Record-high fuel prices in South Africa Orlik (2022) states that South Africa has faced one of its toughest economic slumps, due to the COVID-19 pandemic. Lockdown restrictions had a massive impact on the economy of the country. Many consumers are still facing the financial impact and struggling to keep head above water. South Africa has also seen fuel prices hit a record-high in the first six months of 2022. Fuel prices are mainly affected by two components (BusinessTech, 2022): 1. The rand/dollar exchange rate 2. Changes to the costs of international petroleum products, primarily driven by oil prices Russia’s invasion of Ukraine has a massive impact on the fuel price increase as well. According to André Thomashausen, an emeritus professor of international law at Unisa, fuel prices could continue to rise to over R40 per litre, in the worst-case scenario (Prior, 2022). On top of this, consumers also must pay more for public transport, food and other services, all affected by the increase in fuel price. Consumer are facing even more pressure to survive in trying times. 10 tips to help your tank last longer There must surely be ways to save fuel during these tough economic times with fuel prices continuing to rise. Saving fuel is something we can all benefit from. After all, who would not want their tank of fuel to last longer?  Vitality Drive helps clients save on fuel Click here to read more

If you would like to Apply for Vitality Drive or Do a comparative quote contact Ed in our Short-term department email: service@daberistic.com tel (011)658-1333 Source: Discovery Insure

0 Comments

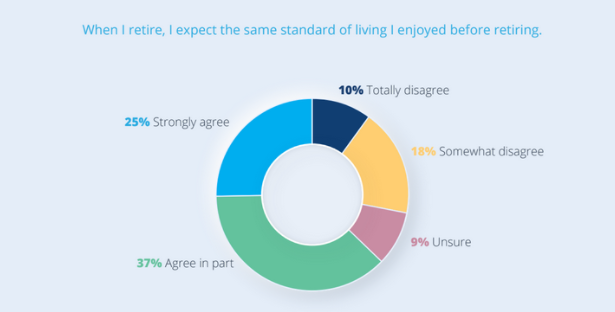

In partnership with Morningstar: Researchers often look at sociodemographic variables, such as age or income, to make predictions about people's saving habits. But the decision to save, of course, extends beyond one's basic demographics - our unique psychological profiles spearhead the decisions we make, including decisions about our finances. What does behavioural science teach us about our problem with saving and how we can overcome it? The 2021 edition of the 10X Retirement Reality Report points to a deteriorating pension outlook for South Africans. In the wake of the Covid-19 pandemic, even fewer now look forward to a comfortable retirement, says Chris Eddy, head of investments at 10X Investments. This is evident across all age groups, demographics and income levels. The 10X report is based on the annual Brand Atlas Survey, which tracks the lifestyles of the 15 million economically active South Africans in households earning more than R8,000 per month. Alarmingly, this modest cut-off already excludes two-thirds of households in the country. In total, 71% of respondents indicated they had no retirement savings plan at all, or just a vague idea of one. That is a lot of people who could be forced to rely on the kindness of family and friends, or to live off South Africa’s meagre older person’s grant (state pension) of R1,890 per month (R1,910 for those older than 75), said Eddy. Within the ‘fortunate’ minority, half the respondents still don’t save because they have nothing left at the end of the month. And even among those who are saving, just 7% anticipate a comfortable retirement; 79% fear they won’t have enough or feel unsure. Most survey respondents (74%) believe they will have to generate some income after they retire. Another 19% are not very sure, leaving just 7% of respondents feeling confident that they are on course for what is increasingly becoming an outdated notion of retirement, based on full financial independence. Breaking this down into different income groups: a mere 6% of those with a household income of R50,000 and above feel sure they will not have to keep earning after they retire. For both other income groups, it was just 7%. This highlights once more that achieving a financially secure retirement is less about how much we earn, and more about how much we engage in the process, inform ourselves and save.  But how much is enough, and how do we start a savings plan to get there? Several leading financial services firms weigh-in: The 80% rule Schalk Louw, portfolio manager at PSG Wealth, notes that many experts recommend using the 80% rule as a benchmark for what you will need to cover your monthly expenses once retired. “I won’t personally guarantee the accuracy of this figure, but it does give us a basis to start from,” said Louw. If you currently earn R15,000 per month, and apply the 80% rule, you will need at least R12,000 per month after retirement to maintain your current living standard. Unlike food products, human beings don’t have a “use by” date, so we have to rely on a safe withdrawal rate to ensure that we do not outlive our savings, said Louw. According to this rate, you should be able to withdraw 5% of your portfolio yearly without having to use any of your remaining capital, he said. “This approach is based on the fact that the historical return on the South African stock market (since 1964) was about 8% higher than the local inflation rate and that you would expect to earn slightly less than that in a typical balanced fund portfolio. “By limiting your withdrawals to 5% of your portfolio, you should still have an additional 5% to 6% growth to cover inflation in the long run.” Based on a 5% annual withdrawal rate after retirement, Louw said that the amount you will need to save in rand terms would look something like this: R12,000 x 12 months = R144,000 (annual income) ÷ 0.05 (5% safe withdrawal rate) = R2,880,000. If you don’t properly compensate for inflation in your portfolio, you may fall short of your required total after retirement, said Louw. “Let’s assume that you are 40 years old and you plan to retire at age 65 (25 years). By using the top of the South African Reserve Bank’s target range, the best-calculated guess we can offer on annual inflation is around 6%. The 4% rule Traditionally, financial advisers, savers and retirees have relied on the 4% rule when working out how much to save for retirement and what kind of annual income retirement savings would provide, noted financial services group Discovery. Simply put, the rule says that if retirees withdraw 4% of their savings annually (adjusting this amount for inflation every year thereafter), their nest egg will last at least 30 years. The rule also requires retirement savings to be split equally between shares and bonds. This method, Discovery said, is also used to determine the lump sum investors need to provide an acceptable annual income when they retire. For example, if you retire with a final salary of R480,000 a year, you need a replacement ratio of 90% of your final salary, which amounts to R432,000. To ensure you do not use all your saved retirement capital in 30 years, R432,000 should be 4% of your total savings, Discovery said. This means you would need R10.8 million saved to draw 4% or R432,000 annually. Put another way:

For example, Bengen’s rule is based on the average long-term annual returns (since 1926) of shares and bonds being 10% and 5.3%, respectively.  75% rule Plan to have 75% of your current pre-tax income, says financial services firm, Sanlam. “You will most likely need less than 100% of your current income to live comfortably when you retire as some expenses fall away once you retire.” Ask yourself these questions:

Allan Gray offers a similar guideline around saving. Aim for an income of 75% of your final salary.

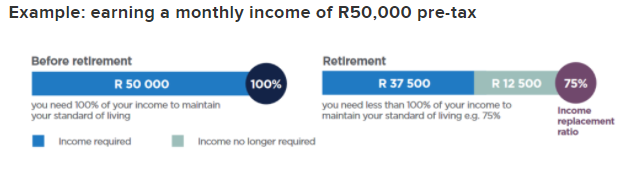

It is widely held that a retirement income equal to 75% of your final salary will allow you to live comfortably during retirement, it said. “This figure accounts for the adjustments many people make as they age, for example, no further retirement savings contributions but higher medical costs.” To assess how much you will potentially need, consider the following factors:

Aim to put away at least 17% of your salary from age 25 “Assuming that you will be comfortable living off 75% of your pre-retirement salary, our research indicates that saving 17% of your salary is a reasonable starting point for the 25-year old saver. “This amount increases dramatically the later you start. You need to save 22% if you start saving at 30, up to 42% if you start at 40, and up to 59% if you start at 45,” Allan Gray said. It is important to note that these numbers are simply averages and assume a consistent, inflationary salary increase each year, that you retire at 65 and that you earn an average return of consumer price inflation (CPI) plus 5%, it said. The 15% rule The general rule of thumb for a comfortable retirement is 15%, noted Gus Van Der Spek, a developer of upmarket retirement village Wytham Estate. “15% of your salary should be put aside for your entire working career of around 40 years. For those wanting to retire in luxury, 20%-plus is advised. Also, bear in mind that what R1 is worth now will differ by the time that you retire,” he said. Van Der Spek shared the advice given to him by financial planners saying, “multiply your needs by 300. Simply put, if you currently live on R50,000 per month, multiply this by 300 to determine what you will need to maintain a luxury lifestyle post the age of 60.” Van Der Spek’s comments dovetail retirement expert Andre Tuck, a senior Investment consultant at 10X Investments. Tuck pointed to three old school ways to ‘guesstimate’ your retirement goal:

He added, however, that if you are hoping to do things you didn’t do during your working years, for example, travel, you should rather multiply your final salary by 17, or even 20.

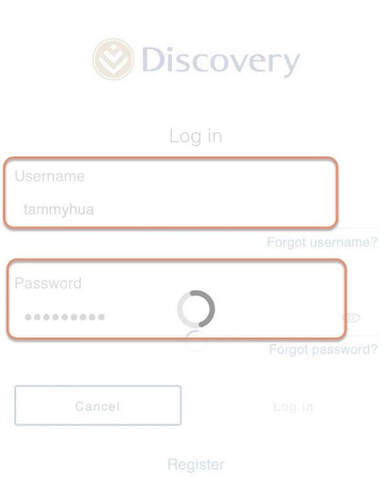

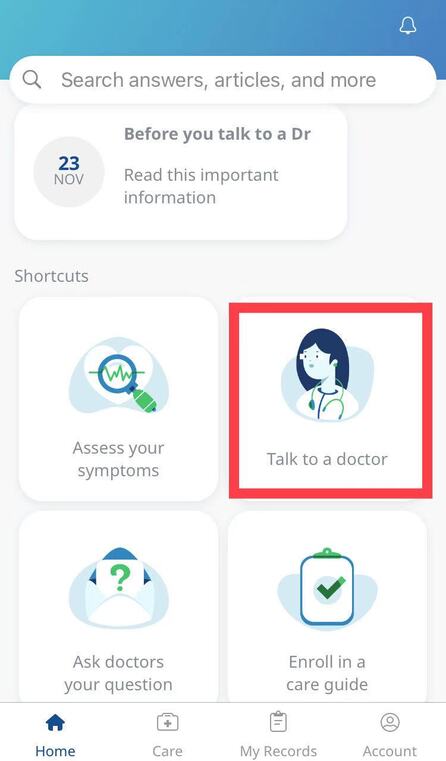

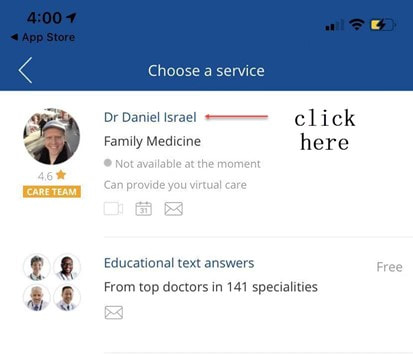

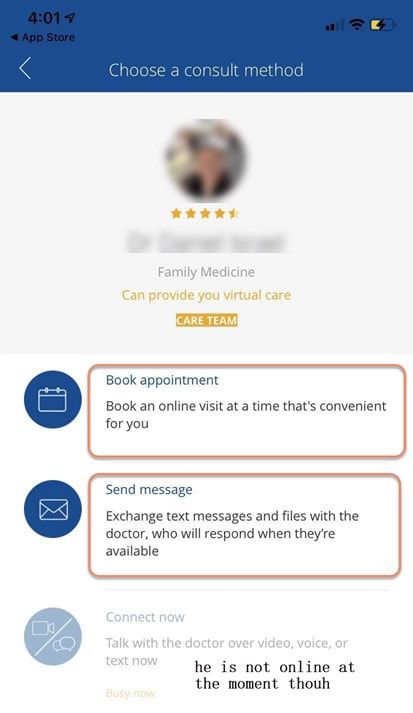

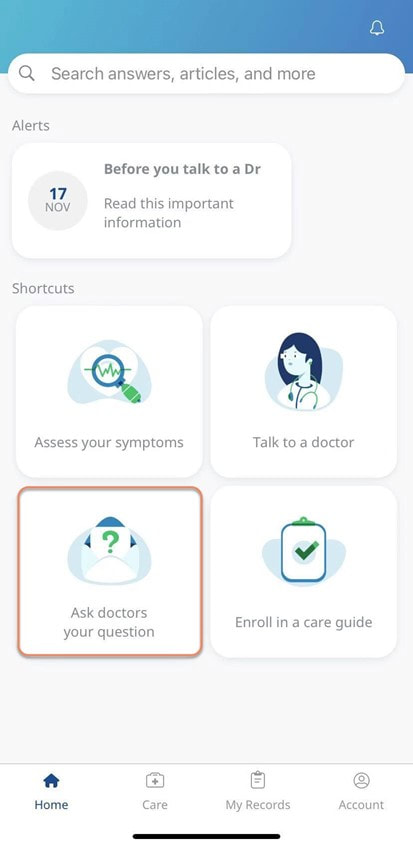

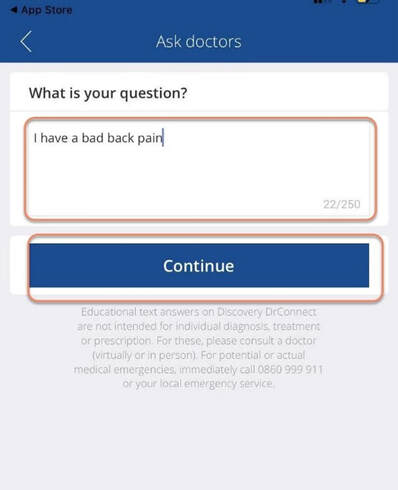

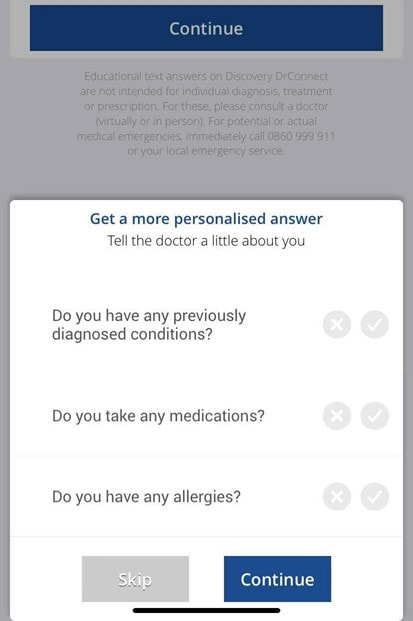

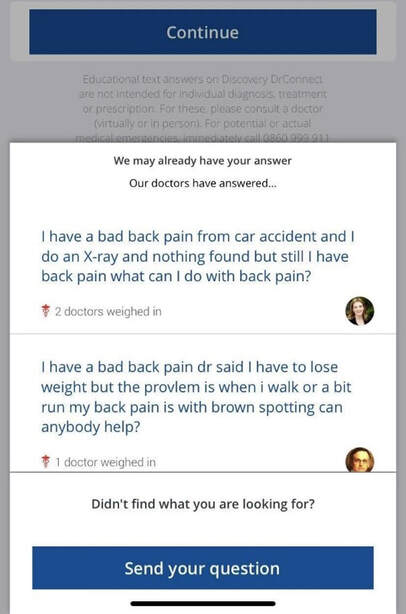

“The more money you have available to invest once you retire, the better your lifestyle will be and the more likely you will be to withstand the impact of unexpected events, such as the current pandemic,” he said. If you would like to speak to a Financial advisor about planning for your retirement contact Kevin tel(011)658-1333 email: service@daberistic.com Source: Businesstech In partnership with Morningstar: South African corporate credit is one of the less covered investments in the fixed income universe. The market is skewed towards the financial sector and characterised by structural illiquidity. In partnership with Morningstar, Keeping it simple this savings month. In a world of information overload, social media, the increasing size of the investable universe, cryptocurrencies and Robinhood trading – to name but a few – it can be easy to get distracted from what is important. With so much market noise, it has become more important than ever to identify the things investors should not care about. We outline our top five below. I have used up my Medical Savings Account, can I still see a doctor? I am a loyal customer of Discovery and have been a member of Discovery Health since I entered the workplace in 1996. During my start-up years from 2006 to 2009, I moved to my wife's company medical aid Sasolmed, then later changed to Medicover. In 2009, I returned to Discovery Health. My medical aid option has been Classic Delta Saver for the last few years. I think this plan is value for money, suitable for our family of five. However, towards the end of the year, I often run out of Medical Savings Account, then I have to pay out of my own pocket to see a doctor or to buy medicine. This plan provides Day-to-Day Extender Benefits: even when the savings account is used up, you can still visit a designated GP and be covered by Discovery. Discovery Health covers up to 6 network GP visits, which is helpful. The protocol to access this extender benefit has changed since the end of last year, however. Although I am a healthcare broker, I forgot to keep up with the change. I still wanted to use the same procedure as I have used in the past. I then ran into a wall and the Discovery Health refused to pay. What is going on here? There were like R30 left in my MSA. In order to use the extender benefits, I went to Dis-chem pharmacy to buy over-the-counter medicine. The intention was to reduce the savings account to zero. I asked the pharmacist to deduct from my savings account first, and I would pay the balance in cash. I also asked the pharmacist to confirm that there was no money in my savings account. After that, I made an appointment for my son with a designated family doctor, to assess his spinal injury. After the consultation, the front desk staff said that the claim had been submitted to Discovery Health, so I didn't have to pay for it. I thought that this extender benefit was really good, only to receive a claim statement from Discovery a few days later that they did not pay. I thought there was some misunderstanding. Upon further investigation, it turned out that I didn't apply the knowledge acquired. At the end of last year, Discovery announced a new process to use extender benefits. The first is to go to a network pharmacy such as Dis-chem to see a nurse. Or download the Dr Connect app on your mobile phone to consult with a doctor online. The infographic below illustrates:  Below are the steps of how DrConnect works 1. Download DrConnect on the smart phone  2. Open the APP and log in  3. Log in with your Discovery Username and Password  4. You will see 4 categories: Assess your symptoms, Talk to a doctor, Ask doctors your questions, Enrol in a care guide.  5. If the GP you have visited before is also a DrConnect network doctor, he/she will appear here. Click the doctor for more options.  6. You can choose to book an appointment, send them a message about your queries, or connect for a video consultation (when they are online).  7. Or, on the main page (home), choose to ask a question.  8. Type in the question you would like to ask.  9. Answer a quick health survey or click Skip to skip it.  10. There may be other people have asked a similar question, which already has an answer to, see if you can find your answer here, if not, click to send your question.   Discovery continues to lead the industry by rolling out exciting benefits and offerings: Mental wellbeing Shari'ah compliance arrangement Infertility and assisted reproductive therapy benefit Hospital network and day surgery updates New clinic and other services for employers Diabetes care programme Chronic Illness Benefits Co-payments and deductibles To find out more, please click on each tab below. Mental wellbeing Statistics according to WHO shows one in four people in the world will be affected by mental disorders at some point in their lives, this positions mental disorder amongst one of the leading causes of ill-health worldwide. Mental ill-ness often left undiagnosed and with 84% of adults never receiving treatment and this impacts society and WHO estimates cost to global economy may exceed $16 trillion by 2030. Discovery’s approach to alleviate this disorder, they have introduced management in mental wellbeing. Below programs offered are:

Shari’ah compliant arrangement From 2021 members from our Muslim community can appoint to have their contribution and claims across all plans to conform with Shari’ah principles through the Shari’ah compliant arrangement. • Model is compliant and is based on Takaful principles • Process flow happens in an acceptable manner • No interest earned or paid at any stage • No ambiguity in contracts • Members’ interests are protected • Investments are managed in Shari’ah Compliant manner • No interest earned or paid on Shari’ah Compliant arrangement. Funds will be invested in a compliant manner allowing members opportunity to earn profit on Medical Savings Account balances. • Members that partake in this arrangement attain affirmation on their contribution and balances remaining after settlement of claims and other expenditure will be invested in Shari’ah compliant investments. Infertility and assisted reproductive Therapy benefit When a couple is looking forward to building a family and the incapability to fall pregnant is aggravating. It affects many families and takes a emotional toll, however, many infertility cases can be remedied through treatment such as drug, surgical repair and assisted reproductive techniques including intra-urine insemination (IUI) and in vitro fertilisation (IVF). Taking a leap of faith on possibility to become a parent can come with a price tag, an average of R65000.00 – R85000.00 for a single IVF treatment cycle, this may be a hefty cost for many families in which will hinder and or have reservations from taking on this treatment. Discovery would like to support couples/ families distressed from infertility with introducing cover for Assisted Reproductive Technologies (ART) and the benefit will include cover for: • Up to two cycles of ART if Scheme’s benefit and clinical entry criteria are met. • This includes a series of care for the progress of the full duration: consultations, ultrasounds, oocyte retrieval, embryo transfers, admission costs including lab fees, medication and embryo and sperm storage. • The total limit of R110 000.00 per person per year at Discovery health rate applies. • Members will be subject to 25% of the costs and any excess above the Discovery Health Rate. • This benefit will be attainable at Southern African Society of Reproductive Medicine and Gynaecological Endoscopy (SASREG) accredited centres only and subject to clinical pathways and protocols. • Lastly, the benefit is only available to female members that has been on Executive and Comprehensive Plans for at least 2 years and the age between 25-42 years old. Chronic Illness Benefits

Diabetes Care Programme 2021 Premier Plus GP network will become the Designated service provider for members with Diabetes on the comprehensive plans. It is supported by the extensive coverage offered by the Premier Plus GP network and the clinical outcomes achieved by the diabetes care programme. The chosen GP will be member’s DSP for the ongoing management of diabetes as well as cardiovascular conditions. Statistics has shown in improvement when member’s care is coordinated by a single doctor. Hospital Network Updates and Day Surgery New hospitals will be added, and some existing hospitals will be replaced with region specific substitutions for 2021 to ensure continued optimisation of the Delta, Smart and KeyCare hospital networks In the Day Surgery, they will extend this offer to Comprehensive plans given focus on provider and patient safety because of COVID-19. The 2021 new hospital network and day surgery lists will be published by the end of October 2020. Limits, Co-payments, deductible and Thresholds

Next: Vitality 2021 - To Help members stay motivated Co-payments For Endoscopic Procedures

New Clinic and Other Services for Employers Daily monitoring of COVID-19 exposure, prevalence, and disease progression:

|

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|