You may have heard of a return on an investment, but have you heard of an investment measure called the internal rate of return (IRR)?

The return on investment (ROI) – sometimes called the rate of return (ROR) – is the percentage by which an investment has increased or decreased over a certain period. By contrast, the IRR measures the actual return on an investor’s money in a portfolio. The IRR calculation takes into account all fees, the investment term, and additional investments and withdrawals, and calculates the growth of the investment in a meaningful way. This enables investors to determine whether their portfolio is on track to achieve the return they need to maintain their standard of living. The IRR calculation shows a portfolio’s return on an annualised (per year) basis. If, for example, you had R100 on January 1 and R110 on December 31, and you made no deposits or withdrawals between those two dates, your IRR would be 10% for the period. If, however, you made monthly deposits of R1 (or R12 in total) and your portfolio was worth R110 on December 31, you would have a negative IRR of –1.9%. After investing a total of R112, you would have less money (R110) than you invested. If, on the other hand, you withdrew R1 every month and you had R110 at the end of the year, your IRR would be 23.2%. Your cash flow during the year would have been R12, and you would have ended the year with an additional R10 in the investment. The IRR calculation is also referred to as the money-weighted return calculation. This is different from a traditional time-weighted return where we exclude any client-generated cash flow in and out of the portfolio and look only at the initial value (R100) and the final value (R110) and get a return of 10%, which ignores how much money had been added or withdrawn over the period. Although these are very simple examples, they illustrate the importance of knowing a portfolio’s IRR. In reality, additional variables, such as fees, are taken into account, thereby providing a more realistic picture of your return. Knowing your portfolio’s IRR is important, because it enables you to monitor whether you are progressing towards achieving your financial goals. It indicates the actual return, including cash flows in and out of your portfolio, over the period. By comparing the IRR to your required rate of return – the rate that your portfolio needs to achieve in order to meet your lifestyle requirements, for example, inflation plus 2% – you will be able to assess your progress towards your goal. Interestingly, two people may be invested in the same portfolio but have a different IRR, because their deposit and withdrawal patterns are different. Let’s say, for example, that the market increases 10% over the year, but it first goes through a valley, falling 5% in the middle of the year. If Investor A added to her portfolio while the market was in the valley, whereas Investor B made a withdrawal, it means that Investor A bought at a discount, while Investor B realised a loss. In this example the portfolios’ overall performance was the same, but their individual IRRs will be different. If, during a financial planning exercise, calculations show that you need an annual return of 3% above inflation to achieve your lifestyle objectives, the calculation assumes that, as long as the money is invested in your portfolio, it is earning 3% above inflation. The IRR calculation is the most appropriate formula for checking whether you are actually earning what your financial plan says you need. To get advise on investment options with a track record of good returns, please contact Kevin or Thato, email: invest@daberistic.com tel no: (011 658-1333) Source: Business day live

0 Comments

The Discovery Dollar Capital Plus Fund

Discovery Invest has just introduced a new structured fund, the Discovery Dollar Capital Plus Fund, which provides investors with exposure to the performance of the US and European equity markets in US Dollars. The Discovery Dollar Capital Plus Fund is based on a global portfolio comprising 30% S&P 500 and 70% Eurostoxx 50 indices, with a minimum return in US Dollars of 40%, if the return of the global portfolio is flat or positive at the end of five years. Some capital protection in US Dollars is provided for falls in the global portfolio of up to 30% during the five-year term. The Discovery Dollar Capital Plus Fund opened on Monday, 22 February 2016. This offer will expire when capacity runs out but will not be available later than 8 April 2016. Please see the Discovery Dollar Capital Plus Fund Factsheet for more information on this special offer. If you are interested in investing in this special offer, please speak to Kevin Yeh or Thato Merementsi to apply, email invest@daberistic.com, Tel 011-658-1333 or 083-633-4671. Introducing the R12/$1 Life Plan Limited Offer! Buy a Dollar Life Plan policy before 31 March 2016, and get a guaranteed exchange rate of R12/$1 on your premium for the next three years! In November 2014, Discovery Life launched the Dollar Life Plan, a first-to-market offshore life insurance policy that offers clients comprehensive risk protection in US dollars. With the Dollar Life Plan, clients can be sure that their risk protection will remain relevant in the long term, regardless of their changing lifestyle needs. Why offshore life insurance makes sense: 1. Sound long-term financial planning With an offshore life insurance policy, denominated in US dollars, clients are protected against the financial impact of a life-changing event – no matter where they may find themselves in the future. 2. Matching liabilities Many clients either have, or could in the future have, offshore liabilities such as a bond, children’s education costs or estate duty in a foreign country. Clients may also be impacted by a fluctuating rand, which typically results in an increase in the cost of goods and services available locally. Risk protection denominated in dollars is therefore critical to ensure that a client’s liabilities are fully matched. 3. Diversification Discovery Life provides an efficient vehicle for clients to supplement and diversify their retirement savings into offshore markets by allowing them to convert their future health and wellness into a tangible offshore financial asset. Clients can further supplement their retirement savings in dollars through three unique features:

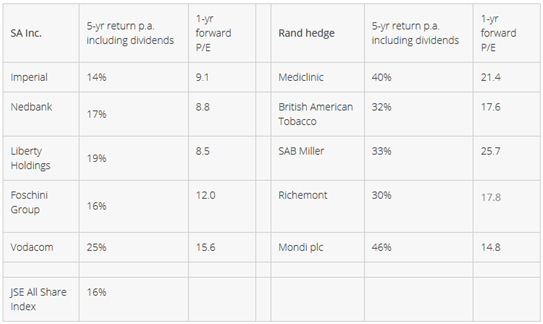

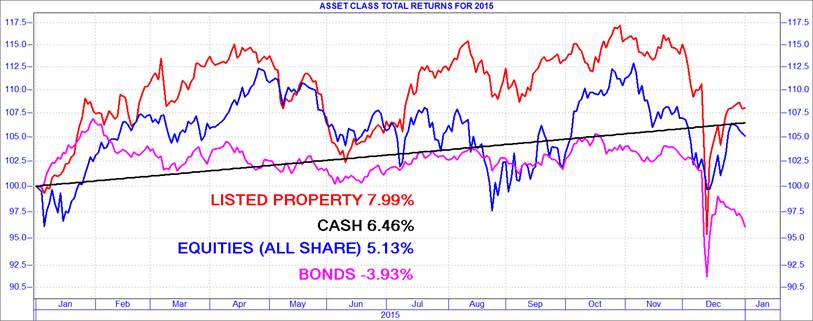

The minimum premium on the Dollar Life Plan has been reduced to $50 per month. This allows more clients to access the benefits of an offshore life insurance policy. You can increase the value of the rand with future certainty! For a limited time only, you will be able to pay the premiums on a new Dollar Life Plan at a substantially lower exchange rate than the market. You will be charged a premium based on a maximum exchange of R12/$1 for the first three years of their policy. This is provided that the exchange rate remains less than R20/$1 And if the exchange rate is higher than (or equal to) R20/$1, you will be charged a premium based on an exchange rate that is 20% less than the rest of the market. For more information, refer to this brochure and limited offer technical document. If you are interested in investing in this special offer, please speak to Kevin Yeh or Thato Merementsi to apply, email invest@daberistic.com, Tel 011-658-1333 or 083-633-4671. Source: Discovery  Website: www.daberistic.com Email: invest@daberistic.com Tel: 011 658 1333/1391 Dear Client / Business Associate Compliments of the News Season In our first edition of Investment Focus 2016 we plan ahead for the year on how to handle Investments, the article on Best direction for your investments in 2016 gives a guide on the market share and which markets to target as well as how the past five years’ share performance and current valuation of five well-run rand hedge companies versus five well-run SA Inc companies listed on the JSE. The one thing that is the hottest news in South Africa currently is, the New Tax law in regards to Tax incentives, with National Treasury encouraging us to save more for retirement by significantly increasing the tax incentives, the article More for the future you, less for the tax man is able to clearly explain the new Tax law. Our articles on 2015 Asset Class Total Returns - Listed Property the best performer in a volatile year, Prudential December Fund Fact Sheets help us look back at how markets performed in 2015. We hope that 2016 be a great year with great Financial return for all our Clients ….All the best Best direction for your investments in 2016 It may come as a surprise that, when viewed from a foreigner’s perspective, the JSE All-share index has not increased in US dollar terms since October 2007. In rand terms, the prices of local equities more than doubled over this period. It’s also worth noting that since 2011 our local market has underperformed the world’s developed markets, as measured by the MSCI World Index, by 119% as the rand depreciated from R6.61 to R14.20 per dollar. Given the rand weakness and superior performance by developed market equities, our clients regularly ask us whether they should take more money offshore. At our client roadshow in early 2011, we advised clients to shift their portfolios towards developed market shares given the over-valued rand at the time and relatively attractive valuations of these markets. This was met with some reluctance given that South African shares had outperformed developed markets by more than 500% over the previous decade. The superior economic growth prospects of emerging markets relative to the developed world were also emphasised, while many investors remembered the painful consequences of moving money offshore at the worst possible time after the rand collapsed in 2001. Recent experiences and performances influence investor sentiment, but our investment philosophy takes us back to valuation/price as the primary consideration for investment decisions, while taking account of the prevailing trends and perspectives in the market. In line with what we have advocated since 2011, our asset allocation portfolios have invested the maximum weight in offshore markets that prudential legislation allows. In our equity selection, we have tilted our portfolios towards ‘rand-hedge’ companies that derive the majority of their earnings offshore and away from so-called SA Inc companies whose fortunes depend on the domestic economy. This has benefited portfolio performance, but we continuously reassess our positioning. The table below shows the past five years’ share performance and current valuation of five well-run rand hedge companies versus five well-run SA Inc companies listed on the JSE.  Click here to read more Please contact Kevin or Thato, email: invest@daberistic.com, if you have any queries about investments Source: Finance24 More for the future you, less for the tax man The tides are changing in the retirement savings space, with National Treasury encouraging us to save more for retirement by significantly increasing the tax incentives. This is one of several important changes that will go ahead from March this year, now that the President has approved the Taxation Laws Amendment Bill, 2015, which was passed by both Houses of Parliament at the end of last year. Gifts from SARS The wait is over for retirement fund members, who will enjoy increased tax deductions from their contributions to retirement funds. This includes provident funds, for which members were not previously able to claim a deduction. The tax deduction of up to 27.5% of the greater of taxable income or employment income, subject to an annual ceiling of R350 000, will come into effect. Another change is that employer contributions to occupational pension and provident funds will be included in the gross income of employees as a fringe benefit. This means that employees will be able to treat these contributions as their own when calculating their tax deductions. These deductions are subject to the limits mentioned above. You will have to buy an income-providing product…Retirement funds will also be aligned, ironing out some of the differences between the different products. One of the key changes is around ‘annuitisation’ – the process of converting retirement savings into a stream of future income. From 1 March, provident fund members, like retirement annuity and pension fund members, will only be allowed to take one-third of their retirement savings as cash and they will have to use the rest of their nest egg to buy a product that pays them an income during retirement. “Treasury has stressed that vested rights will be protected –i.e. the new rules will not apply to historic savings or to growth on those contributions.” …unless you are about to turn 55…If a provident fund member is 55 or older on 1 March, the new requirement will not apply. Any accumulated retirement savings as at 1 March, as well as new contributions and growth after 1 March, can still be taken as a cash lump sumat retirement. …or you have saved under R247 500 Members with a retirement benefit at retirement less thanor equal to R247 500 will be allowed to withdraw the entireamount without the need to purchase an annuity, as of March.This is an increase on the current value of R75 000. Click here to read more Please contact Kevin or Thato, email: invest@daberistic.com, if you have any queries about retirement funds or Allen Gray offerings Source: Allan Gray 2015 Asset Class Total Returns - Listed Property the best performer in a volatile year SA listed property was the best performer with a total return (income and capital) of 7.99% in ZAR in 2015  Global Listed Property (Developed Markets)

Please contact Kevin or Thato, email: invest@daberistic.com, if you have any queries about any investing Source: I-Net Bridge Prudential December fund fact sheets In December the US Federal Reserve finally raised interest rates for the first time since the 2007 Financial Crisis amid supportive economic data, easing some of the uncertainty hanging over global investors and pushing the US dollar still stronger. Chinese economic data also improved, partly relieving another source of uncertainty. However, global growth prospects, particularly emerging markets, continued to be revised downward, driving commodity prices, EM currencies and EM financial markets weaker (Brent crude lose 17.2% during the month). Assets continued to flow back to the US from riskier destinations. Most equity markets lost ground, as did bonds. Developed market equities produced a total return of -1.7% (MSCI World Free Index) and the MSCI Emerging Markets Index fell 2.2%. Global bonds were largely flat as the Barclays Global Aggregate Bond Index (US$) returned 0.6%, while precious metal prices fell: gold was down 0.34%, platinum -15.9% and palladium -20.5% (all in US dollars). South African bonds, listed property and the rand fell sharply amid the global environment and were all punished by "Nene-gate" on 10 and 11 December. Equities also lost ground as financial shares were hard-hit. The average equity fund returned -2.2% for the month, while the average high equity balanced fund delivered -0.2% (according to Morningstar, using ASISA categories). Multi-asset low-equity funds averaged -0.1%, and multi-asset income funds produced -0.3% on average. SA equities were lower in December in line with other developing markets: the FTSE/JSE All Share Index posted a total return of -1.7%. The All Bond Index suffered a 6.7% loss, and SA listed property returned -6.1%. Inflation-linked bonds were down 1.8%, while cash returned 0.5%. Over the month the rand weakened by 6.9% against the US dollar, by 5.0% against the pound sterling, and by 9.5% against the euro, making offshore assets the best performing for December. Prudential High Yield Bond Fund – The fund has returned -5.0% over 1 year and 1.4% over 3 years. This compares to -3.9% for the All Bond Index over 1 year. Long-dated bond yields have become even more attractive in the wake of December's weakness, rising to over 10%, so that the fund remains overweight duration. Please contact Kevin or Thato, email: invest@daberistic.com, for any queries about Prudential investments Source: Prudential Daberistic contacts details Kindly note the following to ensure you get the correct person to assist you with your insurance and investment queries. Life insurance and investments: Kevin Yeh, Thato Merementsi, Nicole Smith Tel 011 658 1333, email life@daberistic.com Medical aid / gap cover:Namhla Zwane,Sophie SuTel 011 658 1333, email health@daberistic.com Short-term insurance (Personal and Business): Thomas Mooke, Calvin Yen, Tel 011 658 1333, email shortterm@daberistic.com Retirement funds: Kevin Yeh, Tel 011 658 1333, email employeebenefits@daberistic.com Tax, Accountancy and Auditors: Su-Lan Chen or Su-Chin Chen, Tel 011 658 1333, email finance@daberistic.com 24-hour emergency cellphone number: 076 200 5488. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|