Buying your first car? You may do a better job by learning from these common mistakes

1. Do your homework and drive that internet search hard Google the name and model of the car, the dealership and check if people have complained about the car or the service from the dealership on Hellopeter. 2. Think about the real reason you want to buy that particular car Assess your budget and consider whether you're living beyond your means and remember, your car insurance premium will increase based on the type of car you purchase. 3. Test drive the car, especially if it's not a brand new car You should test drive all cars, especially second-hand cars on a hill with the air-conditioner on and, over speed bumps to determine if there are problems with the suspension. 4. Blindly trusting the salesman when it comes to used cars Car salesman aren't exactly known for being forth-coming with information about second-hand cars, especially if the car had been in an accident. Get the car tested by a third-party inspection centre and specifically ask them to look for signs of major accident damage and, then request for the key to be sent to the dealership for an a report as well as the service book. 5. Not sourcing your own financing will cost you big time The interest rate will have a major impact on the costs of the car. If you don't shop around for a finance deal with the lowest interest rate, you're likely to end up with a deal that benefits the dealership and not you. Balloon payments? This deal allows you to buy a more expensive car for a lower installment, leaving you with a once-off repayment of an outstanding lump sum. 6. Getting locked in a contract padded with adds-on Keep an eye out for the various add-ons that dealerships tend to add to the contract. The bow that you get on the car, the champagne, flowers and the gift you get when you buy the car – they're all add-ons that you end up paying for. Other add-ons to look out for are, paint protection, extended warranty, sound systems, car alarms and valets. Source: 702/Wendy Knowler; http://www.702.co.za/articles/338794/6-common-mistakes-we-ve-all-made-when-buying-our-first-car

0 Comments

With much expectations, Vitality HealthyDining is finally here!

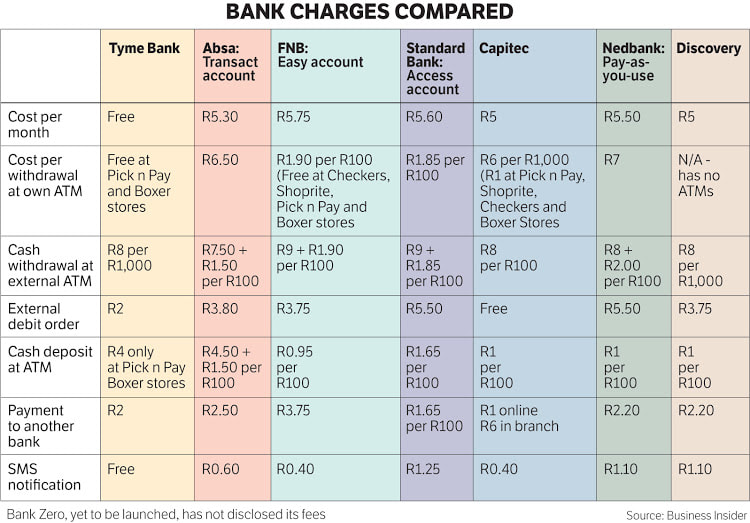

Discovery Vitality members have no more excuses for not eating healthy. With the new HealthyDining benefit, you can get up to 25% cash back on qualifying HealthyMeal choices and 50% cash back on Vitality kids’ healthy meals when ordering through Uber Eats from participating restaurants: Col’Cacchio, Doppio Zero, Nando’s and Ocean Basket. Here’s what you need to do to get up to 25% cash back 1. Activate HealthyDining to earn 10% cash back on Vitality healthy meals. 2. Increase your cash back to 15% by finding out your Vitality Age. 3. Boost your cash back to 25% by completing a Vitality Health Check. If you have children 12 years or younger on your Vitality policy, your will automatically earn 50% on all Vitality kids’ healthy meals. How you can activate HealthyDining: 1. Activate HealthyDining through the Discovery app or website and get a unique code. 2. Link Uber Eats to Discovery Vitality by adding your unique code to your Uber Eats app. 3. Dine in with Uber Eats – order HealthyDining stamped meals from selected partners using the Uber Eats app. Please contact Tammy in our Healthcare team if you have any queries, email health@daberistic.com, tel 011-658-1333. In the past few months, three new banks have launched with a leaner, cheaper business model that will change the face of SA banking — TymeBank, Bank Zero and Discovery Bank. They are here to challenge the Big Four - ABSA, FNB, Nedbank and Standard Bank. The fifth largest bank, Capitec, started in 2001. It now has 11.4 million clients, acquired Mercantile Bank, with over 200,000 new clients opening new bank accounts a month. It also continues to develop its financial technologies. At the same time, Standard Bank the largest bank in South Africa announced it woule be closing 91 branches, affecting 1,200 employees. Many face retrenchments, many will be re-trained to be deployed other departments of the bank. Standard Bank points out that its clients use more of its services online via mobile phones, while having less visits to branches. We witness the waves of technology tsunami hitting the banking industry. The three new banks have very similar focus: digital, with no physical branches. Will they succeed? Will they threaten the Big Four banks? Who are their backers?  TymeBank is controlled by African Rainbow Capital (ARC), an investment company controlled by the eclectic Ubuntu-Botho group headed by Patrice Motsepe. As the Forbes rich list has it, Motsepe is one of the 1,000 wealthiest individuals in the world, with a fortune of $2.4bn. Before it was bought by Motsepe’s company, TymeBank was owned by the Commonwealth Bank of Australia (CBA), one of the world’s top 10 retail banks.  As for Bank Zero, the most entrepreneurially based of the three, it shows how far the Reserve Bank has come that it got the green light. Bank Zero is run by a maverick group of former FNB executives, most of them with strong technology backgrounds, with a few family and friends as shareholders. The chair and figurehead is the former FNB boss Michael Jordaan, based in Stellenbosch. Somewhat ironically, Jordaan is Motsepe’s partner in the data-only telecom network Rain. The Bank Zero CEO, Yatin Narsai (former head of FNB retail), runs the business day-to-day from Bryanston. Discussing the rationale for the bank in an interview with the FM, Narsai says SA ranks among the five countries with the highest bank fees in the world. "This is intolerable in such an unequal society, but then the rest of the bottom five were similarly unequal countries in Latin America," he says. No-one can ignore the competitive threat of cheap banking. Narsai says he personally will save R2,000 a month from his personal and business accounts, when Bank Zero goes live and he can move accounts. "Low fees will become the new normal and I hope that penalty fees will disappear altogether," he says.  Discovery Bank is part of the wider group run by CEO Adrian Gore, which began as a health-care company in 1993. Discovery boasts Remgro associate Rand Merchant Investments (RMI) as its anchor shareholder. Discovery Bank is launching a new business model, based on its Vitality principles. If a client can manage his personal finance and credit well, his money in the account will receive a higher interest rate, while he pays lower interest rate on his home loans. Discovery Bank is hoping to use this business model to incentivise clients to modify and improve their financial habits. The question, however, is what the existing big four banks — FNB, Standard Bank, Absa and Nedbank — will do to counter the threat. "The big banks ignored Capitec in the early 2000s, and lost considerable market share. I am sure they will not make the same mistake again." Below is a comparison of bank charges (Source: Business Insider)  Source: Businesslive

What is Gap Cover?

Gap Cover is the invaluable safety net that covers the shortfall between what medical schemes pay and what specialist doctors charge. Without a gap cover policy, a member would be required to pay this unexpected cost from their own pocket. In addition, a comprehensive gap cover policy also covers co-payments, penalty fees and cancer benefits. At Daberistic, our preferred provider is Sirago. Why Choose Sirago? • Personalised customer service • Gap Cover Solutions • Cover for in and out of hospital • Shortfall cover for day-to-day specialists, GP consultations, dentists and Alternative Therapy • Standard waiting period • Emergency Room Cover for accident, trauma and Illness • No maximum entry age. Benefits do not cease at the age of 65. • Cover for you and your family either on single medical scheme membership or on multiple memberships. • Sirago provides effective turnaround time so as not to compromise policyholders. • A stated benefit is paid straight into the policyholder's bank account or arrangements can be made to settle directly with providers • Claims run weekly • You can claim online, an industry first and for our clients: https://www.daberistic.com/gap-claim-ch.html  Author: Edmond Lee Commercial insurance is a necessity for business owners, but at the same time it is a rather complicated area to understand. We at Daberistic believe in simplifying insurance for our clients, so this article will shed some lights on the basic structure of commercial insurance in South Africa. In the early eighties there were many short-term insurers, flooding a variety of commercial insurance policy wordings onto the market. A sensible comparison of benefit between these policies was virtually impossible, which was to the detriment of the small business insurance consumer. Hence the regulator responded by introducing a standard business policy - known as "Multimark" - in 1987. Over time, Multimark was revised, and today we have the Multimark 3 wording available to us. Even though insurers have since introduced various endorsements to differentiate their products, the basic structure remain largely the same, as the Multimark’s risk-based approach is a solid foundation which ensures that various sections in the policy cover various risks and premium are calculated accordingly. As an example, Fire has a low probability of occurrence but high severity (i.e. all stocks can be affected) if it occurs, as opposed to Theft which has a higher probability but lower severity (because robbers or burglars cannot possible steal all your stock), which explains why covers are broken down into various section. Below is a table summarising the various key sections and their cover areas.  The scope of commercial insurance is broader than the above and continues to evolve as the risk landscape changes, resulting in other covers such as Products liability, Directors’ and Officers’ liability, Cyber crime, Commercial crime, Credit insurance – just to name a few. It is therefore crucial that you make use of an insurance advisor who can advise you on your risks and propose covers that meet your needs.

We at Daberistic believe that by providing the right advice and solution to clients, we can create win-win relationships which will ultimately benefit everyone. If you are looking for advice on your short-term insurance needs, you can contact us on the following channels:

|

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|