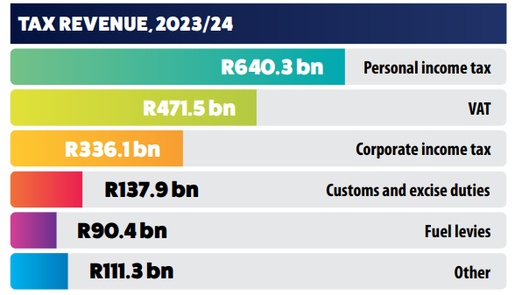

Where The Tax Comes From Highlights Of The BudgetSome of the things that stood out was incentivisation of rooftop solar, energy support packages as well as relief in terms of personal income tax. Energy support package

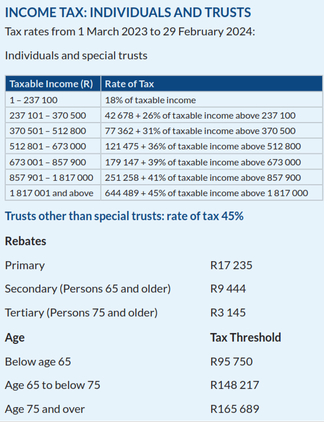

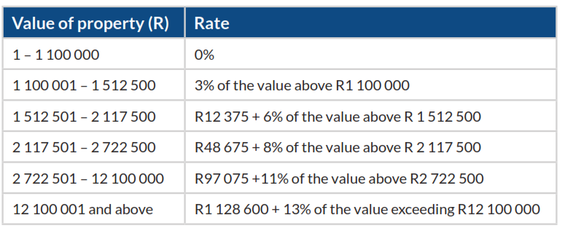

Income Tax - Individuals & Trusts Dividends: Dividends received by individuals from South African companies are generally exempt from income tax, but dividends tax, at a rate of 20%, is withheld by the entities paying the dividends to the individuals. Interest: A final tax at a rate of 15%, is imposed on interest from a South African source, payable to non-residents. Interest is exempt if payable by any sphere of the South African government, a bank, or if the debt is listed on a recognised exchange. Capital Gains Tax: Maximum effective rate of tax: Individuals and special trusts 18%, Companies 21.6%, Other trusts 36% Travelling allowance: Rates per kilometer, which may be used in determining the allowable deduction for business travel against an allowance or advance where actual costs are not claimed, are determined using the table published on the SARS Click here to view Transfer Duty: Transfer duty is payable at the following rates on transactions that are not subject to VAT: Acquisition of property by all persons:  Income Tax - Companies1. Small Business Corporations Taxable Income Rate of Tax 1 – 95 750 0% of taxable income 95 751 – 365 000 7% of taxable income above 95 750 365 001 – 550 000 18 848 + 21% of taxable income above 365 000 550 001 and above 57 698 + 27% of the amount above 550 000 2.Turnover for Tax For Micro Business Taxable turnover (R) Rate of tax (R) 1 – 335 000 0% of taxable turnover 335 001 – 500 000 1% of taxable turnover above 335 000 500 001 – 750 000 1 650 + 2% of taxable turnover above 500 000 750 001 and above 6 650 + 3% of taxable turnover above 750 000 Other Taxes, Duties and LeviesValue-added Tax (VAT): VAT is levied at the standard rate of 15% on the supply of goods and services by registered vendors. A vendor making taxable supplies of more than R1 million per annum must register for VAT. A vendor making taxable supplies of more than R50 000, but not more than R1 million per annum, may apply for voluntary registration. Certain supplies are subject to a zero rate, or are exempt from VAT. Estate Duty: Estate duty is levied on the property of residents and the South African property of non-residents, less allowable deductions. The duty is levied on the dutiable value of an estate, at a rate of 20%, on the first R30 million, and at a rate of 25% above R30 million. A basic deduction of R3.5 million is allowed in the determination of an estate’s liability for estate duty, as well as deductions for liabilities, bequests to public benefit organisations, and property accruing to surviving spouses. Donations Tax: Donations tax is levied at a flat rate of 20% on the cumulative value of property donated since 1 March 2018, not exceeding R30 million, and at a rate of 25% on the cumulative value of property donated since 1 March 2018 exceeding R30 million. The first R100 000 of property donated in each year by a natural person is exempt from donations tax. Securities Transfer Tax: The tax is imposed at a rate of 0.25 % on the transfer of listed or unlisted securities. Securities consist of shares in companies or member’s interests in close corporations. Tax on International Air Travel: R190 per passenger departing on international flights, excluding flights to Botswana, eSwatini, Lesotho and Namibia, in which case the tax is R100. Skills Development Levy: A skills development levy is payable by employers at a rate of 1% of the total remuneration paid to employees. Employers paying an annual remuneration of less than R500 000 are exempt from paying skills development levies. Unemployment Insurance Contributions: Unemployment insurance contributions are payable monthly by employers, on the basis of a contribution of 1% by employers and 1% by employees, based on the employees’ remuneration below a certain amount. Employers not registered for PAYE or SDL must pay the contributions to the Unemployment Insurance Commissioner. GrantsUpdated increases in social grants are as follows:

0 Comments

On 23 February 2022, Finance Minister Enoch Godongwana delivered the annual budget speech, providing an update on South Africa’s finances. Low economic growth, vast unemployment, increasing debt levels, coupled with South Africa still being in a state of disaster two years since the start of the Covid-19 pandemic, all contributed to a complicated juggling act for the Minister of Finance. Given the unrest witnessed in 2021 along with weak foreign investment, the 2022 budget had to be geared not only to curb unemployment and to stimulate economic growth, but to also give assurance to foreign investors. In the words of Minister Godongwana “we need to strike a critical balance between saving lives and livelihoods, while supporting inclusive growth. This budget presents this balance”. Finance Minister Tito Mboweni gave his budget speech on 24 February. Overall it is a taxpayer and investor friendly budget. Old Mutual has a nice summary of tax changes, we share with readers below.  One has to appreciate that it had to be a hard-balancing act for the Minister, however, many are concerned that these higher taxes may hurt the already weak economic environment, which will directly impact households.

Radical economic transformation, inclusive growth and equality were certainly an important feature of Minister Pravin Gordhan’s budget speech yesterday afternoon. The tone of the budget speech was very redistributive and echoed the President’s State of the Nation address a few weeks ago. It, therefore, came as no surprise that the Minister sidestepped the controversial issue of a VAT increase and opted to look to high-income earners to help raise an additional R28 billion. In terms of the progressive tax system, it makes sense to have those who earn more, pay more but there are some concerns that there could still be a risk to growth from the second-round of effects of these increased taxes. Revenue lagged behind the economy, which subsequently lead to an R30 billion shortfall by comparison with the budget estimate a year ago.The impact of a weak economic environment resulted in the shortfall experienced mainly in personal income tax, value-added tax and customs duties. Global growth prospects are looking better, which means that South Africa should benefit from the overall improved outlook, however, the 1.3% domestic growth expectation is still dependent on the implementation of reforms and barring any negative developments on the political front. From a revenue generation perspective, the usual suspects were targeted - being sin taxes and an increase in the fuel levy. Sugar tax does seem to be an inevitability but details need to be finalised. The implementation of the proposed carbon tax has also been kicked further down the road. From a rating agencies perspective, there were some positives and negatives. The Minister stayed on the fiscal consolidation course, as the pace of consolidation was unchanged. However, the budget did disappoint on the reform agenda especially regarding state-owned entities. Written: Tumisho Grater Source: Novare  Few weeks ago, Kevin Yeh (Key Individual of Daberistic Financial Services) attended the Sanlam Individual Life's product workshop and this what he wrote after attending it.

Last Tuesday I attended Sanlam Individual Life's product workshop, during which it launches a range of exciting critical illness benefits. But the highlight for me was its guest speaker, the renowned South Africa political analyst Justice Malala, in terms of his analysis of where is South Africa now, and where we are going in the future. ANC divided, with Zuma camp and Ramaphosa camp Unemployment: 8.9 million people, or 36.3% unemployed. The qualifications hierarchy: Only 4% of school starters eventually get a university degree. He expects minor cabinet reshuffle, probably Deputy Finance Minister being replaced by Brian Molefe. ANC NEC has 80 members, many depend on Zuma for ministerial jobs. Zuma will stay on as South Africa's president until 2019.No massive policy shift. Although Zuma talks about radical transformation, there will be no real change. However, a lot of talks will be on the land issue. He predicts if the voting for the next ANC President takes place today, Dlamini-Zuma will win against Cyril Ramaphosa. Malala predicts ANC will still win the 2019 national election, but EFF and DA will probably take control of Gauteng. In 2024 we are likely to see a coalition government, with EFF playing an increasingly important role. Source: Kevin Yeh Kevin Lings is the Chief Economist of Stanlib. He is a well know economist in the financial services industry, has an approach that makes complicated economic matters easy to understand. Attached is his presentation on the economic outlook of South Africa.

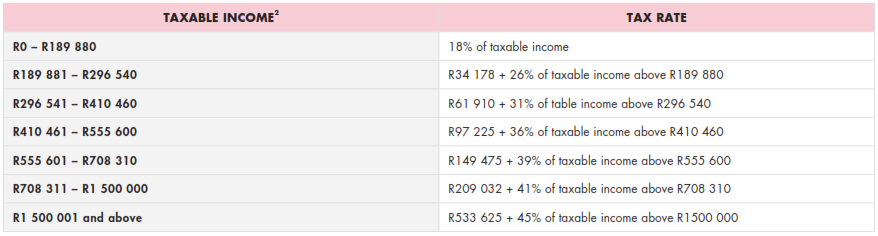

Click here to download presentation Source : Stanlib  INCOME TAX Individuals and special trusts A new top bracket has been introduced for personal income tax - individuals’ taxable income above R1.5 million per year will be taxed at 45%. Previously, the top bracket of 41% was set at R701 301. The new top marginal income tax bracket is accompanied by partial relief for bracket creep 1. The personal income tax rates for the 2017/2018 tax year are listed below.  Companies and trusts

TAX RATE The income tax rate for companies has remained unchanged at 28%, while the income tax rate for trusts (other than special trusts) has increased to 45%. TAX THRESHOLDS Tax thresholds have increased to: „„ R75 750 for taxpayers younger than 65 „„ R117 300 for taxpayers aged 65 to below 75 „„ R131 150 for taxpayers aged 75 and older REBATES The primary rebate (deductible from tax payable) has increased to R13 635 per year for all individuals. The secondary and tertiary rebates have increased to: „„ R7 479 for taxpayers aged 65 and older „„ R2 493 for taxpayers aged 75 and older INTEREST EXEMPTIONS Interest exemptions have remained unchanged at: „„ R23 800 per annum for individuals younger than 65 years „„ R34 500 per annum for individuals 65 years and older MEDICAL TAX CREDITS Monthly tax credits for medical scheme contributions will increase from: 1.R286 to R303 per month for the person who pays the contributions and the first dependant on the medical scheme 2.R192 to R204 per month for each additional dependant Bracket creep occurs when the income tax tables are not fully adjusted for inflation, and inflationary salary adjustments increase an individuals’ effective tax rate, reducing real income. As the increases to taxable income brackets, the tax thresholds, and the rebates are below the expected level of inflation, taxpayers will face a real increase in their effective personal income tax rate in 2017/2018. INTEREST WITHHOLDING TAX (IWT) AND DIVIDEND WITHHOLDING TAX (DWT) Interest Withholding Tax (IWT) on interest from a South African source payable to non-residents has remained unchanged at 15%. Interest is exempt if payable by any sphere of the South African government, a bank or if the debt is listed on a recognised exchange. Dividend Withholding Tax (DWT) on dividends paid by resident companies and by non-resident companies for shares listed on the JSE has increased from 15% to 20%, effective 22 February 2017. The exemption and rates for inbound foreign dividends have also been adjusted in line with the new local DWT rate, resulting in a maximum effective rate of 20%. TAX-FREE SAVINGS ACCOUNTS The annual limit on contributions to tax-free savings accounts has increased from R30 000 to R33 000. RETIREMENT LUMP SUM TAXATION At retirement: The retirement lump sum tax table is unchanged. The table below illustrates how retirement lump sums will be taxed. Click to read more If you have any queries on your personal or business tax, contact our Finance Department, email finance@daberistic.com, tel (011)658-1333 Source: Allan Gray |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|