a spreadsheet such as Excel or Google Sheets, with the following columns: Column 1: Description of the goal Column 2: With whom (you will be doing this with) Column 3: Date (an approximate date is fine) Column 4: Amount required (this is the amount of money required for that goal) Column 5: Bank/investment account for this purpose Column 6: Notes/Comment (this is where you expand, to explain who will contribute, whether you will contribute for someone else, someone else will contribute for you, how you are going to build up the fund, monthly or an ad-hoc lump sum) Column 7: Status - Not started, in progress, completed Write your goals on colour stickers or magnets, stick them on your wall so they are visible, acting as reminders to you. Work out your monthly plan to attain these goals. Revisit your short-term goals spreadsheet monthly, say at the end of the month, to check whether you are on track, or anything you still need to do.  Last month I talked about Step 3 - Do not take on credit. Let's continue with Step 4 - Keep a record of your spend. The foundation of good personal finance is budgeting. Expense tracking is the twin brother of budgeting. Budgeting is the process of creating a plan to spend your money. This spending plan is called a budget. Creating this spending plan allows you to determine in advance whether you will have enough money to do the things you need to do or would like to do. Budgeting is simply balancing your expenses with your income. Track your daily expenses for a minimum period of three months. At the end of each month, sit down and analyse where your money has gone, so you can identify ways of cutting expenses. You will be surprised to find you have been paying every month for something you have not used. There are many ways of tracking your expenses:

2021/5/15, groceries, R522.35 2021/5/16, DSTV, R499 2021/5/16, Nandos takeaway, R136

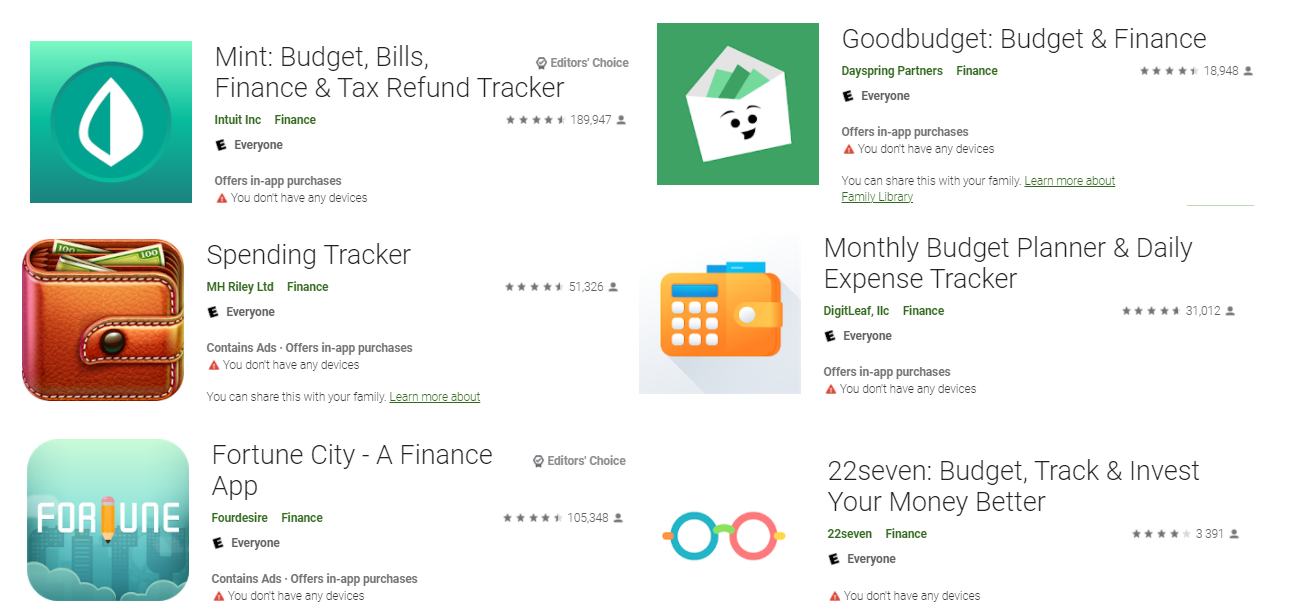

Google Play store: Mint - 4.5 rating Goodbudget - 4.4 rating Spending Tracker - 4.5 rating Monthly Budget Planner & Daily Expense Tracker - 4.7 rating If you like to blend expense tracking with gaming, try Fortune City - 4.4 rating 22seven is developed locally in South Africa, now part of Old Mutual - 4.0 rating  Apple App Store: Mint - 4.8 rating Goodbudget - 4.7 rating Spending Tracker - 4.8 rating If you like to blend expense tracking with gaming, try Fortune City - 4.5 rating 22seven is developed locally in South Africa, now part of Old Mutual - 4.2 rating

Share with us your story of tracking expenses and budgeting! We'd love to hear how it goes with you. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

||||||

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|