Winter is around the corner and while it may give rise to cosy nights by the fireplace, it also brings its fair share of pitfalls which, if not adequately managed, can potentially lead to financial loss. Two of the most common threats that insurers highlight over the winter season are inclement weather activity, such as storms and flooding – particularly in the southern parts of the country, as well as electrical fires caused by heaters.

Winter comes with an increased reliance on electric appliances to bring warmth to our homes, this too comes with a certain level of risk of fires. Both of these have the potential to damage assets, such as homes and vehicles, as well as other goods. Marius Kemp Head: Personal Underwriting at Santam says that prioritising the protection of your home and valuables against winter-related risks is essential. “Now is the time to assess your property's vulnerability and take steps to minimise the impact of seasonal changes. Making these updates and adjustments now can help prevent serious damage in the long run, which may set you back financially.” Kemp shares a comprehensive guide below offering proactive measures to safeguard homes and possessions against potential damage. To mitigate the risk of weather-related damage, Marius Kemp shares the below tips:

As we rely more on electric appliances during the winter months, the risk of residential fires increases. Kemp advises:

For all queries on your Shortterm policy contact Ruva: email service@daberistic.com, tel: (011)658-1333

0 Comments

“Even in this tough economic climate, brokers cannot focus on price alone and must add value to clients through strong risk management capabilities.”

This is one of the key findings of Santam’s 2023 Insurance Barometer released yesterday. The third edition of the biennial report offers deep insights into the evolving risk trends impacting South Africa. It surveyed more than 900 consumers, businesses, and brokers from across the country. The findings were combined with Santam’s own claims data. Focusing on the changing role of the broker, the study said the competition between direct channels and brokers will continue. “Brokers add significant value in both the commercial and personal lines insurance space, but they cannot lose sight of why clients choose to transact through a broker, and how they deliver against those reasons,” the study read. The top trends in the changing role of the modern insurance broker include:

Reduced income for brokers The findings of the study show that the challenging economy resulted in reduced income and increased costs for many brokers. Nearly 40% of brokers made changes to the insurers they recommend based on premium increases, while two-thirds of broker respondents reported an increase in volume and value of claims in the past year. Brokers also noted a change in client behaviour because of the increased cost of living:

Momentous shift The study tracks emerging risk trends in the country. According to Andrew Coutts, the chief executive of Santam Broker Solutions, the South African short-term insurance industry is facing a momentous shift in the risk landscape. “Climate change, infrastructure concerns and socio-economic challenges have created a tough environment for local insurers who bear the responsibility of ensuring their balance sheets can sustainably withstand the cost of the risks dominating the environment they operate in; while also protecting the financial well-being of clients, and the safety of communities,” he said. The survey found that 80% of corporate and commercial entities have been negatively impacted by emerging risks in the past three years. The challenging economy (66%, up from 62% in 2021) remains the key concern for business respondents, but other emerging risks are becoming more of a concern. Political unrest (59%, up from 48% in 2021), cybercrime (48%, up from 36%), and climate change (47%, up from 35% in 2021) have become increasing threats over the past two years. The top 10 traditional risks identified by corporate and commercial businesses include:

Power down The impact of South Africa’s deteriorating infrastructure, particularly that of Eskom, and the socio-economic challenges because of the constrained economy and high inflation were visible in Santam’s claims statistics. Economic challenges also manifested in higher volumes of crime-related claims. “Two standout claims trends developed in both the personal and commercial lines categories over the past two years that required corrective actions. The most notable being an exponential escalation of power surge claims related to loadshedding, followed by high-value vehicle hijacking and theft,” Coutts said. He added that Santam has experienced an exponential jump in the volume and value of power surge-related claims across personal and commercial lines of business for two consecutive years, in 2021 and 2022. The combined claims volume was up by 39% in 2022 (37% in 2021) and the value of claims paid across both lines soared to 48% in 2022 (after an astonishing 53% in 2021). On the motor side, high-value-vehicle hijacking, and theft claims increased by 128% year-on-year in 2022, breaking a long-term declining trend. Fortunately, the risk mitigation efforts in the form of tracking devices proved effective and resulted in full-loss incidents declining by 80% in the first half of 2023. “Insurance makes individuals, businesses, and populations more resilient. Insurers that take the lead in democratising insurance – by providing affordable, appropriate solutions to the low- and mid-income markets, the youth, and small and medium-sized enterprises – will help drive financial inclusion through greater insurance uptake, building a resilient, sustainable future for our industry, our communities, and our economy,” Coutts said. Source: Moonstone Information Refinery  Santam has informed us of the latest changes in their policy endorsements regarding Power Surge & Electricity Grid Failure. The last couple of months has been a period of immense challenges for our country. We have seen high levels of load shedding, which impacts our daily lives. The country’s power utility has reassured all of us that it is working hard to protect our electricity grid by balancing supply and demand in a controlled, risk-managed manner. Within this environment, Santam wants to provide you with clarity on your cover, cover changes, and tips on how to reduce your risk. Power Surge cover Load shedding, the temporary switching off of power supply in a scheduled and controlled manner, in itself, is not explicitly covered by insurance policies. However, it does result in the frequent switching on of electricity supply to your premises and, depending on the quality of the network and the components thereof, it could cause power surge that damages your electronic items. Subject to the electricity grid failure or interruption exclusion noted below, Santam continues to provide cover for power surge damage, including after load shedding, if selected on your policy. During the last 12 months, our power surge claims have however increased by around 50%, and more than 200% over the last 3 years. To ensure the sustainability of this power surge cover, with effect from 1 June 2023, the following comes into effect: 1. You will have a compulsory excess amount of minimum 10% of claim , subject to a minimum of R5 000 when claiming for any pow surge damage. This minimum excess amount will also apply to any lightning strike damage under the business all risk, personal all rand electronic equipment sections of cover. 2. The following will be excluded from our power surge cover: - Power surge damage that occurs as a result of switching on electricity, following load shedding in excess of 12 consecutive hours. - Power surge damage that occurs as a result of switching on electricity, following electricity grid failure or interruption. 3. The Accidental Damage section of cover no longer provides cover for damage caused by power surge, as this can be specifically insured under its own specific section of cover. SOME TIPS TO HELP YOU REDUCE OR EVEN ELIMINATE YOUR RISK OF LOSS DUE TO POWER SURGE: It is best to unplug your devices when the power has been switched off. After power has been restored to your premises, it should be safe to plug them back in again. In an electricity grid failure or interruption scenario, this is especially important. Surge arrestors or surge protection devices may provide protection, depending on the type of surge experienced. The following should be considered: - Any device should come with a warranty of at least 5 years, for which you should receive an installation certificate. - Any device should protect against over voltage, under voltage, multiple strikes and lightning surge. Remember to check your policy to confirm your power supply covers, including their insured amounts. You can select, reduce or increase your power surge cover options at any time, with the resultant impact on your premium. Electricity grid failure or interruption Electricity grid failure or interruption means a total or partial interruption; interference; suspension; blackout; failure; of electricity supply in connection with any national; regional; municipal; local; private; grid, in connection with any premises or business of the Insured. With effect from 1 June 2023, Santam’s electricity grid failure or interruption exclusion applies and where already enforced, is extended to incorporate the following: 1. Any damage caused directly or indirectly by electricity grid failure or interruption, except as specifically provided for under the Business Interruption section in respect of elective extensions to other premises, namely: – Public telecommunications – insured perils – Public utilities – insured perils and then further subject to the Electricity grid failure or interruption being to an area not greater than any one single municipal area. Power surge damage as noted by point 2 under Power Surge cover above2. Click here for link on FAQ on these changes Should you have any questions regarding your policy please contact Koketso email:service@daberistic.com tel:(011)658-1333  Santam has brought to our attention that fake information about Santam’s insurance cover for blackouts is circulating on social media.

As you are aware blackouts are not an insurable risk under an insurance contract. However, Santam does offer cover for damage to sensitive electronic items that are caused by power surges in accordance with the terms and conditions stated in each client’s contract, provided the client opted for this cover. Below is communication clarifying Santam’s cover regarding the exclusion of a general Electricity Grid Failure on all policies and introducing new commercial cover limits for Business Interruption Public Telecommunications and Public Utilities. 2022 had seen unprecedented levels of blackouts due to unexpected breakdowns and planned maintenance to prevent the failure of the larger electricity grid. This has led to pressure from the reinsurance market to limit our exposure to business interruption claims arising from failure of Public Utilities and Public Telecommunications resulting from any cause. In the light of this, Santam is clarifying their cover regarding the explicit exclusion of a general Electricity Grid Failure on all our policies and introducing new commercial cover limits for Business Interruption Public Telecommunications and Public Utilities. Grid Failure Exclusion The grid failure exclusion will be implemented for all Personal Lines and Commercial Lines policies in South Africa and Namibia as follows:

Alignment with implementation dates for business on external systems will be contracted individually. The grid failure exclusion will be added to the General Section. For Personal Lines, the exclusion will also be added to the Contents Section: Contents of refrigerators and freezers coverage. New Commercial cover limits Cover limits for Business Interruption Public Telecommunications – insured perils, and Public Utilities – insured perils, will be limited to the lower of 50% of the Business interruption cover limit and R25 million, VAT inclusive, with a 3-month indemnity period limit. These new limits will apply as follows:

Wording exclusion details Please click here to view the wording changes. Santam acknowledge that the process of recent excess changes, renewal increases, and wording limitations has been extensive. These changes reflect the unprecedented nature of the shifts in our risk environment. While they wish the extent of their actions wasn’t necessary, the complexity of risk increasingly showcases the value of the intermediary and the benefit that can be gained from helping clients to structure the most effective risk management solutions. Should you have any questions, please contact William or Edmond in our Short-term department, email: service@daberistic.com Source: Santam  In an ever-evolving market that’s recently been facing tremendous challenges, Discovery Insure believe that there is an opportunity to be innovative and agile in making sure your clients’ cover remains relevant. Of course, while enabling them to enjoy even more rewards.

We share with you a host of new and unique features, benefits, and product enhancements across personal and commercial lines. Here is a summary of what you can expect from Discovery Insure in the next year. Personal lines Below are some of the innovation’s you can look forward to:

Business insurance Below are some of the innovation’s you can look forward to:

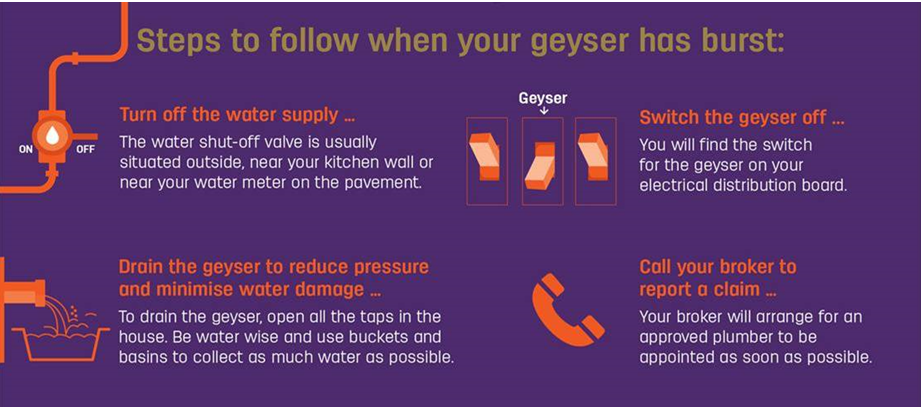

If you would like us to review your Personal or Business Insurance contact William or Edmond in our Short-Term department email: service@daberistic.com Source: Discovery Insure  We continue to share a 5-part series on Home Insurance Tips. In this article we share on Solving your geyser problems. We usually don’t dwell on things that can go wrong with the geyser, the reality is that something will, at some point. Most electrical geyser manufacturers supply a warranty for the actual geyser for between five and ten years, but its individual components only carry a warranty of one to two years. What are geyser components? These are items that generally wear, such as thermostats, elements, pressure control valves, vacuum breakers, seals and gaskets. When a geyser component fails, it doesn’t necessarily mean the geyser needs to be replaced. If something goes wrong with one of these components, check with your broker if your insurance policy covers it. Most importantly, if you suspect that your geyser is leaking or has burst, report your claim to your broker so that they can appoint a qualified plumber to see to the problem. If you don’t, you may find yourself out of pocket due to limits on your policy when not using an approved plumber. Did you know?

What to look out for

If you like us to review your Home cover contact William our Short-term department email service@daberistic.com tel (011)658-1333

Source: Hollard  People sometimes have the perception that insurance claims are declined for ‘no reason’. However, an insurance policy is a contract. The insurer agrees to cover you according to how much risk they think they take on in doing so and set your premium accordingly. When the provisions aren’t met, the contract has effectively been broken and the insurer is exposed to more risk than ‘what your premium covers’ and ‘what was agreed to’.

Beware: In the fine print there might be conditions that could disqualify your claim if not met. The insurance companies are completely within their rights not to cover you – because the contract is not valid anymore. The best course of action is to take care to understand the wording of your policy and to take the stipulations seriously. Story based on actual events, names have been changed to protect identity Rob had his car stolen at a shopping centre. He then contacted us and we registered the claim. The Insurance provider came back and requested the Car tracker logbook. Rob then informed us that his car tracker was cancelled as his policy lapsed due to non-payment. The insurance Company then requested details regarding the cancellation dates, proof of cancellation from tracking company, statements showing non-payment. Ultimately Rob could not provide any of these and later it was found that the tracker policy was under his brother’s name, this then caused the assessor to question “insurable interest” regarding the car. Upon further investigation there were other discrepancies found in the statement and the CCTV footage of the centre where the car was parked was requested for viewing. Ultimately the claim was rejected due to Condition of the policy not being met which is “Tracker is required to be active and working in order to have cover.” There are common pitfalls we see time and time again that result in insurance claims being repudiated, or only partially paid out because the ‘contract’ has been broken. Below are five key examples to look out for: 1.The regular driver and owner of a vehicle differ on a policy An example of where this happens, is if a parent is the policyholder of a vehicle that was purchased for their student child who is the regular driver. The parents have an insurable interest in the vehicle as there is a potential for financial loss if anything happens to it. In addition, if the child is not listed as the regular driver, the claim will likely be rejected and it may have an impact on the parents’ insurance risk profile. What can clients do to avoid this? Update your adviser on the full details of any new vehicle added to a policy, so that appropriate cover can be put in place. Do not assume that simply adding a vehicle to a policy will mean that it is covered. 2. Vehicle extras weren’t specified A case in point was when a client put in a claim for a bulbar that was stolen from his bakkie. No extras were noted in his policy and the sum insured was only sufficient to cover the bakkie itself. The claim was therefore rejected. What can clients do to avoid this? Ensure that all non-factory fitted accessories such as bull bars, sound systems and canopies are specified as additional extras, in addition to the sum insured value of your vehicle. Also keep in mind that you might need cover for mag rims on your tyres, so keep their replacement value in mind – anything you have changed or upgraded compared to the standard vehicle must be noted. 3. Security specifications weren’t adhered to All too common, this is an issue when claiming for a burglary/ theft. If your security features weren’t enabled at the time of the burglary, the claim will likely get rejected. If you tell your insurance company / broker that you have a tracker at the time of taking out the insurance policy it is your responsibility as the client to ensure that this tracking devise must have a valid contract and always be in a working order to prevent problems at claims stage, the client is responsible to ensure that the devise is active and working. If the tracker is no longer active the insurance company needs to be notified ASAP. On high value vehicle this may be a requirement in order to retain insurance cover. What can clients do to avoid this? Make sure you ask about any elements of your cover that are your responsibility. If you are covered for having a locked security gate, vehicle tracking devise, an active electric fence or burglar bars on your windows, these features need to be in place and in good working order at all times. This will keep both your property and you safe. 4. You moved but didn’t say anything to your insurer If you move and don’t notify your insurer of your new address, any claims at the new premises will be rejected. This might seem like an obvious change to make to your policy, but we do experience clients forgetting. What can clients do to avoid this? Insurers usually require that you give written notice of your new permanent, physical address before you move. This is because your new address means your risk has changed and your premium may also change. If you would like us to review your current policy contact Edmond in our Short-term department email; service@daberistic.com tel(011)658-1333 ext 105. Source: Apollotechnical.com, Business Report |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|