|

The FIA Intermediary Experience Awards is the most prestigious and well-known annual recognition event in the South Africa financial services industry for more than 20 years. The Awards recognises product providers (insurers) for the products, solutions and services they offer to the end-consumer through our member intermediaries or financial advisers.

This year's winners are: Sanlam won long-term insurer of the year (risk). The non-life insurance awards were split by sector. Santam won for personal lines; Western National for commercial; and Hollard for corporate. Allan Gray won two awards for investment products: lump sum and savings. Discovery Health won for healthcare Momentum Corporate for employee benefits. We congratulate these product providers for winning this prestigious award. We as Daberistic have had long-term relationship with these product providers, and we will continue to offer the best insurance and investment solutions to our clients.

0 Comments

For urgent assistance and to prevent delayed turnaround times due to reduced number of staff between 20th December 2021 to 3rd January 2022, please contact your insurance provider on the contact numbers below.

Medical Aid 1. Discovery Health: 086 099 8877 2. Fedhealth: 0860 002 153 3. Momentum Health: 0860 11 78 59 4. Bonitas: 086 000 2108 5. BonCap Members: 0861 239 333 Hospitals in Gauteng 1. Bedford Gardens: 011 677 8500 2. Life Fourways Hospital (Fourways): 011 875 1000 3. Morningside Medi-Clinic (Sandton): 011 282 5000 4. Sunninghill Hospital: 011 806 1500 5. Garden City Hospital: 011 495 5000 6. Waterfall City Hospital (Kyalami): 011 304 6600 7. Glynnwood hospital- 011 741 5000 Life cover 1. Discovery Life: 0860 00 54 33 2. Liberty: 0860 456 789 3. Momentum Myriad: 0860 69 74 23 4. Old Mutual Greenlight: 0860 50 60 70 5. Old Mutual Self-service support centre: 0860 60 65 00 6. Sanlam: 0860 726 526 Short-term Insurance (Car & Business) 1. CIB: 0860 104 952 2. Momentum: 086 078 4767 3. Brolink: 0861 338 339 4. Santam: 0860 505 911 5. Discovery Insure: 0860 999 911 6. Echelon: 0860 200 002 / 083 789 9932 7. First Road Assist: 0860 911 326 Emergency services 1. Netcare 911: 082 911 2. ER24: 084 124 3. Ambulance: 10177 4. Police: 10111  Apart from estate planning benefits, the latest budget changes further strengthen the tax benefits of the endowment, which is encouraging investors to revisit the case for this often overlooked product.

To build a successful long-term investment portfolio, one must consider ways to enhance their capital whilst finding efficient mechanisms to reduce your taxes. Endowments remain a useful investment vehicle and offer a disciplined way of saving where you are committed for a certain period so that you can reach your goals. The tax benefits of endowment policies Endowments offer an attractive tax-efficient option for people who want to save more than the maximum annual limit for tax-free savings accounts, and those who have exhausted their annual tax allowances such as tax-free interest income. The recent increase in the CGT inclusion rate means: an 18% effective tax rate on capital gains for individuals in the highest income tax bracket, and 36% for trusts, for an endowment policy, the effective CGT rate for these individuals and trusts is just 12%. In addition, tax on income is 30% for endowments as opposed to 45% when these individuals are taxed according to their marginal tax rates in other investment vehicles. This tax treatment is also beneficial for other income categories as well (i.e. for everyone with a marginal tax rate above 30%). In addition to tax savings, an endowment offers the following advantages: Simplified tax administration as tax is recovered within the endowment and taken care of on behalf of the investor. Insolvency protection – the entire value of the policy will be protected against creditors three years after inception until five years after the maturity, or termination of the policy. Beneficiary nomination can lead to potential savings on executor’s fees (up to 3.99% of fund value). Where a beneficiary has been nominated, payment of the death benefit does not depend on the winding up of the estate and beneficiaries will receive the proceeds relatively quickly. Liquidity is created in the estate as payment of the death benefit does not depend on the winding up of the estate and beneficiaries will receive the proceeds relatively quickly. Advantages of staying invested in an endowment, even after maturity

Source: Sanlam  Yesterday (Happy International Women's Day!) I was fortunate to visit Dodge & Cox in San Francisco, US. Kevin Johnson, an experienced portfolio manager at Dodge & Cox, was kind in spending over an hour with me, for me to understand more about the firm, its operations and investment outlook. Dodge & Cox is situated in the Financial District of San Francisco, occupying 4 floors in this very impressive skyscraper on 555 California Street.

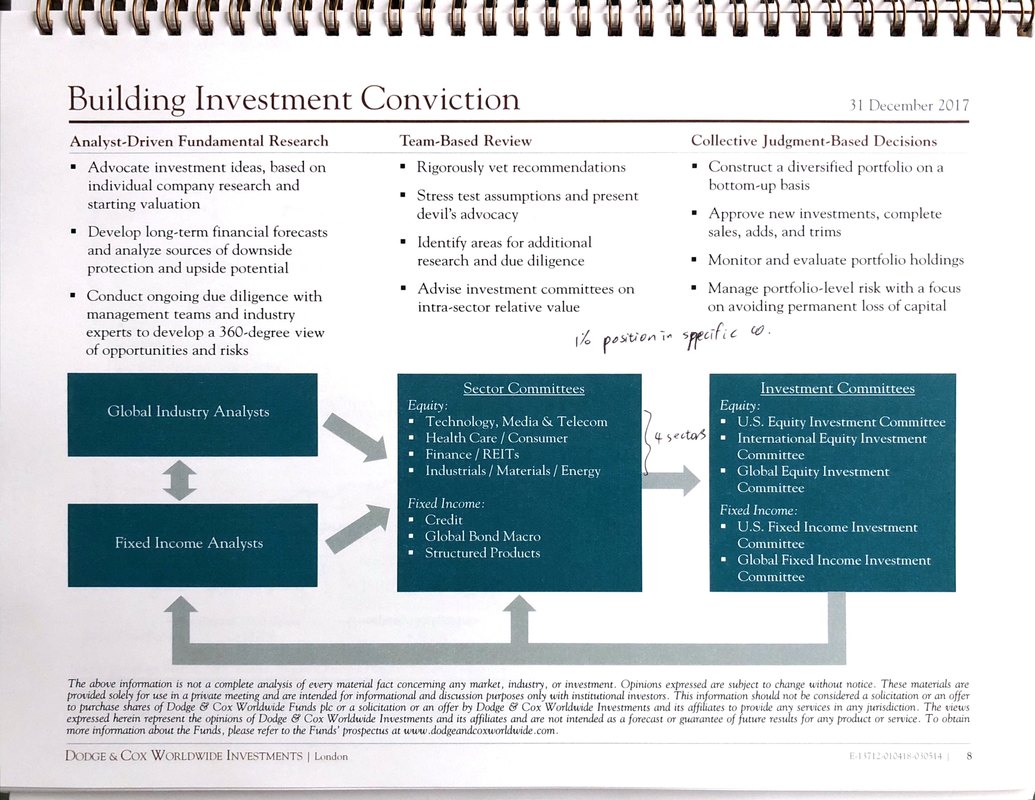

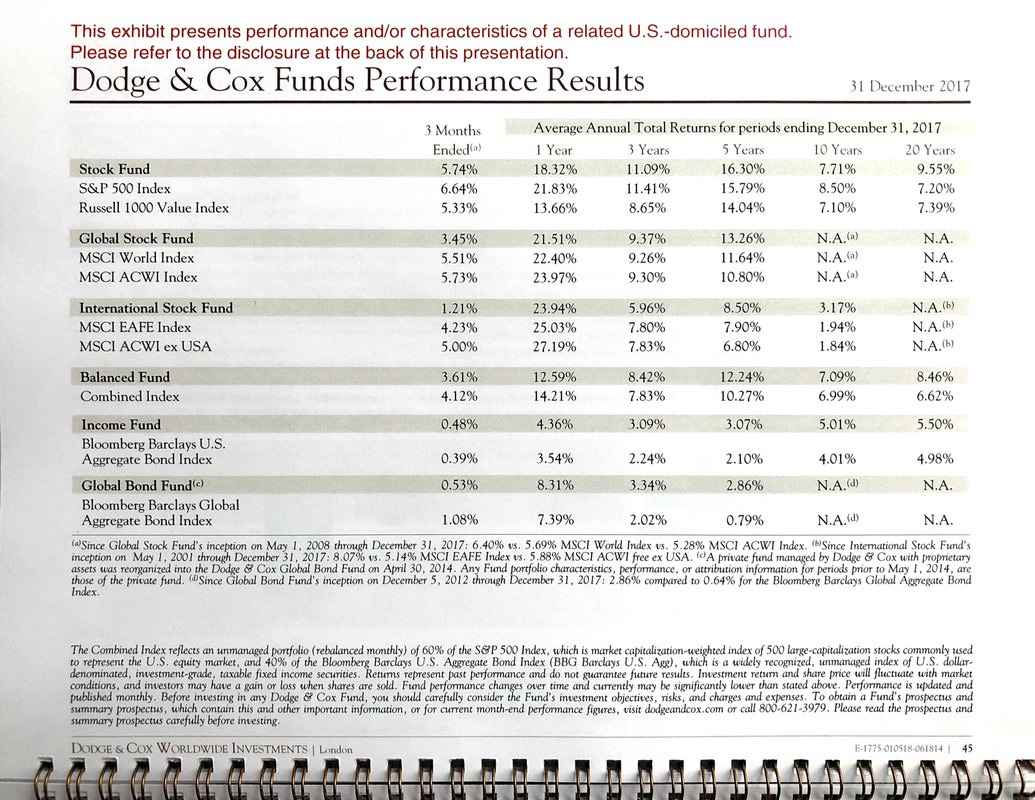

After the guest registration process at the lobby, I was told to take a lift to the 40th floor. When the elevator door opened, I walked onto think carpet, with the gold plated Dodge & Cox signage in front of me. I knew I was at the right place. The office has stunning views of the San Francisco Bay area. The tall building in the second picture is Transamerica Pyramid, 260m high.   Kevin Johnson came and welcomed me, took me to the boardroom with stunning views of San Francisco. I decided to sit with my back facing the view/window, so I could better focus on my discussions with Kevin. Kevin Johnson is well versed in the investment markets, with 28 years of experience at the firm. I gave him a background of what Daberistic does, our wealth management services to our clients, and how Dodge & Cox funds fit into our solutions to our clients. Kevin then gave me a presentation booklet on Dodge & Cox UCITS. I am not familiar with the term UCITS, so afterwards I googled it. UCITS stands for “Undertakings for Collective Investment in Transferable Securities". In essence mutual funds, or unit trusts as known in South Africa. Dodge & Cox was founded in 1930 in San Francisco. It prides itself in having a stable and well-qualified team of investment professionals, most of whom have spent their entire careers at Dodge & Cox. Ownership of Dodge & Cox is limited to active employees of the firm. Currently there are 75 shareholders and 271 total employees. It is a mature fund management business. Kevin emphasised the point that Dodge & Cox is independent, no absentee ownership, no parent company to report to, so not forced to do anything. This is a great contrast to Merrill Lynch, which is owned by Bank of America. Dodge & Cox is solely in the business of investing clients' assets. Apart from the San Francisco office, it only has one small client service office in London. So all its staff are based in the single office in San Francisco. It offers a focused range of strategies (I tend to like fund managers with a small, focused range): US equities Non-US equities Global equities: combination of the above two US Fixed Income Global Fixed Income US Balanced (combining equities and fixed income) Active vs Passive This debate continues to rage on. Kevin and Dodge & Cox are undoubtedly in the Active Managers camp. His comments? Active managers have been overly criticised for high fees, the focus on (comparing to) average active managers return is a mistake. Dodge & Cox wrote an article on the characteristics of good active managers. These include: 1. Low turnover 2. Experienced 3. High active share. Passive is really a Momentum strategy, buying more on the way up. He used the dotcom bubble as an example: in 1998 the tech sector accounted for 45% of S&P, and index trackers would continue buying more of tech companies as their weightings in the index rose. Only to see the dotcom bubble burst until 2002. What is important is to focus on performance after fees, he comments. I 100% agree with this point. Dodge & Cox is a value-driven fund manager. Value as a style has fallen out of favour with investors over last few years, as the bull market continues to rise. Dodge & Cox continues to stick to what it has done over last 88 years, without wavering. Value Defined It is always good to get under the skin of a manger to understand better what they mean. Kevin defines the firm's Value Investing as "what you thing it's going to be worth in the future. It can be strictly metric based, such as PE ratio. It can also be valuation relative. You would want to avoid something with very high premium built in the price, as it may not be sustainable." So Dodge & Cox sees value in a slightly different way to Warren Buffet. It uses four investment hypotheses: Above Average Growth, Compounders, Cyclical or Asset Play, Deep Value or Turnaround. Warren Buffett's style is probably more the first two hypotheses. Risk Management Over the years I have learnt to appreciate that the best fund managers are also the best risk managers. Dodge & Cox has a systematic way of analysing risks, under the six headings of Operational, Macroeconomic, Commodity, Financial, Technological and Political/Legal Risks. These are used to assess what will cause the future outcomes to disappoint. Investment process Dodge & Cox has a tried and test investment process, run by a very experienced team.  I posted some very specific questions to Kevin, his comments are as follows: Schroders as a value manager We as a manager do not worry about what other fund managers do. My impression is they have an excellent reputation, has value orientation. It may have lots of funds. On the question of the use of the word Recovery in Schroders global Recovery Fund: "There can be an element of marketing. This might define value in a more narrow way." Coca-Cola "it is a good business, not a lot of growth, highly priced. We don't own any Coca-Cola stock. Maybe when its PE is 13 it becomes interesting to us." Amazon "A remarkable company, high valuation makes no sense to us. However what it does influences our thinking on other retailers. Retailers like Sears and JC Penny have been in decline for years. Macy's also struggling, not to the same extent. Walmart and Target have done better in response to the changing business environment, the online/offline mix strategy is a good one." Its AWS (Amazon Web Services) also influences our thinking on other tech companies like Microsoft." "of the FANGs, we only own Google" Dell Dell just came out with its update, showing 9% turnover growth and doubling operational losses, so I posted to Kevin. "Dell went largely private, had a series of corporate actions over last 2 1/2 years. Laptops have low margin, the profitable part is server/other services." Portfolio diversification As a wealth manager I am very sceptical of funds with 20% weighting in one stock (Naspers), as I question their risk management and diversification. "We do not have more than 5% of portfolio in one holding. In our Global Stock Fund, we probably will not exceed 3%." Its original (US) Stock Fund has an enviable track record of annualised 9.55% return over 20 years, outperforming S&P500. Over 10 years a respectable 7.71% after fees. The Global Stock Fund, which South African investors can access via Glacier Global Stock Feeder Fund, has done annualised 13.26% in USD over last 5 years.  The time was just too short, if there is an opportunity I would come back again. At the end of the meeting I asked Kevin to take a photo together. He agreed as a gentleman.   A very interesting question almost every investor asks themselves is: "If I want to invest money, do I need to buy a property, keep my money in the bank to earn fixed interest rates or invest in stocks?" This is a difficult question to answer simply. All of us have an ambition to invest our hard-earned funds as optimally as possible to ensure we maximise returns. This question is particularly important considering that a one or two percent difference in annual returns significantly impacts the longer-term result. A look at the figures To try to answer this question, the figures should be thoroughly investigated. The following table shows the annual average returns of shares (measured by the FTSE / JSE All Share Index), money market yields (SteFI Composite Index) and direct residential real estate (average prices of South Africa). This draws a comparison between the potential returns that an investor in the stock market can earn in a bank account versus direct property.  Once the figures are taken into account, it is clear that an investment in equities over the long term provides the highest yield. Also, we saw that direct property prices experienced a boom period during 2002-2007 with an average annual return of 18.2%, and began to show signs of slowing (2008-2016) by delivering an average return of 3.8%.

However, the choice is more complicated than simply considering returns over different time periods. Every South African knows that Cape Town property growth will be more attractive than property yields in smaller towns up-country. So geographical location must be taken into account. If the average annual return of the Eastern Cape (7.8%) is compared with that of the Western Cape (9.3%), it is clear that location plays an important role. This phenomenon is further accentuated with the stagnation of the overall residential property market compared to metropolitan areas, especially Cape Town which still experiences a boom in house prices. The impact of rental income It is also important to understand that the above figures exclude rental income. This component ensures, on average, 5% - 8% additional returns per year in rental yield. The issue of rental yields is more applicable if direct property is bought with cash as opposed to using bank financing. If the rental income is taken into account (at the lower limit of 5%), property falls into the same category of return as equities over the long term (14.65% vs. 14.79%). The choice of investment vehicle will depend on a set of additional factors. These factors are briefly highlighted below. If you would like to invest in a Unit Trust or find out more information, please contact Kevin or Thato, email: invest@daberistic.com tel no: (011 658-1333) Written by: Jan Vlok Source: Sanlam  Decreases in cost and increases in transparency and choice regarding underlying investment options make endowments a viable option to consider for discretionary (non-retirement funding) savings.

In addition to estate planning benefits, the latest budget changes further strengthen the tax benefits of the endowment, encouraging high income investors to revisit the case for this often overlooked product. Increased income tax rates The recent budget proposed that personal income tax rates increase by 1%. This was done from the second bracket (those earning in excess of R181 900 per year) upwards, but considering adjustments to rebates and tax brackets there will only be tax relief for tax payers earning below R450 000 per year. The highest tax bracket for individuals has now increased to 41%. This tax rate now also applies to trusts (other than special trusts), which previously paid 40%. When does an endowment make sense? There are a number of factors to consider when choosing between a pure discretionary savings plan (DSP) or an endowment. This includes availability of interest and capital gains allowances as well as required access to capital within the first five years. A key consideration in how to allocate between the two products is the clients’ tax rate. Income tax legislation requires policyholders of an endowment to be classified as an individual, company or untaxed policyholder and income and capital gains tax varies accordingly. An endowment is available to individuals as well as trusts with individuals as beneficiaries with tax as follows: Tax on income at 30% and effective tax on capital gains at 10%. Individuals in a DSP are now taxed at marginal rates up to 41% resulting in an effective tax rate on capital gains of 13.7%. For such high income earners the endowment can offer significant tax saving. Within the two products there is no differentiation for dividend tax, which is withheld at 15% either way. How much can you save on tax in an endowment? Consider an individual that has no interest and capital gains allowance available and invests R5m for 10 years. Assume a balanced fund-type investment with 11% return per annum and no trading of the portfolio over the period. After five years, allowing redemptions for payment of income tax annually, such an investment would have grown to R8.16m in a DSP. An equivalent investment in an endowment would have grown to R8.23m, but saved about R145 000 over the period. This consists of: income tax saving (30% versus 41% marginal rate assumed) capital gains tax saving (taking 100% of the capital gain into account) additional return earned as a result of higher base to compound from Over the full 10 year period assets in the DSP would be at R13.32m, but the investor would have missed out on a total saving of R426 000 relative to the endowment. Do the math Trusts or individuals with significant discretionary savings and high marginal tax rates should consider an endowment. There are restrictions that may not make it a suitable option, but multiple benefits and the significant potential tax saving are not to be ignored. Benefits of an endowment Greater tax efficiency for higher income earners (above 30% tax rate) who have exhausted their interest exemptions. Beneficiary nomination can lead to potential savings on executor’s fees (up to 3.99% of fund value). Where a beneficiary has been nominated, payment of the death benefit does not depend on the winding up of the estate and beneficiaries will receive the proceeds relatively quickly. Tax administration is taken care of on your behalf (the insurance company calculates, deducts and pays the tax to SARS). Insolvency protection – the entire value of the endowment will be protected against creditors after three years. This protection will continue until five years after the termination of the policy. Investors are not restricted to maximum levels of equities and offshore investments, as in the case of retirement savings products. Investors can also use an endowment to draw income upon retirement – provided the five-year restricted period has passed. This may be done on an ad-hoc basis, and you are not forced to draw income at specific intervals. To get a quote for your Endowment policy please contact please contact Kevin or Thato, email: invest@daberistic.com, tel no: (011 658-1333) Written by: Roenica Tyson Source: Sanlam |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|