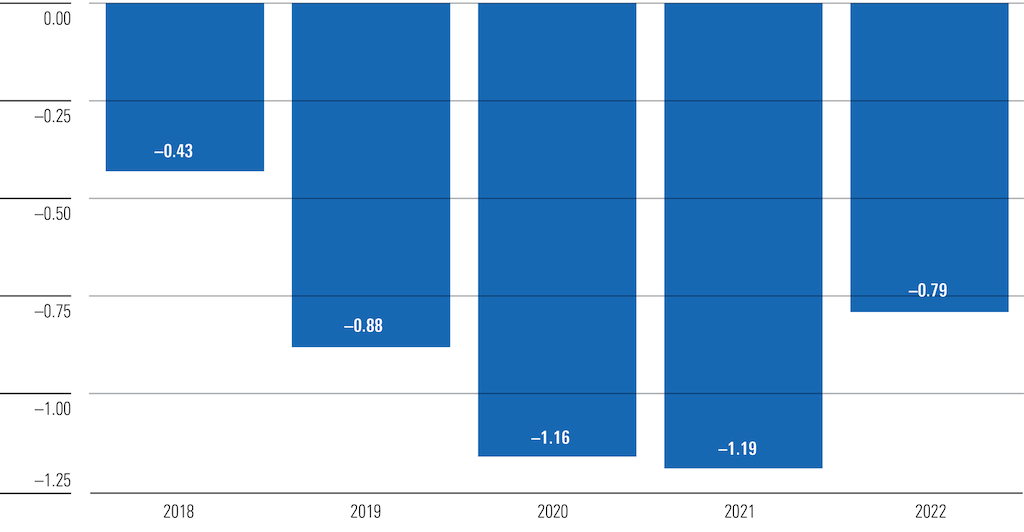

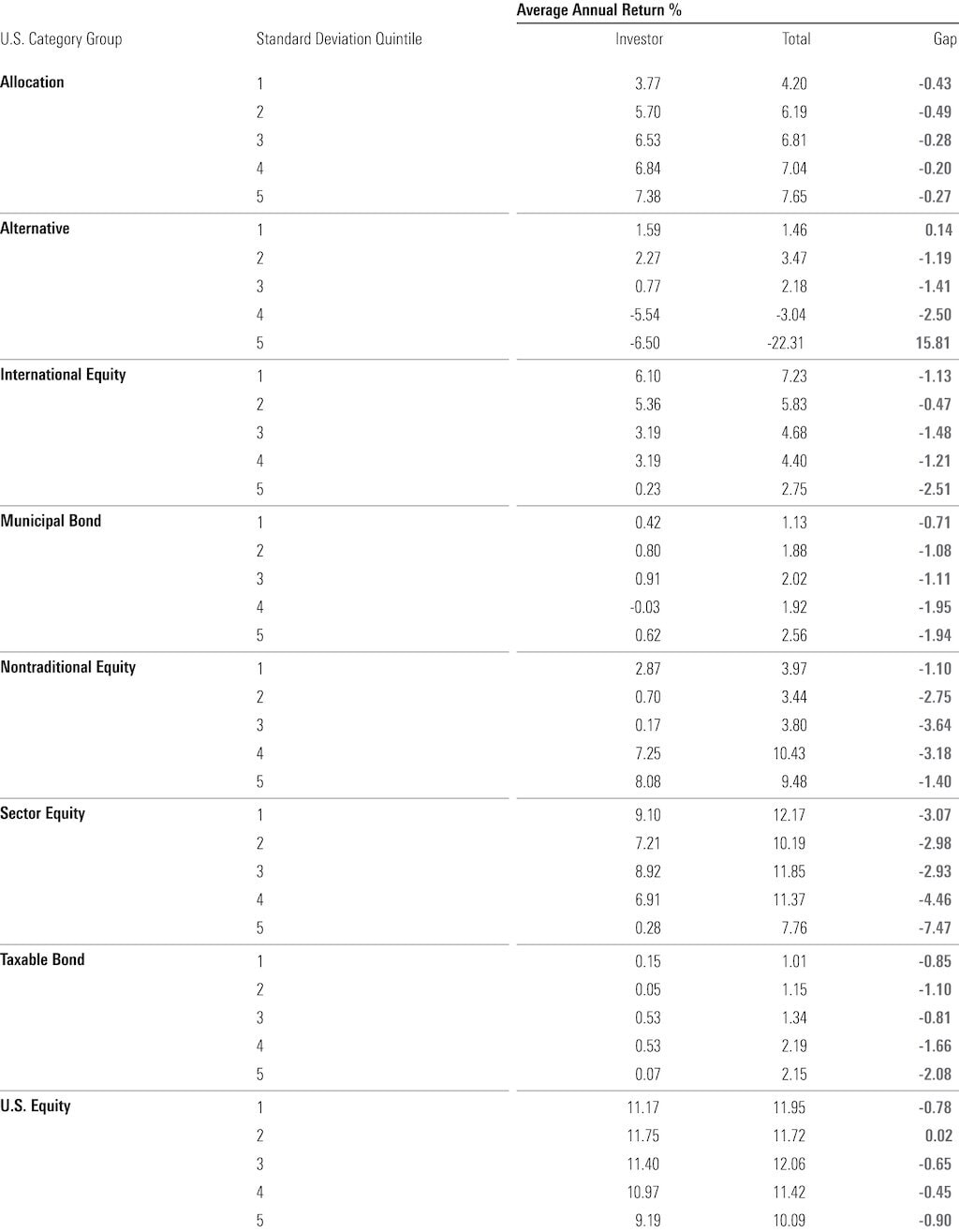

We just published an update of our annual “Mind the Gap” study. The study estimates the return of the average dollar invested in funds and exchange-traded funds (that is, “Investor Return”) and compares it with the average fund’s total return, with any difference attributable to the timing of investors’ purchases and sales. The smaller the gap, the more investors captured their funds’ total returns and vice versa. In this year’s study, we found the average dollar invested in funds earned a 6% annual return over the 10 years ended Dec. 31, 2022, while the average fund gained about 7.7% per year over that same span, for a gap of about 1.7% annually. What this means is that investors missed out on about one fifth of their fund investments’ average net returns, a significant shortfall.  That gap is more or less in line with what we’ve found when estimating the dollar-weighted return gap for the 10-year periods ended December 2021 (-1.7% gap), 2020 (-1.7%), 2019 (-1.5%), and 2018 (-1.6%), suggesting that timing costs are a persistent drag on the returns investors earn. Gaps by Asset Class The gap varied when we grouped funds by certain dimensions like asset class. For example, as shown in the first chart, the average dollar invested in allocation funds gained 6% per year versus a 6.4% return for the average fund, the narrowest gap of any asset class. On the flip side, investors in narrower sector equity funds earned only 6.4% per year on their average dollar, which was 4.4% less per year than the average fund’s return, a large deficit reflecting mistimed flows. Encouragingly, the average dollar invested in U.S. stock funds earned 11% per year over the decade ended December 2022. That was only 0.8% less than the average fund’s return, which was narrower than the gap we estimated over the 10-year periods ended 2019 through 2021, as shown in the chart below. While it would be preferable to see U.S. stock fund investors capture even more of their average fund’s return, it appears that mistimed purchases and sales were less costly as a share of returns than in other asset classes.  That was quite apparent with alternative funds, where the average dollar lost almost 1% per year while the average fund rose about 1% per year. To be sure, the average alternative fund’s return was nothing to write home about, but it is still concerning that investors in these funds ended up frittering away even those modest gains and then some. Gaps by Category We also estimated the dollar-weighted returns of the 10 largest Morningstar Categories by net assets, as shown in the chart below.  The average dollar invested in the most popular U.S. stock categories earned almost as much as the average fund, as evidenced by the relatively small gaps for large-blend, large-growth, and mid-blend. Similarly, the average dollar-weighted return of moderate-allocation funds nearly matched the average fund’s total return. Investors struggled to a greater degree in timing their investments in foreign-stock funds, with larger gaps seen between the dollar-weighted and time-weighted returns of foreign large-blend and diversified emerging-markets funds. Indeed, the average dollar invested in emerging-markets funds earned nothing over the 10 years ended Dec. 31, 2022, a disappointing outcome. Investors also earned meager dollar-weighted returns in bond funds. In fact, the average dollar invested in intermediate core bond funds lost about 0.2% per year over that span. Gaps by Volatility One of the clearer takeaways from our Mind the Gap study is that investors are more likely to mistime their investments in highly volatile funds than they are in less-volatile funds. That relationship held over the 10 years ended Dec. 31, 2022, as shown in the table below, which groups funds by category group and standard-deviation quintile (the first quintile containing the least-volatile funds).  The least-volatile quintile had a smaller gap than the most-volatile quintile in six of the eight category groups. On average, the least volatile funds’ dollar-weighted returns lagged their total returns by around 0.9% per year, which was a full percentage point narrower than the gap for the most-volatile funds.

Takeaways and Lessons While investors have made strides in many ways, our research finds that there’s still room for improvement when it comes to timing their investments. What can investors do to earn more of their fund investments’ total returns? Here are a few lessons to be drawn from our findings: Less Is More Time and again, we have found that investors in allocation funds capture a greater share of the funds’ total returns. Why? They are designed to be all-in-one holdings given they span multiple asset classes and rebalance on a regular basis, sparing investors from having to do much maintenance. Allocation funds also help mitigate the risk of mental-accounting mistakes that investors are prone to, such as buying more of a high-performing stand-alone strategy and selling a lagging one when they should be doing the opposite. Allocation funds combine these separate strategies to form a cohesive whole, and thus the performance divergences that otherwise might push investors’ buttons are largely unseen. More (Focus and Volatility) Is Less Another clear finding from the study is that investors have struggled to successfully use narrowly focused or highly volatile funds. These types of funds—whether they were nontraditional equity offerings or those that were among the most volatile in their category group—saw some of the heftiest return gaps that we measured. Most investors would likely be better off keeping it simple in ways that emphasize wide diversification and low costs, which means steering clear of strategies like these. Good Beats Perfect The evidence suggests investors enjoyed greater success by favoring simpler solutions like allocation funds. Interestingly, we found larger gaps in areas and styles for which there is robust academic support, like tilting to value, smaller-company stocks, or emerging markets, suggesting that the added volatility these strategies entail cost investors any excess return they might have earned and then some. The same held for more-exotic strategies that on paper might push a portfolio closer to the efficient frontier but in real life confound investors into costly mistakes. Source: Morningstar

0 Comments

Forward Estimates

Making accurate forecasts is easy when the trendline has been established. (Making inaccurate forecasts is always easy.) By the mid-90s, it was clear that indexing would boom. And even before I formally bid mutual funds adieu in a 2021 article, exchange-traded funds had already secured their future. ETFs do not yet control more assets than traditional mutual funds—but they certainly will. On other occasions, the task is perilous. Early outlooks for the internet’s prospects consisted, in essence, of monkeys tossing darts. For example, the consensus view entering the new millennium was that the best prospects for recording internet-related profits lay with business-to-business applications. Wrong! Today, four internet-related firms are among the nation’s 10 largest companies: Microsoft, Amazon.com, Alphabet, and Meta Platforms. The first derives half its revenue from businesses, and the latter three hardly any at all. Considering AI Predicting how artificial intelligence will affect the investment industry falls between those two extremes. The internet was so difficult to foresee because it broke radical new ground. Cellphone conversations resembled those from landlines, but the internet experience was unlike anything that came before. Predictions were made from a foundation of sand. In contrast, AI has at least something of a predecessor, with computers. Before AI was developed, microprocessors were the great investment innovation, providing 1) portfolio managers with more information, 2) financial advisors with software, and 3) researchers with improved analytics. The new technology permitted the previously impossible. (For example, Morningstar owes its existence to the availability of personal computers and desktop publishing.) Using the computer revolution as a backdrop, let’s consider how artificial intelligence might affect each of those three investment-industry segments. Portfolio Managers Artificial intelligence is unlikely to change professional money management. Here, the computer analogy fully holds. When super computers arrived in the 1980s, several “quantitative” investment firms boomed. They profited by mining knowledge from huge databases that had not yet been exploited. Their victory was brief. Within a few years, their funds had reverted to the mean. You know why. Any reasonably sized money management business could buy its own computers and investment databases, thereby emulating the quants. And that is exactly what happened. The competitive advantage quickly became mimicking the Joneses. Technologically assisted discoveries no longer mattered because the marketplace had fully incorporated them into equity prices. The same process will occur with artificial intelligence. Any portfolio management boons from employing AI will soon be erased by imitation. The status quo will therefore persist. Most actively managed funds will trail their benchmarks because of their costs, and identifying the happy exceptions will remain a difficult task. Prediction: Given the dominance of indexing, active portfolio managers have little to lose. The good news for them is that artificial intelligence will not hurt them. Unfortunately, neither will it help them. Financial Advisors Here, the computer analogy partially fails. It works in that both computers and artificial intelligence can process data and arrive at conclusions far more rapidly than humans. However, it is incomplete because, unlike AI, computers do solely what they are told. Assigning responsibility for their output is straightforward. A computer is no more to blame for providing flawed advice than is a hammer for striking a nail. The fault lies with those who gave the instructions. One cannot similarly trace artificial intelligence’s steps. That presents a major obstacle when adapting AI for financial advice. On the one hand, AI is well positioned to create customized recommendations, given its flexibility. On the other hand, AI operates outside of human control. Perhaps AI presentations will become so adept at explaining their “reasoning” (to use the term loosely) that customers will grow accustomed to accepting its counsel, without hesitation. Perhaps. However, at least for the foreseeable future, I suspect that AI will supplement current financial-advisory practices rather than supplant them. Conventional software will suffice for most financial-advisory clients. For those with special conditions, AI will serve as a research assistant, offering potential but discretionary suggestions. Prediction: Unlike active portfolio managers, financial advisors were unharmed by the index-fund revolution. Like active portfolio managers, they face little threat from artificial intelligence—and possibly great benefit, if they harness its powers. Investment Researchers The prognosis is most challenging within my own field of investment research. Financial advisors earn their keep from their recommendations. We researchers, on the other hand, are paid to attract attention. That makes artificial intelligence a true rival. Those who care about investing have only so many hours to devote to the subject. They can spend them on work published by either people or AI. My hope, naturally, is that artificial intelligence never becomes sufficiently convincing. It provides valuable basic information and fact-checking, as with Google searches, but its insights are judged to be shallow. The material published by artificial intelligence has already surfaced elsewhere, by an author who truly understands the subject, rather than simulating that knowledge. Whether my hope will be realized remains to be seen. Outdoing computer programs is simple. Even the cleverest programmers struggle to devise output that does not sound witlessly mechanical. Artificial intelligence is quite another matter. AI articles are skillfully written. The content is less sophisticated, but it will surely improve with time. Prediction: There will always be a place for original research, which AI cannot produce. However, most published investment research is not truly new but is instead commentary that popularizes existing ideas. Very soon, such work will face stern competition from artificial intelligence. The views expressed here are the author’s. Source: Morningstar China’s latest economic woes is a stark reminder that investing is complex. Here is a quick update on the main issues dominating media coverage:

Source: Morningstar

Last year was one of those bad outcomes - the stock market experienced its worst ear in a decade-and investors are having a hard time shaking the feeling. The market has rallied nearly 30% since October, which, in theory, means we've entered a new bull market. However, many people simply do not care - last year's scars are still fresh. Taking the pulse of institutional investors, many remain sanguine about the market's prospects. According to the June Marquee QuickPoll, which surveyed nearly 900 institutional investors, only 3% of investors classify themselves as "bullish." Source: Moringstar

Fedgroup, a financial services group based in Sandton, Johannesburg, offers innovative endowment investment products that offer good after-tax returns while doing good for the environment.

Fedgroup's endowment products have the following advantages: - Inflation protection: These portfolios consist of a diverse range of assets that span various geographic and industry parameters and that are unlinked from market sentiment, creating a natural hedge against inflation. - Anti-cyclical: Unlike many traditional asset classes which have performed poorly in recent times, many alternative investments are designed to be less susceptible to volatile markets. - Currency protection: Since most of the produce is sold internationally, the portfolio is shielded from volatility in the rand. - Do good without sacrificing returns: Rather than compromising between doing good and delivering great returns, the assets within these portfolios make a positive impact on people, planet, and profit while generating a market leading return. More information on the investment portfolios: Minimum investment lump-sum: R100,000 Investment term: 5 years Can nominate beneficiaries Impact Portfolio: This invests in green energy, smart agri, property finance and private capital fedgroup_impact_portfolio_f98d085b83.pdf Diversified Alternates Portfolio: This invests in the Fedgroup Participation Bond Fund, green energy, smart agri, property finance and private capital. fedgroup_diversified_alternates_c315d7468a.pdf Fixed Endowment: This invests in selected assets generating a fixed return. It provides an after-tax nett return of about 8% p.a. fedgroup_fixed_endowment_overview.pdf If you are interested in investing in these products or have any questions, please email to service@daberistic.com, a financial advisor will contact you.  The European Golden Visa programs are some of the most popular in the world. And with good reason. A look now at each country one-by-one:

Portugal: From Euro 280,000 - After five years as a Portuguese Golden Visa holder, the investor and their family can apply for permanent residence or citizenship. They are allowed but not required to live in Portugal: as long as they spend at least seven days a year in the country, their residence permit remains valid. Full capital returned in year 5. Spain: From Euro 500,000 - A Spanish Golden Visa holder, the investor and their family do not need to take language and cultural exams to obtain this type of residence permit for 5 years. Also, they are not required to spend time in Spain, and the law allows investment property to be rented out. Malta: From Euro 135,000 - The status under the Malta Permanent Residence Program is granted for life. The investor has to fulfil several investment conditions: buy or rent real estate (for 5 years), pay government fees and make a charitable donation. They must also confirm that they have a capital / net worth of €500,000. A very affordable program. Greece: From Euro 250,000 - The Greece Golden Visa Program requires a minimum of Euro 250k of investment, in some regions, with recent increases to Euro 500k in others. They allow the property to be be rented out. After holding permanent residence for five years, the investor can sell the property and keep the permanent residence permit. Cyprus: From Euro 300,000 Cyprus Golden Visa holders must invest in real estate, residential or commercial. No taxes on global income, and the country has low income and property tax rates. The corporate tax rate is only 12.5%. After 5 years of living on the island in a soft Mediterranean climate next to the sea, a permanent resident can obtain Cyprus citizenship. Italy: From Euro 250,ooo - The Italian residence permit is issued for two years. It can then be extended for three years provided that the investment is maintained. Investors are not required to live in Italy if they do not want to obtain citizenship. Investors get citizenship by naturalisation under general conditions after 10 years of living in the country. Courtesy: Knightsbridge Group. For more information, click here: bit.ly/44mqe3M  A minor can in fact be registered as a taxpayer in South Africa. This is in terms of section 67(1) of the Income Tax Act that "every person who at any time becomes liable for any normal tax or who becomes liable to submit any return contemplated in section 66 must apply to the Commissioner to be registered as a taxpayer in accordance with Chapter 3 of the Tax Administration Act.” If the minor therefore becomes liable to submit a return or becomes liable for any normal tax, the minor must be registered as a taxpayer.

Section 68. Income and capital gain of married persons and minor children.—(1) Any-- (a) income received by or accrued to or in favour of any person married in or out of community of property which in terms of section 7 (2) is deemed to be income received by or accrued to such person’s spouse; or (b) capital gain which is in terms of paragraph 68 of the Eighth Schedule taken into account in the determination of the aggregate capital gain or aggregate capital loss of such person’s spouse, shall be included by such spouse in returns of income required to be rendered by that spouse under this Act. (2) In the event of the death of any person during any year in respect of which such income is chargeable or in which such capital gain is taken into account, the income or capital gain of such person’s spouse for the period elapsing between the date of such death and the last day of the year of assessment shall be returned as the separate income of such spouse. (3) (a) Every parent shall be required to include in his return-- (i) any income received by or accrued to or in favour of any of that parent’s minor children either directly or indirectly from that parent; or (ii) any capital gain or capital loss in respect of any transaction entered into directly or indirectly by that parent, which is taken into account in the determination of the aggregate capital gain or aggregate capital loss of any of that parent’s minor children, together with such particulars as may be required by the Commissioner. (b) Every parent shall be required to include in that parent’s return any income deemed to be that parent’s income in terms of subsection (3) or (4) of section 7 or any capital gain deemed to be that parent’s capital gain in terms of paragraph 69 of the Eighth Schedule. Income of Minor children A taxpayer is liable for the payment of tax on any income which has been received by or accrued to or in favour of any minor children if such income arises from a donation, settlement, or other disposition by – (i) the taxpayer; or (ii) any other person, if the taxpayer made a donation, settlement or gave some consideration directly or indirectly in favour of the other person or his family. A minor child will, however, be liable for tax on income which is received or accrues to him/her independently of him/herself; in his own right, for example, bona fide salary and investment income derived from his/her own funds i.e. from money inherited by him/her or received as a gift from any person other than the person mentioned in (i) and (ii) above or from any other source. Should a minor child’s taxable income be sufficient to render him/her liable for tax, the taxpayer, as the legal guardian, must register him/her for income tax purposes and obtain and submit a return on his/her behalf. All investment income received by or accrued to a taxpayer or his/her minor children must be declared (including investment income which has not been paid but has been utilised, accumulated or re-invested for the taxpayer or his/her minor children’s benefit). Where interest is claimed as a deduction against investment income received, full particulars (i.e. amounts invested/borrowed, interest rates, date of each loan and investment) must retained for a period of five years after submission of the return. Courtesy of: Fedgroup |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|