|

Many will tell you how vital life insurance is, particularly if you have a family. Mainly, this is because life insurance is a way in which you can make sure that you can provide financial support to your loved ones after your passing. This generally includes cover for the cost of the funeral. The question is, when do you need to get life insurance? To help you work this out, we have explained when and why you need life insurance.

When you’re young & single This is because young singles still have certain financial responsibilities, like car payments, Internet contracts, cellphone contracts, and the cost of their own funeral. They might even help support an elderly parent or have others that they care for financially. A life insurance policy will go towards paying off these debts and supporting these loved ones. When you’re buying a home When you approach a bank to obtain a home loan, part of the approval process will include getting life insurance. Most banks require that you purchase life insurance so that this policy can be used to pay the amount owed on the bond should you pass away before your home loan is fully paid off. When you’re part of a no-kids-couple When you become part of a couple, you make big purchases together and you start living according to your combined income. Even if you are both working and are therefore not being supported by one another, your lifestyle most likely takes both of your incomes to maintain. Life insurance will help your partner pay off big purchases, cover the funeral costs, and will go towards maintaining their lifestyle. When you’re starting a family Life insurance should be purchased if you are considering starting a family or you have already started one. Should you pass away, the last thing your partner and children need to worry about is the finances, including the cost of the funeral. Life insurance pays out a lump sum, which your main beneficiary can decide what to do with. This means that your forethought and planning will help pay for your family’s day-to-day expenses, as well as ensuring that your children get a good education. It’s important that you carefully assess your life and consider whether or not you can afford not to have life insurance, especially as you get older. This type of cover can get more expensive if you choose to purchase a policy later on in life. Source: MSN Money Please contact Kevin or Thato in our Life Department; email life@daberistic.com , or tel 083-633-4671, to find out whether you have sufficient life cover.

0 Comments

Seeking guidance from a trusted financial adviser is more critical than ever in current difficult market conditions, says Peter Dempsey, deputy CEO of the Association for Savings and Investment South Africa (ASISA). Investors tend to panic in times of market volatility, economic turmoil and political uncertainty, often resulting in knee-jerk investment decisions that are seldom sensible, adds Dempsey. “It’s important to recognise that times are tough both locally and globally, and that every country has its own problems. The role of an adviser is to guide you through the noise, and help you to make best decisions for your unique circumstances,” he states.

The value of advice Dempsey notes that successful investors have a solid plan and do not sway from their path in difficult times. He points out that most successful investors, even those who are very experienced, work with financial advisers. “Research demonstrates that advised investors remain more disciplined, better protected and have more assets, as financial advisers are able to guide them in balancing the need to face reality with the ability to recognise opportunities and the willingness to act. “Advised investors are therefore able to accumulate more assets and build a balanced portfolio, manage their financial risk wisely, smooth their consumption to save for times they may not have, and optimise their personal balance sheets,” he states. Dempsey explains that a good financial adviser will look at your unique financial situation holistically, and help you implement a watertight financial strategy with a long-term view that will be managed to adapt to your changing needs as you move through various life stages. He adds that this strategy is not simply about choosing investments or unit trusts, but will also involve ensuring that you are prepared financially for planned events such as retirement, and are protected against unforeseen events such as death or disability. “Advice is therefore key to making decisions that will increase or preserve your financial well-being for an independent financial future.” Click here to read more Source: Risk Africa Magazine Please contact Kevin a certified Financial Planner; email invest@daberistic.com , should you like to discuss your current investment portfolios and options The end of the tax year is fast approaching – but there is still time to take advantage of some of the incentives the government has put in place to encourage savings. The introduction of the tax-free savings legislation last year has added an extra arrow to the quiver of tax-efficient options available to investors. Options are great, but having to choose often stops people from acting and can get in the way of our good intentions. If pressed to make a decision between a unit trust-based retirement annuity (RA) or a unit-trust based tax-free investment (TFI) product, which should you choose?

Begin with the end in mind At this time of the year maximising tax breaks is a common, top-of-mind goal. However, it is important to look at your portfolio holistically, either on your own or with the help of a good,independent financial adviser, to ensure your decisions fit in with the long-term plan. Let’s talk tax There has been much debate about the benefits of TFI products versus RAs. First, remember that both an RA account and a TFI savings product grow free of dividends tax, income tax on interest and capital gains tax. In our simple example1., because you are compounding all gains tax free, your investment value at the end of 30 years would end up roughly 45% higher than in a discretionary investment. The main difference between the two products is that an RA offers tax savings now, i.e. you pay less tax now because you make contributions with earnings on which you have not paid tax, but you will pay tax later, i.e. you defer paying tax. With TFI products, on the other hand, you use after-tax money to invest, but you pay no tax later; your withdrawals are completely tax free. So which offers the best deal tax-wise? Let’s consider the detail: Only 15% of non-retirement funding income is eligible for a tax deduction. This is set to change on 1 March 2016 to allow a tax deduction of up to the higher of 27.5% of taxable income or remuneration capped at R350 000 per year. This is a solid increase and will make the tax savings on an RA more relevant for higher income earners (albeit lower for the very high earners where the new annual rand cap is less than the previous 15% limit). Apart from deferring tax in an RA, the tax saving comes from paying a lower average tax rate on the benefits withdrawn from the RA at and after retirement, versus the tax saved on contributions. The first R500 000 of any lump sum you withdraw from your RA is currently tax-free (you can withdraw up to one-third, but this includes any pre-retirement withdrawals), and the rest of the benefit must be transferred to an income-providing product, such as a living annuity or a guaranteed life annuity. When income tax is paid on this benefit, you are likely to be taxed at a lower rate than when you were making contributions, which is where the additional tax savings comes in. Because of this, a disciplined investor paying income tax at marginal rate of 36% could pay more than 50% less tax on their retirement savings over their lifetime. This obviously varies depending on each investor’s personal circumstances, salary, age, how much and how long they have saved and any withdrawals made along the way. When comparing to a TFI product, the difference is that you have a future tax liability, whereas in a TFI your tax would already have been paid, but at a higher rate. What’s the catch? While the tax benefits of the RA and TFI are clear, it’s important to be aware of the restrictions before making a decision. RAs are governed by the retirement fund regulations, specifically Regulation 28 of the Pension Funds Act, which limits the exposure you can have to more risky asset classes, such as equities and offshore investments. In TFI products, there are no restrictions on asset classes but you can only invest in investments that charge fixed fees, which limits your selection. We have recently launched afixed-fee version of our flagship Balanced Fund to accommodate investors who would like to invest in our Tax-Free Investment Account. Another critical point, is that you can only invest R30 000 per year in TFI products. This is the maximum limit for all TFI accounts in your name, across product providers. If your goal is to save for retirement, the maximum annual contribution of R30 000 in a tax-free savings account may not be enough to sustain your lifestyle, and if you over-contribute SARS will hit you with a hefty 40% tax penalty. Access to cash may be another deal breaker: your investments in an RA cannot be accessed before the age of 55. You can access your TFI investment at any time. However, withdrawing from a TFI account impacts negatively on your lifetime investment limit of R500 000 – you cannot replace money that you have withdrawn. Other distinguishing features Both the Allan Gray RA and TFI2 are protected against the claims of creditors and do not form part of your insolvent estate. This feature is not applicable to all TFI products but it is applicable to the Allan Gray TFI, which is a life policy. You may nominate beneficiaries for an RA, although the trustees determine the allocation between your dependants and nominees. You may nominate beneficiaries when the TFI is a life policy. RAs are exempt from estate duty, whereas TFIs forms part of your estate and attract duty, although there are no executor fees if beneficiaries have been nominated. Which product wins? From a retirement savings perspective, in most cases RAs offer the best tax deal. However you need to be able to live with the restrictions described above. For long-term discretionary investments, it probably makes sense to put your first R30 000 into a TFI product. Remember, however, that you will need to be disciplined and resist the temptation of withdrawing from your TFI account. You only get to enjoy the long-term compounding benefits if you don’t dip your hands into the cookie jar along the way. Source: Allan Gray Please contact Kevin or Thato, email: invest@daberistic.com, if you have any queries about Retirement Annuity or Tax Free Investments Around this time of the year, we would like to remind you to consider topping up your retirement annuity fund. According to the current legislation, you may contribute up to 15% of your taxable income (strictly speaking, non-retirement funding income) to a retirement annuity fund and enjoy tax deductions. As 28 February is the end of the tax year, you must calculate and pay the additional amount to your retirement annuity prior to this date, in order to qualify for tax deductions and tax refunds.

Below is an example of topping up your retirement annuity: Mr Thomas has a monthly salary of R50,000. In December he received a bonus of R100,000. Every month he contributes R3,000 to a personal retirement annuity fund. His annual income is then R50,000*12 + R100,000 = R700,000. The maximum tax-deductible contribution to retirement annuity is R700,000 * 15% = R105,000. Over the year he has contributed the following to retirement annuity: R3,000 * 12 = R36,000 The additional amount he may top up in his retirement annuity (RA) is R105,000 Less R36,000 R69,000 He can expect a tax refund of R105,000*39% = R40,950 from his retirement annuity contributions. Should you have any queries on retirement annuity , please contact Kevin or Thato , tel 011-658-133, or email invest@daberistic.com Introducing the R12/$1 Life Plan Limited Offer! If you buy a Dollar Life Plan policy before 31 March 2016, you can get a guaranteed exchange rate of R12/$1 on their premium for the next three years! In November 2014, Discovery Life launched the Dollar Life Plan, a first-to-market offshore life insurance policy that offers clients comprehensive risk protection in US dollars. With the Dollar Life Plan, clients can be sure that their risk protection will remain relevant in the long term, regardless of their changing lifestyle needs. Why offshore life insurance makes sense: 1. Sound long-term financial planning : With an offshore life insurance policy, denominated in US dollars, clients are protected against the financial impact of a life-changing event – no matter where they may find themselves in the future. 2. Matching liabilities : Many clients either have, or could in the future have, offshore liabilities such as a bond, children’s education costs or estate duty in a foreign country. Clients may also be impacted by a fluctuating rand, which typically results in an increase in the cost of goods and services available locally. Risk protection denominated in dollars is therefore critical to ensure that a client’s liabilities are fully matched. 3. Diversification : Discovery Life provides an efficient vehicle for clients to supplement and diversify their retirement savings into offshore markets by allowing them to convert their future health and wellness into a tangible offshore financial asset. Clients can further supplement their retirement savings in dollars through three unique features:

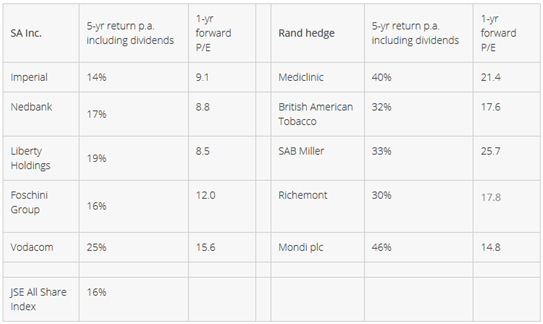

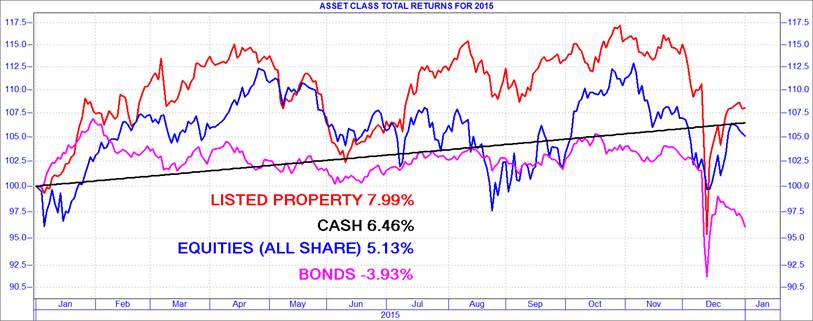

You can increase the value of their rand with future certainty! For a limited time only, clients will be able to pay the premiums on a new Dollar Life Plan at a substantially lower exchange rate than the market. Clients will charged a premium based on a maximum exchange of R12/$1 for the first three years of their policy. This is provided that the exchange rate remains less than R20/$1 and if the exchange rate is higher than (or equal to) R20/$1, clients will be charged a premium based on an exchange rate that is 20% less than the rest of the market. Click here for full brochure Source: Discovery  Website: www.daberistic.com Email: invest@daberistic.com Tel: 011 658 1333/1391 Dear Client / Business Associate Compliments of the News Season In our first edition of Investment Focus 2016 we plan ahead for the year on how to handle Investments, the article on Best direction for your investments in 2016 gives a guide on the market share and which markets to target as well as how the past five years’ share performance and current valuation of five well-run rand hedge companies versus five well-run SA Inc companies listed on the JSE. The one thing that is the hottest news in South Africa currently is, the New Tax law in regards to Tax incentives, with National Treasury encouraging us to save more for retirement by significantly increasing the tax incentives, the article More for the future you, less for the tax man is able to clearly explain the new Tax law. Our articles on 2015 Asset Class Total Returns - Listed Property the best performer in a volatile year, Prudential December Fund Fact Sheets help us look back at how markets performed in 2015. We hope that 2016 be a great year with great Financial return for all our Clients ….All the best Best direction for your investments in 2016 It may come as a surprise that, when viewed from a foreigner’s perspective, the JSE All-share index has not increased in US dollar terms since October 2007. In rand terms, the prices of local equities more than doubled over this period. It’s also worth noting that since 2011 our local market has underperformed the world’s developed markets, as measured by the MSCI World Index, by 119% as the rand depreciated from R6.61 to R14.20 per dollar. Given the rand weakness and superior performance by developed market equities, our clients regularly ask us whether they should take more money offshore. At our client roadshow in early 2011, we advised clients to shift their portfolios towards developed market shares given the over-valued rand at the time and relatively attractive valuations of these markets. This was met with some reluctance given that South African shares had outperformed developed markets by more than 500% over the previous decade. The superior economic growth prospects of emerging markets relative to the developed world were also emphasised, while many investors remembered the painful consequences of moving money offshore at the worst possible time after the rand collapsed in 2001. Recent experiences and performances influence investor sentiment, but our investment philosophy takes us back to valuation/price as the primary consideration for investment decisions, while taking account of the prevailing trends and perspectives in the market. In line with what we have advocated since 2011, our asset allocation portfolios have invested the maximum weight in offshore markets that prudential legislation allows. In our equity selection, we have tilted our portfolios towards ‘rand-hedge’ companies that derive the majority of their earnings offshore and away from so-called SA Inc companies whose fortunes depend on the domestic economy. This has benefited portfolio performance, but we continuously reassess our positioning. The table below shows the past five years’ share performance and current valuation of five well-run rand hedge companies versus five well-run SA Inc companies listed on the JSE.  Click here to read more Please contact Kevin or Thato, email: invest@daberistic.com, if you have any queries about investments Source: Finance24 More for the future you, less for the tax man The tides are changing in the retirement savings space, with National Treasury encouraging us to save more for retirement by significantly increasing the tax incentives. This is one of several important changes that will go ahead from March this year, now that the President has approved the Taxation Laws Amendment Bill, 2015, which was passed by both Houses of Parliament at the end of last year. Gifts from SARS The wait is over for retirement fund members, who will enjoy increased tax deductions from their contributions to retirement funds. This includes provident funds, for which members were not previously able to claim a deduction. The tax deduction of up to 27.5% of the greater of taxable income or employment income, subject to an annual ceiling of R350 000, will come into effect. Another change is that employer contributions to occupational pension and provident funds will be included in the gross income of employees as a fringe benefit. This means that employees will be able to treat these contributions as their own when calculating their tax deductions. These deductions are subject to the limits mentioned above. You will have to buy an income-providing product…Retirement funds will also be aligned, ironing out some of the differences between the different products. One of the key changes is around ‘annuitisation’ – the process of converting retirement savings into a stream of future income. From 1 March, provident fund members, like retirement annuity and pension fund members, will only be allowed to take one-third of their retirement savings as cash and they will have to use the rest of their nest egg to buy a product that pays them an income during retirement. “Treasury has stressed that vested rights will be protected –i.e. the new rules will not apply to historic savings or to growth on those contributions.” …unless you are about to turn 55…If a provident fund member is 55 or older on 1 March, the new requirement will not apply. Any accumulated retirement savings as at 1 March, as well as new contributions and growth after 1 March, can still be taken as a cash lump sumat retirement. …or you have saved under R247 500 Members with a retirement benefit at retirement less thanor equal to R247 500 will be allowed to withdraw the entireamount without the need to purchase an annuity, as of March.This is an increase on the current value of R75 000. Click here to read more Please contact Kevin or Thato, email: invest@daberistic.com, if you have any queries about retirement funds or Allen Gray offerings Source: Allan Gray 2015 Asset Class Total Returns - Listed Property the best performer in a volatile year SA listed property was the best performer with a total return (income and capital) of 7.99% in ZAR in 2015  Global Listed Property (Developed Markets)

Please contact Kevin or Thato, email: invest@daberistic.com, if you have any queries about any investing Source: I-Net Bridge Prudential December fund fact sheets In December the US Federal Reserve finally raised interest rates for the first time since the 2007 Financial Crisis amid supportive economic data, easing some of the uncertainty hanging over global investors and pushing the US dollar still stronger. Chinese economic data also improved, partly relieving another source of uncertainty. However, global growth prospects, particularly emerging markets, continued to be revised downward, driving commodity prices, EM currencies and EM financial markets weaker (Brent crude lose 17.2% during the month). Assets continued to flow back to the US from riskier destinations. Most equity markets lost ground, as did bonds. Developed market equities produced a total return of -1.7% (MSCI World Free Index) and the MSCI Emerging Markets Index fell 2.2%. Global bonds were largely flat as the Barclays Global Aggregate Bond Index (US$) returned 0.6%, while precious metal prices fell: gold was down 0.34%, platinum -15.9% and palladium -20.5% (all in US dollars). South African bonds, listed property and the rand fell sharply amid the global environment and were all punished by "Nene-gate" on 10 and 11 December. Equities also lost ground as financial shares were hard-hit. The average equity fund returned -2.2% for the month, while the average high equity balanced fund delivered -0.2% (according to Morningstar, using ASISA categories). Multi-asset low-equity funds averaged -0.1%, and multi-asset income funds produced -0.3% on average. SA equities were lower in December in line with other developing markets: the FTSE/JSE All Share Index posted a total return of -1.7%. The All Bond Index suffered a 6.7% loss, and SA listed property returned -6.1%. Inflation-linked bonds were down 1.8%, while cash returned 0.5%. Over the month the rand weakened by 6.9% against the US dollar, by 5.0% against the pound sterling, and by 9.5% against the euro, making offshore assets the best performing for December. Prudential High Yield Bond Fund – The fund has returned -5.0% over 1 year and 1.4% over 3 years. This compares to -3.9% for the All Bond Index over 1 year. Long-dated bond yields have become even more attractive in the wake of December's weakness, rising to over 10%, so that the fund remains overweight duration. Please contact Kevin or Thato, email: invest@daberistic.com, for any queries about Prudential investments Source: Prudential Daberistic contacts details Kindly note the following to ensure you get the correct person to assist you with your insurance and investment queries. Life insurance and investments: Kevin Yeh, Thato Merementsi, Nicole Smith Tel 011 658 1333, email life@daberistic.com Medical aid / gap cover:Namhla Zwane,Sophie SuTel 011 658 1333, email health@daberistic.com Short-term insurance (Personal and Business): Thomas Mooke, Calvin Yen, Tel 011 658 1333, email shortterm@daberistic.com Retirement funds: Kevin Yeh, Tel 011 658 1333, email employeebenefits@daberistic.com Tax, Accountancy and Auditors: Su-Lan Chen or Su-Chin Chen, Tel 011 658 1333, email finance@daberistic.com 24-hour emergency cellphone number: 076 200 5488. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|