|

Do you have a Discovery bank account? You can appoint us as your personal banking advisor. We cannot view your bank account's confidential information, but you can share your Discovery Bank mobile app with us online or in person, and we can show you how to navigate the app better and understand its features.

We can assist you with: - Upgrading credit cards or banking packages - Understanding and improving your credit rating - Earning more Discovery Miles rewards - Better use of Discovery Miles for shopping - Opening a foreign currency account - Applying for a home loan (coming soon). If you do not have a Discovery bank account or credit card yet, we can also provide advice and help you open an account. If needed, please email us at service@daberistic.com or call 083-633-4671, 076-200-5488.

0 Comments

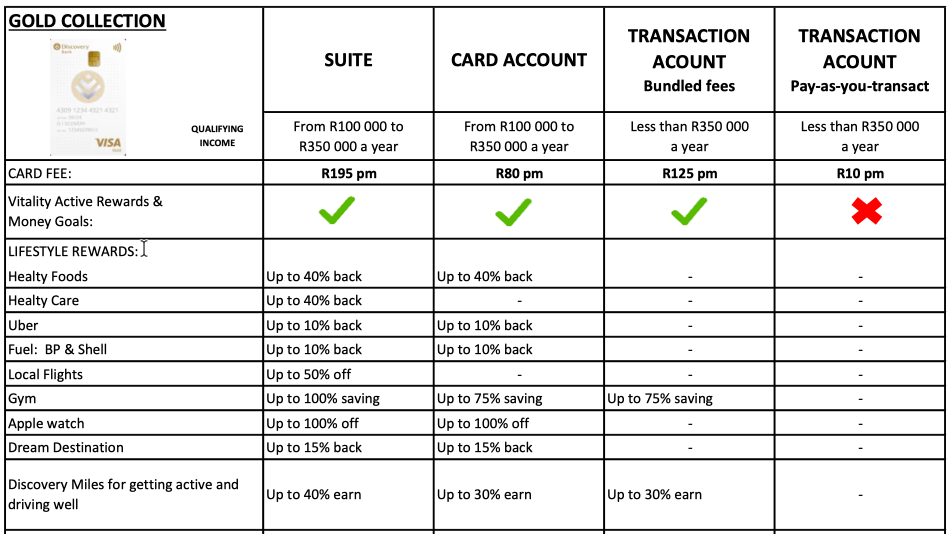

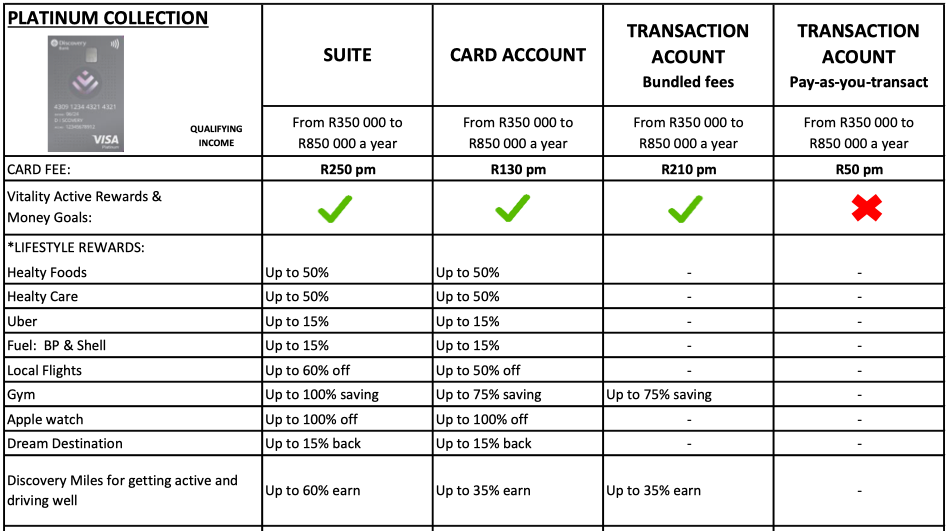

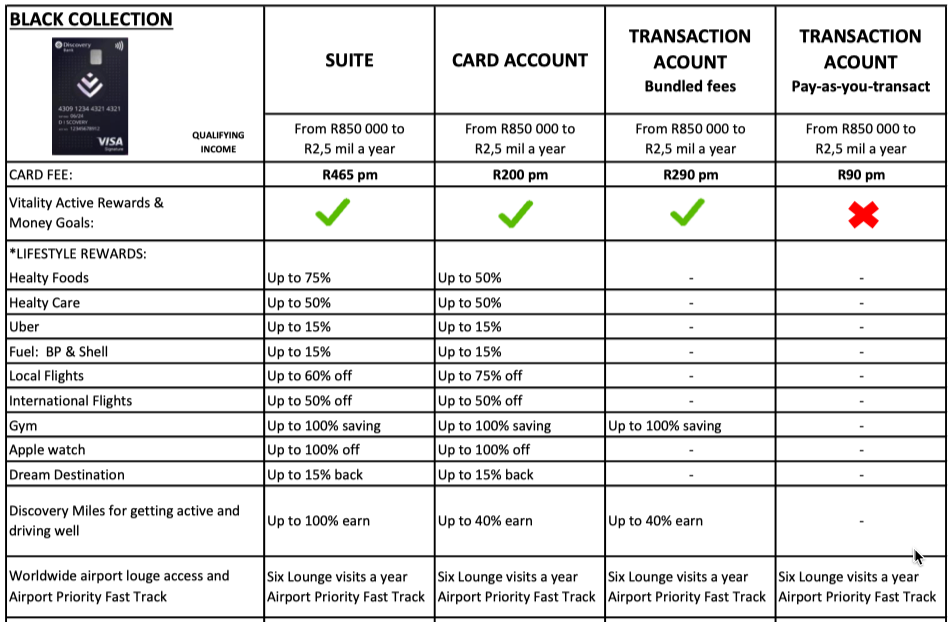

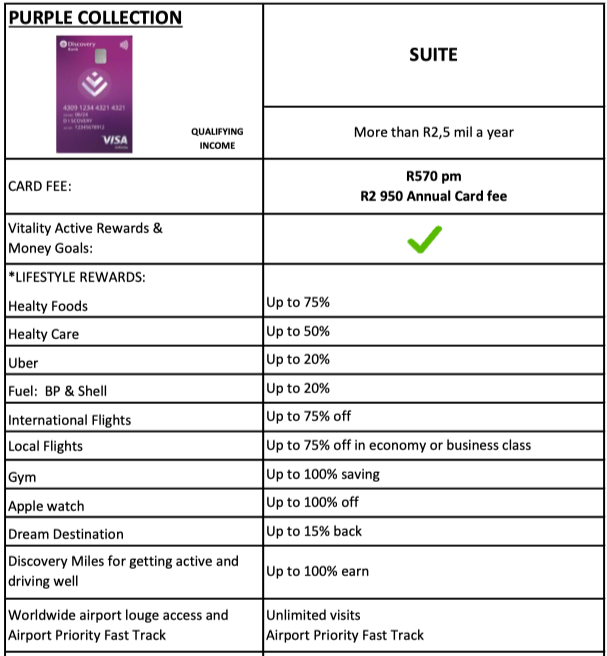

We as an accredited financial advisor can assist you in opening a Discovery Bank account. So which Discovery Bank product is right for you? Discovery Bank in South Africa is the banking brand of Discovery Group, a well-known South African-founded financial services organisation. It was established with the approval of the South African Reserve Bank in 2016. In the past three years, it has been actively growing its mass affluent client base, and now has more than 1 million customers. Here we explain the prerequisites for applying for a Discovery Bank account, as well as the key features of Discovery Bank products. The advantages of Discovery Bank Discovery Bank is a digital bank that focuses on the use of user-friendly technology and powerful security features, allowing customers to safely operate various banking and financial functions on their mobile apps, including: - Checking account balances - Opening a new savings account - Opening a new fixed deposit account - Opening foreign exchange accounts (USD, GBP, EUR) - Opening tax-free savings account - Earn Discovery Miles - View financial portfolio summary on all products you have with Discovery, including Life, Invest, Health and Insure. Discovery Bank is a financial behavioural bank, using gamification to help customers improve financial discipline and financial wellness in the following five areas: savings, investment, real estate, retirement, and debt. If the customer closes all five rings, he will reach the Diamond Vitality Money status, enjoying the best interest rates on positive balances and deposits, and earn the most Discovery miles. Discovery Miles is a virtual currency that can be used to shop online, buy airline tickets, exchange for coffee or game points. Discovery Bank gives interest on account balances. WIth the traditional Big Four banks, there is no interest paid on the positive balance in the transaction account or cheque account. Discovery Bank disrupts the market and allows customers to earn interest on the positive balances of the credit card or transaction account. This gives more money to customers. Disadvantages of Discovery Bank There are no physical branches, and all transactions must be performed on mobile phone app or on the website by customers. If you encounter any problems, you must contact the customer service centre of the bank. Prerequisites for applying for a Discovery Bank account - Customers are already familiar with using the mobile apps of mainstream South African banks such as FNB and Standard Bank to view accounts, download statements, and transfer funds. - Customer has a South African ID card or green ID book. - The client has an annual income of at least R100,000. - Proof of residential address (not older than three months) - Three-month bank account statements showing regular monthly income deposits at a bank. Discovery Bank Products Discovery Bank has four tiers, from Gold, Platinum, Black to the highest level Purple. Gold tier requires an annual income of R100,000 to R350,000. The products, monthly fees and benefits are as follows: Customers can choose to only open a transaction account, credit card account or package (Suite, including both transaction account and credit card).  Platinum tier requires an annual income of R350,000 to R850,000. The products, monthly fees and benefits are as follows: Customers can choose to only open a transaction account, credit card account or package (Suite, including both transaction account and credit card).  Black tier requires an annual income of R850,000 to R2,500,000. The products, monthly fees and benefits are as follows: Customers can choose to only open a transaction account, credit card account or package (Suite, including both transaction account and credit card). Clients have access to six airport lounge visits a year and Airport Priority Fast Track.  Purple tier requires an annual income of more than R2.5 million. The package, monthly fees and benefits are as follows: Customers can enjoy unlimited airport lounge visits and Airport Priority Fast Track.  If you are interested in opening a Discovery Bank account, please email service@daberistic.com with your name and cell number.

It has been widely published that the representation of female-run funds, financial advisors and investment teams over the past decade has been relatively consistent in that women continue to be underrepresented. This is, of course, a serious issue that deserves attention and we need to work harder to continue to attract women to the financial industry.

According to Morningstar’s research, only around 11% of South African fund managers are women. And in the UK, Morningstar data shows there are more funds run by men named Dave than there are female fund managers in total. Of 1,496 UK-listed open-ended funds, 108 are run by managers named David or Dave – equivalent to 7.2% of funds. Meanwhile, just 105 funds in total have a woman at the helm. It’s a stark reminder of the lack of diversity across the fund industry. Improving diversity will take time. We need to start paying more attention to the industry’s graduate recruitment, and the perception of the financial industry. Firms need to look at how they can support the recruitment and retention of more women. There is an industry perception that isn’t landing with young women, as the number of applications for junior roles remains low. Long-term investing is far from the macho image portrayed in movies, and firms should look at ways they can help to change this, starting with job descriptions and with females in the industry sharing their success stories. I spoke to a few of the female advisers that partner with Morningstar Investment Management South Africa to share their experience of the financial industry. The feedback received, painted a very interesting picture. The most prominent being, how rewarding it is for women to work in the financial industry. I’ve highlighted a few key takeaways below, of why more women should consider working in the financial industry - Financial planning and advice enable you to make a difference, whilst earning a living. Being a financial adviser enables you to make a meaningful impact on the lives of your clients. By helping your clients to understand how to work with their money and make their money work for them, you can truly have a positive impact on their lives. If you are someone that wants to pay the bills but do good at the same time, financial planning and advice is a great career option. The great part about finance is, the numbers don’t lie – when you see your client celebrating a savings goal that had been reached, it’s very rewarding to know you helped them reach that goal. “I joined the industry wanting to make a meaningful impact on people’s lives. Something that would enrich my soul whilst earning a living. I wanted to help people realise that through taking the time to understand their relationship with money, they could see money as their enabler, and thus something that they could control, rather than letting their money control them.” – Tessa Lefrère, Certified Financial Planner®, Resolute Wealth Management. It is both pencil skirts and sneakers Contrary to popular belief, working in finance can offer the flexibility of hours, being your own boss, owning your own business, managing your own time and engaging with people regularly. The world of finance isn’t only filled with women doing presentations in tight pencil skirts and high heels. The fantastic part is, that if you would like to do that, you most certainly can! But, if you would prefer to rather ditch the heels for a pair of sneakers, that’s perfectly fine as well. There is room for individualism and to do things your own way. “I also enjoy the fact that I have my own business, I’m my own boss and I manage my own diary. As a mother, this is priceless.” - Cilma Sorour, Certified Financial Planner®, Alchemy Financial Solutions If you are a people’s person – working in finance is a great career choice. Yes, having a keen interest in markets, the economy and investments is most certainly a massive plus. However, the female advisers I spoke with, said that working with people is one of the aspects of the industry they enjoy the most. In addition, being invested and caring about their clients is their most valuable and differentiating quality as an adviser. “I work hard at making sure my clients feel that they have been heard but most of all building a lifelong relationship and friendship that is also professional.” – Stephanie Bakhuis, Certified Financial Planner®, Chartered Wealth “Over the years I kept choosing to work with people more than portfolios and hence I’m now in the financial partnership role with our clients. However, I also love the complexity and the challenges of the investment environment.” – Sunél Veldtman CFA®, CFP®, CEO of Foundation Family Wealth Females in finance support each other It might be known for being male dominant, but the women in the financial industry are proud to support each other, empower one another and there are several “Women in finance” groups that aim to facilitate growth, partnership and collaboration between women in the industry. "Apart from helping my clients, I spend a large part of my time teaching and sharing this knowledge with other financial planners so that they too are upskilled to help their clients with their money relationship. I view this as a value-add to clients in the financial planning industry." - Kim Potgieter, Marketing and Life Planning Director, Certified Financial Planner®, Chartered Wealth Whatever you decide to do in life – let it be to save first! When we asked our female financial advisers, what advice they would give their 20 year old self, the standout answer was to save, save and save some more. "Choose to understand your money; make friends with it, rather than fear it. By empowering yourself in your 20’s, you cannot begin to imagine the life you’re setting up for yourself to live on your terms, in your time." – Tessa Lefrère, Certified Financial Planner®, Resolute Wealth Management. In closing At Morningstar Investment Management South Africa we strive for a diverse team. When it comes to gender, our team in South Africa is made up of more than 50% women. The advantages of greater institutional diversity are well researched and documented, and the local investment community should be doing more to attract young women into the industry. “I love being part of such a diverse team of individuals. Everyone brings something unique to the table, which is really inspiring.” – Abigail Wilson, Customer Success Manager, Morningstar Investment Management South Africa A growing body of research suggests that the presence of women on corporate boards and in the C-suite is linked to superior financial performance – for example, Credit Suisse’s CS Gender 3000 report. We also need to think more broadly about diversity and as such especially the diversity of thought. We often view diversity through a gender or race lens, but true diversity is an expression of different cultures, thoughts, energy and ideas. If the COVID-19 pandemic has shown us anything, it’s that what we thought was ‘normal’ and ‘unchangeable’ is, in fact, hugely open to change, in the most positive way. At Morningstar, we will continue to highlight trends in the fund manager industry to spark conversation and dialogue, especially as it relates to matters of diversity. Source: Morningstar Written by: Victoria Reuvers  Today is day 20 of the lockdown announced by President Ramaphosa. As we are in the 3rd week of lockdown, many people and businesses are affected, as people are not working and businesses are closed to operations. This leads to lost revenue and income. As a result, individuals and businesses are struggling financially during and beyond the lockdown period. In response to the government's call to action, most financial institutions have announced measures to provide financial relief. As the situation evolves from day to day, financial institutions continue to work with the government to reassess the situation, and further relief measures can be expected.

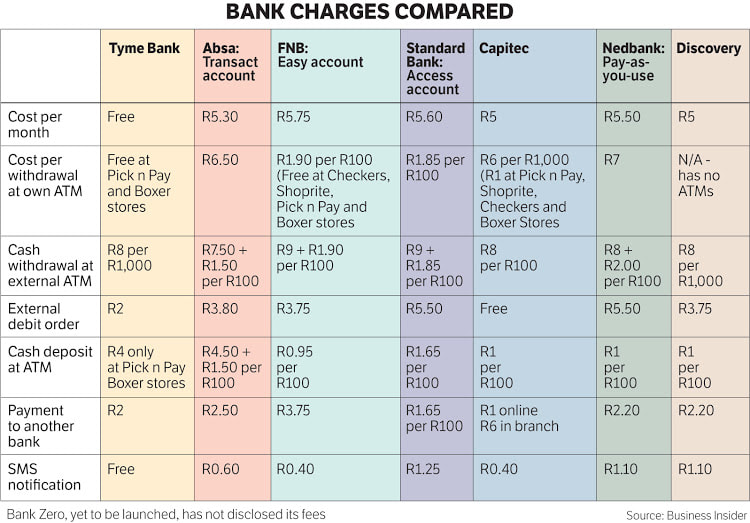

We have gathered below links to financial relief measures provided by financial institutions, we hope these can assist you during this difficult period. Note that the information may not be complete or the most up to date. Please speak to the bank, the insurance company, your broker or financial advisor to confirm. Banks Covid-19 debt assistance: https://www.nedbank.co.za/content/nedbank/desktop/gt/en/personal/covid-19-debt-relief.html?cmpid=dis:ned:ret:debtrelief:banner:ned Nedbank's relief measures for individual and small-business clients, including information on payment holidays, the newly announced SA Future Trust Fund for SMMEs, and other Nedbank debt relief actions, can be found on https://www.nedbank.co.za/content/nedbank/desktop/gt/en/info/campaigns/nedbank-covid19-page.html Select 'Business' then 'Covid-19 Relief'. Nedbank remains committed to meeting your banking needs through this challenging period. Standard Bank: https://www.standardbank.co.za/southafrica/personal/campaigns/covid-19 FNB: https://www.fnb.co.za/press-office/index.html ABSA: https://www.absa.co.za/personal/covid-19/ Capitec: https://www.capitecbank.co.za/global-one/banking_during_the_covid_19_lockdown/ • If you're worried about your income or your ability to make your Capitec loan repayments, talk to us – we can help. To make a payment arrangement, dial 0860 66 77 18 to speak to an agent Life insurance companies (Do consult your financial advisor on the best option for your personal circumstances) Discovery Life discovery_premium_relief.pdf Option 1 – Premium relief option: Qualification rules: The premium payer must be self-employed, a business owner or an employee of such businesses facing severely reduced income themselves, in an industry that is not an essential service as defined in the Labour Relations Act. This applies to small and medium enterprises (SMEs) that meet the definition of a Small Enterprise in South Africa as per the Department of Small Business Development. The policy must have been in force for at least two years. The client must not have received a credit control letter in the past two years. The policy must have Comprehensive Integration with the PayBack benefit. At the moment, the policy's accumulated Surplus PayBack fund or Five-yearly PayBack fund has at least enough funds for two months’ worth of premiums. Policies that are in claim or have a claim registered that is being assessed do not qualify. Option 2 – Suspended cover option (Cover-pause): Qualification Rules: The premium payer must be self-employed, a business owner or an employee of such businesses facing severely reduced income themselves, in an industry that is not an essential service as defined in the Labour Relations Act. This applies to small and medium enterprises (SMEs) that meet the definition of a Small Enterprise in South Africa as per the Department of Small Business Development. The policy must have been in force for at least six months. The client must not have received a credit control letter in the past six months. Policies that are ceded (given as security for a loan) do not qualify. Policies that are in claim or have had claims submitted do not apply Option 3 – Underwriting-free servicing option: • A completed servicing quote is required (reduction) • Removal of benefits will not form part of the offer when up-servicing after three months, free of underwriting Important: • The form for options 1 and 2 must be completed by the policy owner and sent from his or her email address on record. A policy owner is able to contact the Call Centre, be verified and update their email address – 0860 00 54 33. Old Mutual helping_your_customers_during_lockdown_-_rsa_2.pdf Sanlam Liberty life insurance policies riskpremiumbreak_final_.pdf Investment policies investmentpremiumbreak_1pager_.pdf Momentum momentum_myriad_covid19_ppo_information_leaflet.pdf momentum_myriad_covid19_ppo_faq.pdf PPS pps_option_1.png pps_option_2.png Short-term insurance companies Discovery Insure discovery_premium_relief.pdf Santam Premium relief is only available once a client has lapsed their premium. We support all actions being done with clients to restructure their existing cover and reduce their premiums such that they do not have to lapse their policies. In the past few months, three new banks have launched with a leaner, cheaper business model that will change the face of SA banking — TymeBank, Bank Zero and Discovery Bank. They are here to challenge the Big Four - ABSA, FNB, Nedbank and Standard Bank. The fifth largest bank, Capitec, started in 2001. It now has 11.4 million clients, acquired Mercantile Bank, with over 200,000 new clients opening new bank accounts a month. It also continues to develop its financial technologies. At the same time, Standard Bank the largest bank in South Africa announced it woule be closing 91 branches, affecting 1,200 employees. Many face retrenchments, many will be re-trained to be deployed other departments of the bank. Standard Bank points out that its clients use more of its services online via mobile phones, while having less visits to branches. We witness the waves of technology tsunami hitting the banking industry. The three new banks have very similar focus: digital, with no physical branches. Will they succeed? Will they threaten the Big Four banks? Who are their backers?  TymeBank is controlled by African Rainbow Capital (ARC), an investment company controlled by the eclectic Ubuntu-Botho group headed by Patrice Motsepe. As the Forbes rich list has it, Motsepe is one of the 1,000 wealthiest individuals in the world, with a fortune of $2.4bn. Before it was bought by Motsepe’s company, TymeBank was owned by the Commonwealth Bank of Australia (CBA), one of the world’s top 10 retail banks.  As for Bank Zero, the most entrepreneurially based of the three, it shows how far the Reserve Bank has come that it got the green light. Bank Zero is run by a maverick group of former FNB executives, most of them with strong technology backgrounds, with a few family and friends as shareholders. The chair and figurehead is the former FNB boss Michael Jordaan, based in Stellenbosch. Somewhat ironically, Jordaan is Motsepe’s partner in the data-only telecom network Rain. The Bank Zero CEO, Yatin Narsai (former head of FNB retail), runs the business day-to-day from Bryanston. Discussing the rationale for the bank in an interview with the FM, Narsai says SA ranks among the five countries with the highest bank fees in the world. "This is intolerable in such an unequal society, but then the rest of the bottom five were similarly unequal countries in Latin America," he says. No-one can ignore the competitive threat of cheap banking. Narsai says he personally will save R2,000 a month from his personal and business accounts, when Bank Zero goes live and he can move accounts. "Low fees will become the new normal and I hope that penalty fees will disappear altogether," he says.  Discovery Bank is part of the wider group run by CEO Adrian Gore, which began as a health-care company in 1993. Discovery boasts Remgro associate Rand Merchant Investments (RMI) as its anchor shareholder. Discovery Bank is launching a new business model, based on its Vitality principles. If a client can manage his personal finance and credit well, his money in the account will receive a higher interest rate, while he pays lower interest rate on his home loans. Discovery Bank is hoping to use this business model to incentivise clients to modify and improve their financial habits. The question, however, is what the existing big four banks — FNB, Standard Bank, Absa and Nedbank — will do to counter the threat. "The big banks ignored Capitec in the early 2000s, and lost considerable market share. I am sure they will not make the same mistake again." Below is a comparison of bank charges (Source: Business Insider)  Source: Businesslive

|

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|