Yesterday (Happy International Women's Day!) I was fortunate to visit Dodge & Cox in San Francisco, US. Kevin Johnson, an experienced portfolio manager at Dodge & Cox, was kind in spending over an hour with me, for me to understand more about the firm, its operations and investment outlook. Dodge & Cox is situated in the Financial District of San Francisco, occupying 4 floors in this very impressive skyscraper on 555 California Street.

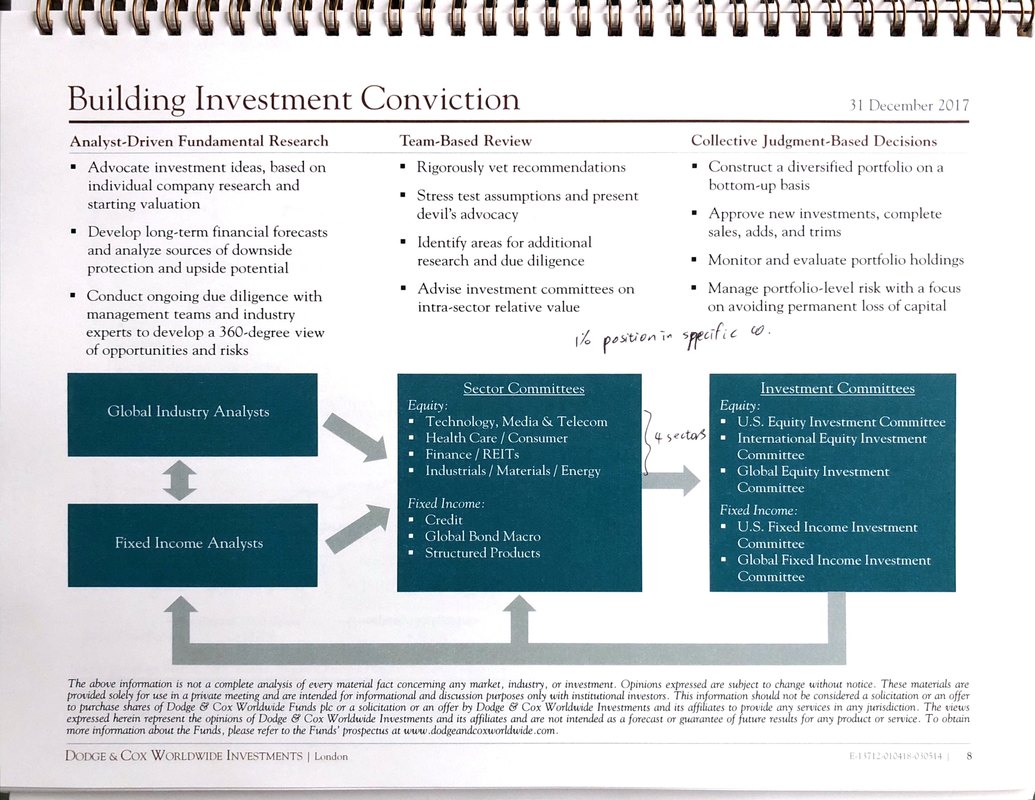

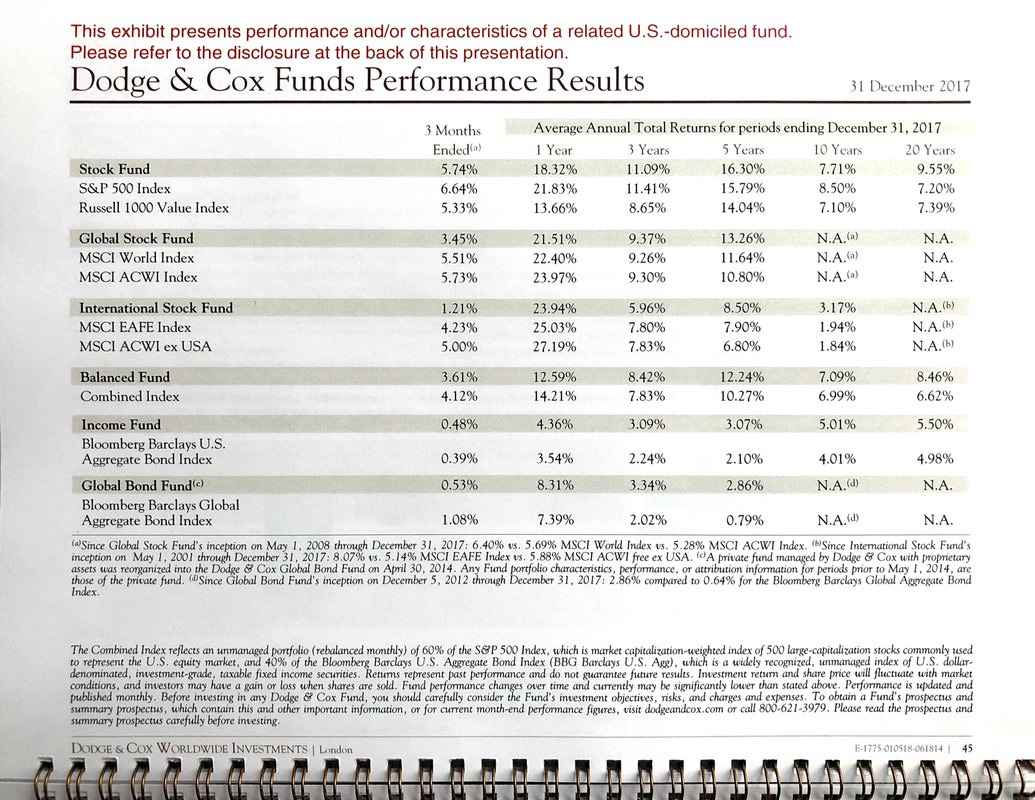

After the guest registration process at the lobby, I was told to take a lift to the 40th floor. When the elevator door opened, I walked onto think carpet, with the gold plated Dodge & Cox signage in front of me. I knew I was at the right place. The office has stunning views of the San Francisco Bay area. The tall building in the second picture is Transamerica Pyramid, 260m high.   Kevin Johnson came and welcomed me, took me to the boardroom with stunning views of San Francisco. I decided to sit with my back facing the view/window, so I could better focus on my discussions with Kevin. Kevin Johnson is well versed in the investment markets, with 28 years of experience at the firm. I gave him a background of what Daberistic does, our wealth management services to our clients, and how Dodge & Cox funds fit into our solutions to our clients. Kevin then gave me a presentation booklet on Dodge & Cox UCITS. I am not familiar with the term UCITS, so afterwards I googled it. UCITS stands for “Undertakings for Collective Investment in Transferable Securities". In essence mutual funds, or unit trusts as known in South Africa. Dodge & Cox was founded in 1930 in San Francisco. It prides itself in having a stable and well-qualified team of investment professionals, most of whom have spent their entire careers at Dodge & Cox. Ownership of Dodge & Cox is limited to active employees of the firm. Currently there are 75 shareholders and 271 total employees. It is a mature fund management business. Kevin emphasised the point that Dodge & Cox is independent, no absentee ownership, no parent company to report to, so not forced to do anything. This is a great contrast to Merrill Lynch, which is owned by Bank of America. Dodge & Cox is solely in the business of investing clients' assets. Apart from the San Francisco office, it only has one small client service office in London. So all its staff are based in the single office in San Francisco. It offers a focused range of strategies (I tend to like fund managers with a small, focused range): US equities Non-US equities Global equities: combination of the above two US Fixed Income Global Fixed Income US Balanced (combining equities and fixed income) Active vs Passive This debate continues to rage on. Kevin and Dodge & Cox are undoubtedly in the Active Managers camp. His comments? Active managers have been overly criticised for high fees, the focus on (comparing to) average active managers return is a mistake. Dodge & Cox wrote an article on the characteristics of good active managers. These include: 1. Low turnover 2. Experienced 3. High active share. Passive is really a Momentum strategy, buying more on the way up. He used the dotcom bubble as an example: in 1998 the tech sector accounted for 45% of S&P, and index trackers would continue buying more of tech companies as their weightings in the index rose. Only to see the dotcom bubble burst until 2002. What is important is to focus on performance after fees, he comments. I 100% agree with this point. Dodge & Cox is a value-driven fund manager. Value as a style has fallen out of favour with investors over last few years, as the bull market continues to rise. Dodge & Cox continues to stick to what it has done over last 88 years, without wavering. Value Defined It is always good to get under the skin of a manger to understand better what they mean. Kevin defines the firm's Value Investing as "what you thing it's going to be worth in the future. It can be strictly metric based, such as PE ratio. It can also be valuation relative. You would want to avoid something with very high premium built in the price, as it may not be sustainable." So Dodge & Cox sees value in a slightly different way to Warren Buffet. It uses four investment hypotheses: Above Average Growth, Compounders, Cyclical or Asset Play, Deep Value or Turnaround. Warren Buffett's style is probably more the first two hypotheses. Risk Management Over the years I have learnt to appreciate that the best fund managers are also the best risk managers. Dodge & Cox has a systematic way of analysing risks, under the six headings of Operational, Macroeconomic, Commodity, Financial, Technological and Political/Legal Risks. These are used to assess what will cause the future outcomes to disappoint. Investment process Dodge & Cox has a tried and test investment process, run by a very experienced team.  I posted some very specific questions to Kevin, his comments are as follows: Schroders as a value manager We as a manager do not worry about what other fund managers do. My impression is they have an excellent reputation, has value orientation. It may have lots of funds. On the question of the use of the word Recovery in Schroders global Recovery Fund: "There can be an element of marketing. This might define value in a more narrow way." Coca-Cola "it is a good business, not a lot of growth, highly priced. We don't own any Coca-Cola stock. Maybe when its PE is 13 it becomes interesting to us." Amazon "A remarkable company, high valuation makes no sense to us. However what it does influences our thinking on other retailers. Retailers like Sears and JC Penny have been in decline for years. Macy's also struggling, not to the same extent. Walmart and Target have done better in response to the changing business environment, the online/offline mix strategy is a good one." Its AWS (Amazon Web Services) also influences our thinking on other tech companies like Microsoft." "of the FANGs, we only own Google" Dell Dell just came out with its update, showing 9% turnover growth and doubling operational losses, so I posted to Kevin. "Dell went largely private, had a series of corporate actions over last 2 1/2 years. Laptops have low margin, the profitable part is server/other services." Portfolio diversification As a wealth manager I am very sceptical of funds with 20% weighting in one stock (Naspers), as I question their risk management and diversification. "We do not have more than 5% of portfolio in one holding. In our Global Stock Fund, we probably will not exceed 3%." Its original (US) Stock Fund has an enviable track record of annualised 9.55% return over 20 years, outperforming S&P500. Over 10 years a respectable 7.71% after fees. The Global Stock Fund, which South African investors can access via Glacier Global Stock Feeder Fund, has done annualised 13.26% in USD over last 5 years.  The time was just too short, if there is an opportunity I would come back again. At the end of the meeting I asked Kevin to take a photo together. He agreed as a gentleman.

0 Comments

Discovery Balanced Fund is a flagship fund offered by Discovery Invest. It is only available on the Discovery Invest platform. It is managed by Chris Freund of Investec Asset Management, a very experienced and successful portfolio manager. He manages investments using an earnings revision approach. Discovery Balanced Fund has attracted a lot of inflows, in fact the fastest growing balanced fund in South Africa, thanks to clients and advisors' support, benefiting from the integration and unique features of a range of Discovery Invest products. Discovery Balanced has been a consistent top-quartile performer in the high-equity balanced fund sector, with the (annualised) performances figures as follows: 10 years: 10.14% 5 years: 11.52% 3 years: 8.05% 1 year: 11.34% This fund has a high cost, with a Total Investment Charge (TIC) of 2.12%. This makes it one of the most expensive balanced funds to invest in. I question this high fund management fee, even given its good performance figures. Were it not for various integration and fee reduction structures offered by Discovery Invest for investing in a Discovery fund, this will erode net returns to investors over the long term. Discovery Balanced Fund is suitable for general long-term investment. Being Regulation 28 compliant, it is suitable for use in a retirement product. Below is the link to download Discovery Balanced Fund's fund fact sheet as at end December 2017.

Firstly, let me dedicate this report to my Lord and Saviour Jesus Christ, may honour and glory be to Him forever and ever! As a Financial Advisor with actuarial qualifications, I am particularly fascinated by investments. I have spent lots of time over the last 21 years studying the subject of investment. I have learnt and analysed all kinds of financial instruments, including shares, unit trusts, CFDs, futures, warrants and ETFs. Over the years the investment markets have taught me a lot of things. It has taught me to be humble. It has taught me to be a ready student, to continue to learn, think and reflect. In the past I have written about share analysis, technical analysis, and general investment advice. This is the first time I write and share a comprehensive report on unit trusts. Over the years I have appreciated the way good unit trusts, or Collective Investment Schemes, has helped me and my clients grow my wealth. They have provided many investors an excellent way of investing in a diversified portfolio of assets, that over the long term have demonstrated significant real returns. This first comprehensive report on unit trusts focuses on high-growth unit trusts. I share this report with my fellow financial advisors in the hope of helping you help your clients make better, independent, informed investment decisions. If you like this report and think this report has helped you, please like it on LinkedIn and share it with financial advisors. Please also comment on this report, so that I can know whether I am on the right track, and how I can continue to refine my investment thinking. Click the link below to download the report.

This group of unit trusts has 100% of the money invested in offshore assets, predominantly in offshore equities. It may have some exposure to the listed property sector, as well as cash and bonds. Given the fact that South Africa only accounts for 0.5% of the world economy, and there are many excellent, well-known international companies not available for investing in South Africa, I encourage investors looking to maximise their returns over the long term to allocate a high percentage of their portfolio to Offshore Unit Trusts. You will also benefit from expected Rand depreciation against the US Dollar over the long term.

International giant brands not available for investing in South Africa include: Alphabet (parent company of Google) Amazon Apple Berkshire Hathaway Microsoft Nestle Samsung Unilever Return profile: Expected high returns over the long term (10 years plus), on average 12% to 16% per annum Volatilities: As stock markets fluctuate, reacting to news and market sentiments, offshore unit trusts also fluctuate daily. It goes up one day, down the next. It goes up one month, maybe down the next. In addition, there is also exchange rate fluctuation, which may magnify price movements if you invest in Rand-denominated Offshore Fund locally. Who is it suitable for:

This group of unit trusts typically has a relatively high weighting, up to 75% of the money, invested in the stock markets, or equities. Most balanced (or known as multi-asset, high-equity) unit trusts invest according to Regulation 28 of the Pension Funds Act, which means up to 75% of its money invested in equities, up to 25% invested offshore, up to 5% invested in Africa, with the balance invested in bonds, money market and property. It may have some exposure to precious commodities such as gold.

Generally this group of unit trusts invest its money for retirement fund members in South Africa, so it is fairly moderate in its risk management approach. It would not want to risk people’s retirement savings. It invests in quite a number of different assets and different companies to diversify. Return profile: Expected higher returns over the long term (5 to 10 years plus), on average 8% to 12% per annum. Volatilities: As stock markets fluctuate, reacting to news and market sentiments, balanced unit trusts also fluctuate daily. It goes up one day, down the next. It goes up one month, maybe down the next. However, the price movements are muted compared to High Growth Unit Trusts. Who is it suitable for:

On the 15th of September Charles de Kock, Portfolio Manager for Coronation Capital Plus Fund and Balanced Defensive Fund, updated financial advisers on the current investment landscape, the performance and positioning of these two funds. Click below to view the presentation.

Conversations with Coronation September 2015 |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

||||||

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|