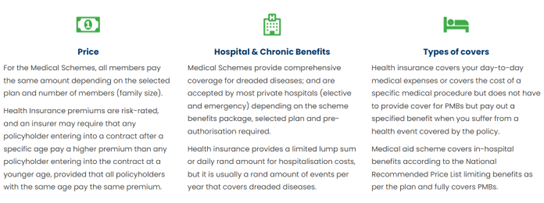

More and more South Africans are experiencing financial problems leading them to try to cut costs and thus leading them to cancel their medical aid. As Daberistic we advise you that you do not have to stay without cover and there are other affordable solutions that will give you peace of mind. We share below about Health Insurance. What is Health insurance? Is a type of insurance coverage that pays for medical, surgical, and sometimes dental expenses incurred by the insured. Health insurance can reimburse the insured for expenses incurred from illness or injury, or pay the care provider directly. The benefit could either be a fixed sum of money per day or a maximum lump sum of money which is paid if a specified health event takes place (e.g. a specific health condition develops). Health insurance policies usually only pay out if certain specific health-related events happen and do not pay your medical expenses as a medical aid scheme would. Unique Principles 1. Limitations and prohibitions: A hospitalisation policy may not cover medical expenses. A health policy, other than a Gap cover policy, may not require the policyholder or insured person to be a member of a medical aid scheme. 2. Waiting period: A hospitalisation policy, gap cover policy and HIV/Aids, tuberculosis and malaria testing and treatment policy may provide for a – general waiting period of up to 3 months; and A condition-specific waiting period of up to 12 months. An insurer may not impose a condition-specific waiting period on a policyholder’s health insurance policy if that policyholder, for at least 90 days before entering into a health policy with the insurer, had a health policy with materially similar benefits and had completed the condition-specific waiting period in respect of that health policy. Where a waiting period of a policyholder under a previous health policy had not expired at the time that that policyholder enters into a new health policy with materially similar benefits, the insurer may only impose a waiting period equalling the unexpired part of the waiting period in respect of that previous policy. 3. Disclosure requirements: A hospitalisation policy, gap cover policy and HIV/Aids, tuberculosis and malaria testing and treatment policy may not create the impression that it is a substitute for medical aid scheme membership. A hospitalisation policy may not create the impression that it covers you for medical expenses. Three areas where Medical Aid Schemes and Health Insurance differ:  If you would like to apply for health insurance, contact Jo in our Health department tel: (011)658-1333 email: service@daberistic.com

Source: CMS

0 Comments

At the conclusion of its Monetary Policy Committee (MPC) in May, the South African Reserve Bank (SARB) increased its repo rate by 50 bps to 8.25%, underlining its inflation-fighting credentials. Although consumer inflation is expected to slow from its current level of 6.8%, the bank has lifted its year-ahead headline CPI forecast for Q2 2024 to 5.3% from 5.0% previously. It also indicated that the inflation risk is skewed to the upside. This leaves the door open for possible future interest rate hikes.

Two of the most significant risks to the interest rate outlook are rand moves and decisions taken in upcoming US Federal Open Market Committee (FOMC) meetings. Recent developments in the currency market are especially important. Rand depreciation can feed through into significant so-called second-round effects when the initial impact of higher import prices on inflation becomes amplified by higher production costs and/or wage demands. It is concerning that the bank warns: “Given upside inflation risks, larger domestic and external financing needs, and load shedding, further currency weakness appears likely”. The bank responds to the inflationary impact of rand weakness, rather than movements in the exchange rate itself. However, the situation is worrying, especially since load shedding is driving up the cost of doing business, while food price inflation is expected to remain high. In this environment, second-round impacts could be significant. At the same time, US Federal Reserve decisions are important, as demonstrated by the tightening of global financial conditions. This is partly responsible for softer foreign capital inflows into SA. Although stresses in the US banking system are likely to persuade the FOMC to keep interest rates on hold when it meets in June 2023, the ongoing tightness of the labour market and the relative stickiness of core CPI may result in another US interest rate hike in July 2023. SA has not fared well against this backdrop. As illustrated this month, the underlying problem is a balance of payments constraint. Net foreign capital inflows, deterred by low prospective returns, policy uncertainty and lack of infrastructure, have been insufficient to fund the current account deficit. This implies macroeconomic policy must be tightened. SA’s pressing socio-economic problems and the failure of specific state-owned companies have precluded aggressive fiscal policy tightening. This has shifted the responsibility onto the SARB to do the “heavy lifting”. It is by no means certain that SA has reached the top of the interest rate hiking cycle. Much will depend on developments in the rand and its potential inflation implications, while the SARB is also keen to see elevated inflation expectations moderate. However, the currency has depreciated significantly, while the interest rate hiking cycle is far advanced. At some point, this is likely to have the desired effect. As 2023 progresses, the focus may shift from interest rate worries to economic growth worries. Historically, the interest rate hiking cycle has typically ended once it is clear inflation has peaked and is heading decisively towards the intended target. Based on current information, we believe SA is approaching that point. Source: By Arthur Kamp, chief economist at Sanlam Investments Innovations and Challenges New tools for investing—such as online trading platforms, cryptocurrency, sustainability, private markets, and separately managed accounts with personalized direct indexing—have energized the investing landscape, garnering interest from both the technology and finance industries. With this new excitement, however, many may have failed to consider how investors are managing this onslaught of new investing tools and to what degree these new capabilities promote investor success. In other words, we need to understand the relationship between investors, their long-term financial goals, and new investing tools. For our investors investing in Morningstar Managed Portfolios, click below to access the latest performance snapshot, market commentary and market performance summary:

Morningstar SA Managed Portfolios Morningstar Global Managed Portfolios (USD) Market Commentary - SA and Global Market Performance Summary - SA and Global Source: Morningstar The tax filing season for individual non-provisional taxpayers will start on 7th July 20223. We would like to remind you to submit your tax return in good time. According to SARS official media release: Here are the dates and criteria for the 2023 Filing Season: Individual taxpayers (non-provisional): 7 July 2023 @ 20:00 to 23 October 2023 Provisional taxpayers: 7 July 2023 @ 20:00 to 24 January 2024 What’s new? Pre-population of ITR12 Third Party Data in preparation for the opening of Filing Season 2023: Please be advised that in preparation for the opening of the Personal Income Tax Filing Season in July 2023, between the period of 2 June 2023 until the opening of Filing Season, there is a possibility that the prepopulated data reflecting within your Personal Income Tax or Provisional Tax returns requested via eFiling, the SARS Mobi application or via a SARS Branch Office during this period, will pre-populate but may not be comprehensive until Filing Season is officially opened to the public. Have you received an Auto Assessment? Between 1 July and 7 July 2023, taxpayers will be notified by SMS or email if they were selected to receive an auto-assessment. Should you receive the SMS, the next step for you would be to review the auto-assessment on the SARS MobiApp or eFiling.

How is Auto Assessment different this year (2023) from last year (2022)? Last year you had 40 days to file a return if you were not happy with your auto-assessment, but this year we are giving you until the due date of 23 October 2023. If an auto-assessment has been issued after 23 October 2023 the 40 business days will start on the date of the notice of the assessment. What to prepare before filing starts?

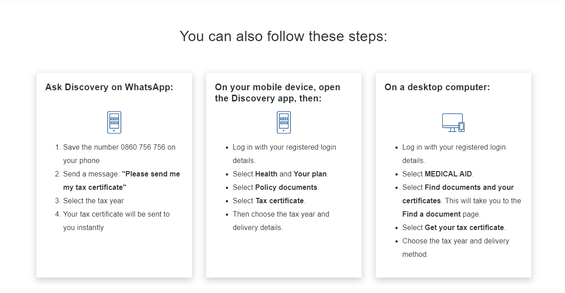

Source: SARS By now you should have received tax certificates from financial institutions in the months of May and June to assist with your tax filing. These include tax certificates from the medical aid, banks, life insurance companies and investment companies. Check your email inbox and junk folder, search for the keyword "tax certificate" to find relevant emails. Download the attached tax certificates in a folder on your local drive or cloud storage for tax filing. Discovery Health: The email from Discovery Health looks like the following: Tax CertificatesBy now you should have received tax certificates from financial institutions in the months of May and June to assist with your tax filing. These include tax certificates from the medical aid, banks, life insurance companies and investment companies. Check your email inbox and junk folder, search for the keyword "tax certificate" to find relevant emails. Download the tax certificates in a folder on your local drive or cloud storage for tax filing.   Allan Gray  To view and download your latest and historical tax certificates, log in to your secure online account at www.allangray.co.za and navigate to ‘Statements & documents’ >> ‘Tax certificates’.

If you have difficulties downloading your tax certificates, or require the service of a tax practitioner, email to service@daberistic.com and our team will gladly assist you. The failure of three US regional banks as well as the collapse of global investment bank Credit Suisse has sparked fears of a looming global banking crisis in the first half of the year. Concerns around a run on bank deposits and a contraction in lending have contributed to relatively widespread pressure on global banking stocks as investors consider the risk of contagion spreading across the sector. South African banks have also come under pressure as investors have generally sold down holdings of perceived risk assets during a turbulent time for capital markets. A systemic banking shock would have especially adverse implications for markets with the experience of the 2008 financial crisis providing a gloomy backdrop for a potential fallout. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|