|

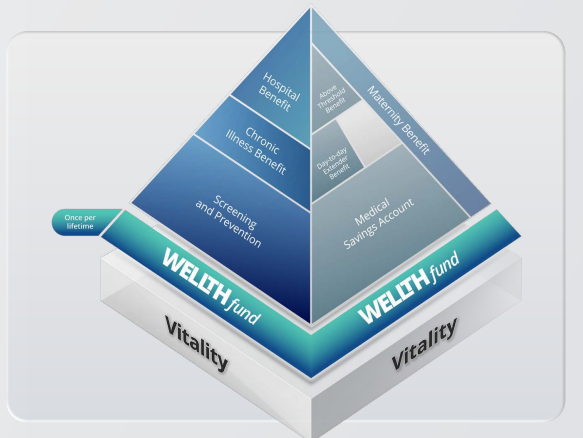

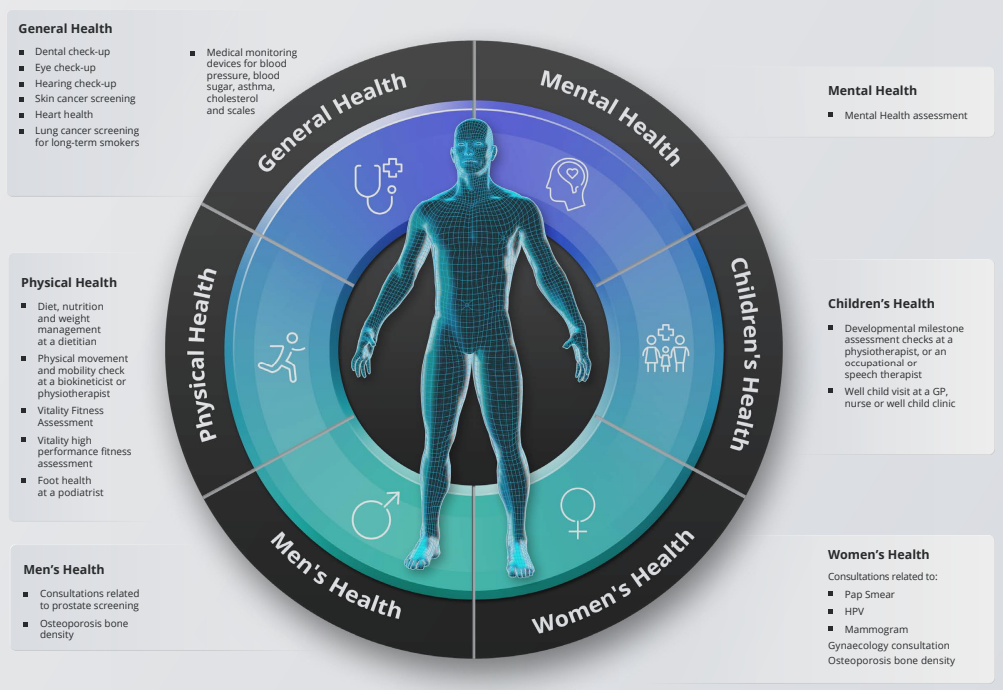

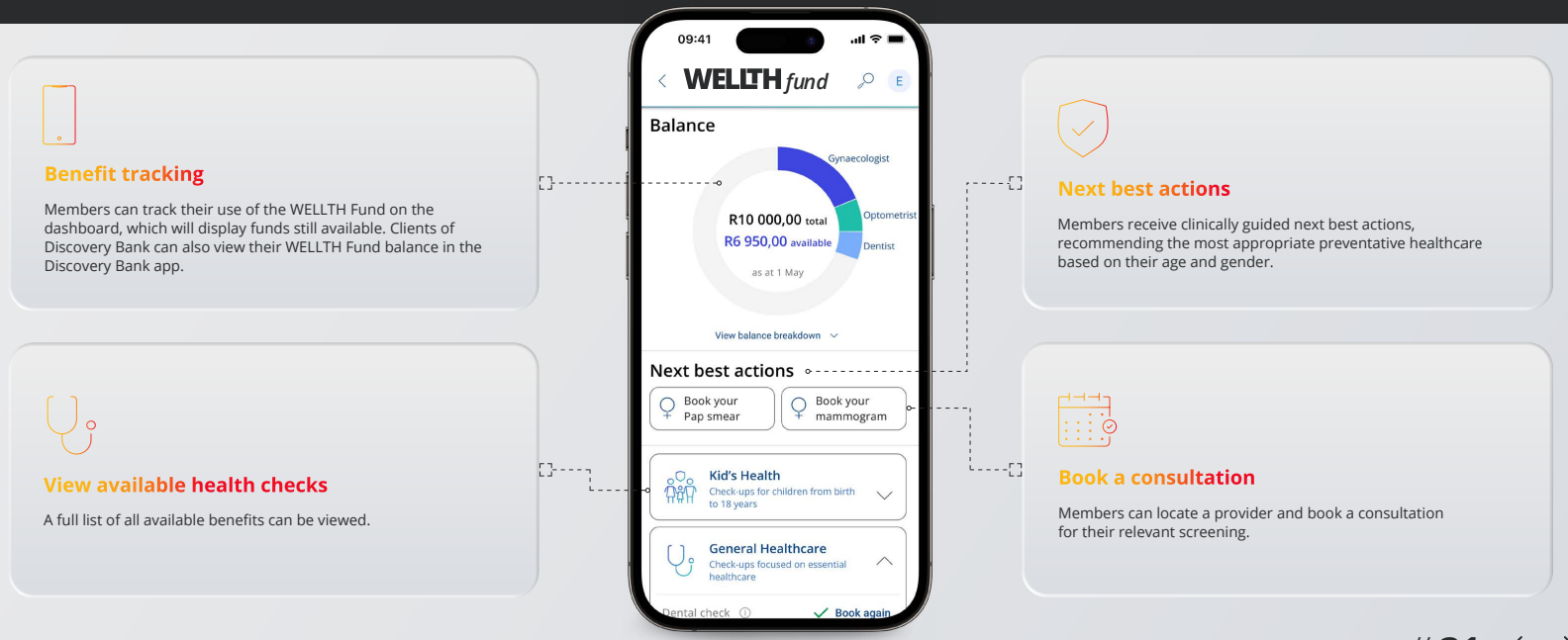

Discovery’s additional benefit the WELLTH fund came into effect on 01 January 2023. This benefit is a once-off benefit to all medical aid members in which it provides up to R10,000 in additional cover for a family’s healthcare needs.  Fund Allocation The WELLTH Fund will be activated in 2023, once members completed their health check in 2022 or 2023 This sets the baseline for a member’s Health Status. To activate the WELLTH Fund, every person on a membership certificate aged 2+ must first complete their relevant health check at a healthcare provider in Discovery’s Wellness Network. Once the member and all their dependents have completed their Health Checks, they will have access to WELLTH Fund of up to R10,000, below is a chart of how funds are allocated.  Where to use your WELLTH Fund The WELLTH Fund covers over and above the annual Screening and Prevention Benefit.  Discovery App WELLTH fund tracking On your Discovery APP the WELLTH Fund Dashboard (shown below) will allow members to view all available health checks and recommended next best actions, book consultations and keep track of their use of the WELLTH Fund.  How tests are covered

This benefit is available once per beneficiary, per lifetime. Discovery pays the above healthcare services from the WELLTH Fund up to the Scheme Rate and up to your WELLTH Fund limit. Some of these tests and treatments have a rand value limit depending on the number of active dependents you have on your membership. Once you have reached your allocated rand value limit for the tests, Discovery will pay any extra screening and preventive tests and treatments from your available day-to-day benefits, where applicable. The Scheme’s clinical entry criteria, treatment guidelines and protocols apply. The normal claims process applies. Discovery will automatically pay this from your WELLTH Fund. FAQ

Yes, the WELLTH Fund covers the following specific medical devices if they have a registered NAPPI code and are bought from a registered healthcare provider with a valid practice number (such as a pharmacy or doctor):

It depends on which health plan you have. Plan network rules apply for members on Smart and KeyCare plans:

Members on all other plans may use a provider of their choice and do not have to use a network provider to be covered by the WELLTH Fund. 4. The WELLTH Fund tool has recommended a list of check-ups that I should go for, am I only covered for these check-ups? No, the WELLTH Fund Tool is just a guide for which screening check-ups are most suitable for you, based on your age and gender. However, you can go for any of the screening and preventative check-ups covered by the WELLTH Fund - you don't have to go for those recommended by the tool. 5. Can I claim for medication from the WELLTH Fund? No, you cannot claim any medication from the WELLTH Fund. 6. How can I book an appointment to use my WELLTH Fund?

For more information, please contact our Health department on 011 658 1333 or email us on service@daberistic.com Source: Discovery

1 Comment

Spring season is finally here and that means the year is coming to an end. We can see a trend that more and more countries are opening up for tourists. In the time of such a pandemic it also reminds us how important it is to have medical cover abroad.

Most medical schemes include international travel medical benefits, but each company's benefits are different. With some medical schemes you need to ensure that you need to activate your International Travel Benefit before you travel. With Discovery Health you do not need are to phone ahead to “activate” this benefit, all you need is your departure and re-entry stamps in your passport as proof! Depending on your chosen medical aid option, your cover limit will either be R5 Million or $1 Million and that will alleviate the burden off your shoulders knowing that you will be able to receive the best medical attention whilst on your travel adventures. Should you wish to find out more about International Travel Benefit topics such as:

If you will be travelling and may require a vaccine certificate, you may contact EVDS on 0800 029 999 to request a vaccine certificate for travel. This is a special request that they do and they will provide the member with an email address to send their information. They will need the below information:

If you have any other queries, please contact Namhla, Tammy or Jo in our Health department, email service@daberistic.com, Tel 011-6581333, Option 2 for Medical Aid.  The last two weeks have brought immense loss and turmoil in the country. With the unexpected unrest in the country a lot of business owners are reassessing their insurance cover.

SASRIA is the only insurer in South Africa that provides cover for loss or damage to insured property as a direct result, of civil commotion, public disorder, strikes, riots and terrorism. SASRIA does not do direct business with the public but is included in most commercial and domestic insurance policies. SASRIA will be for the following coverages:

On the SASRIA website https://www.sasria.co.za/, they note the following: “SASRIA cover excludes theft. Looting is not a stand-alone SASRIA peril and will only be considered as a valid claim in terms of SASRIA if it occurs during an active SASRIA peril for which SASRIA accepts liability.” The above statement speaks of looting, and it is important to understand what it means, SASRIA defines Looting as the following: “To steal goods, typically during a riot, strike, or civil commotion. Looting must take place during an event that SASRIA covers. SASRIA does not cover theft.” There may also be instances where a fire may occur and that may fall under SASRIA. The insurance company will always look at the cause of the accident. If the fire is caused by a gasoline bomb thrown through a window into the building during a riot, SASRIA will be responsible for the compensation of the claim. Currently insurance companies have paused activating any new business during this time of unrest especially on clients with no current insurance in place. It is therefore important to highlight that insurance cover should be taken before the risk is eminent. If you would like a quote for yourself or your business, please contact Marizka or Ed in our Short-term department service@daberistic.com tel:(011) 658-1333  In this month’s article, we focus on a question which our client often asks us: why is my claim taking so long? We will provide insights into the claims process and some of the key factors that affect the its duration.

With “Nowism” being an integral part of our lives - where people want things now more than ever - many clients often get frustrated with the claims process which can be a lengthy one, due to the multiple stakeholders and steps involved. Although its intention is to ensure that the claim is settled in the most fair and reasonable manner for both clients and insurers alike, the clients are often not aware of the continuous effort happening in the background while the clock ticks away. To explain why the claims process takes long, let’s use motor repair claim as an example. Firstly, it is important to acknowledge that there are many stakeholders involved in a motor claim, namely client, broker, third party, police, claims handler, assessor, repairer, parts supplier, and quality assurer. At times, an investigator may also be involved if the insurer wants additional verification to be done. Due to this, a few days here, a few days there, the claims process becomes an inherently long process. Secondly, there are various due diligence in place. For example, a damage assessment is done by an independent assessor to check for all damages on the vehicle, after which an assessment report is sent to an insurer in three to five days. The insurer would then proceed to authorise the claim after they are satisfied with all the information at hand from various parties, including the clients themselves. If needed, the insurer may request the assessor to review certain aspects to ensure that all damages and repair values are accurate. Once authorisation is granted, the repairer would then proceed to order parts and start the repair process. The repairer strips the car and conducts a more thorough review, and more often than not, the repairer would find other damages which mean they need further authorisation from the insurer before any additional repair can be conducted. Thirdly, the duration of the repair depends on parts availability as well. For more popular brands such as Toyota and Volkswagen, parts are more readily available, but for other cars or models that require imported parts, it may take up to three weeks just to get the parts. The repair usually takes about one to two weeks for minor repairs, and two to eight weeks for major repairs. This process is technical in nature and involves various steps and divisions, such as panel beating, fitment, spray painting and quality assurance – all of which are done to ensure that the car is restored to its previous glory. In this regard, the insurer carefully screens and selects their approved repairers to provide peace of mind to the client. In certain cases, the insurers also send their own quality assurers to ensure that the repairs are indeed done to the approved specifications. The above outlines the reason behind a lengthy motor repair process. For a write-off and other losses, the process and stakeholders are very different, but the underlying principle remains the same. Although many people believe that insurers use different tactics to delay a claim, insurers actually want to settle claims as quickly as possible, because there are additional costs involved (many of them are outside of the insurers’ control) when claims take longer than expected. Hence we always advise our clients to include 60-day car hire as part of their cover, so that they are in no way inconvenienced by the claims process. We at Daberistic believe that by providing the right advice and solution to clients, we can create win-win relationships which will ultimately benefit everyone. If you are looking for advice on your short-term insurance needs, you can contact us on the following channels: -WeChat: daberistic -Email: ShortTerm@Daberistic.com -Phone: 011 658 1333  By Edmond Lee, Insurance Advisor

In South Africa, having a car is a necessity which at the same time brings the risk of a motor accident. And let’s face it – motor accident is the last thing on our mind, hence when we encounter it, we often do not know what to do. The purpose of this article is to share some info on the topic, so that you are better prepared in the event of a motor accident. First and foremost, it is imperative that you remain calm and put safety first. Many people often get out of the car immediately in order to check for damages (or in some cases, argue with the other party), without first checking surroundings. This is very dangerous, particularly on a highway or major roads, hence this must be remembered. If you feel unwell after the incident, limit your movement and wait for paramedics to arrive on the scene. Secondly, you should not admit any liability. This is an accident which no one wanted to happen, so leave the liability matter to the insurer who will represent you in the case. Furthermore, record as much evidence as possible. Fortunately, these days we all have a cell phone, so you can take pictures and record key information such as: - Date, time and location of the incident - Accident scene - Damages to cars and properties - Police name and case number - Other parties’ driver license, license disc and contact details - Name and contact details of witnesses, towing trucks and other relevant parties So when should you call the police? If there are no injuries or major blockage of the road, then you don’t have to call the police – you can register the case at the nearest police station within 24 hours. If there are injuries, then the cars can only be moved after police arrives on the scene and takes proper record. In terms of towing, if the car remains derivable, then no towing service is needed. However, if you are worried that driving it may cause further damage (or the car is not derivable at all), then we suggest that you contact your insurer to arrange towing and storage by their appointed service provider to avoid any potential issues. If needed, the police has the right to tow the car for further investigation. Last but not least, remember to inform your insurance advisor after the incident and provide true and accurate information, so that the claim can be processed without delay. If you have any short-term insurance needs, you can contact us on the following channels: - WeChat: daberistic - Email: ShortTerm@Daberistic.com - Phone: Working hours 011 658 1333. After hours 076 200 5488  When times are tough, we understand that people try to save money wherever they can. But never compromise on quality insurance of your most prized possessions. At Santam, we feel there are always ways to structure your policy to suit your pocket so you’re properly covered and we can pay your claim. Let’s look at ways to do this.

How to afford quality insurance First of all, do a quick run-through of your lifestyle, profile and assets. These are the factors that determine how much you are charged every month. Things change all the time – for example, you may have installed extra security measures around your home and not told us, or you’ve changed jobs and your car is now parked in an underground garage instead of outdoors. Perhaps your student daughter now has a job and no longer lives in a high-risk city area. Just by updating your profile, you may find that your premium decreases or that you risk profile has changed. Saving on car insurance premiums Consider Third Party Only car insurance: This is the minimum amount of cover you can give your vehicle, making it the cheapest there is. Raise your excess payment: The greater your excess is, the lower your premium. During the quotation process, you will be asked to select the amount of voluntary excess you will be prepared to pay in the event of a claim. Although there is a compulsory excess amount, you can always choose to increase this. This would mean paying more out of your pocket, so make sure you can afford the higher excess amount. Pay for smaller damages yourself: If you are able to keep a rainy-day fund for smaller nicks and dents, you will manage to stay claim-free for longer and get a big reduction on your premium. Make sure the correct person is noted as the regular driver: Your risk factor is determined by the person who most often drives the car, so be sure to keep this information updated. Install additional security features: Although we know this means spending more money, drivers who install tracking systems in their vehicles could benefit from a lower premium. Vehicle tracking technology could also impact your risk profile, as it will be easier to recover your car in case of a theft or hijacking. How to reduce home insurance payments Increase your excess payment: The greater your excess is, the lower your premium. During the quotation process, you will be asked to select the excess you will be prepared to pay in the event of a claim. Although there is a compulsory excess amount, you can always choose to increase this. This would mean paying more out of your pocket, so make sure you can afford the higher excess amount. Pay for smaller damages yourself: If you are able to keep a rainy-day fund for smaller repairs, you will manage to stay claim-free for longer and reduce your premium. Upgrade security features: Installing a home security system or upgrading your existing security measures can decrease insurance premiums – plus ensure that you are safer. Also join a neighbourhood or block watch, as some insurers will offer reduced rates to homeowners who belong to these types of organisations. Tip: Combine your car, home and building insurance to reduce your insurance premium. To get a quote and cover that will be sufficient for you please contact Sandy in our Short – Term Department, email shortterm@daberistic.com , tel (011)658-1333 Source: Santam  We take out insurance on our car with the expectation that we will be covered (depending on our specific plan) in the event of an accident. However, there are certain cases where insurance companies refuse to provide cover, due to a number of reasons which will be discussed in this article. Make sure that you don’t fit into any of the cases below, if you want to avoid being in a tricky situation where you don’t get the cover which you agreed to.

Be truthful about previous convictions: It is important to be truthful about previous convictions. If you, as the policy holder, withhold vital information in the hopes of receiving a lower premium, the insurance company will not cover you in the event of an accident if they learn that you have not been truthful. Don’t be misleading about who the main driver of the car is: Often, people try to cut their premium payments by being dishonest about the main driver of the car. This usually happens when an inexperienced or young person is the main driver of the car. Make sure that you are honest about this as it can cause your insurance company to not cover you if you are found out. Inform your insurer about all previous claims: It is important to inform your insurer about all issues regarding previous claims, as by not doing this, you are violating the insurance principal of utmost good faith. This includes the following: any modifications that have been made to the car, which could affect its safety or value; a change in your car’s usage; and providing a false address as to where your car is kept. Report a claim immediately after an accident has happened: If you do not report a claim immediately after your accident has happened, the insurer may rule your claim out and refuse to offer compensation. Therefore, be sure not to wait too long to report an accident and file a claim. In summary, it is important to be honest with your car insurance company, in order to avoid tricky situations where you find yourself being refused cover when you need it most. Follow these basic tips and there will be no need to worry! Source: Carinsuresa |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|