|

In partnership with Morningstar: Looking at the year-to-date performance of markets, the ride has been anything but smooth. Inflation, higher interest rates, and the Russian invasion of Ukraine top the current list of investor concerns at the moment.

0 Comments

outh Africa has a relatively small equities market with a handful of dominant shares, spread across a few sectors, which are available to invest in. This presents a significant risk for investors: a highly concentrated portfolio.

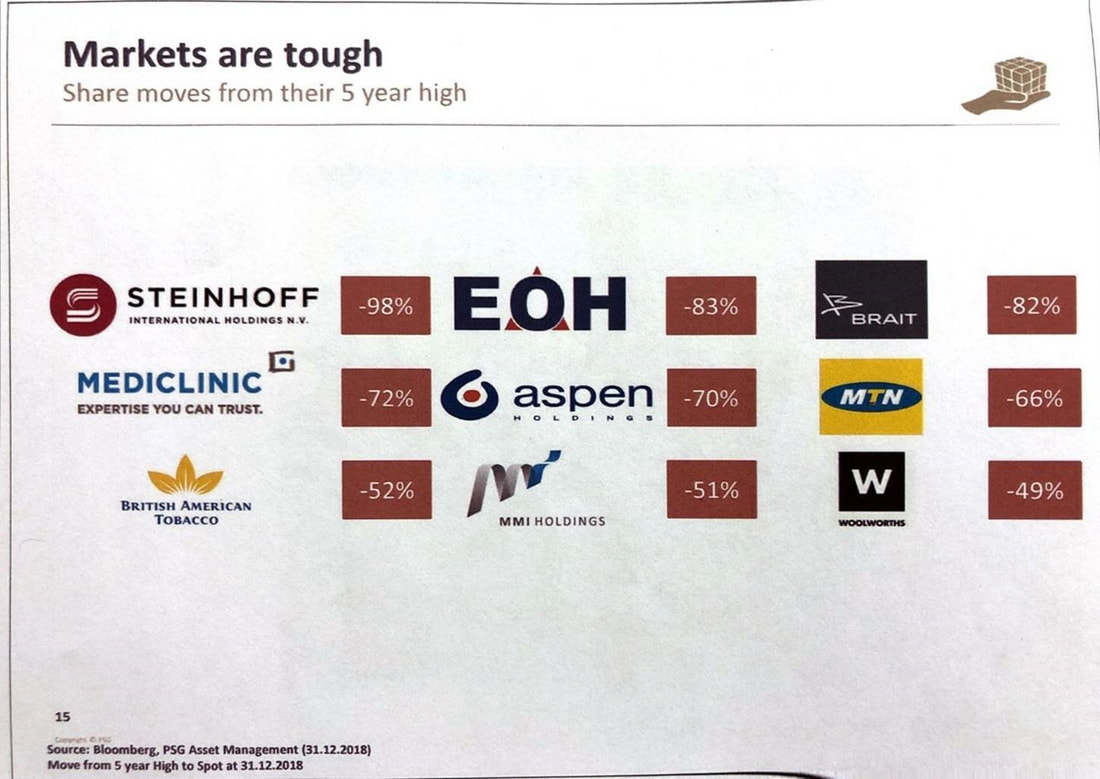

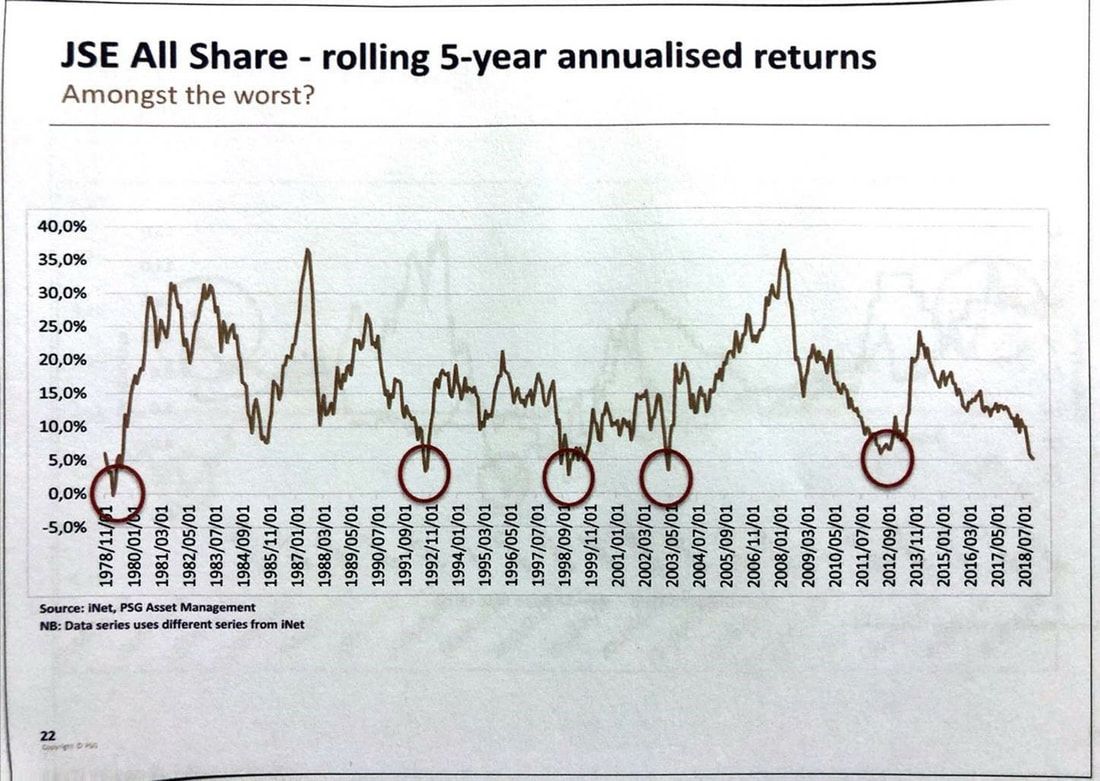

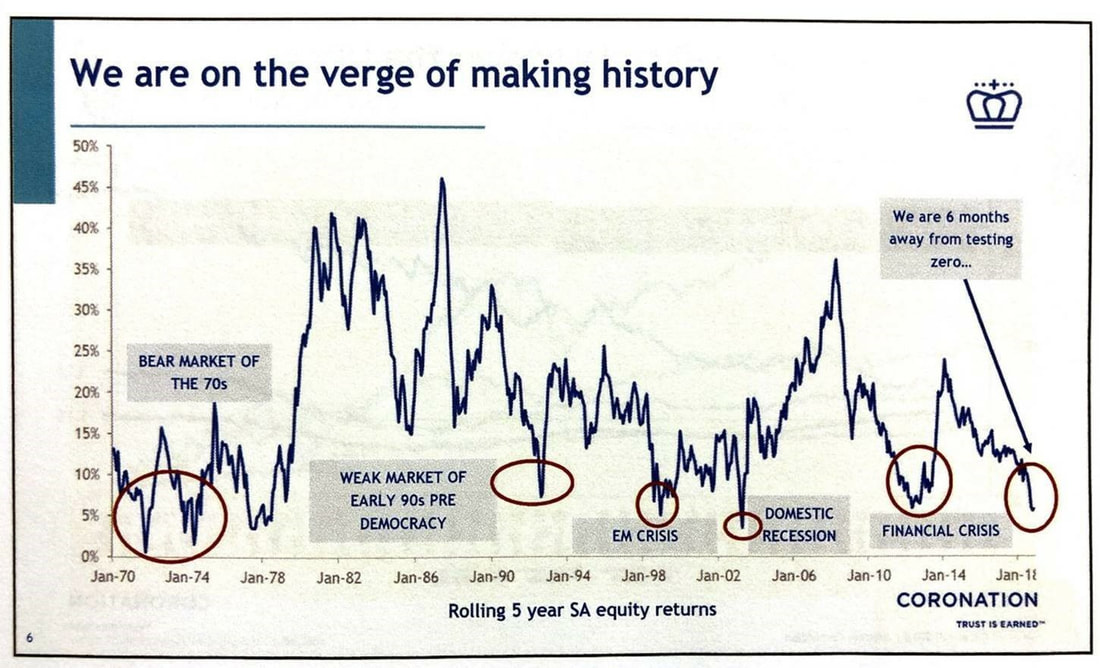

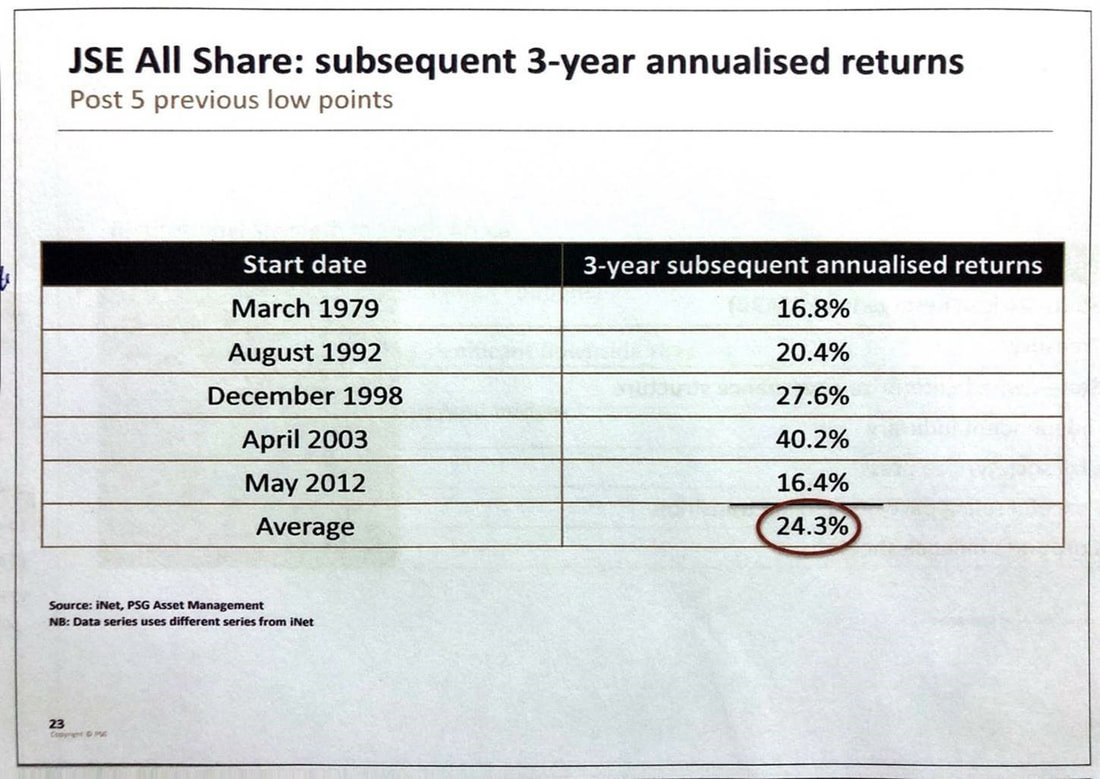

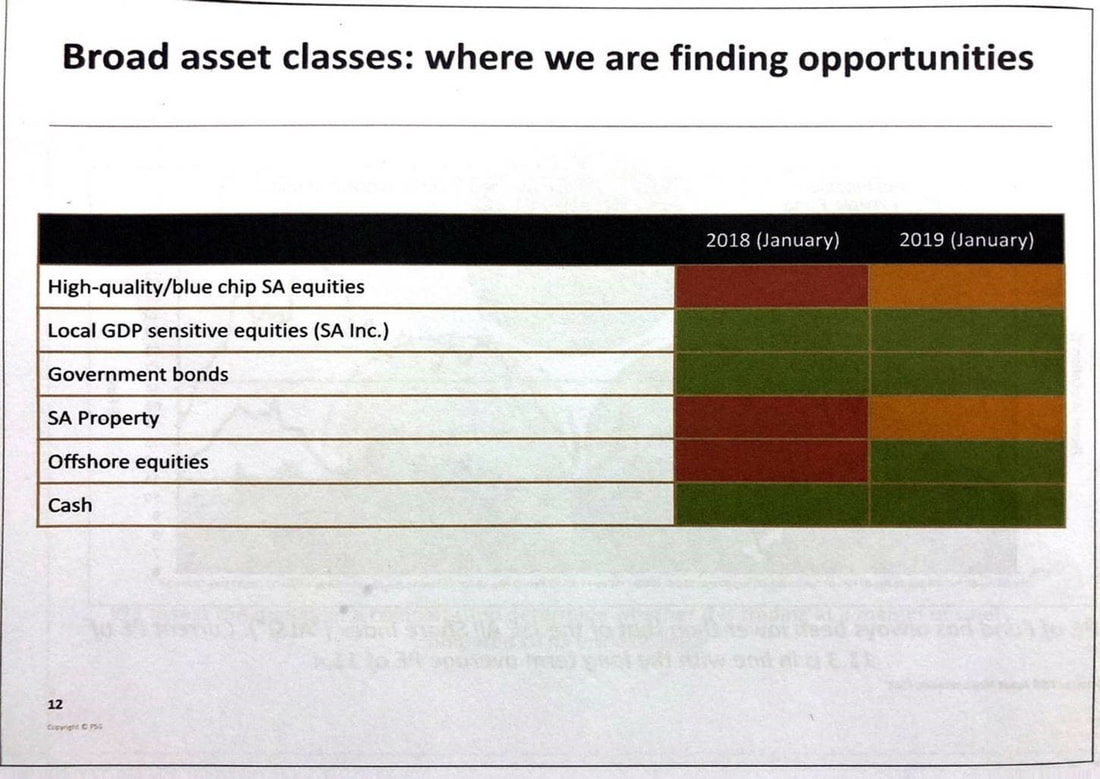

When compared to global markets, the Johannesburg Stock Exchange (JSE) is relatively small, comprising less than 1% of the total global investing universe. It is also highly concentrated, with the top 10 shares on the FTSE/JSE All Share Index (ALSI) making up between 50% and 60% of the index. In contrast, the top 10 shares in one of the world’s major indices, the S&P 500, make up just over 20% of the index. Most of the ALSI’s concentration comes from one share: technology giant Naspers, which makes up 20% of the index. Naspers’ dominance in recent years has increased concentration risk for investors, making portfolios overly sensitive to the factors that drive its value. In general, most investors are happy to contend with the exposure, as long as they are still generating positive returns. But what happens when the proverbial goose stops laying the golden eggs; when the dominant share(s) in your portfolio begins to perform poorly? How you can mitigate your concentration risk As famously stated by American economist Harry Markowitz, who received a Nobel Memorial Prize in Economic Sciences: “Diversification is the only free lunch in finance.” The best way to reduce your concentration risk, without losing out on the potential to earn good returns, is to make sure that you are invested in a combination of assets that have little correlation to one another – essentially, having a diversified portfolio where you generate returns from a wider spread of assets, industries and markets with an acceptable level of risk. To construct a diversified portfolio, one has to consider correlation and volatility. Correlation measures the strength of the relationship between the returns of two assets. A positive correlation indicates a strong positive relationship, i.e. the two assets tend to have higher and lower returns at the same time – this is indicative of an undiversified portfolio. A negative correlation implies the opposite, i.e. returns of the two assets move in opposite directions at any given time. A correlation of zero implies that no relationship (positive or negative) exists between the returns of the two assets. By adding assets with zero, or negative correlation, a portfolio becomes more diversified. You should also look at the overall volatility of your investment to gauge how well your portfolio is diversified. Intuitively, a portfolio consisting of correlated assets should show a larger deviation in its overall returns (i.e. high volatility), while a portfolio that has uncorrelated or negatively correlated assets should show smaller deviations in its overall returns (i.e. low volatility). In essence, if you have a well-diversified portfolio, then your investment should generate returns at lower levels of volatility over the long term. Diversify your portfolio If all this sounds very complicated, you could consider investing in a balanced fund. These are available both locally and internationally and offer a good solution to those investors who want to create a diversified portfolio without the hassle. Your chosen investment manager will carefully select a basket of uncorrelated assets from different markets, companies and industries to ensure that you generate good returns with minimal concentration risk. Local balanced funds offer South African investors some offshore diversification, but remember that Regulation 28 of the Pension Funds Act limits their foreign asset allocation to a maximum of 30% of the fund, with an additional 10% for investments in Africa outside of South Africa. This may not be enough offshore exposure for your needs – in which case you can also invest directly with offshore fund managers of your choice or through an offshore platform, such as the one Allan Gray offers. Every South African resident can use up to R11 million offshore for all foreign expenditure including travel, foreign exchange and for investing purposes. The first R1 million, called the single discretionary allowance, can be used without having to obtain permission from the South African Revenue Services (SARS) and the Reserve Bank. If you want to spend above this allowance, up to R10 million, you would need to get a tax clearance certificate from SARS. To further diversify, many investors choose to invest in more than one of the same type of fund from different managers. If you go this route, it is important to check that the underlying investments are different; otherwise, the combined weighting of the duplicate shares may increase your portfolio’s concentration. Building a diversified portfolio can be complicated and requires a solid understanding of markets and companies. But the good news is that you don’t have to go at it alone. An independent financial adviser (IFA) can help you assess the concentration risk in your portfolio and advise accordingly. It can be tempting to ignore concentration risk when the going is good, and returns are attractive. However, an undiversified portfolio can quickly become a problem if your most concentrated shares begin to perform poorly. Source: Vuyo Nogantshi , Allan Gray Summary The US-China trade war that began more than a year ago has been hurting the economy and trade of the two largest economies of the world, while also disrupting and re-shuffling the global supply chain. In addition, the United States hiked interest rates four times last year, increasing the rate to 2.25%, attracting funds back to the United States, first hitting emerging markets, and then hitting the US stock market. The US stock market had the second worst rate of return in December in the past 100 years (-7.8%). The South African asset management companies that I rate highly agree that the South African stock market and global emerging markets are at or near historical lows, and many good investment opportunities are found at this stage. We recommended long-term investors to continue to have exposure to growth (stock) assets, which could provide a 60% return over the next three years. *** Global The US-China trade war has been more than a year since the US declared it last year. President Trump of the United States believes that China was competing unfairly. The US trade deficit with China is huge and continues to expand. China infringes on intellectual property rights, as well as providing subsidies to public and private companies. Sanctions include imposing 10% tariffs on imported products from China, lawsuits and measures against ZTE, Huawei and other Chinese telecommunications companies, and containing Chinese companies in the 5G sector. From the recent statistics on Chinese economic growth and import and export volume, China’s exports in February fell by 20.7% from the previous year to US$135 billion, the largest decline since February 2016, indicating that the US-China trade war is having a significant negative impact on China. China's stock market fell 25% in 2018, but since the start of 2019, China's stock market has risen by 25% due to the recovery of global investor confidence and the Chinese government's monetary easing. In 2018, the US stock market was steadily rising, until it experienced a sharp 7.8% drop in December and a 6.1% decline over the year, the first annual negative rate of return since the 2008 global financial crisis. However, it has risen 11.48% since the beginning of this year. South Africa After Cyril Ramaphosa was sworn in as new president at the beginning of last year, there were high expectations from all sectors, which was termed Ramaphoria. However, the US-China trade war, the emerging market currency crisis, the ANC party’s two-faction fighting have caused the high spirits to evaporate quickly. The successive commissions of inquiry have opened up the lid on the rampant corruption and briberies during the Zuma era, so now we know that the National Treasury was hollowed out, and the infrastructure is crumbling. Eskom frequently broadcasts news of mismanagement, energy crisis and implements load shedding, which darkens investor confidence. South Africa’s economic growth rate last year is only 0.8%, and this year is not going to be any better due to the Eskom factor. South Africa's stock market fell 8.5% in 2018, the first annual negative rate of return since the 2008 global financial crisis. If former President Zuma sees the stock market return history, he will brag that, during his presidency, the stock market has risen every year and has never fallen! This is a bit ironic. South Africa's stock market has risen 6.3% since the beginning of this year. The four South African fund managers I rank most highly, based on my long-term observation, analysis and evaluation, agree that 2018 was a tough year for all investors: they lost money no matter where they put their money (except bank deposits and bonds). PSG pointed out that 2018 was a year of trying to avoid landmines:  In 2018, the following well-known listed companies have brought huge losses to investors.  The South African stock market is now near the bottom of the five troughs experienced over the past 40 years.  Coincidentally, Coronation also has the same analysis:  However, they also agreed that 2019 is a year of turnaround. The PSG research report pointed out that the annualized rate of return for the three years after the past five lows was as high as 24.3%, that is, the cumulative rate of return for three years was 92%. Even using the lowest annualized return rate of 16.4%, the investor's 3-year cumulative return would reached nearly 60%. This is the so-called reversion to the mean. Even if the South African economy does not do much, by going from the bottom of a market cycle to the average of a market cycle, with a little boost of investor confidence, the investors could receive this kind of return.  PSG Asset Management is currently positive on the following asset classes (marked by green): South African domestically focused stocks, government bonds, overseas stocks and cash.  Even though 2018 was a disappointing year for investment returns, we recommend investors not to give up on the stock market; continue to hold stock positions in the medium and long term, with exposure to South Africa and offshore markets. Allocate positions in shares, bonds and cash. During this trying time, I chose this pearl of wisdom from Warren Buffett to remind myself and investors:

Now is not the time to give up; it is probably the best investment opportunity since the 2008 global financial crisis.  You’re looking for somewhere to invest. You have decided what types of collective investments you want to be in (which are appropriate to your circumstances), and must now decide on asset managers that you believe will do the best job for you.

This is not a decision to be taken lightly, and an experienced, independent financial adviser would help you enormously. Two investment experts, Prasheen Singh, a director and consultant at investment consultancy RisCura, and Rory Maguire, the managing director of British investment consultancy Fundhouse, offer the following advice. (For clarity, the unit trust management company is referred to as the “asset manager” and the person managing the fund the “fund manager”.) 1. Do your research Singh says, given the wealth of information available today, you can do your own research. “Visit the asset managers’ websites and compare the fund fact sheets (or ‘minimum disclosure documents’) of the funds you’re considering. Ensure you understand the risk profile of the portfolio and the mix of asset classes.” Also research the company, fund manager and fund on websites apart from the company’s own to get a balanced picture. 2. Find a company you can trust Speaking at the recent Allan Gray Investment Summit, Maguire says: “Asset managers are stewards of your capital. It’s important that they understand that the money they manage is yours – there must be trust.” There are a number of things you can check for: The business structure must allow for a long-term view, without shareholders pressurising the company to chase short-term earnings. Privately owned companies and family- or staff-owned companies tend to do better in this respect, Maguire says. Be cautious of large funds and companies with many funds. “Asset managers get paid on the size of assets that they manage. A large fund can constrain a manager by being less liquid and less able to access smaller companies,” he says. “So look out for asset managers with limited capacity. It’s frustrating when an asset manager closes a fund to new investment. As hard as that is, it is telling you that they are putting their profits second to your returns.” There must be honesty and transparency. “Look for honesty, clarity, someone who admits mistakes. Avoid managers who are obfuscating and put catch-phrases and jargon in front of you to throw you off the scent,” Maguire says. Singh agrees: “Good fund managers should be able to explain their approach and how they intend to achieve their objectives in a manner that makes sense, even to a novice investor.” Fund managers who have their own money in their funds have a higher success rate than those who don’t, Maguire says. “They are going to care more and try harder. They have to eat their own cooking.” 3. Look for good-quality people Maguire says there must be consistency in how the fund is managed, and this comes through a stable, professional team. The key things to look for are: Passion. Experience. Differences of opinion. “Look out for companies that may be employing similarly-minded people. You get better answers through disagreements and proper debate,” Maguire says. The quality of the people behind the scenes. Employer of choice. “It’s a poor indicator if a company is losing people to its competitors. You want to be attracting good people and retaining them for fairly long periods,” Maguire says. Temperament. “Managers that add value to your portfolio are those that take different views to the market. But to do that requires the right temperament, which is a very hard thing to pinpoint. However, negative temperament is quite easy to spot. When you get defensive, ego-based answers to performance dips, be careful.” 4. The investment process must be consistent Asset managers employ different investment styles: some focus on value (assets at below-average prices), others more on quality (how well a company is run, its profitability, and its prospects), and others on growth (young, progressive companies with the potential to grow exponentially). Whatever the style, the company must be consistent in its investment process, which should counteract the human biases that result in bad investment decisions. This process, Maguire says, must be fairly simple to understand and “must be implemented ruthlessly”. But it also needs to allow for differences of opinion. “We look for outliers, where fund managers are sticking their necks out. And the process needs to allow for that. When you look at a fund manager’s decisions and track record, those outlying moments are important to pin down.” 5. Look at the manager’s track record The two experts say you shouldn’t pay much attention to awards, although Singh says it may be worth looking at a fund that has consistently won awards over an extended period. Don’t forget, the person managing the fund may have changed since the fund's last award. If you are looking at past performance, which is no guarantee of future performance, Maguire says it’s worthless looking at anything less than five-year periods. “The top South African fund managers are quite consistent for five-year performance over long periods. Any shorter period is absolutely meaningless. There is nothing predictive to be gained by looking at shorter than five years, and five years is slightly less predictive than 10,” he says. 6. Consider fees in context All management fees should be clearly stated on the fund’s minimum disclosure document, and these may include a performance fee. Singh says the lower the risk for the fund, the lower the fee should be. For example, a cash fund will have lower fees than an equity fund because it is lower risk. “Remember that fees represent the type of product, not the quality of the product. Higher fees are not an indicator of better quality in the investment world.” Importantly, make sure you understand the total investment cost, which may include advice fees, Singh says. 7. Be patient It’s essential that once you have made your choice, you stick to it. “It takes time for a fund to achieve its objectives – typically between three and five years,” Singh says. “There will be periods when the fund’s strategy is out of favour, and that’s okay. You need to consider it in a long-term context and understand how and why the strategy that is out of favour today can make a comeback in a few years’ time.” Written by: Martin Hesse Source: Personal Finance  Coronation Strategic Income Fund: Conservative fund for short term investors requiring an immediate income.

What is the fund’s objective? Strategic Income aims to achieve a higher return than a traditional money market or pure income fund. What does the fund invest in? Strategic Income can invest in a wide variety of assets, such as cash, government and corporate bonds, inflation-linked bonds and listed property, both in South Africa and internationally. As great care is taken to protect the fund against loss, Strategic Income does not invest in ordinary shares and its combined exposure to locally listed property (typically max. 10%), local preference shares (typically max. 10%), local hybrid instruments (typically max. 5%) and international assets (typically max. 10%) would generally not exceed 25% of the fund. The fund has a flexible mandate with no prescribed maturity or duration limits for its investments. The fund is mandated to use derivative instruments for efficient portfolio management purposes. Who should consider investing in the fund? Investors who are looking for an intelligent alternative to cash or bank deposits over periods from 12 to 36 months; seek managed exposure to income generating investments; are believers in the benefits of active management within the fixed interest universe. What costs can i expect to pay? An annual fee of 0.85% (excl. VAT) is payable. Fund expenses that are incurred in the fund include trading, custody and audit charges. All performance information is disclosed after deducting all fees and other fund costs. We do not charge fees to access or withdraw from the fund. How long should investors remain invested? The recommended investment term is 12-months and longer. The fund’s exposure to growth assets like listed property and preference shares will cause price fluctuations from day to day, making it unsuitable as an alternative to a money market fund over very short investment horizons (12- months and shorter). Note that the fund is also less likely to outperform money market funds in a rising interest rate environment. Given its limited exposure to growth assets, the fund is not suited for investment terms of longer than five years. Source: Coronation  What is the fund’s objective? The Fund aims to create long-term wealth for investors within the constraints governing retirement funds. It aims to outperform the average return of similar funds without assuming any more risk. The Fund’s benchmark is the market value-weighted average return of funds in the South African – Multi Asset – High Equity category (excluding Allan Gray funds)

Fund description and summary of investment policy? The Fund invests in a mix of shares, bonds, property, commodities and cash. The Fund can invest a maximum of 30% offshore, with an additional 10% allowed for investments in Africa outside of South Africa. The Fund typically invests the bulk of its foreign allowance in a mix of funds managed by Orbis Investment Management Limited, our offshore investment partner. The maximum net equity exposure of the Fund is 75% and we may use exchange-traded derivative contracts on stock market indices to reduce net equity exposure from time to time. The Fund is managed to comply with the investment limits governing retirement funds. Returns are likely to be less volatile than those of an equity-only fund Suitable for those investors who:

For each percentage of two-year performance above or below the benchmark Allan Gray may add or deduct 0.1%, subject to the following limits:

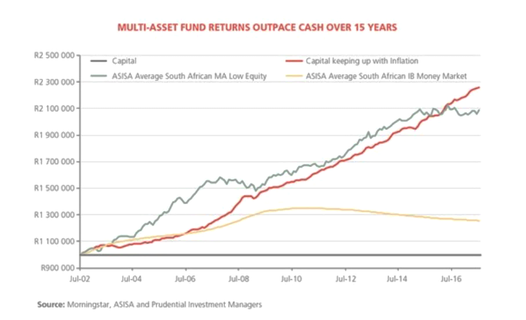

Source: Allan Gray  After three years of low equity returns, investors drawing an income from their investments may be considering shifting some of their portfolio exposure away from multi-asset funds with equity exposure towards cash. However, the appropriate time for switching - if there ever was any - has passed, and retirees are in danger of eroding the longer-term value of their retirement capital should they switch now. This trend towards cash has been evident in South Africa over the past year in the wake of the higher returns (of around 7.0% p.a.) offered by bank deposits and money market funds compared to riskier equity holdings. Poor equity performance has dragged down the returns of well-diversified multi-asset funds in which many retirees are invested: the average ASISA low-equity multi-asset fund delivered only 6.3% p.a. over the three years to 31 July 2017, and the average ASISA high-equity multi-asset fund (the typical “balanced” fund) returned only 5.5% p.a. over the same period, according to Morningstar. Compare these returns with those of the past 15 years, where high-equity fund returns averaged 12.5% p.a., and low-equity funds averaged 10.0% p.a. The longer-term performances are in line with the funds’ generally accepted return targets of inflation + 4% for the less aggressive low-equity category, and inflation + 6% for the more aggressive high-equity category, with long-term inflation at approximately 6%.  Given their recent under performance, retirees dependent on income from multi-asset funds may think that they will benefit by moving to cash now. However, they would be getting their timing wrong by being too late. Current valuations show that prospective returns from multi-asset funds are higher than those from cash assets. So by moving to cash now, retirees will be exposed to falling cash returns in future (the SARB has already started cutting short-term interest rates), and will miss out on any improvement in returns from multi-asset funds.

The accompanying graph shows how a R1.0 million retirement investment has performed over the past 15 years (July 2002-July 2017), starting with a 5% annual drawdown and escalating the drawdown by inflation, when invested in different funds. The initial capital investment is represented by the fixed black line. In order to have maintained its real value over time, it would have needed to grow at a rate equal to inflation, to R2.26 million (as shown by the red line). Would a money market investment have given the retiree an adequate return over the 15 years? Clearly not: the yellow line in the graph depicts how the R1.0 million would have performed invested in the average South African money market fund (the ASISA IB Money Market category) while drawing the income over the period. Due to its low return, the capital would have grown to only R1.25 million. Although it would have successfully given the retiree their income (totalling R1.1 million), the real value of the retiree’s capital would have been significantly eroded (shown by the gap between the red and gold lines). By contrast, an investment in the average low-equity multi-asset fund is shown by the green line. Although the fund return varies over time, it manages to outperform or remain in line with the inflation requirement (red line) for much of the period. Its more recent underperformance is partly compensated by the earlier excess performance. The retiree ends up with R2.09 million, while also having drawn down R1.1 million in income payments over the 15 years. From this evidence, it is clear that multi-asset funds have been delivering the returns they are expected to over longer periods, and investors, especially retirees, need to think twice before moving away from them. Anyone switching to cash now is likely getting the timing wrong – they will receive lower returns over the longer term (as the graph demonstrates), or if they plan to switch back to multi-asset funds later, they will also likely mistime their move. To set up an appointment with our Financial Planners, please contact Kevin, email: invest@daberistic.com tel no: (011 658-1333) Written: Pieter Hugo Source: Prudential |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|