SA Market Commentary

South African equities did not escape the global selloff, with the JSE All Share Index finishing the month sharply lower, weighed down by poor performance from financials exposures. Local bonds had a severe reaction to the global risk off environment, with yields spiking and relatively liquid areas of the bond market including SA government bonds selling off significantly. Local listed property had its worst month on record, with investors becoming concerned about ever increasing loan to value ratios in the sector as well as some local retailers seeking rent free periods during the SA lockdown. The rand was materially weaker against developed market currencies during the month, which did slightly dampen the negative contribution from moves in global equity markets. Global Market Commentary March 2020 will go down as one of the more eventful months in global market history, as significant equity market volatility and declines across the globe dominated news headlines. Concerns around the spread of the coronavirus (COVID-19) were exacerbated by an oil price war which flared up at the beginning of March as OPEC (led by Saudi Arabia) and Russia failed to come to a consensus around OPEC’s demand to cut oil production by 1.5 million barrels a day. The initial effects of lockdowns across the globe in response to the rapid spread of the coronavirus started to filter through to economic data, with US jobless claims hitting a record figure of 6.7 million people for the week ended 28 March. Source: Morningstar

0 Comments

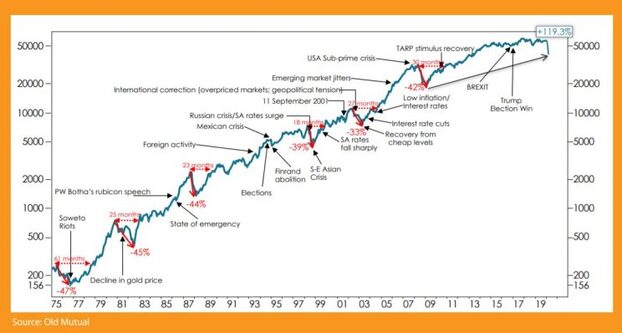

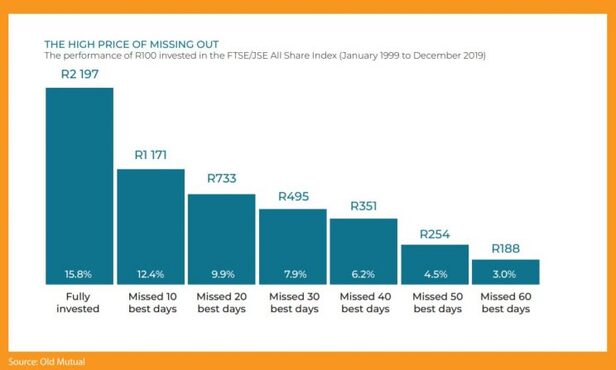

The Covid-19 global pandemic has caused ripples through global financial markets as the virus continues to spread across the globe and governments battle to find the right measures to contain it. We still do not know what the eventual impact will be, and how the pandemic will impact countries, markets and families. From a financial and investment perspective, we can stand back from the current crisis and reflect on the anatomy of a crash and how markets behave during and subsequent to a crash. We should expect a market crash every six years. A market crash or bear market is defined as a market correction where the market falls by more than 20% from its previous high. Looking at the biggest stock market in the world, the US, the S&P 500 (the broad measure of the US market) has experienced 16 bear markets since 1926, averaging one bear market or correction every six years. The average of these market losses has been an eye opening 39%!  From the above, it is clear that South Africa is part of the global village and we are exposed to global market shocks. Except for the Soweto riots, it has taken between 18 and 30 months for the market to recover back to their previous highs following a shock. Lesson 1. Markets have historically recovered from a crash Markets are erratic It is impossible to predict market returns, specifically during a crash when markets are reacting emotionally and erratically. This is clear in looking at share prices during the last week and by merely looking at the headline of one share, Sasol. • March 12: Sasol loses another 40% of its value in an hour • March 13: Sasol surges 45% after announcing sale of stocks and assets The above is an example of how erratic the market can behave during a stock market crash, thus in a few days you could have lost 40% or made 45%. If we stand back from a specific share, and look at the market as a whole, the US sub prime crisis (also know as the financial crisis) resulted in the JSE correcting by 42%. In 2008 alone, the South African market fell by just over 30%. Even though it was impossible at the time to determine when the market would recover, the crash of 2007/2008 was followed by exceptional returns in 2009 with the market recovering by more than 20%, followed by double digit returns in; 2010, 2012 and 2013. Investors where thus rewarded for staying the course, as per their financial plan and objectives. The extreme volatility is also evident in returns the last week, amidst the Covid-19 pandemic: • March 11:US (S&P) selloff approaches 20%, what next? • March 13: US market scores biggest gain since 2008, S&P 500 jumps by 9.28% It is important to remember that in disinvesting from the market, there are two decisions to get right; the right time to disinvest and the right time to reinvest in the market. Thus, investors must get both the exit and entry prices correct which is extremely difficult. The probability of timing the markets is summarised in a research study conducted by Vanguard (one of the world’s largest asset managers): “The biggest takeaway from our analysis is that the probability of being lucky and outperforming the benchmark is already less than 50% when taking just a few days out of the market. This probability then decays rapidly as the number of days out of the market increases. Unless an investor has great skill and/or luck and the conviction to act on these insights, the most effective approach is to remain invested.” The risks in attempting to time the market are further illustrated by the research conducted by Old Mutual Investment Group.  Lesson 2. Markets can be crazy during a crash and are impossible to time. Stay invested. Your portfolio should reflect your financial personality. It is often said that diversification is the only free lunch in investments. The principle behind diversification is investing in several different asset classes or investment types i.e. South African: equities, fixed interest and property and international: equities, fixed interest and property. The spread of investment risk (diversification), reduces the exposure to any one asset class significantly underperforming. Diversifying into international assets acts as a handbrake during global market uncertainty or market corrections. As investors withdraw from emerging markets (which are perceived as risky) and invest into developed market bonds (which are a safe haven in times of uncertainty) emerging market currencies depreciate. In such a scenario the offshore exposure in an investor’s portfolio benefits from rand depreciation, even though the underlying asset prices may be falling. The below illustrates the benefits of diversification by investing in a balanced portfolio during the financial crisis in 2008:  Balanced low equity funds represent a portfolio for conservative investors where the equity exposure is limited to 40%, the equity exposure can go up to 75% in the balanced high equity funds, which is more suited for moderate or growth investors. In both the aforementioned funds, the offshore equity exposure may be up to 30%.

The above analysis illustrates a few important investment principles, that will apply in most market corrections or crashes: • Markets recover after sharp losses or bear markets • Balanced funds provide investors with protection against market corrections. • Balanced low equity funds provide significant protection during periods of uncertainty. They do however significantly lag during the “recovery phase”. Investors often switch to low equity balanced funds during times of uncertainty, this can result in them missing the market recovery and only switching back to higher risk balanced funds subsequent to the market recovery. Timing is a mugs game, investors need to stay true to their specific risk profile and appetite; through both bull and bear markets. Lesson 3. Diversification is the only free lunch and protects investors during a crash Your money personality (risk profile) should not change during a crash. Guaranteed annuities (pensions) provide a sense of comfort during bear markets. During recent years we have seen an increase in the interest in traditional or guaranteed life annuities. Guaranteed life annuities are provided by insurance companies including Old Mutual, Sanlam, Discovery, Liberty and Just SA who guarantee an income for life. There is a wide variety of guaranteed annuities, with the most popular being inflation linked and with profit annuities. Investors’ pensions payments are protected through very strict governances and regulation requiring that insurers hold sufficient capital to back their liabilities i.e. pensions owed to investors. These capital adequacy ratios require that insurers hold enough capital to make provision for market shocks or corrections. Thus a “normal” market correction should have very little impact on insurers’ ability to continue paying pensions. Investors invested in life annuities that provide inflation-linked increases have little reason for concern as their future increases remain linked to inflation. The annual increase of with-profit annuities is linked to the performance of the markets and, depending on the insurer, is linked to market returns over i.e. a five to six-year period. It remains difficult to determine the impact of the current market turmoil on investors invested in with-profit annuities. Should the turmoil continue, and markets not recover, they may be faced with zero increases. For many retirees, with-profit annuities provide an effective annuity or pension strategy, if used appropriately with other annuities or the provision of an emergency fund. The benefit of with-profit annuities is higher pension over time. Globally the flight to safety has had a negative impact on retirees wanting to invest into life annuities. Annuity rates largely depend on bond yields. Global bond yields (which were already low) have fallen even lower as investors pile into bonds which are perceived as a safe haven investment. This has resulted in a decrease in annuity/pensions for retirees in many developed markets. We have not yet seen the same impact in South Africa, with long bond yields remaining relatively stable, thus the SA life annuity yields (starting pension) have remained relatively stable during the last two months. Lesson 4. Traditional life annuities or hybrid annuities provide some comfort during a market crash What should investors do? It is almost impossible to predict how the markets will react or recover during this pandemic. The following are a few principles that investors can follow during this time: Stick to your plan Your financial plan should be developed to consider your personal objectives and your risk profile. It is important to review your plan to ensure this still aligns to your objectives. However, be wary of changing your “money personality” due to the noise and the crisis, your risk profile should remain intact during both bull and bear markets. Let the professional money managers do their job A diversified investment portfolio should include several investment managers and investment mandates aligned to your risk profile. The investment managers will align the underlying portfolio to the current market conditions and increase or decrease the equity exposure within the parameters of the mandates to mange your portfolio and risk on your behalf. Now is the time to be frugal If you have not made provision for an emergency fund, now is the time to be cautious, save on luxuries and where possible build up a buffer or emergency fund. Given the continued uncertainty it is important to diligently manage expenses and increase the allocation to your emergency fund. It is now more prudent to be conservative with your finances than to overextend during these times of uncertainty. The Covid-19 market crash is a shock, and we are all concerned about how this virus will be contained. From a financial perspective, it is important to remind ourselves that this is not the first crash we have seen, and certainly won’t be the last crash that most investors will experience. A well-structured financial plan, implemented through a diversified portfolio, will assist in delivering on investors long-term objectives through difficult markets. Wrritten by Wynand Gouws Source: Moneyweb  With so much uncertainty for many people regarding their income, Medical schemes have various options to assist members in this time to try ensure members remain covered.

Before you consider these options you could also consider: Downgrading your option: Your ability to downgrade may differ from scheme to scheme. Some medical schemes do allow members to buy down to a lower option during the year. This way members can reduce their monthly contributions to the medical scheme without giving up their membership. It is important for members to be mindful that terms and conditions apply to downgrading and these must be checked before a downgrade is requested. Below are the different schemes with a list of options for premium relief. Discovery health

Momentum Health

Fedhealth

PPS & Profmed Hold back termination of medical aid for 90 days due to non-payment. Status of medical aid will be suspended during 90 days. If you need further assistance on your medical aid please contact Namhla or Tammy email:health@daberistic.com tel: (011)658-1333  Below are the different premium relief options announced by short-term insurance companies on car insurance, due to Covid-19 lockdown. It stands to reason that insurance companies should cut the premiums during this period, as people stay at home and do not drive, hence much fewer motor vehicle accidents and claims. This is good news for consumers under financial distress:

Discovery Insure Discovery Insure is offering a Motor Premium Relief Benefit to all Discovery Insure personal and business insurance clients during this time. The Motor Premium Relief Benefit will apply to May Discovery Insure motor vehicle premium and will be based on how much you drive during the month of April, as follows - If the client drives less than 500 km in April, they will receive a 25% discount on their May Discovery Insure premium for that vehicle - If the client drives more than 500 km in April, they will receive a 15% discount on their May Discovery Insure premium for that vehicle Santam There is a premium-relief support for a maximum of two months. Please see below the qualifying criteria for premium-relief due to unpaid premium as a result of the lockdown (Covid-19): - On risk with Santam for minimum 3 years. (Clients under 3 years to be referred) - No unpaid premiums in the last 12 months (up to and including March 2020) - Loss ratio below 70% over 3 years for Personal lines - Loss ratio below 65% over 3 years for Commercial Lines - Three claims or less in the 3 years excluding CAT claims Momentum A premium pause option will be available during, and continue after, the lockdown period. Upon reinstatement of the premium at any point, following the pause, MSTI will not deem the period as a break in cover with MSTI, which otherwise might impact the clients’ risk profile. Pro rata premiums will be charged from that day onwards and cover will be reinstated. Here is a list of discounts on premium offered by other insurers Standard Bank 25% Outsurance 15% Miway 10% Old Mutual iwyze 7.5% This compares favourably with international peers in the US, UK and Australia. If you would like us to do a comparitive quote please contact Edmond or Rethabile email: shortterm@daberistic.com tel: (011)658-1333 With most people at home or working from home, it is important to continue to look after your health and the health of your family. Although Covid-19 is now on top of everyone's mind, don't let the negative news and damaging effect of Covid-19 get to you. Stay positive, have a daily routine, do physical exercise, and take time to reflect. Below we have put together useful health information: Government's coronavirus update and information website https://sacoronavirus.co.za/ Fitness Discovery Vitality Home Workout Channel - short 15-minute workout sessions https://www.discovery.co.za/vitality/vitality-home-work-out-channel Planet Fitness Online Group Exercise Classes https://www.planetfitness.co.za/register/ Cooking Discovery Vitality Home Cooking Channel https://www.discovery.co.za/vitality/vitality-home-cooking-channel Cooking channels and videos on YouTube To consult a doctor Momentum Talk to a Doctor on your phone   Today is day 20 of the lockdown announced by President Ramaphosa. As we are in the 3rd week of lockdown, many people and businesses are affected, as people are not working and businesses are closed to operations. This leads to lost revenue and income. As a result, individuals and businesses are struggling financially during and beyond the lockdown period. In response to the government's call to action, most financial institutions have announced measures to provide financial relief. As the situation evolves from day to day, financial institutions continue to work with the government to reassess the situation, and further relief measures can be expected.

We have gathered below links to financial relief measures provided by financial institutions, we hope these can assist you during this difficult period. Note that the information may not be complete or the most up to date. Please speak to the bank, the insurance company, your broker or financial advisor to confirm. Banks Covid-19 debt assistance: https://www.nedbank.co.za/content/nedbank/desktop/gt/en/personal/covid-19-debt-relief.html?cmpid=dis:ned:ret:debtrelief:banner:ned Nedbank's relief measures for individual and small-business clients, including information on payment holidays, the newly announced SA Future Trust Fund for SMMEs, and other Nedbank debt relief actions, can be found on https://www.nedbank.co.za/content/nedbank/desktop/gt/en/info/campaigns/nedbank-covid19-page.html Select 'Business' then 'Covid-19 Relief'. Nedbank remains committed to meeting your banking needs through this challenging period. Standard Bank: https://www.standardbank.co.za/southafrica/personal/campaigns/covid-19 FNB: https://www.fnb.co.za/press-office/index.html ABSA: https://www.absa.co.za/personal/covid-19/ Capitec: https://www.capitecbank.co.za/global-one/banking_during_the_covid_19_lockdown/ • If you're worried about your income or your ability to make your Capitec loan repayments, talk to us – we can help. To make a payment arrangement, dial 0860 66 77 18 to speak to an agent Life insurance companies (Do consult your financial advisor on the best option for your personal circumstances) Discovery Life discovery_premium_relief.pdf Option 1 – Premium relief option: Qualification rules: The premium payer must be self-employed, a business owner or an employee of such businesses facing severely reduced income themselves, in an industry that is not an essential service as defined in the Labour Relations Act. This applies to small and medium enterprises (SMEs) that meet the definition of a Small Enterprise in South Africa as per the Department of Small Business Development. The policy must have been in force for at least two years. The client must not have received a credit control letter in the past two years. The policy must have Comprehensive Integration with the PayBack benefit. At the moment, the policy's accumulated Surplus PayBack fund or Five-yearly PayBack fund has at least enough funds for two months’ worth of premiums. Policies that are in claim or have a claim registered that is being assessed do not qualify. Option 2 – Suspended cover option (Cover-pause): Qualification Rules: The premium payer must be self-employed, a business owner or an employee of such businesses facing severely reduced income themselves, in an industry that is not an essential service as defined in the Labour Relations Act. This applies to small and medium enterprises (SMEs) that meet the definition of a Small Enterprise in South Africa as per the Department of Small Business Development. The policy must have been in force for at least six months. The client must not have received a credit control letter in the past six months. Policies that are ceded (given as security for a loan) do not qualify. Policies that are in claim or have had claims submitted do not apply Option 3 – Underwriting-free servicing option: • A completed servicing quote is required (reduction) • Removal of benefits will not form part of the offer when up-servicing after three months, free of underwriting Important: • The form for options 1 and 2 must be completed by the policy owner and sent from his or her email address on record. A policy owner is able to contact the Call Centre, be verified and update their email address – 0860 00 54 33. Old Mutual helping_your_customers_during_lockdown_-_rsa_2.pdf Sanlam Liberty life insurance policies riskpremiumbreak_final_.pdf Investment policies investmentpremiumbreak_1pager_.pdf Momentum momentum_myriad_covid19_ppo_information_leaflet.pdf momentum_myriad_covid19_ppo_faq.pdf PPS pps_option_1.png pps_option_2.png Short-term insurance companies Discovery Insure discovery_premium_relief.pdf Santam Premium relief is only available once a client has lapsed their premium. We support all actions being done with clients to restructure their existing cover and reduce their premiums such that they do not have to lapse their policies. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|