|

Dear Valued Clients,

In the world of investing, success is not solely determined by market trends or economic forecasts. Rather, it often hinges on our ability to navigate the complexities of human behavior and emotion. That's where behavioural coaching comes into play – a powerful tool that can significantly enhance your investment outcomes. Behavioural coaching recognises that our decisions as investors are influenced by a multitude of psychological factors, from fear and greed to overconfidence and herding behavior. By understanding and addressing these behavioral biases, we can make more informed and rational investment choices, ultimately leading to better long-term results. Here's how behavioral coaching can benefit you: 1. Emotion Management: Investing can evoke strong emotions, particularly during periods of market volatility. Behavioural coaching helps you recognize and manage these emotions, preventing knee-jerk reactions that could derail your investment strategy. By maintaining a calm and rational mindset, you can avoid impulsive decisions that may harm your portfolio's performance. 2. Goal Alignment: Behavioural coaching focuses on aligning your investment decisions with your long-term financial goals. By clarifying your objectives and risk tolerance, we can tailor an investment strategy that reflects your unique needs and aspirations. This ensures that your portfolio remains aligned with your overarching financial plan, providing a clear path towards achieving your objectives. 3. Overcoming Biases: We all harbor cognitive biases that can distort our perception and decision-making process. From anchoring bias to recency bias, these cognitive pitfalls can lead to suboptimal investment outcomes. Behavioural coaching helps you recognize and overcome these biases, allowing you to make more rational and objective investment decisions. 4. Long-Term Perspective: One of the key principles of behavioural coaching is promoting a long-term investment perspective. By focusing on the bigger picture and tuning out short-term noise, you can avoid making reactionary decisions based on temporary market fluctuations. This disciplined approach fosters patience and resilience, essential qualities for successful long-term investing. 5. Accountability and Discipline: Behavioural coaching instills accountability and discipline in your investment approach. By adhering to a well-defined investment plan and regularly reviewing your progress, you stay on track towards your financial goals. This disciplined approach helps you resist the temptation to deviate from your strategy, ensuring consistency and continuity in your investment journey. In conclusion, behavioural coaching serves as a guiding light in the often turbulent waters of investing. By harnessing the power of psychology and emotion, we can navigate market uncertainties with confidence and clarity. As your trusted advisor, we are committed to providing personalized behavioral coaching to support you on your investment journey. Remember, successful investing is not just about numbers – it's about understanding human behaviour and making smart decisions accordingly. Together, let's harness the power of behavioural coaching to achieve your financial goals and secure a brighter future. Best regards, Kevin Yeh, CFP Director

0 Comments

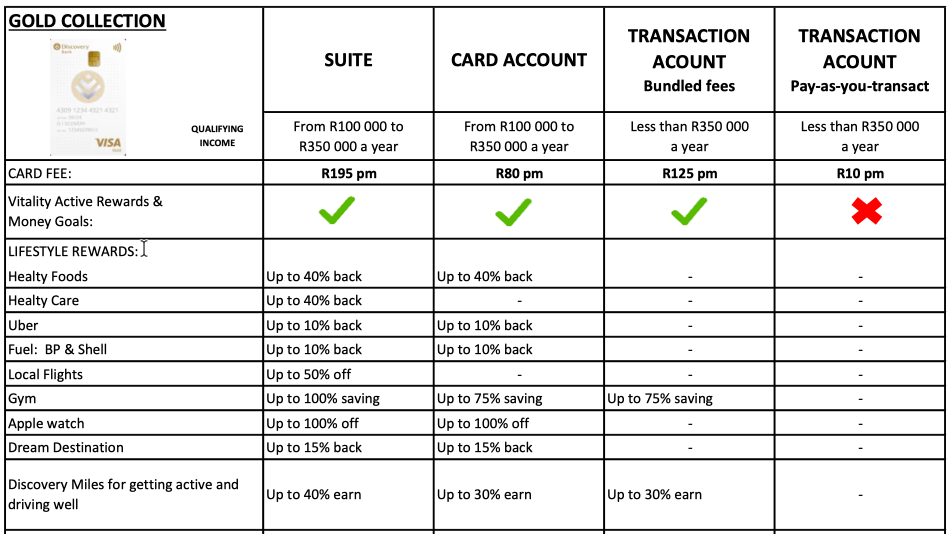

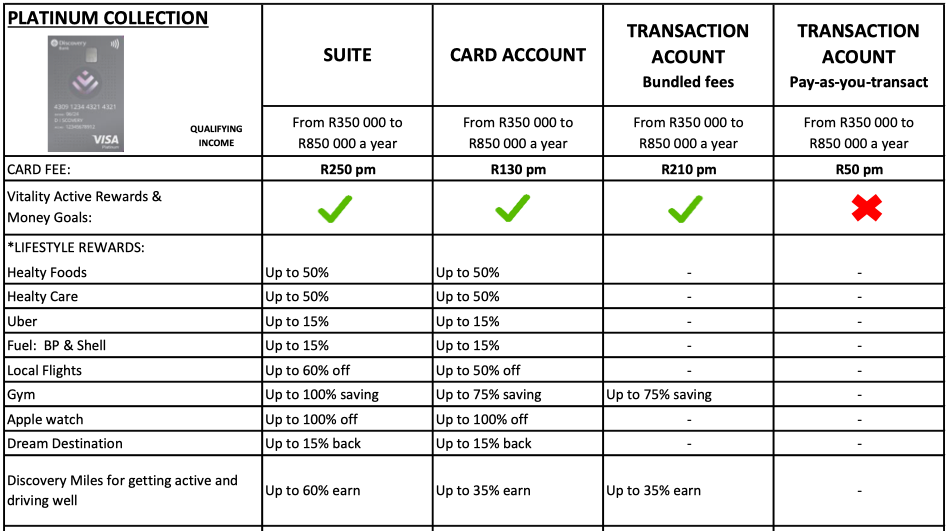

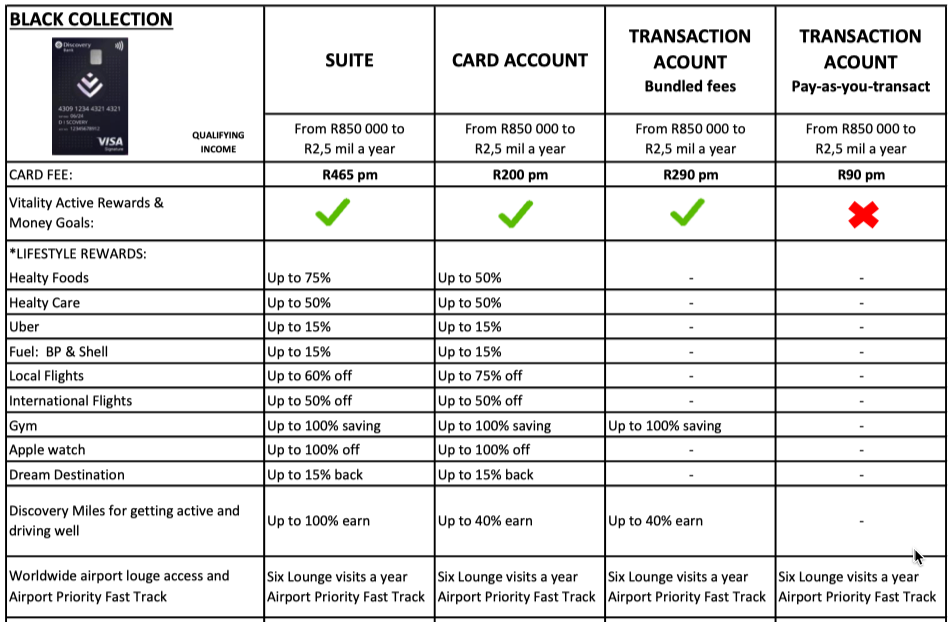

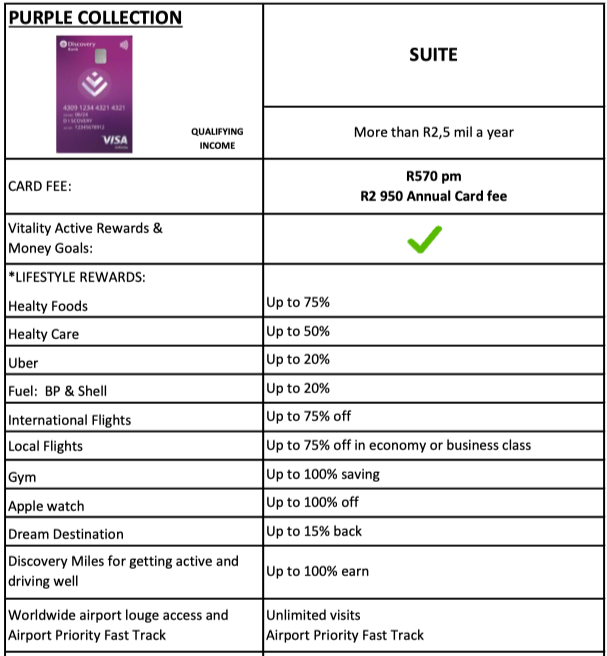

We as an accredited financial advisor can assist you in opening a Discovery Bank account. So which Discovery Bank product is right for you? Discovery Bank in South Africa is the banking brand of Discovery Group, a well-known South African-founded financial services organisation. It was established with the approval of the South African Reserve Bank in 2016. In the past three years, it has been actively growing its mass affluent client base, and now has more than 1 million customers. Here we explain the prerequisites for applying for a Discovery Bank account, as well as the key features of Discovery Bank products. The advantages of Discovery Bank Discovery Bank is a digital bank that focuses on the use of user-friendly technology and powerful security features, allowing customers to safely operate various banking and financial functions on their mobile apps, including: - Checking account balances - Opening a new savings account - Opening a new fixed deposit account - Opening foreign exchange accounts (USD, GBP, EUR) - Opening tax-free savings account - Earn Discovery Miles - View financial portfolio summary on all products you have with Discovery, including Life, Invest, Health and Insure. Discovery Bank is a financial behavioural bank, using gamification to help customers improve financial discipline and financial wellness in the following five areas: savings, investment, real estate, retirement, and debt. If the customer closes all five rings, he will reach the Diamond Vitality Money status, enjoying the best interest rates on positive balances and deposits, and earn the most Discovery miles. Discovery Miles is a virtual currency that can be used to shop online, buy airline tickets, exchange for coffee or game points. Discovery Bank gives interest on account balances. WIth the traditional Big Four banks, there is no interest paid on the positive balance in the transaction account or cheque account. Discovery Bank disrupts the market and allows customers to earn interest on the positive balances of the credit card or transaction account. This gives more money to customers. Disadvantages of Discovery Bank There are no physical branches, and all transactions must be performed on mobile phone app or on the website by customers. If you encounter any problems, you must contact the customer service centre of the bank. Prerequisites for applying for a Discovery Bank account - Customers are already familiar with using the mobile apps of mainstream South African banks such as FNB and Standard Bank to view accounts, download statements, and transfer funds. - Customer has a South African ID card or green ID book. - The client has an annual income of at least R100,000. - Proof of residential address (not older than three months) - Three-month bank account statements showing regular monthly income deposits at a bank. Discovery Bank Products Discovery Bank has four tiers, from Gold, Platinum, Black to the highest level Purple. Gold tier requires an annual income of R100,000 to R350,000. The products, monthly fees and benefits are as follows: Customers can choose to only open a transaction account, credit card account or package (Suite, including both transaction account and credit card).  Platinum tier requires an annual income of R350,000 to R850,000. The products, monthly fees and benefits are as follows: Customers can choose to only open a transaction account, credit card account or package (Suite, including both transaction account and credit card).  Black tier requires an annual income of R850,000 to R2,500,000. The products, monthly fees and benefits are as follows: Customers can choose to only open a transaction account, credit card account or package (Suite, including both transaction account and credit card). Clients have access to six airport lounge visits a year and Airport Priority Fast Track.  Purple tier requires an annual income of more than R2.5 million. The package, monthly fees and benefits are as follows: Customers can enjoy unlimited airport lounge visits and Airport Priority Fast Track.  If you are interested in opening a Discovery Bank account, please email service@daberistic.com with your name and cell number.

Last month we talked about Focus on Building Assets. This month is our 12th and final instalment on the series, we focus on Regularly Review Your Progress. Congratulations on make it this far!

Let's recap the first 10 steps: Step 1 - Make as much money as you can Step 2 - Do not spend more than you earn Step 3 - Do not take on credit Step 4 - Keep record of your spend Step 5 - Invest 15% of your earnings Step 6 - Set up an emergency fund Step 7 - Money is a means to an end Step 8 - Set up short-term goals Step 9 - Step up long-term goals Step 10 - Focus on building assets So what have you learnt so far? What have you written down and implemented? The last step of Regularly Review Your Progress completes the cycle. Review your actual progress against your budget, short-term goals and long-term goals, to check whether you are on track. In terms of your monthly budget, you should check monthly. In terms of your short-term and long-term goals, you should review your progress at least annually. Typically the good time to review would be the end of a calendar year, the beginning of a year, or the middle of a year (June/July). They tend to coincide with the school holidays. Regular reviews can check whether you are on track, ahead of your schedule or behind your schedule. Are you moving forward, or backward? What were the unexpected things that happened, good or bad? It will help you identify what has worked, what has not worked, whether you have developed good financial habits, whether you are disciplined in implementing the plan. It is like looking yourself in the mirror and detect any blemishes to get rid of. You want to have a close look, be honest with yourself. Monthly budget On a monthly basis, typically at the end of the month or the beginning of the following month, check whether you are within your monthly budget. Did you overspend or underspend? What categories did you overspend, and the reasons? Were are able to save money at the end of the money? If you use a budgeting app on your smartphone, you probably can figure these out quickly. Jot down your thoughts in your (digital) diary or notes app. Think about how you can improve your spending, and write it down. Are there credit card instalments or personal loan instalments coming off your bank account? These typically have high interest rates that suck money out of you. Prioritise to pay off the full balances quickly. Are there monthly debits going off you bank account that you don't even know what they are? Check with you banker. Small debits add up, chewing your money away. Do you subscribe to DSTV, Showmax, Netflix and Amazon Prime Video? Do you need all these? Can you cut down to two, or even one? Do you have all these small policies debiting a few hundred rands from your bank account? Is it better to consolidate? Are you paying multiple funeral policies? Speak to a qualified Financial Planner to review all your policies, to see whether you should consolidate and save some money. Short-term and Long-term goals You should review your progress, at least annually. If you work with a financial advisor, schedule a time that is convenient for both of you. The review session is normally one to two hours, depending on how complex your financial affairs are. Otherwise, I have found the good time to review would be the end of a calendar year, the beginning of a year, or the middle of a year (June/July). They tend to coincide with the school holidays, when you may have some breathing space, some downtime, to relax, to refocus and strategise. Go through your short-term goals, your "quick wins" one by one. Tick off the ones you have achieved, pat yourself on the back. For the ones in progress, are they on track? For the goals you didn't achieve, what are the reasons? Some things may be within your control, some may be out of your control. For example, you might have planned a year-end holiday in Mauritius, and you have saved up for it. However due to the COVID-19 pandemic, and the latest new Omicron variant, Mauritius has re-introduced travel bans, and you could no longer take the family to Mauritius for a holiday. Instead, you had to change to local destinations such as Cape Town or Kruger National Park, or worse still, because of the increasing number of infections, you decided to stay put and stay home. We plan, and plan for the best to happen. But we must also be aware of the environment we are in, and there are many things outside of our control. Recognise them, be pragmatic. Focus on the things we can control. Write down your thoughts in your (digital) diary. Go through your long-term goals, one by one. Goals like long-term savings, child education fund, retirement, emigration, financial freedom. What progress did you make? Was it good, little or no progress? What caused you not to progress as planned? Changing jobs, poor business environment, load shedding, financial markets, your own behaviour and habits? What can you do to improve? What help do you need? What type of people can help you, e.g. life coach, business coach, financial advisor, accountant, IT specialist, mentor? How do you go about building the team around you, to support you? Write down your thoughts and action items in your (digital) diary. Implement the action items. If you do the reviews month-in, month-out, year-in, year-out, I am sure you will count your progress, achievements big and small, and be thankful of blessings received, and the advisors that have helped you along the way. Epilogue Twelve months, twelve articles on 11 Steps to Financial Freedom! Thank you for walking this journey with me, as we go through another tough year during the COVID-19 pandemic. Importantly, these are the steps I have followed to realise my financial freedom, and I have advised all my clients to follow. I hope you have found some of these insights helpful. If you have any testimonial, if you have any comments, questions or suggestions, please write to me on kyeh@daberistic.com. I don't proclaim to have all the answers, your comments and suggestions help us all improve on the process. Do follow us on Facebook, our company's Daberistic Financial Services page, and Instagram @daberisticw, for regular ideas and inspirations on personal finance, wealth and journey to financial freedom. May you be blessed with life, health and wealth. Here's to a Merry Christmas and a prosperous 2022! Kevin Yeh, CFP®  Last month I talked about Step 2 - Do Not Spend More Than You Earn. Let's continue with Step 3 - Do Not Take On Credit.

South Africa is a westernised economy, its financial system is modelled on the European and American credit system. If you have a steady income and a good credit score, it is easy for you to get credit. Credit is generally defined as a contractual agreement in which a borrower receives something of value now and agrees to repay the lender at a later date—generally with interest. Simply put, when you buy something now and pay it later, you are using credit. Examples are when you use your credit card to buy furniture and TV and put it on budget over 12 months. Based on your income and good credit score, the banks will want you to apply for credit card and give you a credit limit. As you manage the card well, pay the amount due in time, and your income rises, the banks determine that you are creditworthy and increase your credit limit. The banks advertise that the advantage of a credit card is you can get 55 days free of interest, that is the maximum interest-free period you can get. When you receive your monthly credit card statement (by now most banks send the statements electronically), you need to pay attention to: credit limit - the amount granted to you by the bank closing balance - the amount you owe on the credit card at statement date minimum amount due - the minimum amount you need to pay the bank payment date - the date by which you need the pay the bank It is very important to note: IF YOU DON"T PAY THE FULL BALANCE DUE BY THE PAYMENT DATE, YOU WILL PAY INTEREST Many clients I have consulted don't understand this, and they think it's OK to pay interest on their credit card, as they only pay the minimum amount due. But this is not OK! This is poor financial behaviour. Financially smart people understand how credit cards work. They use credit cards to their advantage. They buy things on credit. They pay the full closing balance on or before the Payment Date. They don't pay interest on their credit cards. You need to inspect your credit card statements for the last three to six months. If you pay interest every month, then you need to reset. Reduce or stop spending using your credit card, work on paying off the full balance. Once you have done that, then you get into the habit of paying the full balance by the payment date every month. Set up a reminder or have an automatic debit order to settle the balance. Remember, the amount you owe on your credit card, to you it is credit card debt. To the bank it is credit card asset. It is an asset because they earn interest from you. Currently the banks charge you between 12% to 18% interest on your credit card debt. That's a lot of interest to pay! You don't even earn this kind of return on your long-term investments. Stop giving more money to the bank than you need to! Rather keep that money in your pocket. I have some rules for credit cards, which I advise my clients to follow:

Don't take on credit, it means you get into debt. Apart from financing high-value items such as a property, a car, business or study loans, you should not take on credit. Morningstar has published this excellent article on Slow and Steady Wins the Race - It Is OK to Build the Wealth Slowly. It talks about the importance of perseverance, patience and compound interest in building wealth. Building wealth is a journey, it is like a marathon. It is not a 100m sprint. We share with the readers here. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|