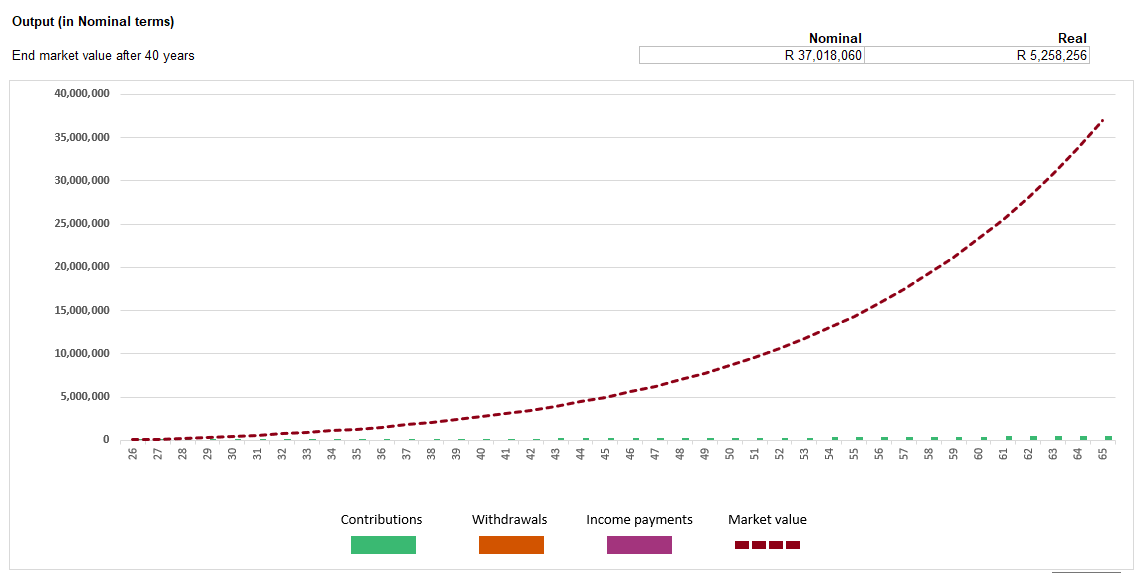

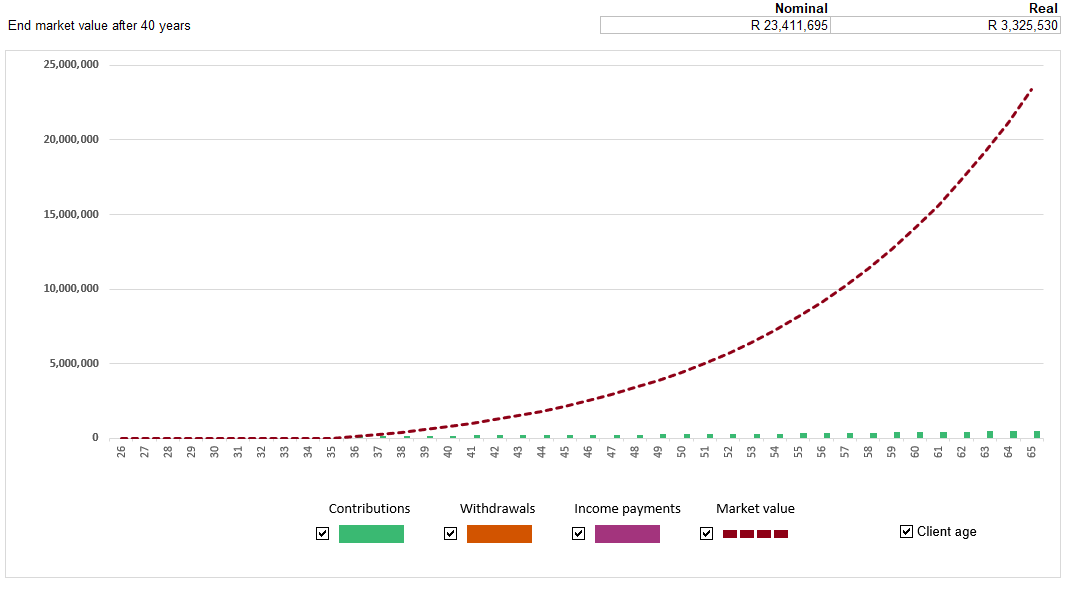

Last month I talked about Step 4 - Keep a record of your spend. Let's continue with Step 5 - Invest 15% of your earnings. Robert Kiyosaki, a leading personal finance and business coach of our time, advocates "Pay yourself first". People who choose to pay themselves first allocate money to the asset column of their balance sheet before they’ve paid their monthly expenses. Essentially, you set aside a specific amount of money right off the bat, and then live off what’s leftover. And that’s how wealth grows. In South Africa, this means putting 15% of your monthly pay into a retirement annuity, a tax-free investment, an offshore investment, or getting a business education or subscription. Let's unpack this. When I have my first meeting with new financial planning clients, one of the areas we cover is Personal Balance Sheet. Personal Balance Sheet essentially is a list of a person's assets and liabilities. At the end we calculate a person's Net Asset Value (NAV) by subtracting liabilities from assets. Many people have no ideas of what are assets, what are liabilities, and the differences between the two. They work hard, they try to get a better income. After many years, they wonder why they have little to show for it, and where money has gone to. They are busy paying everyone else, the taxman, banks, credit card companies, municipality, Eskom, DSTV, cellular providers. Then they have no money to pay themselves. So they go through their life, by the time they get to 40s or 50s, then realise they don't have enough saved up for retirement. It is important for us to instill in our teenage children, young adults the importance of savings, that they should start saving 15% of their income when they start their first job or business venture. Don't rely on what your employer would do for you. In the past, many corporates in South Africa would provide generous employee benefits, including a pension after retirement. Due to changes in accounting standards, increased competition and tougher economic environment, many corporates have cut back on employee benefits. Just about all have moved to Defined-Contribution arrangements, they no longer guarantee employees a pension after retirement. We need to educate our children (and ourselves) to create that financial nest egg ourselves. No one else is going to do it for us. Not the employer, not the government, not your parents. Starting early is key. If a young person in their twenties start their first job, and save 15% of their income every month, invest wisely, then by the time she gets to 65, she should have built up a retirement capital, a sum of money to draw an income from. What we call "comfortable retirement." Below is a chart illustrating a 25-year old earning R40,000 a month, saving 15% of her income per month (i.e. R6,000). Assume her income increases at 5% per annum, and she keeps her savings rate at 15%. Also assume she gets 8% return on her investments. At 65, the projected capital she will built up is R37 million.  If she delays the decision to invest until age 35, i.e. she only starts saving 10 years later, then at 65, the projected capital she will build up is R23.4 million. See the chart below. While still significant, it is 37% less than if she had started at age 25.  So a 10-year delay will cause her wealth at age 65 to reduce by 37%! Investment products for long-term investmentYou may consider using the following products for investing for long-term: Tax-free investment account: while limited to R3,000 per month or R36,000 per year contribution, you invest tax-free, and you can invest up to 100% offshore. Watch this video to get the basics of a Tax-Free Investment account: Retirement annuity: This is designed for saving for retirement, offers great tax benefits. Watch this video to understand the basics of a Retirement Annuity: Offshore investment: This allows you to invest in hard currencies such as the US Dollar, Euros and Pounds, by converting your Rands into these currencies and investing offshore. This is great for diversification, and accessing investment opportunities not available in South Africa. Unit trusts: This allows you to invest in a wide range of collective investment schemes. You should invest in a number of funds for diversification, and your portfolio should be suitable for your risk profile. Endowment policy: This forces you to invest for a minimum period of five years, investment growth is taxed within the policy, so when it pays out you receive the proceeds tax free. Watch this video to understand the basics of an endowment policy: Contact us today at service@daberistic.com if you would like to speak to a Financial Advisor, on how best you can invest 15% of your money, to create your wealth.

0 Comments

Leave a Reply. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|