There is one day I look forward to in my calendar as a Financial Advisor, and that is the publication of the Annual Raging Bull Awards. This morning after I dropped my son Enxuan at the gym for his swimming session, I rushed to the local Pick n Pay store to buy a copy of the Saturday Star, to read about the hot-off-the-press Personal Finance section, which focuses on the 2016 Raging Bull Awards. I already know more or less who the winners are likely to be, the usual suspects of Allan Gray, Nedgroup, PSG etc, as I monitor the developments of larger fund managers closely. But it is still important to get the official results. So here it is: The winner is Allan Gray, second place PSG, third place Nedgroup Investments. Below is the full list. PlaxCrown ranking of management companies to December,2016  I did an analysis of the past winners, dating back to 2007. It looks like this:

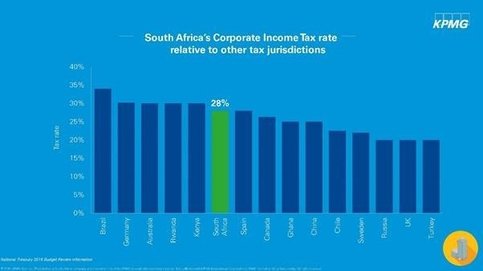

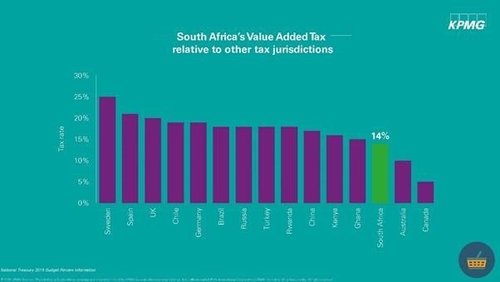

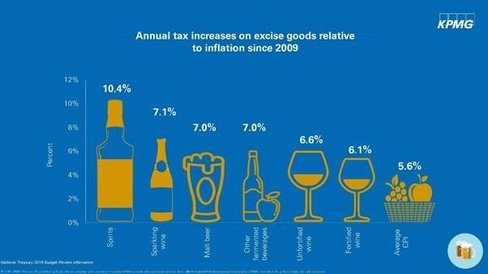

Allan Gray has won five times, Coronation 3 times, Nedgroup once, and Stanlib once. If I give the winner 3 points, the runner-up 2 points, and 3rd place 1 points, and tally the points over the 10 years, it gives an interesting picture of the consistently best larger fund managers in South Africa: Allan Gray: 20 points Nedgroup Investments: 13 points Coronation: 12 points Prudential: 7 points PSG: 4 points Allan Gray and Nedgroup Investments have been strong performers for a long time. PSG certainly is becoming a strong contender. Coronation has been underperforming over the last 12 months, but given its experience and depth of investment skills, it will make a comeback sometime. Prudential was featured prominently in the top 3 between 2007 to 2010, but since then it may be finding the competition heating up, now reducing to number 4 or 5. The analysis above does not mean managers not mentioned above are not worthy of consideration. Veterans like Investec and Old Mutual have some good funds worth considering. Boutiques like Rezco and Truffle also have some good offering. But the headline in the newspaper is true, "Larger and Mostly Independent Asset Managers Dominate Raging Bull Awards." Asset managers under insurance companies have consistently struggled to break into the top 5 positions. Should you require assistance and advice on what funds to invest in contact Thato or Kevin , tel 011-658-133, or email invest@daberistic.com Source: Kevin Yeh  In the march newsletter we will be focusing on on the 2017 Budget speech. This month we look predictions made by experts. Below is an article on views by Analyst before the budget speech. In the mini budget last year, Finance Minister Pravin Gordhan explained that additional revenue would be sourced through various tax increases. This is in the face of slowing economic growth and falling tax revenue collection. Analysts, senior economist at KPMG South Africa, Muziwethu Mathema and Grant Thornton’s director and leader tax Eugene du Plessis share their expectations of where they think Gordhan will find the “additional” revenue. Personal Income Tax (PIT) KPMG: PIT accounts for 35% of tax revenue. In SA, higher income individuals pay a higher proportion of tax, which means Gordhan would increase taxes for these high income earners to generate significantly higher revenue. This can be through the introduction of a 45% marginal tax rate for individuals earning above R1.5m per annum. Treasury could raise between R75bn and R10bn through this approach.  Grant Thornton: To avoid a VAT hike, increasing the tax rate for higher income earners is likely. Treasury may add a percentage to the top tier bracket. Or government may reduce the bracket creep adjustment, but this may result in a higher effective tax rate. If the bracket creep adjustment is chosen, to compensate for higher inflation pushing up income into higher brackets, it could offset or avoid a VAT increase. Corporate Income Tax (CIT) KPMG: Treasury is unlikely to raise CIT given the weak macro-economic environment. Increasing the CIT rate will be uncompetitive. SA’s current statutory tax rate is already higher than most tax jurisdictions, Treasury could lower the tax rate to attract investment.  Value-added Tax (VAT) KPMG: SA’s VAT rate is low compared to other tax jurisdictions. A one percentage point increase in VAT could generate R15bn in additional revenue. However raising VAT could have a negative impact on inequality, real GDP growth and inflation, according to the Davies Tax Commission First Interim report.  Grant Thornton: Treasury may be considering a VAT increase. If this happens government would have to take measures to minimise the impact of a VAT increase on poor households, for example through increasing social grants. An alternative option would be to introduce a dual or multiple-rate VAT system, where VAT is increased on luxury items and be lower on other items, and maintain a zero rate on basic items. But the costs related to the administration of this approach outweighs the benefits. There may also be a political fallout following the increase in VAT. Specific Excise Tax KPMG: Treasury is likely to introduce higher-than-inflation increases in sin taxes, which could generate between R5bn and R7bn. But increasing this tax may result in an increase in black market consumption. The sugar-sweetened beverages tax could generate between R2.5bn and R4bn. However the job losses incurred in this second may negatively impact PIT and CIT tax bases.  Grant Thornton: The proposed sugar tax is supposed to come into effect on 1 April 2017, but the process is still underway. The tax may be deferred and is unlikely to contribute to the fiscus any time soon.

Fuel levy KPMG: Treasury is not likely to increase the fuel levy. The higher crude oil prices also limit Gordhan from increasing the levy. The fuel levy could raise between R5bn and R7bn. Grant Thornton: An increase in the fuel levy could be another source of revenue. Although this may negatively impact poor households, it would be much “easier to sell” than a VAT increase. Other adjustments KPMG: Gordhan could provide reduced tax relief to short-term revenue. In Budget 2016, Treasury raised R7.6bn through this option. Failure to give tax relief over a sustained period is regressive. Gordhan may introduce adjustments to wealth-related taxes, similar to last year’s property taxes. Grant Thornton: The Special Voluntary Disclosure Programme, which involves exchange control and tax relief, may raise funds. The Davis Tax Committee is also looking at interest-free or low interest loans made to a trust will. Under certain circumstances where this results in donations, tax must be paid. But this is unlikely to make an impact on tax revenue collection this year. The committee is also considering the viability of wealth taxes. There may also be new measures related to transfer pricing and common reporting standards to avoid illicit transfer of funds to ensure tax revenue collection. Written by: Lameez Omarjee Source: Fin24  As 2017 gets underway, a look at asset valuations across the globe tells us that, going forward into the new year, returns that substantially beat inflation are likely to be harder to come by for South African investors than they have been in the past few years. Not only is global growth slow, but many assets are expensive compared to their long-term histories. This means that investment managers like Prudential will have to search even harder for attractive sources of real returns, while being ever-vigilant of the risk involved. Political risk will also play a greater role in the new year given the uncertainty surrounding the policies of the Trump administration in the US, Brexit in the UK and possible election victories for anti-euro populists in France, Germany and the Netherlands.

Finding good value in SA bonds So how are we positioning our multi-asset funds to earn the best possible returns over the medium term? From a global perspective, we believe that South African bonds are cheap compared to their long-term fair value, and offer good prospective returns. This follows their weakness stemming from elevated political risk (incidents such as “Nenegate” and threats to the Finance Minister’s position), as well as the ongoing risk of a credit rating downgrade, both being priced into yields. Relatively high yields of around 8.9% (for the 10-year government bond at year-end 2016) offer attractive real returns on a risk/reward basis. The stronger rand, easing of inflation and diminished likelihood of further interest rate hikes have improved – to an extent – the outlook for interest-rate-sensitive assets like bonds and listed property, despite very slow economic growth. Local listed property, meanwhile, is priced to deliver low-double-digit returns in the medium term (in the absence of a market de-rating). This is well above inflation, and we consider it attractively priced. As such, we are overweight both SA bonds and listed property (to a lesser extent) in the Prudential Balanced and Inflation Plus Funds. SA equities now more attractively priced South African equities fell to cheaper valuations in December compared to their long-term fair value: at 31 December 2016 the FTSE/JSE All Share Index’s 12-month forward P/E was 13.8x, versus 15.2x at the end of September. In response Prudential moved to an overweight position in our multi-asset unit trust funds. Within equities, we are underweight expensive global heavyweights like Aspen and Steinhoff. By contrast, British American Tobacco is one of our top overweights as a solid defensive stock. We also retain our defensive positioning in resources, being underweight specialised miners like Anglogold and Implats, and preferring diversified miners (like Anglo American) and non-mining shares such as Sappi. We are also overweight financial stocks, including Old Mutual, Barclays Group Africa and Investec, all of which remain undervalued. Finally, we continue to be underweight retail shares, despite the recent improvement in valuations, as we believe SA consumers and the economy will continue to struggle over the medium-term. Global equities expensive, especially in the US For global equities, our portfolios are currently neutrally weighted generally. This is despite a rally in share prices in November and December of this year (particularly in the US) as a result of the surprise election of Donald Trump, in anticipation of more expansionary spending policies. Some European markets do still offer value, where concerns over growth have kept share prices under pressure. At the same time, certain emerging market equities are also valued attractively, but we are very selective in our exposure as many also come with relatively high risks. India is a market that we like. In the Prudential Balanced Fund we are near the 25% maximum exposure allowed for offshore equity. Prepare for volatility, take advantage of downturns In conclusion, South African investors can expect continued volatility in 2017 amid high levels of global uncertainty and political risk. The bullish Trump-related rallies in the US could yet prove to be overdone. Locally, despite the marginally improving outlooks for inflation, interest rates and growth, material risks remain for a possible credit rating downgrade mid-year. Economic growth remains sluggish and pro-growth reforms difficult to implement. To cope with market volatility, investors would be prudent to save and invest more, stay well diversified, maintain a long-term view and ignore the short-term “noise”. Remember that there are always opportunities to add well-priced assets to a portfolio in downturns, and as an investment manager Prudential will certainly be taking advantage of these. Should you require assistance and advice on what funds to invest in contact Thato or Kevin , tel 011-658-133, or email invest@daberistic.com Written by: David Knee Source: Prudential  Decreases in cost and increases in transparency and choice regarding underlying investment options make endowments a viable option to consider for discretionary (non-retirement funding) savings.

In addition to estate planning benefits, the latest budget changes further strengthen the tax benefits of the endowment, encouraging high income investors to revisit the case for this often overlooked product. Increased income tax rates The recent budget proposed that personal income tax rates increase by 1%. This was done from the second bracket (those earning in excess of R181 900 per year) upwards, but considering adjustments to rebates and tax brackets there will only be tax relief for tax payers earning below R450 000 per year. The highest tax bracket for individuals has now increased to 41%. This tax rate now also applies to trusts (other than special trusts), which previously paid 40%. When does an endowment make sense? There are a number of factors to consider when choosing between a pure discretionary savings plan (DSP) or an endowment. This includes availability of interest and capital gains allowances as well as required access to capital within the first five years. A key consideration in how to allocate between the two products is the clients’ tax rate. Income tax legislation requires policyholders of an endowment to be classified as an individual, company or untaxed policyholder and income and capital gains tax varies accordingly. An endowment is available to individuals as well as trusts with individuals as beneficiaries with tax as follows: Tax on income at 30% and effective tax on capital gains at 10%. Individuals in a DSP are now taxed at marginal rates up to 41% resulting in an effective tax rate on capital gains of 13.7%. For such high income earners the endowment can offer significant tax saving. Within the two products there is no differentiation for dividend tax, which is withheld at 15% either way. How much can you save on tax in an endowment? Consider an individual that has no interest and capital gains allowance available and invests R5m for 10 years. Assume a balanced fund-type investment with 11% return per annum and no trading of the portfolio over the period. After five years, allowing redemptions for payment of income tax annually, such an investment would have grown to R8.16m in a DSP. An equivalent investment in an endowment would have grown to R8.23m, but saved about R145 000 over the period. This consists of: income tax saving (30% versus 41% marginal rate assumed) capital gains tax saving (taking 100% of the capital gain into account) additional return earned as a result of higher base to compound from Over the full 10 year period assets in the DSP would be at R13.32m, but the investor would have missed out on a total saving of R426 000 relative to the endowment. Do the math Trusts or individuals with significant discretionary savings and high marginal tax rates should consider an endowment. There are restrictions that may not make it a suitable option, but multiple benefits and the significant potential tax saving are not to be ignored. Benefits of an endowment Greater tax efficiency for higher income earners (above 30% tax rate) who have exhausted their interest exemptions. Beneficiary nomination can lead to potential savings on executor’s fees (up to 3.99% of fund value). Where a beneficiary has been nominated, payment of the death benefit does not depend on the winding up of the estate and beneficiaries will receive the proceeds relatively quickly. Tax administration is taken care of on your behalf (the insurance company calculates, deducts and pays the tax to SARS). Insolvency protection – the entire value of the endowment will be protected against creditors after three years. This protection will continue until five years after the termination of the policy. Investors are not restricted to maximum levels of equities and offshore investments, as in the case of retirement savings products. Investors can also use an endowment to draw income upon retirement – provided the five-year restricted period has passed. This may be done on an ad-hoc basis, and you are not forced to draw income at specific intervals. To get a quote for your Endowment policy please contact please contact Kevin or Thato, email: invest@daberistic.com, tel no: (011 658-1333) Written by: Roenica Tyson Source: Sanlam |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|