Several South African insurance companies are excluding damages related to the possible failure of Eskom’s national grid, which could result in a catastrophic event.

“This decision has arisen as reinsurers have indicated they would not provide coverage in event of a total grid failure. This effectively leaves insurance companies with no option but to consider grid failure as an uninsurable risk,” says Guy Jameson, Sales Operation Consultant at GIB. Sasria has also stated that it would not be liable for any pay-outs in the event of a total grid failure, because loadshedding is not an insurable risk. Although the country has not suffered a total grid failure, insurers are seeing increasing claims following loadshedding to clients’ equipment. Loadshedding is different from a grid failure, so some insurers have not excluded claims following a power surge, even though loadshedding is not an insured peril. Companies need to start thinking about disaster management plans in the event of total grid collapse. There are warnings of possible looting and civil unrest, with the consequences of severe damage to infrastructure across the country and where Eskom would likely face difficulties in getting the grid operational due to its extensive national footprint. Although the likelihood of a total blackout is low, the consequences of such an incident could be devastating, making it worth preparing for. Although a total blackout presents several dangers, the primary threat is the time it takes to bring a system back up from that total collapse with estimates stretching into weeks rather than days. Major considerations for organisations developing blackout plans are the eventual failure of South Africa’s telecommunications networks and financial systems together with water and fuel shortages. “This scenario could see current logistics and supply chains becoming unstable, increasing the potential for fuel shortages. Generators requiring diesel could become less reliable than backup solutions such as solar-powered systems. From an IT perspective, regular data backups are always a must for any business but considering possible eventualities, they are now more important than ever,” adds Jameson. Experts are suggesting that business continuity planning for load-shedding and grid failure are very different. The first can usually be managed within the business premises, with on-site power, water and other backups which will allow the business to continue to operate efficiently for a few hours. However, in the case of a large-scale outage, the same is required but for a greatly extended period and in addition to backups for critical resources that cover tech, telecoms, water supply and logistics. GIB says initial commentary from insurers has been somewhat ambiguous in terms of what is covered and what is not. What seems to be clear is that there is a definite push to avoid any losses associated with grid failure. “This raises questions around consequential loss and whether it can be directly associated with a particular claim. If grid failure results in any other public supply being affected (for example, water), then any consequential loss might also not be covered,” he says. So, what exactly will be covered? “If a defined event takes place at your premises as a direct result of grid failure (fire, stock deterioration that has caused financial loss to the business), there will be no cover. Should this occur, you need to consider the consequences of this with your insurance advisor so that a well-considered and structured response is in place,” says Jameson. Glossary of terms: The different terminology relating to power failures can become quite confusing, so in short: Loadshedding is a controlled interruption of the electricity supply to the public, to prevent damage to the electricity grid. Grid failure occurs when there is more electricity demand on a network than available supply, which loadshedding has helped to avoid for years. When demand exceeds supply, it will cause an imbalance in the system, resulting in the grid operating at a lower frequency than what it is designed for, resulting in a total or partial interruption, interference, suspension, blackout, and/or failure of the electricity grid supply. A power surge is a sudden rapid variation of the voltage magnitude / electrical transient voltage or a power spike in any electrical system. Due to its sudden unforeseen nature, insurers invariably cover losses due to these occurrences if so, stated in their insurance schedule and mainly relating to mainly domestic, but have capped their exposures to certain limit. Source: FA News Written by: Guy Jameson, Sales Operation Consultant at GIB

0 Comments

In our previous living annuity article, we discussed the impact of drawdowns and volatility in a living annuity portfolio, and how to choose an acceptable drawdown rate. This was done to provide context about choosing the right drawdown, so you do not run out of funds. It’s every retiree’s goal to not run out of money in retirement. Without the comfort of a defined-benefit plan that pays out guaranteed income, many retirees are left to generate cash flows from their investments exposed to the market. It is therefore important to have a portfolio that is geared towards generating healthy growth and returns, offers protection and is cost-effective, to ensure a long-term capital pool to draw an income from. As with the very best sporting teams, every asset in a portfolio plays a role—some assets are more proficient at defence and others press forward to attack—but they need to work together. It is also this cohesion that makes great portfolios. For our investors investing in Morningstar Managed Portfolios, click below to access the latest performance snapshot, market commentary and market performance summary:

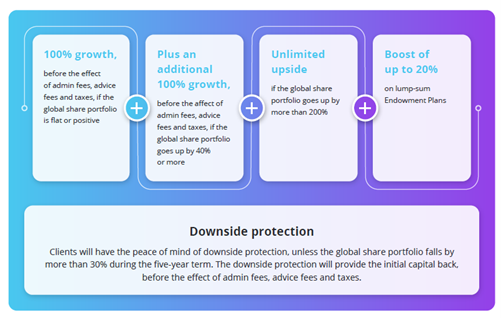

Morningstar SA Managed Portfolios Morningstar Global Managed Portfolios (USD) Market Commentary - SA and Global Market Performance Summary - SA and Global  The first tranche of the Discovery Capital 200|300+ had an overwhelming response. Due to demand from the market, Discovery will make another tranche available from 15 May 2023 to 19 June 2023 on the Discovery local Endowment. The Discovery Capital 200|300+ July 2023 tranche, similar to its predecessor, will give clients the possibility of 100% growth if the global share basket is flat or positive. It will also offer an additional 100% growth if the global share basket is up by more than 40% over the five years. Growth is before the effect of fees and taxes. With a global portfolio linked to 20 companies in Europe and the United States of America, clients can also get enhanced upside returns with downside protection, hedged against currency movements. In addition, they'll have access to a boost of up to 20% on new lump sum Endowment Plans. How it works  The growth clients can get

Clients will get 100% growth if the underlying global share portfolio return is flat or goes up by as little as 1% over a five-year period. If the global share portfolio grows by 40% or more, over the same period, they will get an extra 100% growth. If the global share portfolio goes up by more than 200% over five years, clients will also receive any additional growth above that level. Clients will also receive downside protection Should the portfolio fall by up to 30% during the five-year term, downside protection will kick in. Should the global share portfolio fall by more than 30% from its initial level at any point during the five-year investment period, the downside protection will fall away. The downside protection will provide clients' initial capital back, before the effect of admin fees, advice fees and taxes. The growth, conditional downside protection or any other resulting return is before the effect of advice fees, Discovery admin fees and taxes where applicable. These fees and taxes will affect the final return. Clients can enjoy a boost of up to 20% on client investment In addition to the return of the Discovery Capital 200|300+ Fund, clients can get a boost of up to 20% on their investment if they take out a new Endowment Plan. Clients will receive a portion of the boost after five years, and the rest of the boost after 10 years. For clients with an existing Endowment Plan, the boost will not apply to transfers into the Discovery Capital 200|300+ Fund from non-qualifying funds. This offer is available on our lump sum Endowment Plans from 15 May 2023 to 19 June 2023. To apply for the Discovery Capital 200|300+ (July 2023 tranche), contact Kevin or Sandra in our Investment department, email service@daberistic.com, tel (011)658-1333 Source: Discovery  Are you recently diagnosed with High Blood Pressure? Or Diabetes? Did you know that your Medical aid actually covers your monthly medication?

Different medical aid schemes may cover different chronic conditions, but the general 27 conditions are covered by most of the medical aid across all plans. Below we list them:

How to apply for Chronic illness benefit? Discovery:

Once the form has been received and reviewed you will get a confirmation via email whether or not the request has been approved, and/or what medications are approved/declined. The letter of benefit will have details on how you will be covered under the condition. If your script has an end date (such as 3 months or 6 months), to continue with treatment, you must visit the doctor again to get the new script, and send it to Discovery to assess and update the approved medication. If you have any updated new prescription (medication or dosage), you must email the new prescription to Discovery as well so they can update it on their system. Medications that are covered Discovery has its medication formulary. If you are on the Essential Smart plan or Keycare plan, then your medication MUST be from the formulary; if you are on other plans, then medications from the formulary will be paid fully, and medications outside of the formulary will be paid partially. Approved medicine on the Chronic Illness Benefit medicine list (formulary) Bonitas: There are two ways to activate your Chronic Illness Benefits with Bonitas

Follow-up consultation and nominated doctor online Doctors normally advise you to follow up online to save time, normally this is perfect for members who need blood test review. They would send you to the nearest pathology for a blood test. Momentum

For further queries regarding your Chronic Illness Benefit contact Namhla in our Health department tel(011)658-1333, email service@daberistic.com A record amount of R1.6 trillion is currently held in South African bank accounts as retail savings deposits. This is a staggering amount of money which is currently conservatively invested. In many ways, this movement of funds reflects the significant uncertainties faced by investors, both in South Africa and globally. Many investors are sitting in cash with the hope that an attractive entry point into markets may be on the horizon. Unfortunately, as history has taught us, trying to time markets can mostly be regarded as a fool’s errand. Investors are often better off being guided by their willingness and ability to take risk when making investment decisions, rather than the current news flow or the latest geopolitical event. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|