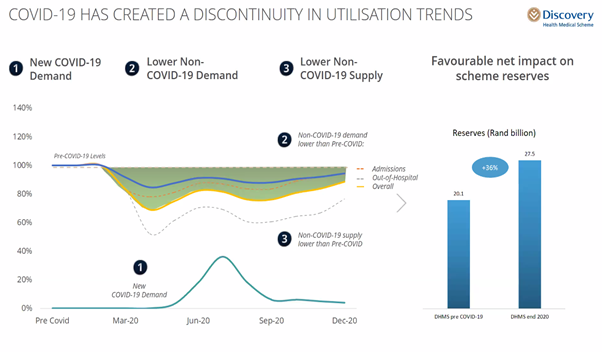

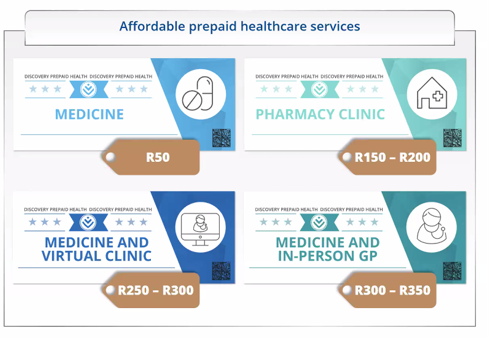

On 30 September 2020, Discovery hosted its first ever virtual workshop with over 10,000 brokers, to announce Discovery Health's benefits and contribution update for 2021. Discovery reiterates that its core purpose is to make people healthier and enhance and protect their lives. 2020 has been a very challenging year from the healthcare perspective. According to Discovery Health's statistics, during the lockdown period over the last few months, the number of elective surgeries has drastically reduced as members chose to delay these treatments and avoid going to the hospital. The COVID pandemic meant most of the healthcare resources were directed towards the testing and treating COVID patients. No increase in contributions up until 30 June 2021Discovery Health understands that everyone has gone through financial strain during the lockdown, so we are excited to announce that Discovery has decided to freeze all scheme contribution increase across all plans for the first 6 months of 2021. However, this alleviation is not long term, thus the contribution increase will be announced during the second quarter of the year and implemented on 1 July 2021. The expected increase will be CPI + 2%, capped at 5.9%. Doing so, they are looking to assist members in affordability, sustainability and spreading the financial impact everyone has gone through during 2020. Based on its data analysis and observations during the pandemic, four trends have emerged: Utilisaiton discontinuity - how the COVID pandemic has disrupted the normal medical utilisation pattern. Technology - the pandemic has pushed the use of technology to the fore, to enable digital healthcare services from the comfort of one's home. Quality care Access - recognising that millions of South Africans don't have medical aid, Discovery announces a solution to make healthcare affordable and accessible to all. We use a few infographics to illustrate these trends:  Discovery Health's experience shows the COVID pandemic peaked around June to August. What has helped the scheme was from late March to now the number of non-COVID hospital admissions have reduced by 20% to 30% compared to last year.  Discovery Health has always been innovative and progressive with technology. Since the lockdown began, virtual consultations have increased by 8-fold. Discovery Health now introduces Connected Care, where it enables a range of appropriate home-based healthcare services for all levels of care. The picture above shows the TytoHome diagnostic device Discovery is bringing into the country and offering its members.  Discovery's research shows 50% of South Africans are on "pre-paid" healthcare. They have launched Prepaid Health to cater for all South Africans. This new offering launching at the end of December 2020 is one of the exciting products where good healthcare is available to anyone on a pay-as-your-go basis. Discovery leverages on its network, so you have access to good healthcare at a discounted rate. For members on hospital plans only, they can also purchase these vouchers for their day-to-day benefits. Discovery Health Plan Guides 2021Below are the Discovery Health Plan Guide brochures for 2021 (note these are still subject to approval by the Council for Medical Schemes): Next: Other highlights in Discovery Health Product Update 2021

0 Comments

Much debate has taken place around the proposed National Health Insurance Bill (NHI). Discovery’s overall position on NHI is unequivocal. We would like to provide some additional information to answer any questions you may have.

Discovery Health is supportive of structural change that assists in strengthening and improving the healthcare system for all South Africans, and we are committed to assisting where we can in building it, and making it workable and sustainable, seeking to ultimately strengthen both the public and private healthcare systems for all South Africans. While the NHI is a huge, complex and multi-decade initiative and a considerable amount of debate and effort will be required to make it workable, in this brief note, we review some of the key issues arising from the NHI Bill and then look at the NHI policy process going forward. The role of medical schemes once the NHI is implemented A central issue is the future role of private healthcare and medical schemes once the NHI is implemented. The NHI Bill states that when the NHI is ‘fully implemented”, medical schemes will not be able to provide cover for services that are paid for by the NHI. Discovery's strong view is that limiting the role of medical schemes would be counterproductive to the NHI because there are simply insufficient resources to meet the needs of all South Africans. Limiting people from purchasing the medical scheme coverage they seek will seriously curtail the healthcare they expect and demand. It poses the risks of eroding sentiment, and of denuding the country of critically needed skills, and is impacting negatively on local and international investor sentiment and business confidence. Crucially, by preventing those who can afford it from using their medical scheme cover, and forcing them into the NHI system, this approach will also have the effect of increasing the burden on the NHI and will drain the very resources that must be used for people in most need. Discovery also believe that limiting the rights of citizens to purchase additional health insurance, after they have contributed to the NHI, would be globally unprecedented and inappropriate. In virtually every other country with some form of NHI, citizens are free to purchase additional private health insurance cover, including cover that overlaps with services covered by the national system. A restriction on choice of medical scheme cover is not dissimilar to limiting the rights of citizens to purchase private education for their children or private security, on the basis that the public system already provides state schooling and security services. Given the substantial harms that this approach of limiting the role of medical schemes will cause, it must surely be strongly justified for good policy reasons. However, we are not aware of any sound policy reason or justification that has been put forward for this approach. Discovery believe that medical schemes will continue to cover all of the healthcare services which they currently cover for the foreseeable future for a number of reasons:

Discovery is already actively engaging with the Department of Health on this critical set of issues, alongside the broader business community, and we will continue to do so in order to ensure that medical schemes and private healthcare remains a critical part of the healthcare system, together with the NHI. The financing of the NHI system The Bill makes no reference to the likely costs of the NHI once fully implemented. Any fundamental change that improves quality and access and seeks to contract with private providers will require substantial additional funding. We understand that National Treasury will soon be publishing a costing document, and that this is likely to be based on an incremental approach to providing NHI benefits. The Bill specifies that payroll taxes and a surcharge on personal income tax could be considered as sources. Such taxes would need to be determined by National Treasury. At the presentation of the Bill, the Minister of Health indicated that no tax changes are envisaged over the 3 year period of the current Medium Term Expenditure Framework. In our view, there are material challenges to raising new revenues to supplement the current government budget for healthcare, and this is unlikely to change in the foreseeable future. This suggests that the rollout of the NHI will be slow unless there is a substantial improvement in the country’s economic prospects. The role of private hospitals and health professionals The Bill envisages that the NHI Fund will contract on a voluntary basis with private hospitals and health professionals to supplement the current public sector delivery system. For the foreseeable future, we expect that the NHI will contract with some GPs to supplement primary care services, and also that it will contract for certain high priority services to address specific gaps in public sector provision. If this is achieved, it will already be a significant step forward. Beyond that, we expect that the vast majority of NHI services will continue to be delivered by public sector clinics and hospitals, and that private hospitals, specialists and other providers will continue to be funded by medical schemes. South Africa is blessed with a committed, highly skilled and world-class healthcare professional community. These professionals work hard, provide excellent care and are committed to our country. We will work hard to defend their rights to fair remuneration, to an optimal working environment that promotes sustainability and ideal patient care, and to retaining and supporting them within our broader healthcare system. The NHI Bill Process The NHI Bill has been tabled in Parliament and is now in the hands of the Portfolio Committee on Health, which will hold formal hearings in early 2020. Discovery is actively participating in a direct engagement process between Business Unity South Africa and the Department of Health to discuss a number of issues of common interest, including the NHI. There is also a parallel process within NEDLAC, offers further opportunities for business, labour and government to engage on the final content of the Bill. We expect the Bill to be finalized sometime during 2020 at the earliest. Concluding remarks While the NHI Bill certainly raises some serious concerns, we recognize the need for structural change to improve healthcare for all in SA. We believe this should leverage the strengths of the key elements of the current public and private healthcare systems, and we remain confident that the final outcome will be rational and workable. Discovery is committed to playing its role in building a positive future - for our members, South Africa’s healthcare professionals, and for all South Africans. Frequently asked questions

o Physiotherapy consultations and treatment o Biokineticist consultations and treatment o Dietician consultations and treatment o A smoking cessation programme o Blood tests o X-rays

o New moms will also be able to access vouchers offering up to 70% off baby products at Baby City 2020 Contributions The Fund announced that the increases for 2020 range from just 6.2%, with an average increase on risk contributions of 9.4% and an average increase of 9.9%. The increases were as follows:

Click here to download the 2020 product brochure Please contact Namhla or Tammy in our Health and Wellness Department, email health@daberistic.com, if you have any queries about Bonitas Source: Bonitas  Click here to read more on Medical Aid enhancements

Please contact Namhla or Tammy in our Health and Wellness Department, email health@daberistic.com, if you have any queries about Discovery Health Source: Discovery  It’s now time to review your medical aid scheme cover for 2020. This means you have a window within which you can switch to a different plan for the new year. This window usually closes at the end of November (depending on your current provider), so don’t delay collecting the necessary information. This is not a decision to be rushed.

Why do I have to decide now? Medical aid providers allow you to switch to a higher plans once a year (at the end of the year) without penalties or consequences. If you want to save on premiums or you need to increase benefits, now is the time to do it. What if I want to change providers altogether? If you are unhappy with your medical aid provider, you can switch to another at any time of the year. But before you do, consider the following: Waiting Periods Medical Aids by law must accept anyone who applies to join their scheme. To protect themselves from older or sickly members that join without having contributed to the risk pool, they usually impose a waiting period of between 3 and 12 months. Waiting periods will apply if 1) you have not been a member of another South African medical aid for the past three months or more, 2) if you change medical schemes before 2 years of being covered with your previous medical aid provider and 3) if you have a pre-existing medical condition. Finding out about any waiting periods is extremely important before deciding to change providers. Late joiner penalty As an additional means to manage the risk of older or sickly members joining without having contributed to the risk pool, medical schemes (according to the Medical Schemes Act) are entitles to add a late joiner penalty to your premium if you were not part of a medical scheme before 01 April 2001. The late joiner penalty is calculated (using a prescribed formula) based on the number of years that you were not on a registered South African medical scheme. The late joiner fee can range between 5% and 75% of the total contribution, depending on the number of years that you were not covered by a medical scheme. Please contact Namhla or Tammy in our Health Department, email health@daberistic.com, to find out about different Medical aid options Source: Medicalaid.co.za  Medical aid is a form of insurance where you pay a monthly amount, called contribution or premium, in return for financial cover for medical treatment you may need, as well as any related medical expenses.

Medical aid and health insurance are two different products. Medical aid, or medical scheme, is regulated by the Medical Schemes Act, provides in-hospital cover and chronic illness benefits, and pays for treatment according to specific medical scheme tariffs. Some medical aids also provide for day-to-day medical expenses. Health insurance, on the other hand, is regulated by the Short-term Insurance Act. It provides a more limited set of health benefits, up to a monetary limit. Health insurance is a cheaper alternative for people who cannot afford medical aid. Why medical aid is important Having a good medical aid plan with a reputable medical scheme can help you protect both your health and your wallet. The reality is that your health, and that of your family holds immeasurable value to you. There are many advantages of belonging to a medical aid. It financially protects you if you suddenly have to pay large, unexpected medical costs. Being a member of a scheme also means you have access to private medical care, instead of having to rely on public health services. If you are looking for advice on healthcare needs for you, your family or your company, you can contact us on the following channels: - WeChat: daberistic - Email: Health@Daberistic.com - Phone: working hours 011 658 1333  Medical aid is a necessary yet expensive purchase in South Africa. Due to the public healthcare system unable to cope with the public demand, people who can afford it or who work for larger employers will choose private healthcare. They buy medical scheme products to cover such healthcare expenses.

Since medical aid is expensive, it is important for a member to understand its benefits, in order to make the best use of it when needed. As each new year begins medical aid members start with a clean slate, with new benefits and replenished savings available. If you manage your medical expenses correctly you can avoid out-of-pocket expenses and limit the possibility of running out of benefits. 1. Read up on your medical aid plan Take the responsibility of understanding your medical aid plan. Visit the medical scheme's website, find your specific medical aid plan information and read through it. Check out the FAQs. If your medical scheme creates YouTube videos on your specific plan and benefits, watch these videos. The more you understand your medical aid plan, the better you are in a position of making use of benefits provided for by the plan. 2. Speak to your Healthcare Advisor Medical aid plans are complex. A medical aid plan has many details, terms and conditions. Many members will struggle to make sense of it. A Healthcare Advisor with suitable qualification, training and years of experience can simplify matters for you and answer your specific questions. 3. Find a GP on your medical aid's network Using network doctors is an invaluable tool to make your medical aid last longer as it means you won’t be charged more than a specific amount. 4. Always use partner networks Medical schemes negotiate preferential rates with providers who have partnered with them. This means if you use a network hospital, doctor or pharmacy you will not be charged more than the rate agreed with the scheme. This will also help you to avoid co-payments, deductibles and additional out-of-pocket expenses. 5. Ask your pharmacist Buy over-the-counter medicine to treat less serious ailments and consider using generic medicine which is cheaper but effective. Pharmacists are able to provide sound medical advice on problems such as rashes, colds or illnesses that are not severe, simply ask! 6. Going to hospital - get the facts Talk to your doctor or specialist before being admitted to hospital. Check what they are going to be charging and what your scheme will cover. If there is a large difference, don’t be afraid to approach your doctor to see if they are prepared to adjust their fee. Alternatively, you can also check if there are other healthcare providers who are on your scheme’s network that will charge you a better rate. 7. Remember to pre-authorise Pre-authorisation is required for all hospital admissions to ensure your stay will be covered. Always ask if there are any co-payments or sub-limits that will apply and what you can do to avoid these. For planned procedures, it’s also worth checking with your scheme if you will obtain better cover by using contracted providers or having the procedure performed in the doctor’s rooms or a day clinic. 8. ICD-10 codes If you need to undergo an operation, ask your surgeon for the codes that will be charged. This will include the procedure codes and those for any other products that will be needed, this all helps with pre-authorisation and ensuring the costs will be covered. 9. Chronic health conditions Some schemes offer programmes to help you manage severe chronic conditions such as cancer, diabetes and HIV/AIDS. These programmes are usually covered from the risk portion of your medical contribution and are not funded from your savings account. They help you use your benefits to maximum advantage while ensuring you receive quality care by using specific providers. With thanks to: www.w24.co.za |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|