|

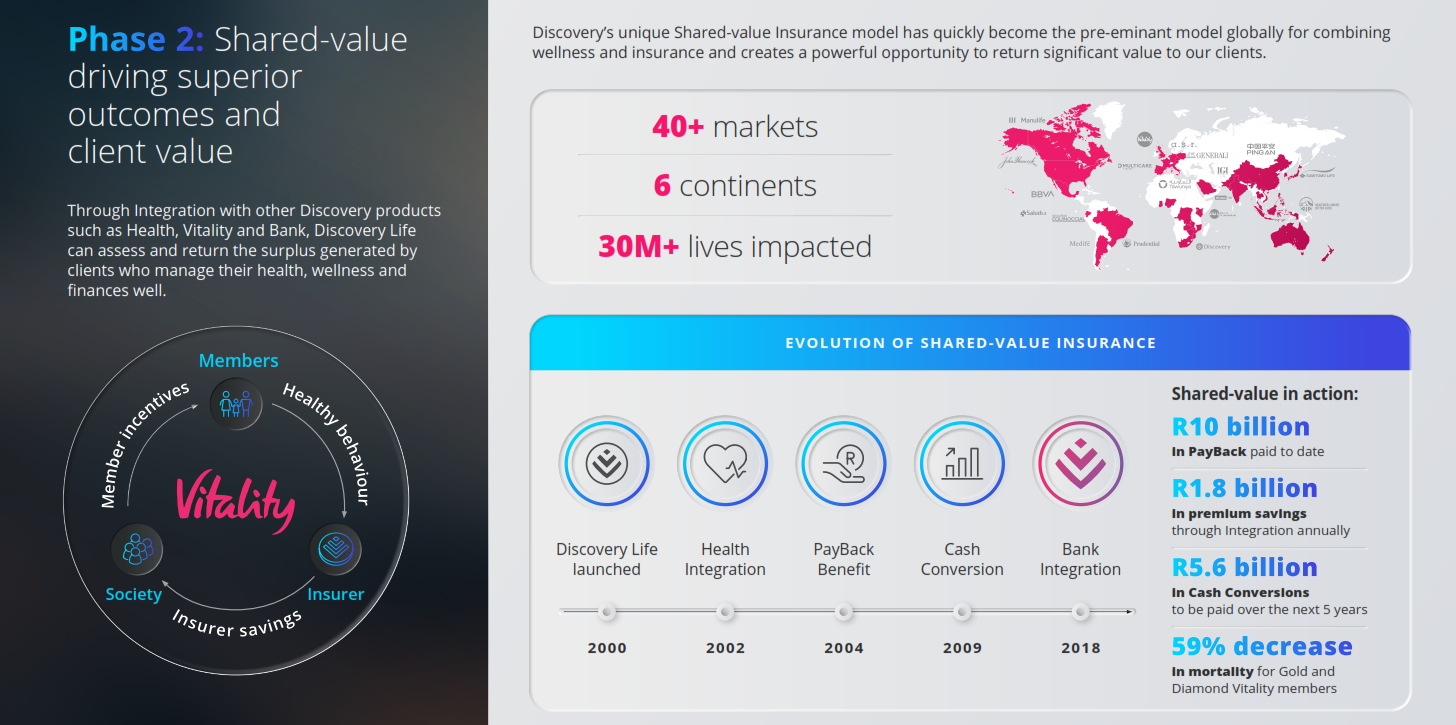

Discovery Life gave us an update on the Evolution of Discovery Life for 2023. Discovery has pioneered the evolution of Life Insurance in three distinct phase: The separation of risk from investment, the introduction of the Shared-value Insurance model, and now, the personalization of the client experience through digitisation. Each phase embodies innovative product that meet Discovery client needs and create unmatched value, while making them healthier, and enhancing and protecting their lives. Discovery Life has introduced the revolutionary new Discovery Life Plan 3.0 – The Future of Life Insurance, Now. On 22nd February 2023 Discovery have introduced the Discovery Life Plan 3.0, which personalises life insurance through digitisation, to deliver a seamless and hassle-free experience for you and your clients. As we move towards the modern digital era, this next-generation life insurance will be accessed on the mobile phone, offering your clients convenience and ease. This plan includes:

If you would like us to prepare on a Life quote for you contact Kevin or Sandra in our Life Department email: service@daberistic.com tel: (011)658-1333

0 Comments

There are several factors to consider when determining how much life insurance coverage you need. Here are some steps you can follow to calculate your coverage needs:

1. Determine your financial obligations: Make a list of your current and future financial obligations, such as outstanding debts, mortgages, and tuition payments. 2. Calculate your income: Consider your current income and any future income you anticipate receiving, such as raises or promotions. 3. Consider the length of your coverage: Determine how long you need your coverage to last, taking into account the length of time your dependents will need financial support. 4. Calculate your expenses: Estimate your living expenses, including housing, food, transportation, and any other recurring costs. 5. Consider any additional expenses: Think about any one-time expenses that your dependents may incur in the event of your death, such as funeral and burial costs. 6. Add up your obligations and expenses: Add up all of your financial obligations and living expenses to get a total amount of coverage you need. It's good idea to review your coverage needs periodically to make sure they are still adequate as your circumstances change.  Do you think of yourself as a healthy person? If you exercise a few times a week, make mostly positive eating choices, and rarely become seriously ill, you might well consider yourself to be. In fact, the thought of contracting a severe illness has most likely never entered your mind. Until you arrive at work one day to find out that an apparently healthy colleague of the same age as you has just been diagnosed with cancer. Then the realisation hits, there's a chance it could just as easily have happened to you.

Suddenly you start to consider the possibility that a severe illness could become a reality in your own life. And that protecting yourself and your family against the risk of an illness is more than a nice-to-have it's a must-have in every way. Do I really need severe illness cover? It's a good question and if you're relatively young and in good health, you may think the answer to be a resounding no. But for a more accurate assessment of your potential risk factors, a look at actual statistics might help shed some valuable light. Over the past year, the severe illness claims paid out to Discovery Life clients have painted an interesting picture:

Cover for severe illness When choosing your level of cover you should consider any outstanding debt and other liabilities that you would have to settle if you were to become severely ill. It is also important to consider the cost of modifications or lifestyle changes that would be required as a result of a severe illness. Set up an appointment with a Financial Advisor Kevin, please contact Nicole in our Life Department, email life@daberistic.com, tel (011)658-1333 Source: Discovery  Being diagnosed with a severe illness may dramatically impact your life in the short term and long term. You can have peace of mind, knowing that you will have sufficient funds available to pay for possible medical treatments, home nursing or any other costs that may arise.

Example John has a Severe Illness Benefit of R1 000 000. John submits a claim for his illness, acute renal failure which require further treatments. This condition is life-threatening, has several causes and is a common complication after any type of surgery. Although this condition is not cancer or a stroke, only prompt diagnosis and treatment can reduce the his risk of death. John qualifies for a 50% payout, providing him with R500 000 to use towards additional expenses and homecare assistance. Due to the benefit payout, John’s family can now focus on supporting him emotionally and not worry about financial hardship. Do I really need severe illness cover? It's a good question and if you're relatively young and in good health, you may think the answer to be a resounding no. But for a more accurate assessment of your potential risk factors, a look at actual statistics might help shed some valuable light. Over the past year, the severe illness claims paid out to Discovery Life clients have painted an interesting picture with these stats Few years ago: On average, 38% of claimants in 2015 were female, while the majority of 62% were male. Of the claims made, a full 51% paid out to females were for cancer-related diseases, compared to 31% for men. While claims made for body systems such as gastrointestinal, ear nose and throat, respiratory, eye and musculoskeletal tended to be evenly paid out between genders, a total of 35% of claims made by men were due to heart and artery conditions, compared to just 8% for women. Finally, claimants between the ages of 41 and 60 were by far in the majority, representing 61% of claims made in 2015, with claimants from 26 to 40 representing only 16%. What these figures clearly indicate is that no matter your gender, age or health profile, severe illness cover always needs to be a priority not for you, then for the continued well-being and support of your family. Cover for severe illness When choosing your level of cover you should consider any outstanding debt and other liabilities that you would have to settle if you were to become severely ill. It is also important to consider the cost of modifications or lifestyle changes that would be required as a result of a severe illness. If you would like us to do a quote for your Life and Severe Illness cover please contact Kevin in our Life Department email: service@daberistic.com tel:(011)658-1333 |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|